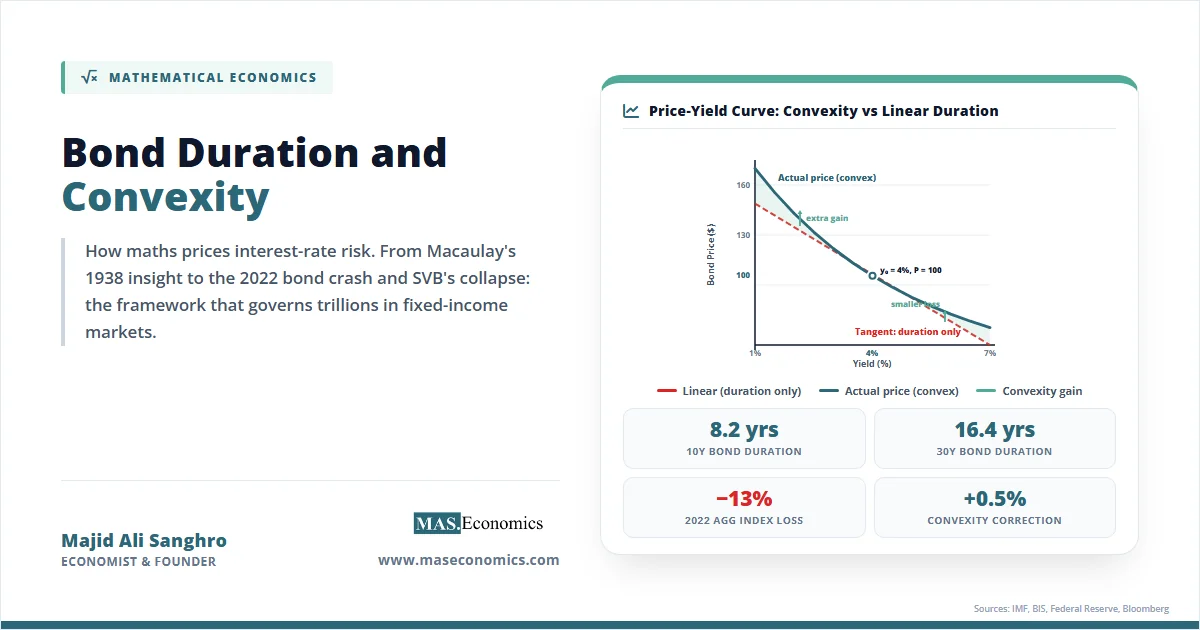

Mathematical Economics Bond Duration and Convexity: How Maths Prices Interest-Rate Risk Bond duration and convexity are the mathematical tools fixed-income markets use to measure how bond prices respond to interest-rate changes,... May 1, 2026