The Balance of Payments (BOP) is one of the most comprehensive economic indicators a country possesses. It records every transaction between residents and the rest of the world, covering trade in goods and services, cross‑border investment income, and financial transfers. When the BOP is in equilibrium, a nation can finance its external obligations without resorting to emergency measures. When disequilibrium strikes, it can trigger currency crises, deplete foreign reserves, and force painful policy adjustments.

Despite its importance, the Balance of Payments is frequently misunderstood. Many people equate “balance of payments” only with the trade balance, ignoring the capital and financial accounts that often determine whether a country can sustain its deficits. This article provides a deep dive into the equilibrium and disequilibrium in the balance of payments, exploring the underlying causes of imbalances and the policy toolkit available to restore stability. By the end, you will understand why even advanced economies, such as the United States, Singapore, and the United Kingdom, constantly monitor their BOP, and how emerging markets like Pakistan and India have navigated recurring pressures.

What Is Equilibrium in the Balance of Payments?

Equilibrium in the Balance of Payments is a state where a country’s total receipts from the rest of the world equal its total payments over a given period, typically one year. In accounting terms, the BOP always balances in the sense that every transaction is recorded twice (once as a credit and once as a debit). However, when economists speak of “equilibrium,” they refer to a situation where there are no undesired changes in official reserve assets.

- Autonomous transactions (those driven by profit, consumption, or investment motives) are roughly balanced.

- Accommodating transactions (official interventions to finance a surplus or deficit) are minimal.

In practice, equilibrium means a country does not experience a persistent drain on its foreign exchange reserves nor an excessive accumulation that distorts the domestic money supply. It implies that the exchange rate is at a sustainable level, and the economy can meet its external obligations without disruptive policy shifts.

Why Equilibrium Is Rare

Global trade and finance are inherently volatile. Terms of trade shift, investor sentiment changes overnight, and natural disasters or geopolitical events can alter a country’s external position within months. Therefore, the Balance of Payments is more often in a state of disequilibrium, either a deficit or a surplus. The key question is whether that disequilibrium is temporary or structural.

Understanding Disequilibrium

Disequilibrium occurs when autonomous receipts do not equal autonomous payments. This manifests as either a Balance of Payments deficit or a Balance of Payments surplus.

| Type | Definition | Common Characteristics |

|---|---|---|

| BOP Deficit | Total payments > total receipts |

|

| BOP Surplus | Total receipts > total payments |

|

|

||

A deficit is often viewed negatively because it signals that a country is living beyond its means internationally. However, temporary deficits can be healthy if they finance investments that boost future export capacity. Conversely, a persistent surplus can distort global trade balances and may indicate that a country is relying too heavily on exports while suppressing domestic consumption.

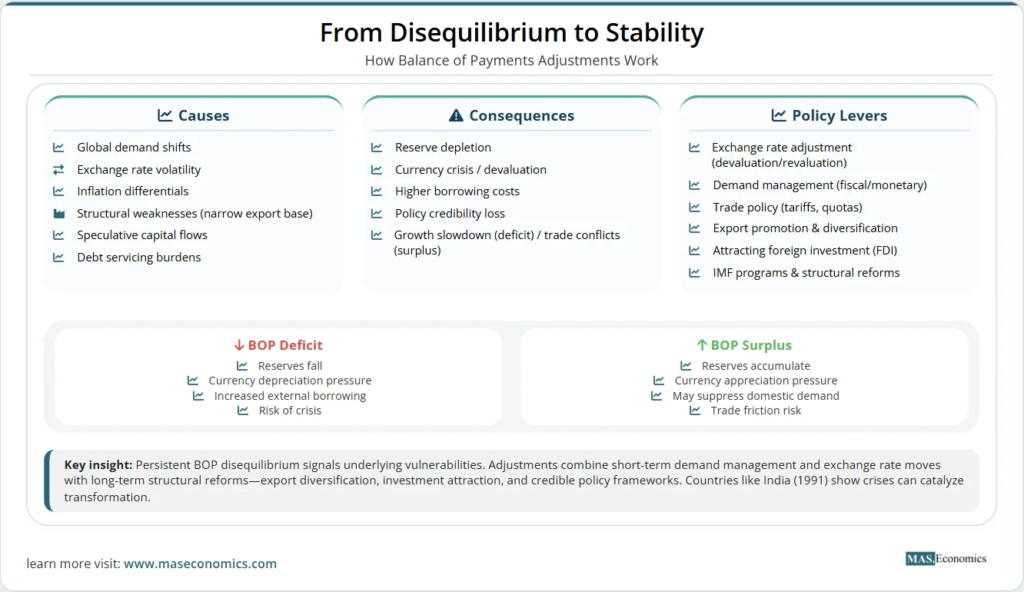

Key Causes of BOP Disequilibrium

Global Demand Shifts

A country’s export earnings are directly tied to the economic health of its trading partners. When global demand for a major export commodity collapses, for example, oil, textiles, or IT services, the current account quickly deteriorates.

Example: During the 2008–2009 global financial crisis, many emerging economies saw export revenues drop by over 20%, pushing their BOP into deficit despite stable domestic policies.

Exchange Rate Volatility

Exchange rates directly influence the relative prices of exports and imports.

- Overvalued currency: Makes exports expensive abroad and imports cheap at home. This tends to widen the trade deficit.

- Undervalued currency: Boosts exports but can lead to inflationary pressures and trade friction with partners.

When the exchange rate is not market‑determined (e.g., a rigid peg), imbalances can accumulate until a speculative attack forces a devaluation.

Inflation Differentials

If a country’s inflation rate consistently exceeds that of its trading partners, its goods become less competitive. Export growth slows while imports become relatively more attractive. This “real exchange rate appreciation” can erode the current account even if the nominal exchange rate remains stable.

Structural Weaknesses

Some economies suffer from chronic BOP deficits because of deep‑rooted structural issues:

- Narrow export base: Reliance on one or two commodities (e.g., cotton, copper) makes the BOP vulnerable to price swings.

- Low value‑added production: Inability to move up the global value chain keeps export earnings low.

- Inadequate infrastructure: Poor transport or energy supply raises production costs, hurting competitiveness.

Structural disequilibrium cannot be fixed by exchange rate adjustments alone; it requires long‑term investment and reforms.

Speculative Capital Flows

The capital account has become as important as the current account. Sudden reversals of portfolio investment, often triggered by interest rate changes in advanced economies or political uncertainty, can create BOP crises. This phenomenon, known as “sudden stop,” has been documented in numerous emerging markets (e.g., the 1997 Asian financial crisis).

Debt Servicing Burdens

For heavily indebted countries, the BOP must accommodate interest and principal payments on external debt. If debt service exceeds new inflows, the current account may show a deficit even if the trade balance is neutral. This is a particular challenge for low‑income countries that borrowed heavily during periods of low global interest rates.

Consequences of Persistent Imbalances

Left uncorrected, prolonged BOP disequilibrium can have severe economic consequences:

- Reserve depletion: Central banks may be forced to use scarce foreign reserves to defend the currency, leaving the country vulnerable to shocks.

- Currency crisis: A loss of confidence can lead to rapid devaluation, increasing the cost of imports and fueling inflation.

- Higher borrowing costs: International credit rating agencies downgrade countries with chronic deficits, raising the cost of new debt.

- Policy credibility loss: Persistent imbalances may force a country into an IMF program, which often comes with strict conditionality that can be politically unpopular.

Even surpluses can be problematic if they arise from artificially low exchange rates or protectionism. They can lead to trade conflicts and may indicate that domestic demand is being suppressed, reducing the standard of living.

Policy Solutions to Restore Balance

Restoring BOP equilibrium requires a mix of expenditure‑switching and expenditure‑reducing policies. Below are the most common tools used by policymakers.

Exchange Rate Adjustments

Devaluation (or depreciation) is the classic remedy for a BOP deficit. It makes exports cheaper and imports more expensive, encouraging a shift in domestic and foreign spending. However, success depends on the Marshall‑Lerner condition: the combined price elasticities of demand for exports and imports must exceed one for devaluation to improve the trade balance.

For countries with a surplus, revaluation can help rebalance by making exports costlier and imports cheaper.

The effectiveness of exchange rate adjustments often depends on the degree of capital mobility and the monetary policy framework—a relationship formally captured by the Mundell‑Fleming model.

Demand‑Management Policies

Monetary and fiscal tools can reduce aggregate demand, thereby curbing import demand.

- Contractionary fiscal policy: Reducing government spending or raising taxes lowers overall expenditure, including spending on imports.

- Contractionary monetary policy: Higher interest rates discourage borrowing and consumption, again reducing import demand. It also attracts short‑term capital flows, which can temporarily finance a deficit.

These measures are effective in the short run but may come at the cost of slower growth and higher unemployment.

Trade Policy Interventions

Tariffs, quotas, and import licensing can quickly reduce the import bill. However, they risk retaliation from trading partners and may violate World Trade Organization (WTO) commitments. They also raise costs for domestic industries that rely on imported inputs.

Export Promotion and Diversification

Sustainable equilibrium requires expanding export capacity. Strategies include:

- Export subsidies (subject to WTO rules)

- Improving trade logistics and reducing border delays

- Diversifying export products and markets to reduce vulnerability to demand shocks

- Investing in quality and certification to meet international standards

Attracting Foreign Investment

Foreign direct investment (FDI) and long‑term portfolio flows can finance a current account deficit without adding to external debt. Countries often offer tax incentives, special economic zones, and regulatory reforms to attract such flows. Unlike short‑term speculative capital, FDI is generally more stable and contributes to technology transfer.

Global Perspectives

Different countries experience BOP dynamics in ways that reflect their unique economic structures, currency roles, and policy frameworks. Examining three advanced economies, the United States, Singapore, and the United Kingdom, reveals that equilibrium is not a one‑size‑fits‑all concept.

United States: The “Exorbitant Privilege”

The United States has run persistent current account deficits for decades. In 2026, that deficit is estimated at $800 billion, roughly unchanged from previous years. Yet unlike most countries, the US does not face the usual constraints. Because the dollar is the world’s primary reserve currency, foreign central banks, investors, and corporations willingly hold US assets, effectively lending to the US at very low cost. This “exorbitant privilege” allows the US to finance its deficit without the currency crises that would otherwise follow.

That privilege, however, is not unlimited. The IMF’s April 2026 forecast downgraded US growth to 1.8%, citing trade tensions and policy uncertainty. Core inflation has eased to 2.5%, close to the Fed’s target, and the policy rate remains at 3.625%, a level that still attracts foreign capital but also reflects a balancing act. If fiscal deficits continue to widen, even the dollar’s special status could eventually be tested. For now, the US illustrates how a country can sustain a large structural deficit when its currency is the global anchor.

For the latest economic data on the United States, visit our country profile page.

Singapore: Surplus as a Deliberate Strategy

Singapore offers the opposite picture: a consistent current account surplus, projected at $80 billion in 2026. This surplus is not accidental. Singapore deliberately runs a trade surplus by focusing on high‑value electronics, chemicals, and financial services, and it manages its exchange rate as the primary tool of monetary policy. The Monetary Authority of Singapore allows the Singapore dollar to appreciate gradually against a trade‑weighted basket, which helps keep inflation low, just 1.2% as of February 2026.

With $360 billion in foreign reserves, Singapore’s surpluses are channelled into two sovereign wealth funds (GIC and Temasek), which invest globally and generate long‑term returns. The city‑state demonstrates that a BOP surplus, when managed transparently, can be a source of national wealth rather than a distortion.

For the latest economic data on Singapore, visit our country profile page.

United Kingdom: Services Strength, Goods Weakness

The UK’s BOP reflects its post‑Brexit economic structure. Goods trade has suffered from new barriers with the EU, while services, especially financial, legal, and consulting, remain strong. The resulting current account deficit widened to an estimated $200 billion in 2026. London’s role as a global financial hub, however, means the financial account typically attracts enough inflows to cover the deficit.

The Bank of England’s policy rate stands at 4.5%, a level that has helped bring inflation down to 3.1%. The pound has stabilised around 0.75 GBP/USD, a far cry from the volatility seen after the 2022 mini‑budget. The UK’s experience shows that a deficit can be sustainable if it is financed by stable, long‑term capital flows, but also that confidence can shift quickly when policy signals are mixed.

For the latest economic data on the United Kingdom, visit our country profile page.

Case Study: Pakistan’s Ongoing BOP Challenges

Pakistan’s recent history illustrates the high cost of structural vulnerabilities. In the 2022–2023 crisis, the country saw reserves plummet, inflation spike to 29%, and the rupee lose nearly half its value. By 2026, thanks to a $3 billion IMF Stand‑By Arrangement and painful policy adjustments, the situation has stabilised. Inflation fell to 7.0%, reserves recovered to $20.9 billion, and the rupee held steady around 279 PKR/USD.

Yet the underlying challenges remain. The current account is still in deficit (around $2.8 billion in USD terms), and the export base is narrowly concentrated in textiles. Pakistan’s case reinforces a key theme of this article: short‑term fixes can restore stability, but a durable equilibrium requires structural reforms, export diversification, energy sector improvement, and consistent policy frameworks.

For the latest economic data on Pakistan, visit our country profile page.

Case Study: India’s 1991 Balance of Payments Crisis

India’s 1991 crisis is the classic example of a BOP emergency that triggered deep reform. At the time, reserves covered barely two weeks of imports, and the country was on the brink of default. The response, devaluation, liberalisation, and opening to FDI, laid the foundation for a dramatic transformation.

Today, India’s external position is unrecognisable from that era. Foreign exchange reserves stand at a record $620 billion, the current account deficit is a manageable $200 billion (roughly 1.5% of GDP), and growth is projected at 6.5% for FY2026. The rupee has depreciated only gradually, reflecting strong capital inflows and a diversified export base that includes IT services, pharmaceuticals, and engineering goods. India’s journey shows that a BOP crisis, while painful, can become a catalyst for building lasting resilience.

For the latest economic data on India, visit our country profile page.

Conclusion

Equilibrium in the Balance of Payments is more than an accounting concept; it is a reflection of a country’s ability to sustain its economic model without external distress. Persistent disequilibrium, whether deficit or surplus, signals underlying vulnerabilities that can eventually force disruptive adjustments.

The tools to manage BOP imbalances range from short‑term demand management and exchange rate moves to long‑term structural reforms. Countries as diverse as the United States, Singapore, and the United Kingdom show that even advanced economies must constantly monitor their external balances. Meanwhile, the experiences of Pakistan and India demonstrate that while crises are painful, they can also spur necessary policy changes. For any economy, regular monitoring of BOP components, especially the current account, capital flows, and reserve levels, is essential to anticipate problems before they become emergencies.

FAQs:

What is equilibrium in the Balance of Payments (BOP)?

Equilibrium in the Balance of Payments occurs when a country’s total financial inflows match its total outflows over a given period, indicating balanced economic transactions without significant accumulation or depletion of foreign reserves.

What causes disequilibrium in the Balance of Payments?

Disequilibrium arises when total payments to foreign entities do not equal total receipts, leading to a deficit (outflows exceeding inflows) or a surplus (inflows exceeding outflows). Common causes include changes in global demand, exchange rate fluctuations, inflation differences, structural economic issues, and speculative capital movements.

How does a BOP deficit impact a country’s economy?

A BOP deficit depletes foreign reserves as the country pays more to foreign entities than it earns. Persistent deficits may lead to reliance on foreign borrowing, currency devaluation, or corrective policy measures to restore balance.

What factors contribute to a BOP surplus?

A BOP surplus occurs when a country’s foreign currency inflows exceed its outflows, often due to high export revenues, an undervalued currency boosting exports, or large inflows from foreign investments. While beneficial in the short term, persistent surpluses can indicate over-reliance on exports or restrained domestic consumption.

How do exchange rate changes influence BOP disequilibrium?

An overvalued currency makes exports more expensive and imports cheaper, worsening a BOP deficit. Conversely, an undervalued currency boosts exports by making them more competitive internationally, potentially leading to a surplus.

Why is inflation a critical factor in BOP imbalances?

Higher domestic inflation reduces export competitiveness by making goods more expensive for foreign buyers. It also encourages cheaper imports, leading to a BOP deficit as imports exceed exports.

What strategies can correct a BOP deficit?

Exchange rate adjustments, such as currency devaluation, encourage exports and reduce imports. Fiscal and monetary tightening can manage domestic demand, while import restrictions and export promotion strategies can directly address imbalances by altering trade flows.

How does export promotion help achieve BOP equilibrium?

Export promotion increases foreign currency inflows by improving product competitiveness and finding new markets. Diversification of exports can reduce dependency on a narrow range of goods, stabilizing the current account and supporting overall BOP equilibrium.

Thanks for reading! Share this with friends and spread the knowledge if you found it helpful.

Happy learning with MASEconomics