Welcome to MASEconomics, your go-to source for insightful analysis of economic developments. In this in-depth examination, we dissect the most recent Monetary Policy Statement released by the State Bank of Pakistan on September 14, 2023. Our goal is to break down the essential points, provide insights, and present a clear understanding of Pakistan’s current economic situation, monetary policy decisions, and their potential impacts.

Let’s dive in to break down essential points.

Key Monetary Policy Decision

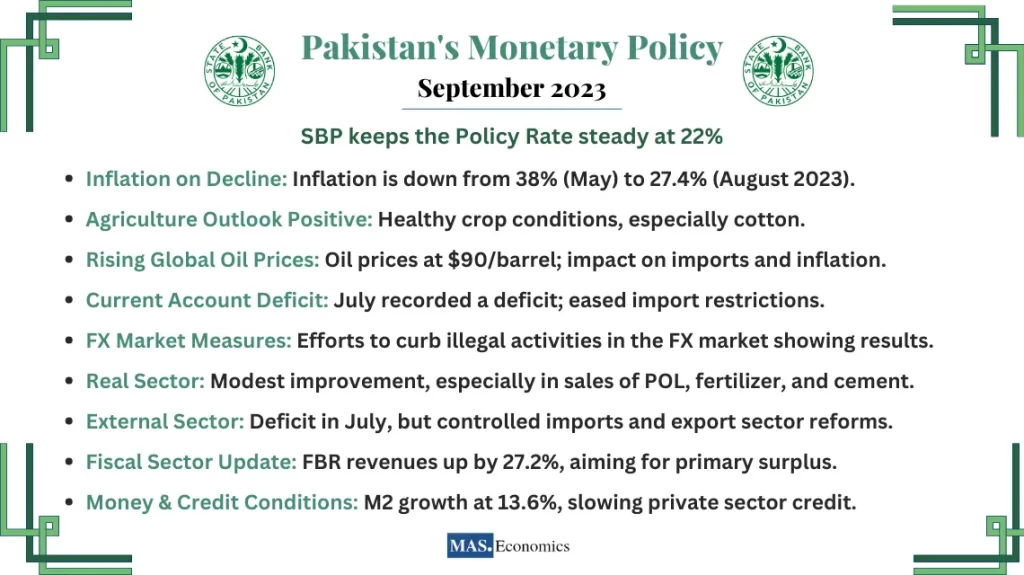

Policy Rate Maintained at 22 Percent: The Monetary Policy Committee (MPC) decided to maintain the policy rate at 22 percent in its latest meeting. This decision aligns with their assessment of the ongoing decline in inflation rates, which dropped from 38 percent in May to 27.4 percent in August 2023. Despite recent increases in global oil prices, the committee anticipates a continued downward trajectory of inflation, particularly in the year’s second half. This decision ensures that real interest rates remain favorable, supporting price stability. Additionally, improvements in agriculture output and measures to curb speculative activity in FX and commodity markets contribute positively to the inflation outlook.

The decision to maintain the policy rate at 22 percent is prudent, given the delicate balance between curbing inflation and fostering economic growth. This approach acknowledges the positive trajectory in agriculture and measures to mitigate speculative activities, which contribute favorably to inflation prospects.

Key Developments Since July

Four Significant Changes Highlighted:

- Agriculture Outlook: Positive agricultural developments are evident, with data on cotton arrivals, favorable input conditions, and satellite data indicating healthy vegetation for other crops.

- Global Oil Prices: Oil prices have risen, currently hovering around $90/barrel, which could impact Pakistan’s import bill and inflation.

- Current Account Deficit: After four consecutive months of surplus, July recorded a current account deficit, influenced partly by eased import restrictions.

- Administrative and Regulatory Measures: Efforts to improve the availability of essential food commodities and curb illegal activities in the foreign exchange market have started to show results, narrowing the gap between interbank and open market exchange rates.

The assessment of critical developments underscores the multifaceted challenges Pakistan faces. While the positive agriculture outlook and efforts to stabilize essential commodities are encouraging, the shift from a current account surplus to a deficit highlights the need for sustainable strategies to bolster external accounts.

MPC’s Focus on Inflation and Fiscal Responsibility

The MPC remains vigilant in monitoring risks to the inflation outlook and is ready to take necessary actions to maintain price stability. Simultaneously, they emphasize the importance of maintaining a prudent fiscal stance to control aggregate demand. This fiscal prudence is crucial to achieving the medium-term target of 5-7 percent inflation by the end of FY25.

The MPC’s dual focus on inflation and fiscal responsibility is commendable. Striking the right balance between monetary and fiscal policies is essential for achieving sustained economic stability. Ensuring that fiscal measures align with the monetary policy objectives is a step in the right direction.

Real Sector Outlook

High-frequency indicators suggest a modest improvement in economic activity. Sales of critical inputs like POL, fertilizer, and cement have picked up moderately, with a slight increase in import volumes. The agriculture sector outlook has improved, with reduced concerns about floods and increased cotton arrivals. Domestic demand is expected to remain contained due to monetary tightening and fiscal consolidation, aligning with earlier moderate growth expectations.

The real sector outlook presents a mixed picture, with modest improvements in some areas. The challenge lies in sustaining this momentum and addressing structural issues to foster robust economic growth.

External Sector Assessment

After four surplus months, the current account balance recorded a deficit of $809 million in July 2023. Despite this, overall imports are projected to remain controlled due to favorable trends in non-oil commodity prices, moderate domestic demand, and improved cotton production. Structural reforms in exchange companies will enhance their governance and market functioning, supporting the export outlook.

Efforts to bolster the external sector’s resilience are commendable. Structural reforms in exchange companies can strengthen the country’s export capabilities, diversifying revenue sources.

Fiscal Sector Update

In the initial two months of FY24, FBR’s revenues increased by 27.2 percent compared to last year, reflecting fiscal measures and economic recovery. Achieving the targeted primary surplus of 0.4 percent of GDP is essential to support monetary policy’s price stability objective. Fiscal consolidation through broadening the tax base, targeted subsidies, and public sector enterprise reforms is vital for sustainable economic growth.

The fiscal sector update indicates progress, but challenges persist. Achieving a primary surplus is vital for maintaining price stability and economic sustainability. Ongoing efforts to broaden the tax base and reform public enterprises are steps in the right direction.

Money and Credit Conditions

As of September 1, M2 growth has decelerated to 13.6 percent year-on-year, primarily due to a slowdown in credit to the private sector. Fiscal consolidation, planned external inflows and economic activity upticks are expected to create room for moderate private-sector credit expansion this year.

Balancing money and credit conditions is a delicate task. The deceleration in M2 growth aligns with the need for controlled credit expansion while sustaining economic activity.

Inflation Outlook

CPI inflation declined to 27.4 percent in August, mainly due to moderation in food prices. However, the decline was slower than anticipated, mainly due to surging global oil prices and their impact on administered energy prices. Near-term inflation expectations have reversed, partly due to uncertainty in FX markets. Regulatory measures and law enforcement are expected to address supply constraints and illegal FX market activities, facilitating a downward inflation trajectory, especially in the year’s second half.

The inflation outlook is central to economic stability. Addressing supply constraints and curbing illegal FX market activities are crucial to achieving price stability.

Conclusion

Pakistan’s monetary policy is cautious, focusing on inflation control and fiscal responsibility while acknowledging positive developments in agriculture and the external sector. Monitoring the evolving economic landscape will be crucial in guiding future policy decisions.

Stay informed, stay ahead, and keep learning with MASEconomics!