The standard teaching of international economics begins with a clean result: free trade raises welfare, tariffs reduce it, and any deviation from open markets is a deadweight loss the country bears for the sake of political or strategic objectives. The result is correct under standard assumptions and stands up well against the empirical record. But the assumptions matter. One assumption in particular, that the country imposing the tariff is too small to affect world prices, hides a result that has shaped trade policy debates for over a century. When a country is large enough to influence the price of what it imports, the free-trade prescription no longer follows mechanically. Optimal tariff theory is the analytical framework that describes when, and by how much, a country can raise its own welfare by imposing a tariff.

The theory dates back to Charles Bickerdike’s work in 1906 and was given its modern form by Harry Johnson in two papers in 1953 and 1954. It is not a justification for protectionism. It is a precise statement of one specific case in which a tariff can produce a national welfare gain, and an even more precise statement of why exploiting that case is dangerous in a world where other countries can retaliate. Understanding optimal tariff theory is essential for any serious discussion of trade policy, tariff wars, and the role of the WTO.

Small vs. Large Countries

The starting distinction in optimal tariff theory is between a small country and a large country. The label has nothing to do with population or geographic area. It refers to whether a country’s import demand is large enough to move the world price of the good in question.

A small country is a price-taker in world markets. When it imposes a tariff, world prices are unaffected. The full cost of the tariff falls on the country’s own consumers, who pay the world price plus the tariff. Some of the revenue goes to the government, some goes to protected domestic producers, but the country as a whole loses through reduced consumer surplus and production inefficiency. There is no offsetting gain. The familiar conclusion that tariffs reduce welfare follows directly.

A large country is a price-maker. Its import demand is great enough that when it imposes a tariff and demand contracts, world prices fall. Foreign exporters take part of the hit, accepting lower prices to retain access to the market. The country’s terms of trade, the ratio of export prices to import prices, improve. This terms-of-trade gain is the key mechanism that distinguishes the large-country case. It is a transfer from foreigners to the home country, and it offsets at least part of the domestic inefficiency that the tariff creates.

In practice, the small-country assumption fits most economies. A tariff imposed by Costa Rica on imported steel has no effect on world steel prices. A tariff imposed by Bangladesh on imported cars has no effect on world car prices. For most countries, the optimal tariff is zero, and the standard free-trade prescription applies. The cases where optimal tariff theory matters are limited to large economies, the United States, the European Union, China, and perhaps a handful of others, and to specific commodity markets where smaller economies happen to be large buyers.

The Terms‑of‑Trade Mechanism

The way a tariff lowers import prices is worth explaining carefully, because it is the engine of the entire theory.

Imagine a large country importing steel at a world price of $100 per ton. The country imposes a 20 percent tariff. Domestic consumers now face a price of $120, and the quantity demanded falls. Because the country’s import demand was large enough to influence world prices, the fall in demand caused foreign exporters to lower their prices to retain sales. The world price falls, perhaps to $90. Domestic consumers now pay $90 plus the 20 percent tariff, or $108, rather than the $120 they would have paid in the small-country case.

The country’s government collects tariff revenue on each ton imported. Domestic consumers face a higher price than they would under free trade. But foreigners are now selling at a lower price than they were before. Part of the tariff is, in effect, being paid by foreign exporters rather than by the importing country. This is the terms-of-trade gain. Whether it is large enough to offset the domestic distortions depends on how responsive foreign exporters are to price changes. The less responsive, the larger the terms-of-trade gain.

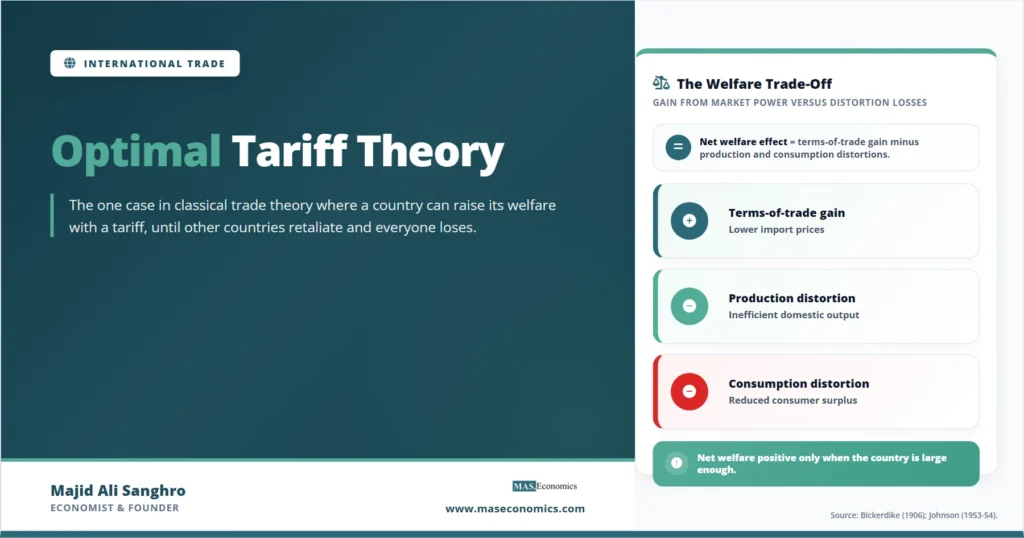

Welfare Decomposition of a Tariff

The total welfare change from a tariff in the large-country case can be split into three components. Two are losses; one is a gain. The net effect depends on whether the gain dominates.

Terms-of-trade gain. Foreign exporters reduce their prices in response to the country’s tariff. This is a transfer from foreigners to the home country and is positive.

Production distortion. The tariff raises the domestic price of the imported good. Domestic producers expand output beyond the level they would produce at world prices, drawing resources into a less efficient use. This is a loss.

Consumption distortion. The same higher domestic price reduces consumption below the free-trade level. Consumers lose surplus from forgone consumption that the protected domestic producers do not capture. This is also a loss.

The optimal tariff is the rate that maximizes the gap between the gains and the losses. At low tariff rates, the terms-of-trade gain accumulates faster than the distortions, and welfare rises. As the tariff increases, distortions accelerate while the marginal terms-of-trade gain shrinks. At some point, the two are exactly balanced. That tariff rate is the optimum from the country’s national welfare perspective.

| Component | Mechanism | Direction | Notes |

|---|---|---|---|

| Terms-of-trade gain | Foreign exporters lower their prices in response to falling import demand | Positive | Larger when foreign-export supply is inelastic |

| Production distortion | Domestic producers expand output beyond the efficient level under free trade | Negative | Larger when domestic supply is elastic |

| Consumption distortion | Consumers face higher domestic prices and reduce consumption | Negative | Larger when domestic demand is elastic |

| Net welfare effect | Sum of the three components | Sign depends on parameters | Positive at optimum if country is large enough |

|

Source: Standard treatment in Krugman, Obstfeld, & Melitz; based on Bickerdike (1906), Johnson (1953-54).

|

|||

The Optimal Tariff Formula

Johnson (1953-54) derived an explicit formula for the optimal tariff rate, expressed in terms of the elasticity of foreign-export supply.

Optimal Tariff Rate

The formula has a clean intuition. If foreign exporters are highly price-responsive (high ε_f), a small price change triggers a large supply response, and the country can extract very little terms-of-trade gain. The optimal tariff is small. If foreign exporters are very unresponsive (low ε_f), even a small change in the country’s demand produces a large price reduction abroad, and the country can capture a large terms-of-trade gain. The optimal tariff is high.

In the extreme case where foreign-export supply is perfectly elastic (ε_f approaches infinity), the optimal tariff approaches zero. The country is effectively a price-taker, and free trade is optimal. In the other extreme, where foreign-export supply is perfectly inelastic, the optimal tariff can be arbitrarily large; the country captures the entire surplus from foreign exporters.

Empirical estimates of foreign-export elasticities suggest optimal tariff rates of perhaps 10 to 30 percent for the largest economies in their most concentrated import sectors. The exact numbers are contested, and a country must have substantial market power in a specific product line for the calculation to be meaningful. The optimal tariff for the United States on, say, Mexican avocados might be substantial. The optimal tariff for the United States on a generic manufactured good for which there are many global suppliers is close to zero.

The Retaliation Problem

So far the analysis has assumed that other countries do not respond. They sit passively while the home country imposes its optimal tariff and captures the terms-of-trade gain. This assumption is the most important weakness of the theory in practice. Foreign countries can and usually do retaliate.

Once retaliation enters the picture, optimal tariff theory becomes a problem in game theory. Each country faces a choice: free trade or tariffs. If the other side stays at free trade, your country gains by imposing a tariff. If the other side retaliates, both lose. The dominant strategy for each country, taken in isolation, is to impose a tariff. The result is the Nash equilibrium of mutual tariffs, in which both countries are worse off than they would be under mutual free trade. The structure is a classic prisoner’s dilemma in Nash equilibrium language.

This is not a theoretical curiosity. The Smoot-Hawley Tariff Act of 1930, which raised US tariffs to historic highs, triggered widespread foreign retaliation and contributed to the collapse of world trade during the Great Depression. World trade volume fell by roughly 60 percent between 1929 and 1933, far more than the fall in output, and the protectionist response is widely seen as having deepened and lengthened the Depression. The episode is the canonical empirical illustration of why national optimal tariffs, exercised in a world of retaliation, produce outcomes that are globally and individually destructive.

The prisoner’s dilemma of tariffs. If only one country imposes its optimal tariff, it gains. If all countries impose their optimal tariffs, every country loses, because each loses more from foreign tariffs on its exports than it gains from its own tariffs on imports. Optimal tariff theory in isolation describes a profitable strategy. Optimal tariff theory in a world of strategic interaction describes the trap that the WTO system was specifically designed to prevent.

The Institutional Response: GATT and WTO

The General Agreement on Tariffs and Trade (GATT), signed in 1947 and later expanded into the World Trade Organization in 1995, was a direct institutional response to the lesson of the Smoot-Hawley. By committing to mutual tariff reductions and binding tariff ceilings, member countries gave up their unilateral right to impose optimal tariffs in exchange for foreign commitments not to do the same. The resulting equilibrium, although it deprives each country of the gains its optimal tariff would individually produce, leaves each country better off than the Nash equilibrium of mutual tariffs would.

The WTO’s most-favored-nation (MFN) principle, which requires members to apply the same tariff rate to imports from all WTO members, prevents discriminatory tariff strategies. The dispute settlement system provides a mechanism for retaliation that is rule-based rather than escalating, limiting the damage when disputes do arise. The architecture is not perfect, and it has come under significant strain during recent tariff wars, but the underlying logic remains intact: cooperative restraint dominates the unilateral pursuit of optimal tariffs once retaliation is anticipated.

Strengths and Limitations of the Theory

Optimal tariff theory is on solid ground in three ways and contested in several others.

It is correct as a static analytical statement. Given the assumptions, the math is right, and a large country can, in principle, raise its own welfare by imposing a tariff. The theory has not been refuted; it has been refined.

It correctly predicts retaliation. The Smoot-Hawley experience, the 1980s steel and Japanese auto tariffs, the 2018-2019 US-China tariff war, and the 2025-2026 wave of global tariffs all confirm that affected countries respond. The Nash equilibrium of mutual tariffs is the empirical norm in real tariff conflicts.

It correctly identifies the conditions under which a tariff can produce a national welfare gain in isolation. Countries with substantial buying power in specific markets and specific products with inelastic foreign supply are the candidates.

The theory is on weaker ground when applied to manufactured goods in modern global supply chains. The trade-in-tasks framework has shown that imported goods are often bundles of value added from many countries, including the importing country itself. A tariff on Chinese smartphone imports also taxes the substantial US value embedded in those phones. The terms-of-trade gain in such cases is much smaller and harder to identify than the basic model suggests.

The theory also abstracts from the political economy of tariff design. Real tariffs are not set by benevolent planners maximizing welfare. They are set by political processes shaped by lobbying, electoral considerations, and bureaucratic capacity. The tariff that emerges is usually nowhere near the theoretical optimum, even when the underlying conditions for one exist.

The Theory in Modern Trade Economics

Optimal tariff theory occupies a particular position in modern trade economics. It is the standard analytical justification for the proposition that free trade is not unconditionally optimal. The Heckscher-Ohlin framework, the Ricardian model, and most modern trade theory take place in a small-country world where tariffs are pure loss. Optimal tariff theory carves out the one classical exception. It is also the analytical bridge between trade theory and the empirical literature on tariff wars, including the 1930s, the 2018-2019 US-China episode, and the broader global tariff wave that emerged in 2025-2026.

The theory is rarely a policy recommendation. The conditions under which a national optimal tariff produces a net gain are narrow, the retaliation problem is severe, and the political economy of real tariff-setting is far removed from the theoretical optimum. The theory is used mainly to explain why countries pursue tariff policies that look damaging in welfare terms, why the WTO system was built the way it was, and why tariff wars end up where they do.

Explains

Four concepts that extend the optimal tariff framework

Continue exploring international trade theory on the MASEconomics blog.

Explore the MASEconomics BlogConclusion

Optimal tariff theory is the precise statement of the one case in classical trade analysis where a tariff can raise a country’s welfare. The conditions are restrictive: the country must be large enough to influence world prices, the targeted import must come from suppliers with limited price flexibility, and other countries must not retaliate. When all three hold, the country can use a tariff to capture a transfer from foreign exporters that more than offsets its own domestic distortions. The formula t* equal to one over the foreign-export supply elasticity gives the analytical magnitude.

The reason the theory matters for modern trade policy is not as a recipe for unilateral protectionism. It is as the analytical foundation for understanding why tariff wars happen and why they end the way they do. The unilateral incentive to impose an optimal tariff exists. The mutual incentive of all countries to impose them produces a Nash equilibrium of mutual losses. The WTO architecture is the institutional response to that equilibrium, an attempt to make cooperative restraint the default rather than the exception. Every tariff dispute since the 1947 GATT can be read as a test of whether that institutional response is holding.

Frequently Asked Questions

What is optimal tariff theory?

Optimal tariff theory is the analytical framework that identifies the conditions under which a country can raise its national welfare by imposing a tariff. The result requires the country to be large enough to affect world prices for the imported good. When that condition holds, a tariff can capture a terms-of-trade gain from foreign exporters that more than offsets the domestic production and consumption distortions a tariff creates.

Why is the optimal tariff zero for small countries?

Small countries are price-takers in world markets. When a small country imposes a tariff, world prices do not change. The full cost of the tariff falls on the country’s own consumers and producers as deadweight loss. There is no offsetting terms-of-trade gain because foreign exporters do not adjust their prices. For small countries, the standard free-trade conclusion holds and the optimal tariff is zero.

What is the optimal tariff formula?

Harry Johnson’s 1953-54 derivation gives the optimal tariff rate as t* equal to one divided by the elasticity of foreign-export supply. If foreign exporters are highly responsive to price changes, the optimal tariff is small. If foreign exporters are unresponsive, the optimal tariff is large. The formula provides the analytical link between a country’s market power and the size of its welfare-maximizing tariff.

Why does retaliation undermine optimal tariff theory?

The theory in isolation assumes foreign countries do not respond. In practice, they do. Each country has a unilateral incentive to impose its own optimal tariff. When all countries follow that incentive, the result is a Nash equilibrium in which every country imposes tariffs and every country is worse off than it would be under mutual free trade. The structure mirrors the prisoner’s dilemma, and the WTO system was built specifically to coordinate cooperative restraint and avoid this outcome.

How does optimal tariff theory relate to the WTO?

The WTO and its predecessor GATT were built to prevent the Nash equilibrium that optimal tariff theory predicts when countries act unilaterally. By committing to bound tariff ceilings and most-favored-nation treatment, members give up the right to pursue their individual optimal tariffs in exchange for mutual commitments. The system is designed to deliver the cooperative outcome of mutual restraint, which leaves every country better off than the mutual-tariff equilibrium would.

Did optimal tariff theory predict the Smoot-Hawley experience?

It anticipated the structure of what happened. The 1930 Smoot-Hawley Tariff Act raised US tariffs to historic highs, and dozens of countries retaliated with their own tariffs. World trade collapsed by roughly 60 percent between 1929 and 1933, far more than the fall in output. The episode is the canonical empirical illustration of why pursuing national optimal tariffs in a world of retaliation produces mutually destructive outcomes, and it shaped the design of the postwar trade system.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics