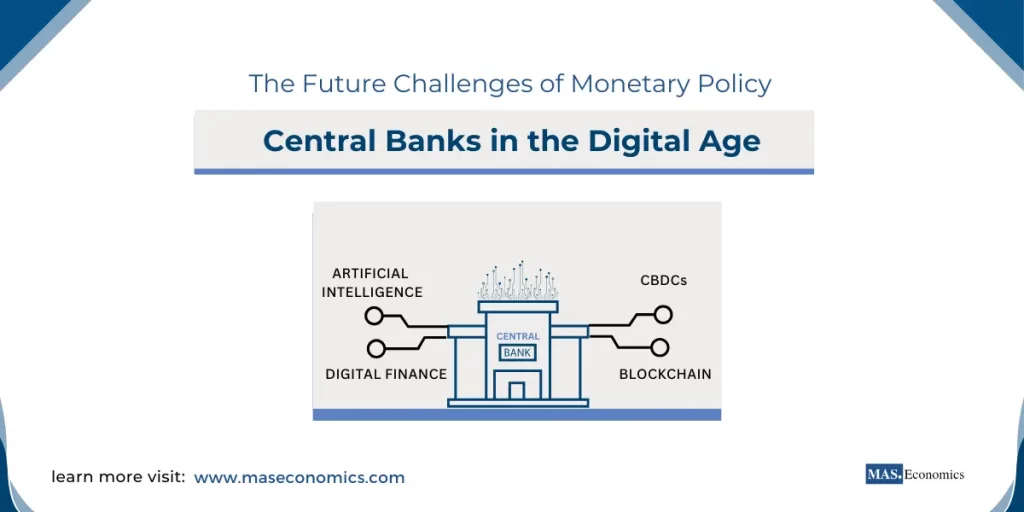

The digital revolution has transformed nearly every aspect of our lives, including central banking. Innovations like fintech, digital currencies, and advanced financial technologies are reshaping the environment in which central banks operate, presenting new challenges that demand fresh strategies and frameworks.

Central banks in the digital age must address the challenges of the digital age, focusing on how evolving technologies impact monetary stability and central bank independence. Key obstacles arise as central banks strive to maintain effective control over monetary policy in an increasingly digital world.

Digital Currencies

One of the most significant changes in recent years has been the development of central bank digital currencies (CBDCs). Central banks worldwide are assessing the feasibility of introducing digital versions of their currencies to complement physical cash and facilitate faster and more secure transactions. However, with this development come several challenges:

The Threat to Financial Intermediaries

The introduction of CBDCs has raised concerns about the potential disruption to commercial banking. If consumers prefer holding CBDCs instead of depositing money in traditional bank accounts, the intermediation role of banks could be severely compromised. This could affect the availability of credit, as banks might lose a key source of funding that they use to provide loans to businesses and individuals. Central banks, thus, need to balance the convenience of CBDCs while ensuring that the stability of financial intermediaries is not compromised.

Privacy Concerns and Data Security

CBDCs also introduce potential challenges related to privacy and data security. A central bank issuing digital currency would have to decide on the degree of anonymity allowed for transactions. On one end, ensuring a high level of anonymity could lead to money laundering and tax evasion risks. On the other hand, a system with reduced privacy could face resistance from the public due to fears of government surveillance. Central banks must, therefore, tread carefully, establishing robust data protection measures and a balanced approach to privacy to gain public trust.

The Rise of Fintech and the Erosion of Monetary Policy Control

Fintech innovations, including digital payment systems, peer-to-peer lending, and blockchain-based financial platforms, have further complicated the tasks of central banks. As financial activities increasingly move to unregulated fintech platforms, the traditional mechanisms central banks use to monitor and control monetary flow face challenges. This has several implications:

Impact on Money Supply and Velocity

The rise of digital payment systems and cryptocurrencies has implications for money supply and its velocity. Traditional indicators, which central banks use to gauge economic activity, such as M1 and M2 money supply, might no longer provide an accurate reflection of the liquidity available in the economy. As consumers adopt non-bank financial platforms and cryptocurrencies, central banks need to innovate and adapt new models to measure economic activity effectively.

Challenges with Regulatory Oversight

Fintech firms are often less regulated than traditional banks. This lack of regulation presents challenges for central bank oversight of systemic risks. Fintech platforms that handle vast amounts of money pose a risk of financial instability if they fail or become compromised. As such, central banks must push for regulatory frameworks that ensure fintech companies operate under comparable standards of security and accountability as traditional financial institutions.

Case Study

In recent years, several central banks have attempted to adapt to the challenges of the digital era. The People’s Bank of China (PBoC) has been at the forefront of developing its own CBDC, called the digital yuan. The PBoC aims to maintain control over monetary supply and offer a government-backed alternative to existing cryptocurrencies. The goal is to enhance monetary policy effectiveness while preventing the risks posed by the widespread use of privately issued cryptocurrencies.

Meanwhile, in the United States, the Federal Reserve has taken a more cautious approach, conducting extensive research on the implications of CBDCs. The Federal Reserve recognizes the need to balance innovation with financial stability, ensuring that a digital dollar would not jeopardize the commercial banking sector or infringe on the privacy rights of citizens.

Maintaining Central Bank Independence in the Digital Age

As central banks grapple with the challenges of the digital revolution, the question of their independence becomes more pressing. Central bank independence has always been seen as a cornerstone of effective monetary policy, insulating central banks from political pressures. However, the digital age has introduced new challenges to the maintenance of this independence.

Increased Expectations and Public Scrutiny

With the rise of digital technologies, central banks are facing greater public scrutiny and expectations. Digital communication channels have amplified the voices of critics, and central banks now need to defend their policies in the face of instant public feedback. The perception of central bankers has shifted dramatically—from being viewed as grey technocrats to being seen as almost omnipotent figures with a significant public presence.

Central bankers are frequently called upon to comment not only on monetary policy but also on broader economic and social issues, such as climate change. This expanded role can, paradoxically, undermine central bank independence, as public and political pressures grow to have central banks use their balance sheets for purposes beyond their core mandate of price stability.

The Role of Central Banks in Regulating Digital Finance

To preserve their independence while managing the challenges of the digital era, central banks need to play an active role in the regulation of digital finance. Ensuring that digital currencies and fintech platforms are regulated in a manner consistent with the broader goals of monetary policy will be crucial for maintaining control over the economy.

One of the major concerns for central banks is maintaining exchange rate stability given the rise of digital assets that are not linked to national currencies. Digital currencies have the potential to introduce significant volatility, as their value can be driven more by speculation than by economic fundamentals. Central banks must develop strategies to mitigate the volatility introduced by digital currencies and prevent destabilizing capital flows driven by speculative activities in the cryptocurrency markets.

Strategies for Central Banks in the Digital Era

Embracing Technological Innovation

To adapt to the changing landscape, central banks must also embrace technological innovation themselves. This means not only researching and potentially implementing CBDCs but also adopting big data analytics and artificial intelligence to enhance decision-making processes. By utilizing modern technologies, central banks can more effectively track financial flows, forecast economic trends, and implement appropriate policy responses.

Enhancing Collaboration with Other Regulatory Authorities

Central banks must work closely with other financial regulators to ensure a unified approach to digital finance. The rise of fintech has blurred the lines between financial sectors, necessitating enhanced collaboration between central banks, securities regulators, and even competition authorities. Such collaboration will help develop a consistent framework that minimizes regulatory arbitrage—where companies move operations to less regulated jurisdictions—and ensures that digital financial activities do not undermine economic stability.

Communication as a Tool for Stability

The digital age demands that central banks become more transparent in their communications. Effective communication can help anchor expectations during times of uncertainty. The Federal Reserve has been particularly effective in using press conferences and forward guidance as tools for stabilizing markets and guiding expectations. Such measures are more important than ever in a digital environment where financial news—and rumors—can spread globally in seconds.

Conclusion

The digital era presents Central banks in the digital age with challenges like managing digital currencies and balancing fintech innovations with financial stability. To ensure monetary stability, central banks must embrace innovation while maintaining effective regulatory oversight.

In an age of rapid communication and technological change, central bank independence, adopting new regulatory tools, and clear public communication are crucial. As central banks adapt, their success in safeguarding economic stability will depend on their ability to innovate and collaborate in the digital age.

FAQs

What challenges do digital currencies pose to central banks?

Digital currencies, particularly central bank digital currencies (CBDCs), present challenges such as disrupting traditional banks’ role in credit provision, balancing privacy with security, and ensuring data protection. Central banks must also manage the potential impact on monetary policy effectiveness and financial stability.

How does fintech affect central bank control over monetary policy?

Fintech innovations, including digital payment systems and cryptocurrencies, complicate central bank control by moving financial activities outside traditional banking. This shift makes it harder for central banks to monitor money flow, impacting traditional economic indicators and reducing policy effectiveness without new regulatory measures.

Why is central bank independence difficult to maintain in the digital age?

Central banks face growing public scrutiny and pressure to address social and economic issues beyond their core mandates, like climate change or digital finance risks. This expanded role can lead to increased political influence, challenging central bank independence and their focus on core objectives, such as price stability.

What role do central banks play in regulating digital finance?

Central banks work to regulate digital finance by overseeing digital currencies and fintech platforms to prevent risks like financial instability and speculative capital flows. Their role includes developing frameworks for digital assets, collaborating with other regulators, and managing risks to exchange rate stability.

How can central banks adapt to the challenges of the digital age?

To adapt, central banks are embracing technological innovations like big data and artificial intelligence for better economic monitoring and policy decisions. They also enhance collaboration with regulatory authorities to develop unified frameworks and use effective communication to manage public expectations in a rapidly changing environment.

What is the significance of central bank communication in the digital era?

In the digital age, rapid information flow means central banks must communicate transparently and proactively to anchor expectations and reduce market volatility. Tools like forward guidance and regular press conferences help them clarify policy intentions, stabilize markets, and manage economic uncertainties effectively.

Thanks for reading! Share this with friends and spread the knowledge if you found it helpful.

Happy learning with MASEconomics