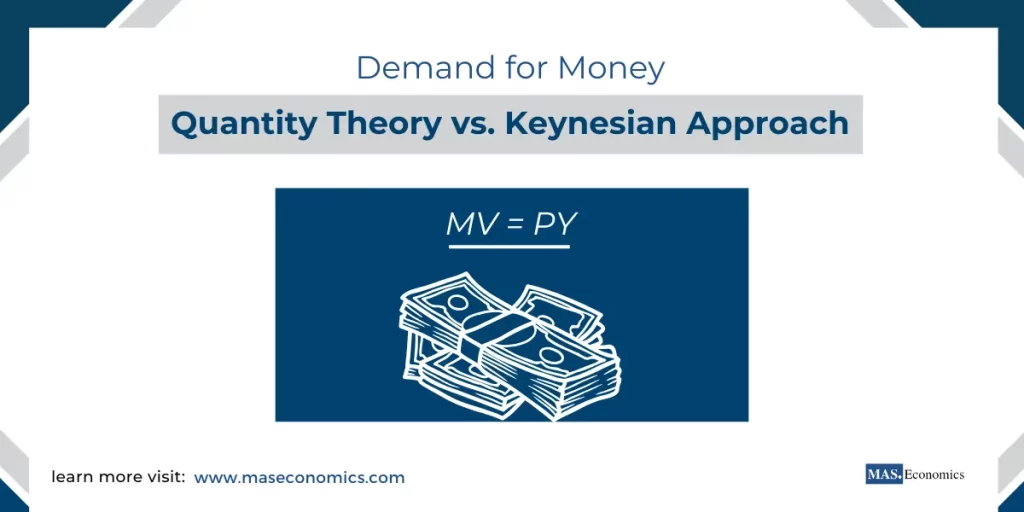

Let’s start by breaking down a fundamental concept that’s key to understanding how our economies work: the demand for money. Now, when we talk about the demand for money, we’re not just talking about how much people want in their bank accounts. Instead, we’re exploring why people hold onto money rather than spending or investing it. Why does money sit in our wallets or bank accounts instead of constantly flowing into goods, services, or investments? This is what we mean by “demand for money” in macroeconomics.

In this article, we’ll explore two significant approaches to understanding the demand for money: the Quantity Theory of Money, a classical view, and the Keynesian Approach, which takes a more nuanced, modern perspective. By the end of this piece, you’ll understand the differences between these theories, why they matter, and how they influence aggregate demand and economic policy. So let’s dive right in!

Quantity Theory of Money: A Classical Perspective

The Quantity Theory of Money is one of the oldest and most fundamental economic theories. Its origins go back as far as the 16th century, but it was refined by economists like Irving Fisher in the early 20th century. At its core, the Quantity Theory of Money is pretty straightforward—it proposes a direct relationship between the amount of money in an economy and the overall price level. Essentially, it tells us that more money circulating in the economy will lead to higher prices.

The Equation of Exchange

To make things easier to understand, the Quantity Theory of Money is often summarized using Fisher’s Equation of Exchange:

\( MV = PY \)

Let’s break down these letters:

- \( M \): This represents the total money supply in the economy. Think of it as all the cash and bank deposits people and businesses hold.

- \( V \): The velocity of money—this term captures how frequently money changes hands within a given period. It measures how actively money is being used for transactions.

- \( P \): This is the price level of goods and services. If prices are rising, then \( P \) is increasing.

- \( Y \): The real output or the total quantity of goods and services produced (essentially, the real GDP).

In simpler terms, the product of \( M \) (money supply) and \( V \) (velocity) equals the product of \( P \) (price level) and \( Y \) (output). So, according to this theory, if the money supply \( M \) goes up and velocity \( V \) stays the same, then something on the right side of the equation also has to rise. Usually, it’s the price level \( P \) that increases, which means inflation. If the output \( Y \) remains stable, adding more money into the system mostly leads to higher prices.

Proportionality and Assumptions

The classical economists made a few big assumptions here. They assumed that velocity \( (V) \) and output \( (Y) \) remain pretty stable over time. This means that if you increase the money supply \( (M) \), prices \( (P) \) will go up proportionally. In this view, money is mainly used as a medium of exchange—a simple tool to buy goods and services. Because of these assumptions, the theory suggests a pretty clear-cut relationship: more money leads to higher prices.

It’s this simplicity that made the Quantity Theory so attractive to early economists and policymakers. If you double the money supply, the theory suggests that you’re going to double the price level—assuming everything else stays the same.

Criticism of the Quantity Theory

While the Quantity Theory of Money helps us understand inflation and its connection to the money supply, it’s not without flaws. Critics argue that velocity \( (V) \) isn’t actually constant—it fluctuates depending on people’s expectations about the future, interest rates, and general economic conditions. So, the neat proportional relationship between money supply and price level doesn’t always hold true in practice.

Another criticism is that the Quantity Theory doesn’t consider the other roles money plays, like being a store of value or a tool for speculation. In reality, people don’t always immediately spend the extra money they have; they might save it, invest it, or use it in ways that don’t directly affect the price level. To get a more nuanced understanding of the demand for money, we need to take a look at the Keynesian Approach.

Keynesian Approach to the Demand for Money

Enter John Maynard Keynes—one of the most influential economists of the 20th century. Keynes brought a fresh perspective to understanding why people hold money. Unlike the classical Quantity Theory, which mostly looks at money as something we use to buy things, Keynes argued that people hold onto money for several different reasons, which makes the demand for money more dynamic and complicated.

Motives for Holding Money

Keynes identified three main motives for holding money:

Transactions Motive

This one is straightforward. People need money for their day-to-day expenses. Whether it’s buying groceries, paying the rent, or covering bills, people need money on hand for regular transactions. This is similar to the classical idea of money as a medium of exchange.

Precautionary Motive

Life is unpredictable, and Keynes recognized that. People hold money to cover unexpected expenses—things like a sudden car repair, a medical emergency, or other surprises. This is the precautionary motive, where individuals prefer having some extra liquidity just in case something unexpected happens.

Speculative Motive

This is where Keynes really diverged from the classical view. He argued that people also hold money because they are waiting for a better investment opportunity. If someone expects that bond prices are going to drop, they might prefer to hold onto cash rather than invest. This speculative motive means that the demand for money is affected by interest rates and people’s expectations of future financial conditions.

Liquidity Preference Theory

Keynes called his theory of money demand the Liquidity Preference Theory. According to this theory, people want money because it’s liquid—they can use it whenever they need it, whether for everyday transactions or for taking advantage of investment opportunities. One of the major implications of Keynes’s view is that the demand for money is influenced by interest rates. When interest rates are high, people prefer to invest in assets like bonds that offer good returns. When rates are low, the opportunity cost of holding money is low, so people are more likely to hold onto their cash.

This relationship is what sets Keynes apart from the classical view: for Keynes, the demand for money is negatively related to the interest rate. Higher interest rates mean less demand for money, and lower rates mean more people are willing to hold cash.

Differences from the Quantity Theory

One of the major differences between the Keynesian and Quantity Theory approaches is that Keynes viewed the demand for money as flexible, or elastic—it changes based on interest rates and people’s preferences. In contrast, the Quantity Theory assumed a more rigid relationship between money supply and price levels.

Keynes also paid attention to economic downturns and recessions. He argued that during tough times, people might hoard money, and increases in the money supply don’t always lead to increased spending. This idea, known as a liquidity trap, shows why simply adding money to an economy doesn’t always boost economic activity.

Comparing the Quantity Theory and Keynesian Approach

To put it simply, the Quantity Theory of Money and the Keynesian Approach give us two different ways of looking at why people want money:

The Quantity Theory says that there’s a fixed and direct relationship between the money supply and the price level, assuming velocity and output are stable. It’s straightforward and emphasizes money’s role as a tool for transactions.

The Keynesian Approach sees the demand for money as more complex. It’s not just about transactions—it’s about dealing with uncertainty, waiting for opportunities, and the impact of interest rates. In this way, the demand for money isn’t fixed but can change based on people’s expectations and economic conditions.

The Keynesian Approach is generally seen as a more flexible and realistic explanation, especially during economic fluctuations. It’s particularly useful for understanding why, during times of uncertainty or economic downturn, increasing the money supply may not lead to more spending. Instead, people may save more, reducing the impact on aggregate demand.

Impact on Aggregate Demand

The key difference between these theories becomes even more apparent when we consider aggregate demand:

According to the Quantity Theory, if the money supply increases, people will spend more, leading directly to an increase in aggregate demand. This suggests that policies that expand the money supply should always boost economic activity.

The Keynesian Approach suggests that an increase in the money supply doesn’t necessarily lead to a proportional increase in aggregate demand. Other factors come into play, like people’s expectations, the interest rate, and whether the economy is already operating at full capacity. If people are pessimistic about the future, they might save rather than spend, which can limit the effectiveness of monetary expansion.

Real-World Implications

Both the Quantity Theory and Keynesian Approach have shaped how governments and central banks make decisions about economic policy:

During inflationary periods, the Quantity Theory can offer a clear solution—reducing the money supply can help bring down prices.

During economic downturns, however, the Keynesian perspective tends to be more useful. It shows that simply pumping money into the economy might not be enough if people are scared or unsure about the future. In such cases, additional tools like government spending and tax cuts (fiscal policies) may be more effective in reviving aggregate demand.

Think back to the global financial crisis of 2008. Central banks injected a lot of money into the financial system, but it didn’t lead to the expected increase in aggregate demand. People were anxious, and businesses were uncertain, so a lot of that money stayed put rather than flowing into new investments or increased consumption. This is a perfect example of Keynesian ideas in action.

Conclusion

So, why does understanding the demand for money matter? Both the Quantity Theory of Money and the Keynesian Approach offer us valuable insights into how money works in the economy, and when each theory is most applicable. The Quantity Theory gives a simple, proportional view of how changes in money supply affect price levels, which is useful when thinking about inflation. On the other hand, the Keynesian Approach provides a richer, behavior-driven perspective that helps explain how people’s motivations, interest rates, and expectations influence the economy.

These theories help explain why governments and central banks take the actions they do—whether it’s trying to control inflation or stimulate spending during tough times. Ultimately, both theories have their strengths, and understanding when to apply each one can make all the difference in effectively managing an economy.

FAQs:

What is the demand for money in macroeconomics?

The demand for money refers to the desire to hold cash or bank deposits rather than spending or investing them. It explains why people keep money at hand instead of immediately using it to buy goods, services, or assets.

What is the Quantity Theory of Money?

The Quantity Theory of Money suggests a direct relationship between the money supply and the overall price level. It states that if the money supply increases while output stays constant, prices will rise, resulting in inflation. Irving Fisher’s equation of exchange expresses this relationship as:

What assumptions does the Quantity Theory make?

The Quantity Theory assumes that the velocity of money and the economy’s output remain stable. It implies that increases in the money supply will proportionally raise the price level. This theory views money primarily as a tool for transactions.

What is the Keynesian approach to the demand for money?

John Maynard Keynes proposed that people hold money for different reasons beyond transactions, including precautionary needs and speculative motives. His theory, known as the Liquidity Preference Theory, emphasizes that the demand for money depends on interest rates, with people holding more cash when rates are low and investing when rates are high.

How does the Keynesian approach differ from the Quantity Theory?

While the Quantity Theory focuses on the money supply’s impact on prices, the Keynesian approach considers how interest rates, uncertainty, and future expectations influence money demand. Keynes argued that during downturns, increasing the money supply might not boost spending because people may save or hold onto cash.

What is the liquidity trap?

A liquidity trap occurs when increasing the money supply fails to stimulate spending because people prefer holding cash due to economic uncertainty or low interest rates. This concept, introduced by Keynes, highlights the limitations of monetary policy during deep recessions.

How do these theories impact aggregate demand?

The Quantity Theory suggests that expanding the money supply directly increases aggregate demand, leading to higher spending and economic activity. In contrast, the Keynesian approach points out that other factors—like interest rates and expectations—play a role, and monetary expansion alone may not be enough to boost demand during downturns.

Which theory is more relevant for policymakers?

Both theories offer useful insights. The Quantity Theory helps address inflation by controlling the money supply, while the Keynesian approach is more applicable during recessions or financial crises, where monetary policies need to consider interest rates, expectations, and consumer behavior. Central banks often use a mix of both theories to manage the economy effectively.

Thanks for reading! Share this with friends and spread the knowledge if you found it helpful.

Happy learning with MASEconomics