Central banking sits at the centre of every modern economy. The Federal Reserve, the European Central Bank, the Bank of Japan, and the Bank of England together set the price of money for roughly 60 percent of global GDP. As of May 2026, their policy rates span an unusually wide range: 3.50 to 3.75 percent at the Fed, 2.00 percent at the ECB deposit facility, 3.75 percent at the Bank of England, and 0.75 percent at the Bank of Japan after the BoJ’s first hiking cycle in three decades. That divergence is the clearest single illustration of what central banking does, and what it cannot escape.

Modern central banks share four jobs: managing the money supply, setting short-term interest rates, supervising the banking system, and acting as lender of last resort during financial stress. The instruments differ across institutions, but the underlying logic is the same. A central bank steers a short-term rate, the financial system transmits that rate into credit and asset prices, and credit conditions move spending, employment, and inflation. The rest of this article unpacks how that chain works, who controls it, and where the framework is being stretched.

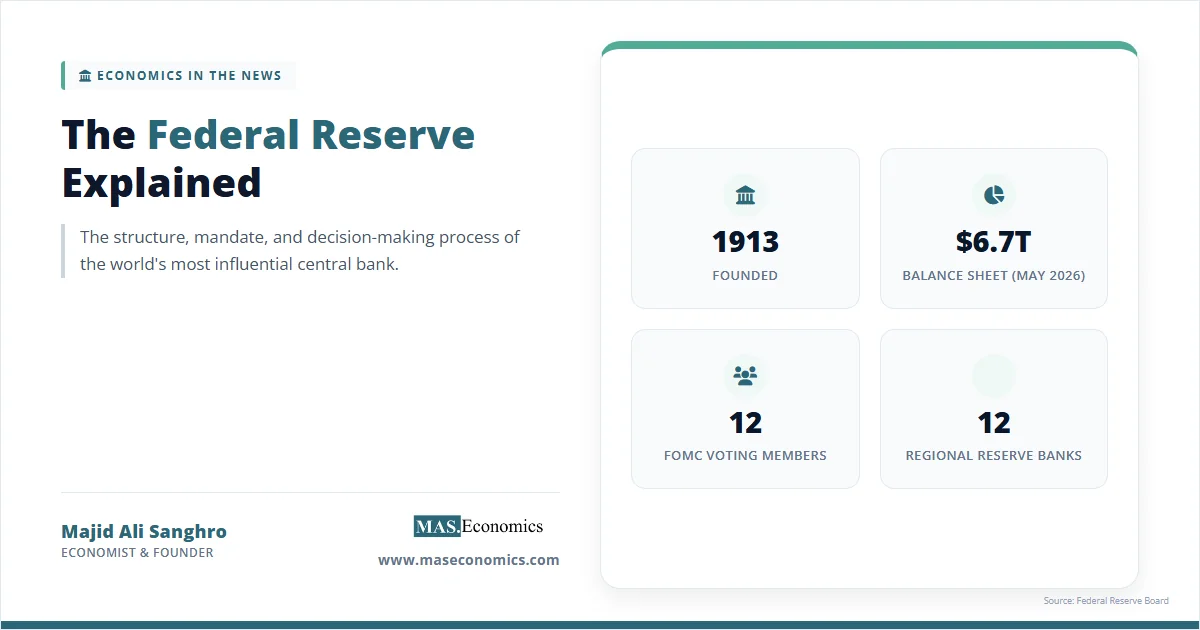

Quick reference. Federal Reserve founded 1913 (dual mandate: maximum employment and price stability). European Central Bank founded 1998 (primary mandate: price stability at 2 percent). Bank of England founded 1694 (operational independence since 1997, 2 percent CPI target). Bank of Japan founded 1882 (2 percent inflation target, abolished yield curve control in March 2024).

What Central Banking Actually Is

Central banking is the practice of managing a national currency, the banking system, and short-term interest rates through a single public institution. The institution has a monopoly on issuing legal tender, holds the reserve accounts of commercial banks, and conducts monetary policy on behalf of the state. That bundle of powers is what separates a central bank from any other financial institution.

Three features define the modern central bank. The first is the issuance monopoly. Only the central bank can create base money: physical currency plus commercial bank reserves held at the central bank. The second is the reserve-account function. Every commercial bank holds an account at its central bank, and payments between banks ultimately settle on the central bank’s balance sheet. The third is monetary policy authority. By changing the price or quantity of reserves, the central bank influences the entire term structure of interest rates.

These functions did not all emerge at once. The earliest central banks were created to finance wars or to stabilise a chaotic note-issuing system. The modern policy mandate, with explicit inflation targets and independence from day-to-day political control, is a late twentieth-century construction, formalised in most advanced economies between 1989 and 1998.

From the Riksbank to the Modern Mandate

The Swedish Riksbank, chartered in 1668, is the oldest central bank still in operation. The Bank of England followed in 1694, founded to lend the Crown 1.2 million pounds at 8 percent to finance the Nine Years’ War against France. The Bank of France was established by Napoleon in 1800, the Nederlandsche Bank in 1814, and the Reichsbank in 1876. Each of these institutions began as a privileged commercial lender to the state and only gradually acquired the public-policy role.

The United States took longer. The First Bank of the United States (1791) and Second Bank (1816) were both shut down after 20-year charters expired amid political opposition. The country operated without a central bank from 1836 until the Panic of 1907, when a private syndicate organised by J.P. Morgan had to act as the de facto lender of last resort. The Federal Reserve Act of 1913 created the present system, with twelve regional Reserve Banks and a Board of Governors in Washington.

The transformation from the bank of the state into an independent policy authority happened mostly after 1989. New Zealand was first, with the Reserve Bank Act 1989 introducing the world’s first explicit inflation target. Canada followed in 1991, the UK in 1992, and Sweden in 1993. The Bank of England received operational independence in 1997, and the European Central Bank was created with statutory independence in 1998 under the Maastricht Treaty. By 2000, inflation targeting under an independent central bank had become the standard framework across advanced economies.

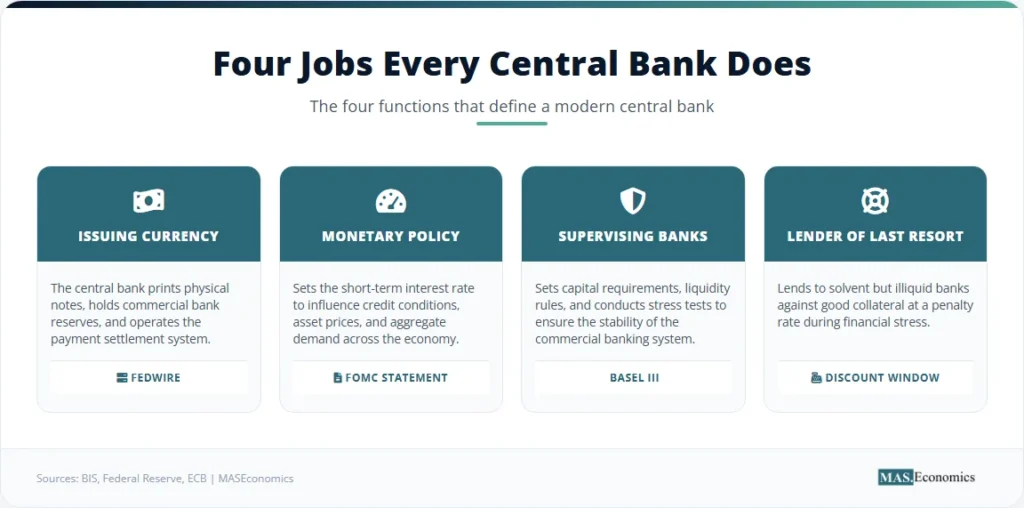

Four Jobs Every Central Bank Does

Modern central banks share four core functions. Each is documented in the founding statutes of the major institutions and reaffirmed in their annual reports.

Issuing currency and managing reserves. The central bank prints physical notes, holds the reserve accounts of commercial banks, and operates the payment system that settles interbank transactions. In 2024, the Bank for International Settlements reported that central-bank-operated real-time gross settlement systems processed payments worth roughly five times annual world GDP.

Conducting monetary policy. The central bank sets a short-term interest rate, the price at which banks borrow reserves overnight. Changes in this rate are transmitted through the yield curve into mortgage rates, business loans, equity valuations, and the exchange rate. The Federal Reserve’s Monetary Policy Report and the ECB’s quarterly Economic Bulletin document this transmission for the US and the euro area.

Supervising the banking system. Central banks (in some jurisdictions jointly with separate regulators) set capital requirements, liquidity rules, and stress tests for commercial banks. The Basel III framework, agreed under the auspices of the Bank for International Settlements, defines the minimum standards that supervisors apply.

Acting as the lender of last resort. When a solvent bank cannot fund itself in the market, the central bank lends against good collateral at a penalty rate. The principle dates to Walter Bagehot’s 1873 book Lombard Street, and it remains operational in the Federal Reserve’s discount window, the ECB’s marginal lending facility, and the Bank of England’s discount window facility. The lender of last resort function was activated repeatedly during 2008, 2020, and in March 2023, due to banking stress around Silicon Valley Bank and Signature Bank.

Secondary functions vary by jurisdiction. Foreign exchange reserve management, public debt management on behalf of the Treasury, financial-stability macroprudential policy, and increasingly the design of central bank digital currencies all fall within the contemporary remit.

How Major Central Banks Compare

The four largest reserve-currency central banks operate under different mandates, governance structures, and policy frameworks. The differences explain why their interest rates can move in opposite directions, as they have through 2024 to 2026.

| Feature | Federal Reserve | European Central Bank | Bank of England | Bank of Japan |

|---|---|---|---|---|

| Founded | 1913 | 1998 | 1694 | 1882 |

| Mandate | Dual: maximum employment and price stability | Primary: price stability at 2% | Single: 2% CPI target, subject to financial stability | Price stability at 2%, financial stability |

| Decision body | FOMC (12 voters) | Governing Council (26 members) | MPC (9 members) | Policy Board (9 members) |

| Meeting cadence | 8 per year | 8 per year | 8 per year | 8 per year |

| Main policy rate (May 2026) | Fed funds target 3.50–3.75% | Deposit facility 2.00% | Bank Rate 3.75% | Uncollateralised O/N call 0.75% |

| Balance sheet (% of GDP) | ~22% | ~37% | ~26% | ~120% |

| Operating framework | Ample reserves (IORB + ON RRP floor) | Floor system (DFR) | Floor system (Bank Rate) | Negative-rate exit, QQE wind-down |

| Independence statute | Federal Reserve Act 1913 (1951 Accord) | TFEU Article 130 | Bank of England Act 1998 | Bank of Japan Act 1997 |

|

||||

The table makes the contrast concrete. The Fed runs the only formal dual mandate, while the ECB has a hierarchical mandate in which price stability dominates and economic support is secondary. The Bank of Japan’s balance sheet, at roughly 120 percent of GDP, dwarfs every peer institution. The BoJ is the only major central bank that has held more than half its sovereign bond market, the outcome of two decades of quantitative and qualitative easing.

Governance also varies. The Federal Open Market Committee has 12 voting members: the seven Board governors plus five of the twelve regional Reserve Bank presidents, with the New York Fed president always voting. The ECB Governing Council has 26 members (six Executive Board members plus the 20 national central bank governors), of whom 21 vote on a rotating basis. The Bank of England’s Monetary Policy Committee has 9 members, five internal and four external. The Bank of Japan Policy Board has 9 members appointed by the cabinet with Diet consent.

The Six Tools of Monetary Policy

Central banks have a broader toolkit than the textbook trio of open market operations, discount rate, and reserve requirements. Modern practice involves six distinct instruments, deployed in different combinations depending on whether reserves are scarce or ample and whether the policy rate is constrained by the zero lower bound.

Administered rates. Since 2008, most major central banks have moved to a “floor system” in which the policy rate is set directly by paying interest on reserves. The Fed pays interest on reserve balances (IORB) at 3.65 percent as of May 2026, and offers an overnight reverse repo (ON RRP) facility at 3.55 percent. The ECB sets the deposit facility rate (DFR) as its primary stance variable. This replaces the older mechanism of scarce-reserve open market operations.

Open market operations. Outright purchases and sales of government securities, or repurchase agreements collateralised by them, adjust the quantity of reserves in the system. Under ample reserves, open market operations are used less for daily rate management and more for balance sheet expansion or contraction.

Standing facilities. The lending and deposit windows that bound the policy corridor. The Fed’s discount window, the ECB’s marginal lending facility, and the Bank of England’s operational standing lending facility all serve this purpose, lending against eligible collateral at a penalty rate above the policy rate.

Reserve requirements. A specified fraction of deposits that banks must hold as reserves at the central bank. The Fed reduced its reserve requirement ratio to zero in March 2020 and has not raised it since. The ECB requires 1 percent, while the People’s Bank of China actively uses the reserve requirement ratio as a primary policy instrument, currently around 6.5 percent for large banks. The monetary policy tools toolkit varies across institutions because the underlying operating regime varies.

Quantitative easing and quantitative tightening. Outright purchases of long-duration assets to compress term premia at the zero lower bound. The Fed’s balance sheet peaked at USD 8.97 trillion in April 2022 and has been reduced by roughly USD 2.1 trillion through quantitative tightening since then. The ECB’s APP and PEPP portfolios are being run down. The BoJ began winding down its JGB and ETF purchases in March 2024.

Forward guidance. Verbal commitments about the future path of the policy rate. Forward guidance can be qualitative (data-dependent), data-based (“rates will stay low at least until end-2023”), or state-contingent (“until inflation has been at 2 percent for some time”). The 2013 Taper Tantrum and the 2020 average inflation targeting framework review are the canonical episodes that shape current practice.

The Policy Rate Path Since 2000

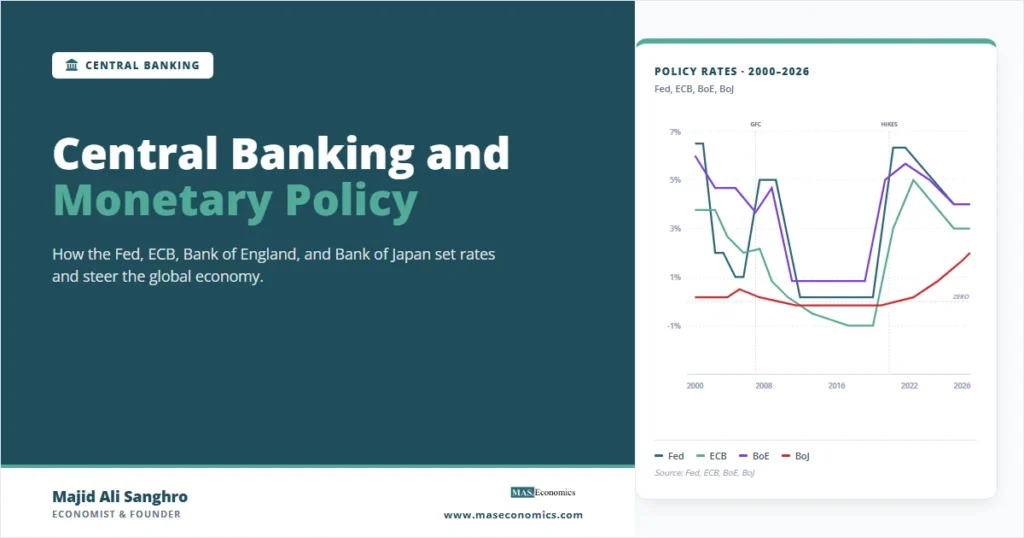

The history of central banking since 2000 is best told through the policy rates themselves. Three cycles stand out: the synchronised tightening of 2004 to 2007, the synchronised cut to near-zero from 2008 to 2009, and the post-COVID divergence that began in 2022. The fourth phase, the current 2024 to 2026 cycle, is the first in which the four major central banks are moving in distinctly different directions at the same time.

Three episodes deserve attention. The 2007 to 2009 collapse from 5.25 percent (Fed), 4.00 percent (ECB), 5.50 percent (BoE), and 0.50 percent (BoJ) down to the effective zero lower bound represents the largest synchronised cut in central banking history. The Bank of Japan had already been there since the late 1990s. The other three joined in. For the next decade, conventional rate policy was effectively suspended, replaced by quantitative easing and forward guidance.

The 2022 to 2023 tightening was the steepest in 40 years. The Fed raised the upper bound from 0.25 percent to 5.50 percent in 16 months. The ECB lifted the deposit facility rate from -0.50 percent to 4.00 percent over the same period, abandoning eight years of negative rates. The Bank of England moved from 0.10 percent to 5.25 percent. The Bank of Japan held -0.10 percent throughout, finally exiting negative rates in March 2024 and reaching 0.75 percent by early 2026 in its first hiking cycle since 1989. The 2026 divergence pattern visible at the right edge of the chart is unusual in the post-Bretton Woods era.

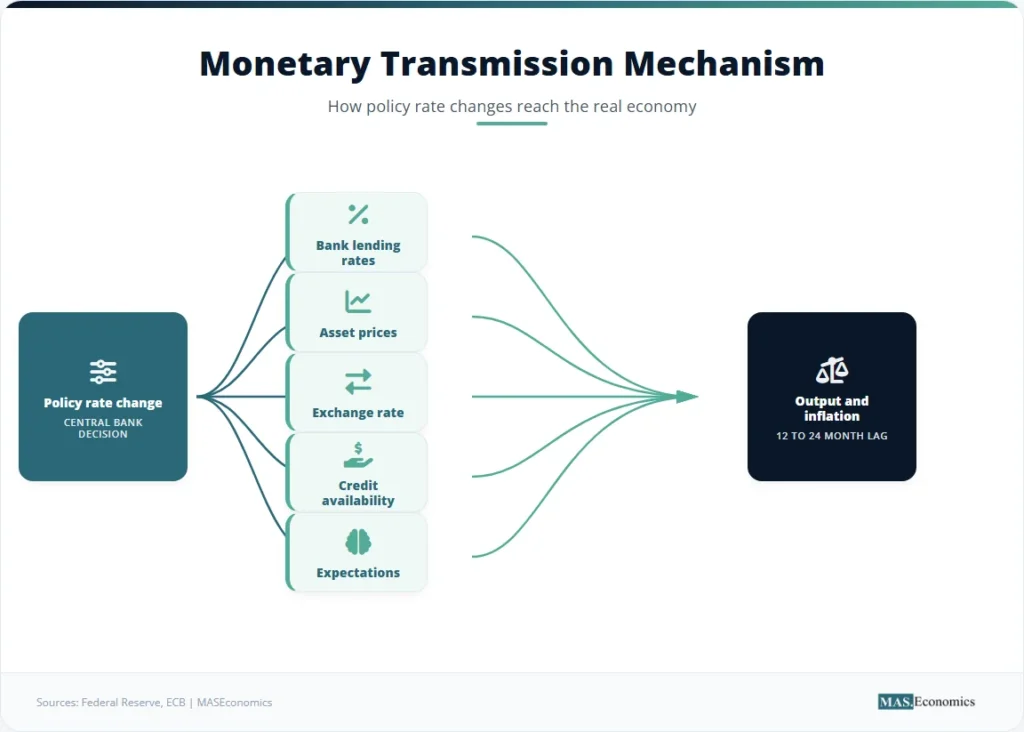

How Monetary Policy Reaches the Economy

A change in the policy rate works through five transmission channels, all operating with lags of six months to two years. The Federal Reserve estimates that the full effect of a rate change on output peaks at around 12 to 18 months, and the effect on inflation at around 18 to 24 months. These monetary policy lags are why central banks must act on inflation forecasts rather than current data.

The five channels are the interest rate channel (policy rate moves bank lending rates and bond yields, which affect investment and durable goods consumption), the credit channel (rate changes affect bank willingness to lend and borrower balance sheets), the asset price channel (equity and house prices respond to discount rates, generating wealth effects), the exchange rate channel (higher domestic rates appreciate the currency, suppressing net exports), and the expectations channel (credible forward guidance moves long rates and inflation expectations before any action is taken). The monetary transmission mechanism integrates these into the conventional New Keynesian framework.

The relative strength of each channel varies across economies. In the United States, where roughly 30 percent of household wealth is in equities, and most mortgages are 30-year fixed, the asset price channel is strong but the interest rate channel passes slowly to existing mortgages. In the United Kingdom, where most mortgages reset within five years, the interest rate channel hits households quickly. In the euro area, where bank lending dominates corporate finance, the credit channel does more of the work than in the US, where corporate bond markets are deeper.

Expansion, Contraction, and the Choice Between Them

Monetary policy operates in two broad directions. Expansionary policy lowers interest rates, expands the central bank balance sheet, or both, with the aim of raising aggregate demand. Contractionary policy does the reverse. The decision rule that links these directions to the state of the economy is the central question of monetary policy.

The most influential formalisation is the Taylor Rule, proposed by John Taylor in 1993. The rule prescribes a policy rate equal to the neutral rate plus 1.5 times the inflation gap (current inflation minus target) plus 0.5 times the output gap (current output minus potential). When inflation is above target, the policy rate should rise more than one-for-one, the so-called Taylor principle that ensures real rates rise when inflation rises. Central banks do not mechanically follow the rule, but every major central bank publishes Taylor-type benchmarks for comparison.

Expansionary policy faces a hard constraint at the zero lower bound. Once the policy rate is at or near zero, further cuts are difficult because savers can hold physical cash at zero return. The ECB, the Swiss National Bank, and the Bank of Japan all tested negative interest rates in the 2014 to 2024 period. The evidence is mixed: negative rates eased financial conditions but compressed bank net interest margins and produced political pushback. Most central banks now treat the zero lower bound as the effective floor.

Contractionary policy faces a different constraint. Rate increases work with long lags and produce visible costs (higher unemployment, mortgage stress) well before they show measurable benefits in lower inflation. The 2022 to 2023 cycle illustrated this clearly: unemployment in the US rose modestly while inflation fell from 9.1 percent peak to under 3 percent by mid-2024. Some commentators argued this was the cleanest soft landing on record. Others argued it was largely supply-side normalisation that would have occurred without the rate increases.

Inflation Targeting as the Dominant Framework

Since 1989, inflation targeting has become the standard monetary policy framework across advanced economies and many emerging markets. The framework has three elements: a numerical inflation target (typically 2 percent), public commitment by the central bank to achieve it, and an explicit accountability mechanism. New Zealand was first in 1989, followed by Canada (1991), the UK (1992), Sweden (1993), Australia (1993), the euro area (1998 under a different name), and Japan (2013).

The Fed adopted a formal 2 percent target only in January 2012, and modified it to “average inflation targeting” in August 2020. Under average inflation targeting, the Fed aims to achieve inflation that averages 2 percent over time, allowing inflation to run above 2 percent for some period to offset earlier shortfalls. The 2020 framework review explicitly acknowledged that policy at the zero lower bound for extended periods had produced persistent inflation undershoots. The framework was reviewed again in 2025 to clarify how the average is measured. The broader literature on inflation targeting has examined alternatives including price-level targeting, nominal GDP targeting, and the original Friedman k-percent money growth rule, but none has displaced the 2 percent target as the operational standard.

Critics raise three concerns. First, the 2 percent target is empirically grounded but theoretically arbitrary, chosen partly to provide a buffer against the zero lower bound rather than from any optimal-policy calculation. Second, inflation targeting takes the central bank’s eye off financial stability, a critique that intensified after 2008. Third, the framework assumes the central bank can credibly commit to its target, which becomes harder when fiscal authorities issue debt at levels that may eventually require central bank monetisation.

Where Monetary Policy and Fiscal Policy Diverge

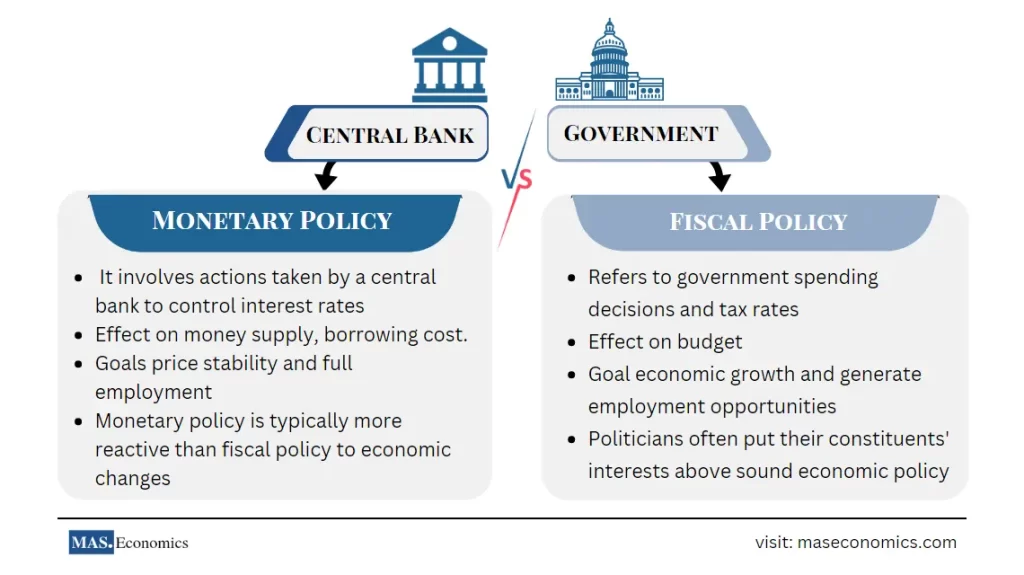

Monetary and fiscal policy share an objective (macroeconomic stability) but differ in instruments, decision-makers, and lags. Monetary policy adjusts interest rates and the central bank balance sheet through an independent authority. Fiscal policy adjusts government spending and taxation through the legislature and the executive. Both affect aggregate demand, but they do so through different channels and at different speeds.

Three operational differences matter. Monetary policy is faster: a central bank can change its policy rate within hours of a meeting, while fiscal policy typically requires legislation that takes weeks or months. Monetary policy is more reversible: a rate cut can be undone at the next meeting, while a tax cut or spending programme is politically costly to unwind. Monetary policy is more centralised: a small committee at one institution decides, rather than a legislature with competing interests.

The relationship is also two-way. Central bank actions affect the government’s borrowing costs (through the term structure of yields) and the value of central bank securities holdings (gains and losses that flow to or from the Treasury). Large fiscal deficits can constrain monetary policy by raising the risk that disinflation requires unacceptably high real rates. This concern, formalised in the literature on “fiscal dominance”, has gained renewed attention as advanced-economy government debt has risen to levels last seen after World War II.

The Independence Argument and Its Critics

Modern central banks operate with a degree of independence from the executive and the legislature that is unusual among public institutions. The Federal Reserve sets policy without congressional approval; the ECB cannot accept instructions from any government under Article 130 of the Treaty on the Functioning of the European Union; the Bank of England has had operational independence since 1997. The empirical case for central bank independence rests on cross-country evidence that more independent central banks have, on average, delivered lower inflation without higher unemployment.

The argument has theoretical foundations in the time-inconsistency literature of Kydland and Prescott (1977) and Barro and Gordon (1983). A government that controls monetary policy faces a temptation to generate surprise inflation to lower the real value of debt or to boost employment before an election. Rational agents anticipate this, raising inflation expectations and producing higher inflation without the temporary output boost. Delegating policy to an independent central bank with a price-stability mandate removes the temptation and restores credibility.

The critique has three strands. First, independence is granted by legislatures and can be removed by them, so the de jure independence is always conditional on the de facto political settlement. Second, central banks have expanded into areas (financial stability, climate, distribution) where the technocratic justification is weaker. Third, the post-2008 expansion of central bank balance sheets has blurred the line between monetary and fiscal policy in ways that strain the independence framework. The recent 2025-2026 Fed transition and the long-running debate over political systems and monetary policy show that the question is still open.

The Frontier: CBDCs, Climate, and Digital Money

Three developments are reshaping the central bank toolkit. The first is central bank digital currency. The Bank for International Settlements 2024 survey found that 134 jurisdictions are exploring CBDCs, 44 are running pilots, and three have launched (the Bahamas, Jamaica, and Nigeria). The People’s Bank of China’s e-CNY is the most advanced large-economy project, with active retail use in selected cities. The ECB’s digital euro project is in the preparation phase, with a launch decision pending. The Fed has not committed to a retail CBDC but is researching wholesale applications.

The second is the climate question. The Network for Greening the Financial System, founded in 2017, now includes 138 central banks and supervisors. The debate is whether central banks should incorporate climate risk into their monetary policy and supervisory frameworks, and how. The ECB has tilted its corporate bond purchases toward issuers with lower carbon footprints. The Bank of England has run climate stress tests for the largest UK banks. The Fed has been more cautious, framing climate involvement as financial stability rather than monetary policy work.

The third is the future role of central banks in an increasingly digital monetary system, where private stablecoins, tokenised deposits, and CBDCs compete for the same functional space that physical currency and bank deposits have occupied for two centuries. The institutional design choices being made now will shape the next 50 years of monetary policy.

MASEconomics Explains

Four economic concepts behind modern central banking

These concepts are explored in depth across our educational articles library.

Explore the MASEconomics BlogConclusion

Central banking has become the principal mechanism through which modern economies stabilise prices, manage credit, and respond to financial stress. The four major reserve-currency central banks share a common toolkit (administered rates, open market operations, standing facilities, reserve requirements, asset purchases, and forward guidance) but differ in mandate, governance, and operating framework. Their policy rates as of May 2026 span a range from 0.75 percent at the Bank of Japan to 3.75 percent at the Bank of England, reflecting different inflation paths and different positions in the post-pandemic cycle. Independence from short-term political pressure, an explicit inflation target, and a credible commitment to lender-of-last-resort actions are the three institutional features that distinguish modern central banking from its pre-1989 predecessors. The frontier debates over digital currency, climate, and the boundary between monetary and fiscal policy are now reshaping the framework that took shape across the 1990s.

Frequently Asked Questions

What is the main role of a central bank?

A central bank issues the national currency, sets short-term interest rates, supervises commercial banks, and acts as lender of last resort during financial stress. These four functions together give the central bank operational responsibility for monetary and financial stability.

How is monetary policy different from fiscal policy?

Monetary policy is conducted by the central bank and works through interest rates and the central bank balance sheet. Fiscal policy is conducted by the government and works through taxation and public spending. Monetary policy is typically faster to enact and easier to reverse, while fiscal policy can target specific sectors or income groups.

Why do central banks aim for 2 percent inflation rather than zero?

A 2 percent target provides a buffer against the zero lower bound on nominal interest rates, allows for measurement error in inflation indices, and gives the economy room to adjust relative prices and wages without negative nominal changes. The target is empirical rather than theoretical, and major central banks adopted it between 1989 and 2013.

What are the main tools of monetary policy?

The six core tools are administered rates (such as interest on reserves), open market operations, standing facilities (discount window, marginal lending), reserve requirements, large-scale asset purchases (quantitative easing), and forward guidance. Modern central banks use these instruments in combination, with the mix depending on whether the policy rate is constrained by the zero lower bound.

Who actually controls monetary policy decisions?

Monetary policy is set by a committee at the central bank, typically with 8 to 26 voting members appointed by the executive and confirmed by the legislature. The Federal Open Market Committee, the ECB Governing Council, the Bank of England Monetary Policy Committee, and the Bank of Japan Policy Board are the major examples. Their statutory independence from day-to-day political instruction is the institutional foundation of modern central banking.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics