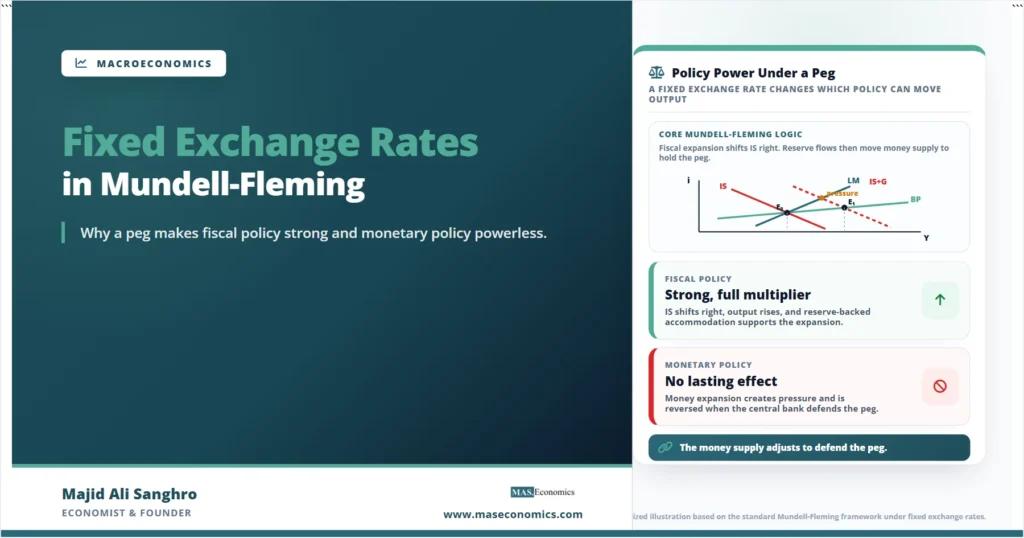

In the decades after Bretton Woods, governments that pegged their currencies kept discovering the same uncomfortable rule: once the exchange rate is fixed and capital can move, the central bank can no longer decide its own money supply. A peg defended with reserves turns the money stock into something the balance of payments controls, not the central bank. The behavior of fixed exchange rates Mundell-Fleming analysis predicts is exactly this, and it produces a result that surprises people the first time they see it: under a credible peg with mobile capital, fiscal policy becomes unusually powerful while monetary policy loses its grip entirely.

That reversal is not a quirk. It falls directly out of the open-economy diagram developed by Robert Mundell and J. Marcus Fleming, where goods market equilibrium, money market equilibrium, and external balance must hold together. The Mundell-Fleming model shows that the exchange-rate regime decides which variable adjusts when the external accounts move out of balance, and under a peg that variable is the money supply itself. Tracing one fiscal expansion through the diagram is the cleanest way to see why.

Peg Commitment and Money Supply

A fixed exchange rate is a promise to buy or sell domestic currency at a stated price in foreign currency. Honoring that promise has a mechanical consequence for the money supply. When the balance of payments runs a surplus, foreign currency flows in, and the central bank must buy that foreign currency with domestic currency to stop the exchange rate from appreciating. Buying foreign currency means issuing domestic currency, so the domestic money supply expands. When the balance of payments runs a deficit, the process runs in reverse: the central bank sells reserves, buys back domestic currency, and the money supply contracts.

This is the heart of the fixed-rate case. The money supply is endogenous. It is whatever the defense of the peg requires, which means the central bank cannot independently set it. The accounting behind this sits in the balance of payments: any imbalance on the current and capital accounts has to be settled through official reserve transactions, and those transactions move the monetary base.

The key commitment. Under a fixed exchange rate with capital mobility, the money supply adjusts automatically to whatever level keeps the balance of payments in equilibrium. The central bank surrenders control of the money stock as the price of holding the peg.

In the diagram, this commitment means the LM curve is not anchored by the central bank. It moves on its own whenever reserve flows change the money supply, and it keeps moving until the economy returns to a point on the BP curve, where the external accounts balance and reserve flows stop. That endogenous LM curve is what makes the fixed-rate results so different from the closed-economy intuition of the IS-LM framework.

Fiscal Expansion Through the Diagram

Consider a government that increases spending or cuts taxes, under a fixed exchange rate and high capital mobility, so the BP curve is relatively flat. The fiscal expansion raises planned spending at every interest rate, which shifts the IS curve to the right. The first thing that happens is exactly what the closed-economy model would predict: higher output and a higher domestic interest rate at the new IS-LM crossing.

But that crossing now sits above the BP curve. The domestic interest rate has risen above the level consistent with external balance, and with mobile capital that gap pulls in foreign funds. The capital account swings into surplus, the overall balance of payments moves into surplus, and the peg comes under upward pressure. Defending it forces the central bank to buy the incoming foreign currency and issue domestic currency, so the money supply rises and the LM curve shifts to the right. The adjustment continues until the economy reaches a new equilibrium back on the BP curve.

The path runs from E0 to the temporary point A and then to E1. Point A is where the new IS curve crosses the original LM curve, and it lies above the BP curve, which is the visible sign of the balance-of-payments surplus. The economy does not stay at A. Reserve inflows expand the money supply, the LM curve slides right, and the economy settles at E1, where IS1, LM1, and BP all meet again. Output has risen from Y0 to Y1, and because capital is highly mobile, the interest rate ends up close to where it started.

The reason fiscal policy is so effective here is that the monetary response reinforces it rather than offsetting it. In a closed economy, a fiscal expansion raises the interest rate and crowds out private investment, which blunts the output gain. Under a fixed rate with mobile capital, the higher interest rate instead triggers a capital inflow that forces the money supply up, the LM curve shifts to accommodate the fiscal push, and the crowding-out is undone. Fiscal policy gets the full multiplier with no monetary leakage.

Monetary Policy Ineffectiveness Under a Peg

The same mechanism that strengthens fiscal policy disables monetary policy. Suppose the central bank tries to stimulate the economy by expanding the money supply directly, shifting the LM curve to the right on its own. Output rises and the domestic interest rate falls at the new internal crossing, which now sits below the BP curve. With mobile capital, the lower interest rate sends capital abroad, the balance of payments swings into deficit, and the peg comes under downward pressure.

Defending the peg now forces the central bank to sell reserves and buy back domestic currency, which contracts the money supply and pushes the LM curve straight back to where it began. The attempted monetary expansion is reversed by the defense of the peg. The only lasting effect is a fall in reserves. Under perfect capital mobility the reversal is complete, and the central bank ends up with the same money supply, the same interest rate, and the same output as before, having simply traded reserves for nothing.

Caveat. This is the high-mobility benchmark. With imperfect capital mobility the BP curve is steeper, the reversal is partial rather than complete, and monetary policy retains a little short-run traction before reserve losses force a retreat.

The result is the central tension a peg imposes. A country that fixes its exchange rate and allows capital to move freely gives up monetary autonomy. It cannot set interest rates to manage its own business cycle, because any attempt to do so is undone by the reserve flows that defend the peg. This is one face of the open-economy policy constraint formalized in the Mundell trilemma, which states that fixed exchange rates, free capital movement, and independent monetary policy cannot all hold at once.

Policy Effects Side by Side

Setting the two experiments next to each other makes the asymmetry concrete. The exchange-rate regime does not change which instrument exists; it changes which instrument bites. Under a peg with mobile capital, fiscal and monetary policy effectively swap their usual reputations.

| Policy action | Curve that shifts first | Balance-of-payments response | Effect on output |

|---|---|---|---|

| Fiscal expansion | IS shifts right | Surplus, reserves rise, money supply expands | Strong increase |

| Fiscal contraction | IS shifts left | Deficit, reserves fall, money supply contracts | Strong decrease |

| Monetary expansion | LM shifts right | Deficit, reserves fall, money supply reverses | No lasting change |

| Monetary contraction | LM shifts left | Surplus, reserves rise, money supply reverses | No lasting change |

|

Source: MASEconomics editorial synthesis of the Mundell-Fleming fixed-rate case.

|

|||

The pattern is the mirror image of the floating-rate case, where monetary policy is strong and fiscal policy is weak. That symmetry is one of the reasons the model has lasted: a single diagram delivers two opposite policy worlds depending only on whether the exchange rate is fixed or free, and the difference traces entirely to what adjusts when the balance of payments moves. The broader question of how the two instruments interact when both are in play is the subject of work on fiscal and monetary policy coordination.

What the Result Assumes

The sharp conclusion that monetary policy is powerless rests on two assumptions worth stating plainly. The first is that the peg is fully credible, so markets do not expect a devaluation and the domestic and foreign returns differ only by the interest rate, not by an expected exchange-rate change. When credibility weakens, expected devaluation drives a wedge into the capital-account response and the clean result breaks down. The second is high capital mobility. With limited mobility, the BP curve steepens, capital responds sluggishly to interest-rate gaps, and monetary policy keeps some short-run effect before reserves run down.

A third practical limit is sterilization. A central bank can try to offset reserve flows by selling or buying domestic bonds, holding the money supply steady despite the balance-of-payments imbalance. The model treats this as temporary. Sterilization can delay the monetary adjustment, but it cannot prevent it indefinitely, because the underlying imbalance keeps draining or building reserves until the peg either forces the money-supply change or breaks. The diagram captures the end state toward which the economy is pushed, not the speed at which it arrives.

Note. The fixed-rate results describe the short run with fixed prices. Over longer horizons, price-level adjustment and the sustainability of the reserve position add constraints the static diagram does not show.

Conclusion

The lesson of fixed exchange rates Mundell-Fleming analysis is that a peg redistributes policy power rather than simply constraining it. By tying the money supply to the defense of the exchange rate, a credible peg with mobile capital makes fiscal policy unusually effective, because the monetary system accommodates the fiscal push instead of crowding it out. The same mechanism strips monetary policy of any lasting effect, since any attempt to move the money supply is reversed by the reserve flows that hold the peg in place.

The driving force throughout is the endogenous money supply. Under a fixed rate, the central bank cannot choose the money stock; the balance of payments chooses it. A fiscal expansion that pushes the economy above the BP curve draws in reserves and expands the money supply until equilibrium is restored at higher output. A monetary expansion that pushes the economy below the BP curve drains reserves and contracts the money supply until the original position returns.

That mechanism is why the fixed-rate case is the natural counterpart to the floating-rate case rather than a separate model. Both are read off the same open-economy diagram by shifting one curve and tracing the adjustment back to external balance. Holding the exchange rate fixed simply assigns the adjustment to reserves and the money supply, and from that single assignment the entire pattern of strong fiscal policy and ineffective monetary policy follows.

Frequently Asked Questions

Why is fiscal policy more effective under fixed exchange rates?

A fiscal expansion raises the domestic interest rate, which attracts foreign capital under high mobility and pushes the balance of payments into surplus. Defending the peg forces the central bank to expand the money supply, which shifts the LM curve right and accommodates the fiscal push. Because the monetary system reinforces rather than offsets the expansion, crowding-out disappears and output rises by the full amount.

Why does monetary policy fail under a fixed exchange rate?

A monetary expansion lowers the domestic interest rate, which sends capital abroad and pushes the balance of payments into deficit. Defending the peg forces the central bank to sell reserves and buy back domestic currency, which contracts the money supply and reverses the original expansion. Under high capital mobility the reversal is complete, leaving output unchanged and reserves lower.

What is the role of foreign reserves in defending a peg?

Reserves are the buffer the central bank uses to hold the exchange rate at its stated level. When the balance of payments is in surplus the central bank accumulates reserves and the money supply expands; when it is in deficit the central bank sells reserves and the money supply contracts. These reserve transactions are exactly what make the money supply endogenous under a fixed rate.

Can a central bank sterilize reserve flows to keep monetary control?

It can try. Sterilization means offsetting reserve-driven changes in the money supply by trading domestic bonds, holding the money stock steady for a time. But the underlying balance-of-payments imbalance keeps moving reserves, so sterilization delays the monetary adjustment rather than removing it. Sustained over time, the imbalance forces either the money-supply change or a break in the peg.

How does capital mobility change the fixed-rate results?

The strongest results assume high capital mobility, which makes the BP curve flat and the monetary reversal complete. With imperfect mobility the BP curve is steeper, capital responds weakly to interest-rate gaps, and monetary policy keeps some short-run effect before reserve losses force a retreat. The fiscal-policy advantage remains but is less extreme.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics