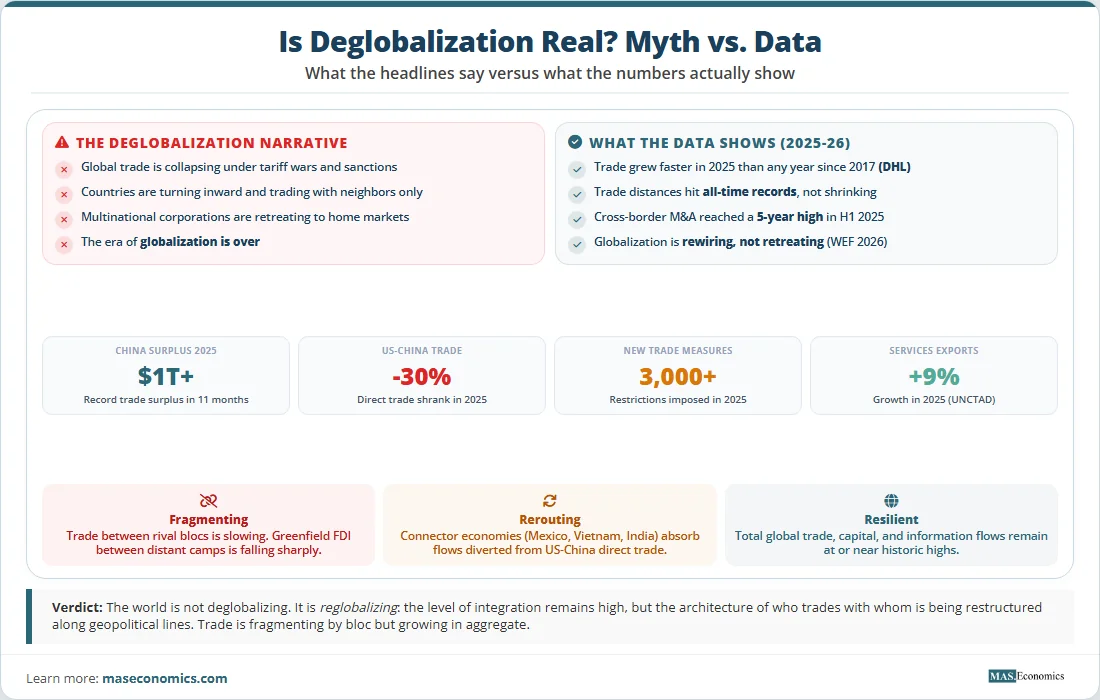

The headlines paint a grim picture. Wars in the Middle East have disrupted the flow of oil through the Strait of Hormuz. Tariff walls between the world’s two largest economies are higher than at any point since the 1930s. Over 3,000 new trade restrictions were imposed in 2025 alone. Traditional alliances between Western nations are fraying under the weight of unilateral decision-making. The World Trade Organization’s dispute settlement system remains paralyzed. And a growing chorus of commentators is declaring that the era of globalization, the defining economic force of the past four decades, is over.

But is it?

The answer, according to the most comprehensive data available, is no. Global trade grew faster in 2025 than in any year since 2017. Average distances in trade and foreign direct investment reached all-time records. Cross-border mergers and acquisitions hit a five-year high. China’s trade surplus exceeded $1 trillion in just eleven months. And the share of economic activity flowing across international borders, rather than staying domestic, has not declined.

The world is not deglobalizing. It is rewiring. The level of global integration remains remarkably high, but the architecture of who trades with whom, through which routes, and under what rules is being restructured along geopolitical lines. Understanding the difference between deglobalization and this structural rewiring is essential for anyone trying to make sense of the global economy in 2026.

The Deglobalization Narrative

The idea that globalization is reversing did not appear overnight. Economists Pinelopi Goldberg and Tristan Reed of Brookings have identified three distinct phases in the deglobalization movement, each driven by different economic forces.

Phase One (2015 to 2018): The Populist Backlash. The first wave emerged from growing awareness that while globalization had lifted hundreds of millions out of poverty worldwide, it had also created significant disruption in advanced economies. Communities that lost manufacturing jobs to lower-wage countries, particularly to China, experienced rising inequality, declining social mobility, and political radicalization. This frustration produced Brexit in the United Kingdom, a new wave of tariffs in the United States, and a broader turn toward protectionist rhetoric across the developed world.

Phase Two (2020 to 2022): The Supply Chain Shock. The COVID-19 pandemic exposed the fragility of global supply chains that had been optimized for efficiency rather than resilience. When Chinese factories shut down, and shipping containers piled up in the wrong ports, companies and governments around the world suddenly discovered that they depended on a single country for everything from semiconductor chips to medical supplies. The word “resilience” replaced “efficiency” as the organizing principle of supply chain strategy.

Phase Three (2022 to Present): Geopolitical Fragmentation. Russia’s invasion of Ukraine, followed by unprecedented Western sanctions, demonstrated that economic interdependence could be weaponized. The US-China rivalry intensified with export controls on advanced semiconductors, restrictions on foreign direct investment, and the emergence of competing technology ecosystems. Most recently, the global tariff war of 2025 to 2026 pushed average US tariff rates to their highest levels since the Smoot-Hawley era, and the closure of the Strait of Hormuz during the US-Iran conflict disrupted the flow of roughly 20% of the world’s daily oil supply.

Each of these phases added momentum to the narrative that globalization was dying. But narrative and data are not the same thing.

Six Facts That Challenge the Narrative

The most comprehensive assessment of global connectedness comes from the DHL Global Connectedness Report 2026, which tracks international flows of trade, capital, information, and people across 14 categories from 2001 to 2025. Its findings directly contradict the deglobalization narrative.

Fact 1: Trade Grew Faster in 2025 Than in Any Year Since 2017

Global goods trade expanded rapidly in 2025, exceeding the growth rate of every year since 2017 (excluding the pandemic rebound). This is the opposite of what deglobalization would predict. If countries were genuinely turning inward, trade volumes would be declining relative to GDP. Instead, they are growing.

Fact 2: Trade Distances Reached All-Time Records

If regionalization, the idea that countries are trading more with nearby neighbors and less with distant partners, were real, we would expect average trade distances to be shrinking. The opposite is happening. Both goods trade and greenfield FDI crossed their longest average distances on record in 2025, while the share of these flows occurring within major geographic regions fell to new lows.

Fact 3: Cross-Border Investment Remains Strong

Goldman Sachs reported that the international share of mergers and acquisitions transactions reached a five-year high during the first half of 2025. Greenfield FDI relative to world GDP, despite modest declines in 2024 and 2025, remained in line with the average over the past decade. Business leaders have not embraced a general shift toward domestic rather than international investment.

Fact 4: China’s Trade Surplus Hit a Record

China announced that its 2025 trade surplus exceeded $1 trillion in just eleven months, according to World Economic Forum analysis. This is not the behavior of a country retreating from global trade. It reflects China’s continued role as the world’s manufacturing hub, even as direct trade with the United States has declined.

Fact 5: Services Trade Is Booming

Much of the deglobalization narrative focuses on goods trade, which peaked as a share of GDP around 2008. But the services trade tells a completely different story. According to UNCTAD’s January 2026 trade update, services export growth reached 9% in 2025, with digitally deliverable services now representing 56% of global services exports. Globalization is not ending; it is evolving from a goods-dominated model to one increasingly driven by services, data, and digital flows.

Fact 6: The Largest Economies Distort the Picture

The DHL report highlights a critical statistical illusion. The ten largest economies generate two-thirds of global GDP but account for less than half of total global trade. Because these large economies have enormous domestic markets, their relatively low trade intensity drags down the global average. Beyond the superpowers, an increasingly multipolar world is actually driving globalization forward. Smaller and medium-sized economies are becoming more, not less, connected to global trade networks.

| Indicator | What Deglobalization Would Predict | What the Data Shows (2025) | Source |

|---|---|---|---|

| Trade volumes | Declining relative to GDP | Fastest growth since 2017 | DHL Report 2026 |

| Trade distances | Shrinking (regionalization) | All-time record highs | DHL Report 2026 |

| Cross-border M&A | Declining share | Five-year high in H1 2025 | Goldman Sachs |

| China trade surplus | Declining exports | Record $1T+ in 11 months | WEF 2026 |

| Services exports | Stagnant or declining | +9% growth in 2025 | UNCTAD 2026 |

| FDI distances | Shortening (nearshoring) | Longest distances on record | DHL Report 2026 |

|

|||

So What Is Actually Happening? The Rise of “Reglobalization”

If the world is not deglobalizing, what is happening? The World Economic Forum coined a useful term in January 2026: “reglobalization.” The level of global integration remains high, but its architecture is being restructured. Three forces are reshaping the map of global trade.

Geopolitical Bloc Formation

Research from the Bank for International Settlements has shown that trade between countries in opposing geopolitical camps has grown more slowly than trade within those camps. Greenfield FDI between geopolitically distant countries has fallen sharply, while intra-bloc investment and “friendshoring” have held up. The world is not breaking into isolated blocs, but economic flows are increasingly following geopolitical alignment.

This pattern is visible in the data. Direct US-China trade shrank by 30% in 2025, particularly in sensitive sectors like semiconductors and advanced technology. But this decline did not reduce total global trade. Instead, “connector economies” absorbed the diverted flows. Mexico and Vietnam import intermediate goods from China, assemble or process them, and export finished products to the United States or Europe. As J.P. Morgan’s analysis documented, supply chains are proving “flexible and resilient,” with production shifting elsewhere rather than returning home.

The Rise of Connector Economies

The biggest winners of trade restructuring are countries positioned between the major blocs. Mexico has overtaken China as the largest source of US imports. Vietnam’s exports to the United States have surged as manufacturers relocate from China. India is attracting record levels of foreign investment as companies seek alternatives to Chinese manufacturing. Poland, Turkey, and Morocco are playing similar roles for European supply chains.

These connector economies are not replacing globalization. They are enabling it to continue in a more geographically distributed form. The result is a trading system that is more complex, more politically fragmented, but not actually less integrated in aggregate.

The Weaponization of Interdependence

Perhaps the most significant structural change is that economic interdependence, once seen as a force for peace, is now explicitly used as a tool of coercion. Sanctions on Russia, export controls on China, the closure of the Strait of Hormuz during the recent conflict, and the proliferation of tariffs all reflect a world in which governments view trade linkages as leverage rather than mutual benefit.

This creates a paradox. Countries want the economic benefits of trade but are simultaneously trying to reduce their vulnerability to trading partners who might use those linkages against them. The result is not less trade, but more complicated trade: longer supply chains, more intermediaries, more redundancy, and higher costs. Multinational corporations are not retreating from global operations. They are adding layers of complexity to manage geopolitical risk while maintaining access to global markets.

Source: World Bank, WTO, UNCTAD (2026). Services trade data from WTO Services Statistics. Projections for 2025-26 from DHL Global Connectedness Report 2026 | MASEconomics.com

The chart reveals the central paradox of the deglobalization debate. The dashed red line shows trade restrictions surging exponentially, particularly since 2018. Yet goods trade as a share of GDP (the solid teal line) has remained remarkably stable, hovering near its 2008 peak. Meanwhile, services trade (the green line) has climbed steadily, more than compensating for any stagnation in goods. The world is imposing more barriers to trade than ever, but trade itself refuses to decline.

Why Deglobalization Is Harder Than It Looks

There is a simple economic reason why deglobalization has not happened despite the political pressure for it: the gains from trade are enormous, and the costs of unwinding global supply chains are even higher.

When a company builds a factory in Vietnam to serve the US market, it is not just chasing lower wages. It is accessing a trained workforce, established logistics networks, port infrastructure, supplier ecosystems, and regulatory frameworks that took decades to build. Moving that production back to the United States would require replicating all of these complementary assets, at vastly higher cost and over many years. This is why the CHIPS Act, which committed over $50 billion to rebuilding US semiconductor manufacturing, will take until the end of the decade to produce significant output. You can pass a law in a day, but you cannot build a semiconductor fabrication plant in less than three to four years.

The arbitrage that drives globalization, the international differences in costs, skills, and resources, has not disappeared. As long as it remains profitable to produce goods in one country and sell them in another, international trade will continue. Tariffs and sanctions can redirect trade flows, but they cannot eliminate the underlying economic incentives.

Globalization Is Evolving, Not Dying

If you have read our foundational article on what globalization is, you know that globalization has never been a straight line. It has always advanced in waves, punctuated by crises that temporarily slow integration before new technologies, new trade agreements, or new economic opportunities push it forward again. The current moment fits this pattern precisely.

The first great era of globalization (1870 to 1914) ended with World War I. The interwar period saw genuine deglobalization: trade collapsed, empires fragmented, and the global economy shattered. But after 1945, a new architecture of international institutions, the WTO, the IMF, the World Bank, and multilateral trade agreements, rebuilt and deepened global integration to levels the pre-war world could never have imagined.

Today’s disruptions, as serious as they are, do not yet resemble the collapse of 1914 to 1945. Trade is growing, not collapsing. Investment is rerouting, not retreating. Technology is making services trade easier, not harder. The risks are real: a major escalation in the US-China conflict, a prolonged closure of critical shipping lanes like the Strait of Hormuz, or a cascade of retaliatory tariffs could push the world toward genuine fragmentation. But we are not there yet.

The DHL Global Connectedness Report captured it best: “Deglobalization remains a possibility, but it is not today’s reality.”

MASEconomics Explains

Four concepts essential to understanding the deglobalization debate

Deglobalization

A sustained decline in the cross-border flows of trade, capital, information, and people relative to domestic economic activity. Despite widespread claims, comprehensive data from DHL, the WEF, and UNCTAD shows that genuine deglobalization has not occurred as of 2025, though geopolitical fragmentation is real.

Reglobalization

A term coined by the World Economic Forum in 2026 to describe the current restructuring of global trade. The overall level of integration remains high, but the architecture of who trades with whom is being reorganized along geopolitical lines. Some links fragment while new ones form.

Connector Economies

Countries positioned between major geopolitical blocs that absorb diverted trade flows. Mexico, Vietnam, India, Poland, and Turkey are prominent examples. These economies import intermediate goods from one bloc (often China), process or assemble them, and export finished products to another (often the United States or Europe).

Friendshoring

The strategy of concentrating supply chains among geopolitically allied nations rather than optimizing purely for cost. Friendshoring reduces vulnerability to sanctions, export controls, and political coercion but increases production costs. It represents a shift from efficiency-first to resilience-first trade architecture.

Key Takeaway and Conclusion

The deglobalization narrative is powerful, emotionally compelling, and supported by real disruptions: wars, tariff walls, sanctions, and the fracturing of longstanding alliances. But it is not supported by the data. Global trade grew faster in 2025 than in any year since 2017. Trade distances reached all-time records. Cross-border investment remained strong. Services trade boomed. The world economy is more interconnected today than at any previous point in human history.

What is changing is the architecture of globalization, not its scale. Trade is fragmenting along geopolitical lines, with flows between rival blocs slowing while flows within blocs and through connector economies accelerate. This is reglobalization, not deglobalization. It is messy, expensive, and politically fraught, but it is not a retreat from international integration.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.