On April 11, 2026, the Orion capsule from NASA’s Artemis II mission splashed down in the Pacific Ocean, concluding a historic 10-day journey around the moon. The crew of four, Reid Wiseman, Victor Glover, Christina Koch, and Jeremy Hansen, became the first humans to travel beyond low Earth orbit since Apollo 17 in 1972. Their safe return was not just a triumph of human exploration. It was a powerful validation of a new economic model for space, one where public-private partnerships and commercial competition are as essential as rocket fuel.

While the world celebrated the crew’s return and marveled at the “Earthset” image they captured, our blue planet slipping behind the lunar horizon, a quieter revolution was unfolding. SpaceX has cut the cost of launching a kilogram to orbit from $54,000 to under $2,700. Blue Origin is building private space stations designed as orbital business parks. Venture capital firms poured a record $12.4 billion into space technology in 2025. The global space economy, currently valued at over $630 billion, is projected to reach $1.8 trillion by 2035, according to the World Economic Forum and McKinsey & Company. This is the Commercial Space Race: the transformation of space from a government-led scientific endeavor into a dynamic, market-driven economic frontier.

From Government Monopoly to Market Dynamism

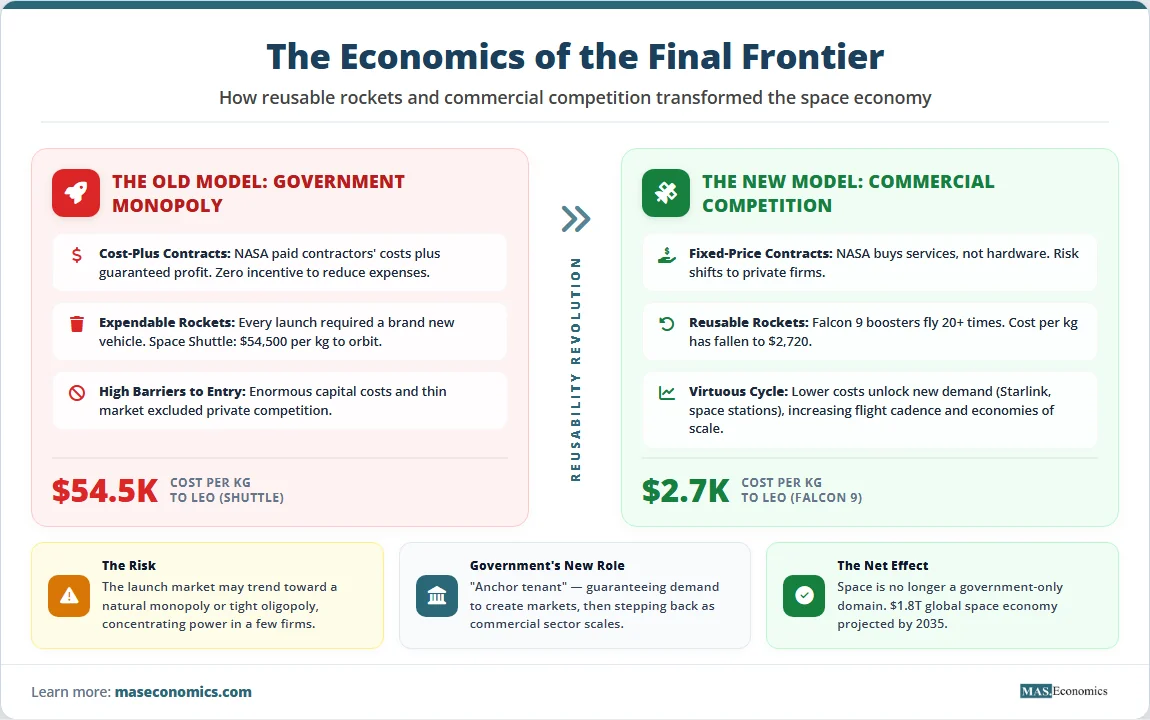

For most of the space age, access to orbit was defined by a single economic reality: it was extraordinarily expensive. NASA’s Space Shuttle, the workhorse of American human spaceflight for three decades, cost an estimated $54,500 per kilogram to reach Low Earth Orbit (LEO). European and Russian rockets were cheaper, but still commanded prices in the range of $8,000 to $10,000 per kilogram. These costs were not driven by greed but by physics and economics. Rockets were expendable; each mission required building an entirely new vehicle. The market was thin, dominated by government customers with specific national security or scientific requirements. There was little incentive to innovate on cost. The launch industry, in economic terms, resembled a natural monopoly sustained by high barriers to entry and cost-plus government contracting.

This model began to fracture in the early 2000s with the emergence of “NewSpace”, a wave of privately funded companies aiming to disrupt the status quo. The pivotal breakthrough was reusability. In December 2015, a SpaceX Falcon 9 booster flew back from space and landed vertically at Cape Canaveral. It was a moment that many in the aerospace industry had dismissed as impossible. That same booster has now flown more than 20 times. Reusability fundamentally altered the cost structure of space access. The most expensive part of a rocket, the first stage, no longer had to be thrown away after each flight. This single innovation has driven down the price of launch by more than an order of magnitude, from $54,500 per kilogram on the Shuttle to as little as $2,720 per kilogram on a Falcon 9, and potentially under $1,000 per kilogram on SpaceX’s in-development Starship.

The result has been a virtuous economic cycle: lower costs have unlocked new sources of demand, from satellite mega-constellations like Starlink to commercial space stations and lunar cargo delivery. This increased demand has, in turn, raised flight cadence, enabling companies to spread their enormous fixed costs across more missions and achieve genuine economies of scale. The Artemis program itself is a product of this new model. NASA’s Space Launch System (SLS) rocket and Orion capsule were developed through traditional cost-plus contracts and remain eye-wateringly expensive; each SLS launch is estimated to cost over $2 billion. But the Human Landing System that will carry astronauts from lunar orbit to the surface is being built by SpaceX, and a second lander is being developed by Blue Origin, both under fixed-price commercial contracts that shift financial risk from taxpayers to private companies. The Artemis II mission, which just returned from the moon, relied on commercial partners for everything from launch services to spacesuit components.

The timeline below traces the key milestones in this economic transformation, from the first privately developed rocket to reach orbit to the dawn of private space stations and the return of humans to the moon.

Timeline: Key Milestones in the Commercial Space Economy

| Year | Milestone | Economic Significance |

|---|---|---|

| 2008 | SpaceX Falcon 1 reaches orbit | First privately developed liquid-fueled rocket to reach orbit; proves NewSpace model viable. |

| 2012 | SpaceX Dragon docks with ISS | First commercial spacecraft to resupply the International Space Station under NASA contract. |

| 2015 | First Falcon 9 booster landing | Demonstrates reusable rocketry, the single most important cost-reduction innovation in spaceflight history. |

| 2020 | SpaceX Crew Dragon Demo-2 | First commercial flight to carry NASA astronauts to the ISS, ending US reliance on Russian Soyuz. |

| 2022 | Artemis I launches | Uncrewed test flight around the Moon; validates Orion and SLS for human missions. |

| 2024 | Intuitive Machines lands on Moon | First private company to successfully land on the lunar surface under NASA’s Commercial Lunar Payload Services program. |

| 2025 | Private space investment hits $12.4B | Record venture capital and private equity funding signals strong market confidence in space economy. |

| April 2026 | Artemis II crew returns from Moon | First human mission beyond LEO in over 50 years; validates public-private partnership model for deep space. |

| 2026 (planned) | Blue Origin’s New Glenn first flight | Introduces major new competitor in heavy-lift launch market; challenges SpaceX’s current dominance. |

|

||

The Artemis II crew’s safe return is more than a scientific milestone. The iconic “Earthset” image they captured, Earth dipping behind the lunar horizon, a view last seen by human eyes during Apollo, has become a symbol of this new era: one where economic forces of innovation, competition, and scale are as critical as rocket fuel. The question now is not whether humans will return to the moon, but what kind of economy they will build there.

Four Forces Shaping the Final Frontier

The commercial space race is not just a technological contest. It is a powerful demonstration of four fundamental economic principles that explain why costs are falling, who is winning, and what comes next.

Economies of Scale

Economies of scale refer to the cost advantages that firms achieve as their production volume increases. In most industries, higher output allows fixed costs, like factory construction, research and development, and specialized equipment, to be spread across more units, reducing the average cost per unit. The space industry is a particularly extreme case. Designing a new rocket costs billions of dollars. Building a launchpad costs hundreds of millions. For an expendable rocket, these enormous fixed costs are spread across a handful of launches per year, resulting in astronomical per-kilogram prices.

Reusability is a multiplier of economies of scale. A Falcon 9 booster that can be flown 10, 15, or even more than 20 times amortizes its manufacturing cost across many missions. As flight cadence increases, SpaceX launched 134 times in 2025, more than the rest of the world combined, operational efficiencies are discovered, supply chains mature, and the marginal cost of each additional flight falls. This creates a self-reinforcing virtuous cycle: lower costs unlock new demand (satellite internet, space tourism, lunar cargo), which increases flight cadence, which drives further economies of scale and even lower costs. Starship, designed to be fully reusable with rapid turnaround, could push this logic to its extreme, potentially reducing launch costs to just tens of dollars per kilogram, a price point that would fundamentally transform what is economically feasible in space.

Public Goods and Government’s Evolving Role

In economics, a pure public good is both non-rivalrous (one person’s consumption does not reduce availability to others) and non-excludable (it is difficult to prevent people from benefiting). Basic scientific knowledge about the cosmos, planetary defense against asteroid impacts, and climate monitoring from orbit all exhibit public good characteristics. Because private markets tend to underproduce public goods, firms cannot easily capture the full social benefit of their investment; there is a strong economic rationale for government involvement in space.

However, the nature of that government involvement has fundamentally changed. During Apollo, NASA was both the designer and the customer; it told contractors exactly what to build and how to build it, reimbursing their costs plus a guaranteed profit. This cost-plus model eliminated financial risk for contractors but also eliminated any incentive to control costs. The result was the Space Shuttle and SLS, marvels of engineering that are also among the most expensive transportation systems ever built.

The new model, pioneered by NASA’s Commercial Crew and Commercial Cargo programs, repositions government as an “anchor tenant” rather than a sole operator. NASA specifies the service it wants, e.g., delivery of cargo or crew to the ISS, and private companies compete to provide that service at a fixed price. By guaranteeing demand, NASA helps create a market that enables private firms to achieve the economies of scale necessary to lower costs for all users. This public-private partnership leverages public funding to stimulate private innovation, ensuring that public goods are provided while fostering a competitive commercial market. The Artemis program’s Human Landing System, procured through this commercial model, is estimated to cost a fraction of what a traditional cost-plus development would have required.

Innovation and Creative Destruction

Joseph Schumpeter’s concept of creative destruction describes how innovation disrupts and ultimately destroys old industries to create new ones. The commercial space race is a textbook example. Reusable rockets have effectively “destroyed” the business model of the traditional expendable launch industry, which was built on cost-plus government contracts and low flight rates. Companies that failed to adapt have lost market share or exited the launch business entirely.

But creative destruction is not just about destruction. It is about the reallocation of capital and talent to more productive uses. The collapse in launch costs has opened the door to entirely new industries that were previously economically impossible. Constellations of thousands of satellites providing global broadband internet, SpaceX’s Starlink now has over 5 million subscribers and generated an estimated $6.8 billion in revenue in 2025. Private space stations, like Blue Origin’s Orbital Reef and Voyager Space’s Starlab, are being developed as destinations for research, manufacturing, and tourism. In-space refueling depots, orbital debris removal services, and asteroid mining are transitioning from science fiction to venture-backed business plans. This wave of innovation is what excites investors, who see opportunities not just in launch but across the entire space economy value chain.

Natural Monopoly

A natural monopoly occurs when a single firm can supply an entire market’s demand at a lower cost than two or more firms could, due to extremely high fixed costs and significant economies of scale. The launch market, particularly for large payloads to orbit, has characteristics of a natural monopoly. The capital required to design, build, and certify a new heavy-lift rocket is measured in billions of dollars. The market for large launches, while growing, is still relatively small compared to other transportation industries. SpaceX’s current dominance, with its Falcon 9 offering a price of approximately $2,720 per kilogram, far below the industry average of $15,000 to $20,000 per kilogram, seems to support the natural monopoly thesis.

However, a true natural monopoly would see all competitors exit the market, leaving a single supplier. That has not happened. Blue Origin’s New Glenn rocket, United Launch Alliance’s Vulcan Centaur, and Europe’s Ariane 6 are all actively competing for launch contracts. National space programs in China and India have their own domestic launch capabilities. The market appears to be evolving toward an oligopoly, a small number of dominant global players competing on price and reliability, rather than a pure monopoly. Furthermore, as launch demand diversifies across different orbits, payload sizes, and mission profiles, multiple providers may find profitable niches. A rocket optimized for launching thousands of small satellites to low Earth orbit may be poorly suited for sending a large probe to Jupiter. The launch market of the future may resemble the airline industry: a few global giants alongside numerous regional and specialized carriers.

The Collapse of Launch Costs

The chart below compares the estimated cost to launch one kilogram of payload to Low Earth Orbit (LEO) for various launch vehicles, adjusted to 2026 dollars. The difference between legacy systems and modern reusable rockets is stark, a reduction of more than 95% in some cases. This cost collapse is the single most important economic fact of the new space age.

Cost Per Kilogram to Low Earth Orbit (LEO) by Launch Vehicle (2026 USD)

Sources: Data compiled from CSIS Aerospace Security Project, Our World in Data, and company-reported pricing. All values adjusted to 2026 USD for comparability.

The following table provides a snapshot of the key players in the 2026 commercial space economy, from established giants to emerging challengers, and their primary economic activities.

Key Players in the 2026 Commercial Space Economy

| Company/Entity | Primary Focus | Economic Advantage | 2025 Estimated Revenue |

|---|---|---|---|

| SpaceX (USA) | Launch (Falcon, Starship), Starlink, Lunar Lander | Reusability, vertical integration, lowest launch costs | $15B+ (private estimate) |

| Blue Origin (USA) | Launch (New Glenn), Space Station (Orbital Reef), Lunar Lander | Long-term vision, significant capital from Jeff Bezos | ~$2B (private estimate) |

| United Launch Alliance (USA) | Launch (Vulcan Centaur, Atlas V) | Proven reliability for national security missions | ~$3.5B |

| NASA (USA) | Deep space exploration, R&D, anchor contracts | Guaranteed demand as “anchor tenant” for new markets | $27.2B (FY2025 budget) |

| CNSA (China) | Tiangong Space Station, Lunar and Mars missions | State-directed funding, long-term strategic planning | ~$14B (estimated) |

| ISRO (India) | Cost-effective satellite launch, Gaganyaan human spaceflight | Highly efficient, low-cost engineering and operations | ~$1.9B |

|

|||

The New Distribution of Gains and Losses

The commercial space race is not a tide that lifts all boats equally. It creates clear winners and introduces new risks for those left behind.

The Winners

Cost-sensitive industries and new space entrants are the immediate beneficiaries. Satellite internet providers like Starlink and Amazon’s Project Kuiper, Earth observation companies like Planet Labs, and even pharmaceutical firms exploring microgravity manufacturing gain access to space at a fraction of historical costs. The barriers to entry for space-based business models have fallen dramatically, unleashing a wave of entrepreneurial activity.

Nations with agile commercial space sectors are best positioned to capture the economic benefits. The United States, with its ecosystem of private space companies, venture capital funding, and supportive public policy (including the regulatory framework of the Federal Aviation Administration’s Office of Commercial Space Transportation), currently leads. However, nations like India, with its incredibly cost-effective space program, are becoming major players. The Indian Space Research Organisation (ISRO) has built a reputation for delivering missions at a fraction of the cost of Western counterparts, and its commercial arm is capturing a growing share of the global launch market.

Investors and the broader economy stand to gain significantly. The space economy is one of the few sectors projected to grow at double-digit rates for the foreseeable future. Venture capital and private equity are flowing into the sector, with firms like Seraphim Space and Space Capital tracking record investment levels. More importantly, space-based technologies, from GPS and weather forecasting to global communications, are foundational to the modern global economy, creating value across agriculture, logistics, finance, and national security. A 2024 study by the Satellite Industry Association estimated that the global satellite industry alone generated $384 billion in revenue, enabling trillions in downstream economic activity.

The Losers

Legacy aerospace giants built on cost-plus government contracts face an existential threat. Companies that failed to invest in reusability and cost reduction are losing market share to more agile competitors. United Launch Alliance, a joint venture of Boeing and Lockheed Martin that once held a monopoly on US national security launches, is now competing fiercely with SpaceX and racing to develop its own reusable capabilities. In Europe, Arianespace is facing similar pressures, with its new Ariane 6 rocket struggling to compete on price with Falcon 9.

Nations without a space program or domestic launch capability risk being left out of a major future economic sector. The “space divide” could exacerbate global inequality, as countries without the means to access or benefit from space-based assets lose out on economic growth, strategic advantages, and the ability to shape the rules of the emerging space economy. A 2025 report from the OECD highlighted that over 90% of global space manufacturing revenue is concentrated in just five countries.

Workers in the traditional aerospace manufacturing sector may face disruption as the industry pivots to new production methods. Building a bespoke, expendable rocket requires a different skill set than mass-producing reusable boosters. The shift toward vertical integration, where companies like SpaceX manufacture most components in-house rather than relying on a vast network of subcontractors, is also reshaping the aerospace workforce. Retraining programs and regional economic development strategies will be essential to manage this transition.

What the Commercial Space Race Teaches Economics

The commercial space race offers four lessons that extend far beyond the aerospace industry.

First, the government’s role in frontier industries is not obsolete; it has evolved. From being a sole operator, the state’s most powerful role is now as an “anchor customer” and investor in enabling infrastructure. By guaranteeing demand for new services (like crewed flights to the ISS or lunar cargo delivery), governments can catalyze private investment, reduce risk for early movers, and accelerate the virtuous cycle of economies of scale. The public sector’s strategic investments can unlock private sector innovation in ways that direct government operation cannot.

Second, reusability is the single most disruptive innovation in the history of spaceflight. It fundamentally changes the cost structure of accessing space, transforming it from a bespoke, one-off endeavor into a potentially high-volume, industrial operation. This shift unlocks economies of scale and makes space a viable domain for commercial activity far beyond communications satellites. The lesson for other capital-intensive industries, from aviation to energy, is that reusability and standardization can be more powerful drivers of cost reduction than incremental technological improvements.

Third, while the launch market may trend toward a global oligopoly, the overall space economy is far more diverse and competitive. The real value creation will likely come not just from getting to space, but from what you do once you’re there. This creates opportunities for startups and established companies alike in areas like in-space manufacturing, satellite servicing, orbital logistics, and resource utilization. As market structures in microeconomics teach us, different segments of an industry can have very different competitive dynamics.

Fourth, the space economy illustrates the power of fixed-price commercial contracts over cost-plus government contracting. By shifting financial risk from taxpayers to private companies and allowing firms to innovate on cost and schedule, the commercial model has delivered capabilities faster and cheaper than traditional procurement. This lesson is now being applied in other government domains, from defense contracting to infrastructure development. The Coase Theorem reminds us that clearly defined property rights and competitive markets can often solve problems more efficiently than centralized planning.

MASEconomics Explains

Conclusion

As the Artemis II astronauts drifted back to Earth and their Orion capsule splashed down in the Pacific, they were not just returning home. They were returning to a planet where the economics of space had been fundamentally and irrevocably changed. The cost of reaching orbit has collapsed. The market for space services is booming. And the model for exploration has shifted from government monopoly to public-private partnership. The commercial space race is far more than a technological contest; it is a powerful demonstration of how market forces, when combined with strategic public investment, can unlock new frontiers. What humanity chooses to build in space, and who gets to participate in that economy, will be one of the defining questions of the coming century. The final frontier is no longer just a place for exploration; it is the new landscape for commerce, competition, and growth.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.