On March 19, 2020, with the COVID-19 panic cresting in funding markets, the Federal Reserve announced that its dollar liquidity swap arrangements with five major foreign central banks were being supplemented with temporary lines to nine additional jurisdictions. Within a fortnight, foreign central banks had drawn more than $200 billion through these facilities, with the European Central Bank, Bank of Japan, and Bank of England the largest users. Less than a year later, almost all of that balance had been repaid. The episode was the third time in fifteen years that central bank swap lines had been used at scale to extinguish a global dollar funding fire, and it confirmed something already implicit in the architecture: when offshore dollar markets seize, the Federal Reserve is the only lender that can fix them.

The mechanism is administratively simple but politically consequential. A swap line lets a foreign central bank borrow dollars from the Federal Reserve against an equivalent value of its own currency, on-lend those dollars to commercial banks in its jurisdiction, and reverse the trade at maturity at the original exchange rate. There is no FX risk to the Fed, no balance-sheet exposure to the foreign banks borrowing the dollars, and no congressional appropriation. What the Fed provides is the one thing offshore dollar markets cannot manufacture in a crisis: dollars, on demand, at a known price.

Offshore Dollar Funding Problem

To see why swap lines matter, start with the size of the offshore dollar system. Banks headquartered outside the United States hold trillions of dollars in dollar-denominated assets, much of it long-term, funded by dollar liabilities, much of which is short-term. The Bank for International Settlements estimates that non-US banks’ on-balance-sheet dollar positions reached roughly $13 trillion by the end of 2022, with substantial additional off-balance-sheet dollar funding through FX swaps and forwards. The activity is concentrated in European, Japanese, and Canadian banks lending to multinationals, commodity traders, and emerging market sovereigns.

The structural problem is that these banks fund long dollar assets with short dollar liabilities they do not control. They rely on wholesale dollar markets: US money market funds, the interbank market, FX swaps, and certificates of deposit. When those markets work, dollar funding rolls over every few days at low cost. When they fail, the position turns into a wrong-way bet. A French bank holding a five-year dollar loan to a US shale company cannot pay it down on a Friday because its overnight dollar funding dried up on Thursday. It has to either fire-sell assets, default on dollar obligations, or find emergency funding somewhere else.

The “somewhere else” was historically the FX market. A bank short of dollars could swap euros for dollars at whatever rate the market quoted. In normal times, covered interest parity holds: the FX-implied dollar interest rate equals the cash dollar rate. In crisis times, parity breaks. During the 2008 panic, the implied dollar rate from a three-month EUR/USD swap exceeded LIBOR by more than 200 basis points, a level that bankrupts a balance sheet funded at LIBOR. The euro area’s European Central Bank could print all the euros its banks needed; it could not print dollars.

Swap Line Mechanics

Suppose the ECB activates its swap line with the Federal Reserve for $50 billion. On day one, the ECB delivers euros to the Fed at the prevailing market spot rate; the Fed credits $50 billion to the ECB’s account at the New York Fed. The ECB then auctions these dollars to euro area banks against eligible collateral, charging the OIS overnight index swap rate plus a fixed spread set by the Fed. Banks receive dollars, post collateral with their home central bank, and use the funds to settle dollar obligations.

At maturity, typically seven days or 84 days, the trade reverses. Banks return dollars to the ECB; the ECB returns dollars to the Fed and receives its euros back, at the same exchange rate as on day one. The ECB has earned a spread from its banks; the Fed has earned its fee from the ECB; no party has taken currency risk, because the unwinding rate was fixed at inception.

Three properties of this architecture matter. First, the Fed bears no credit risk on the foreign banks borrowing dollars; the credit risk sits with the foreign central bank, which knows its own banking system. Second, the foreign central bank bears no FX risk because the round-trip exchange rate is contractually fixed. Third, the dollars distributed are real Federal Reserve dollars created on the Fed’s balance sheet, indistinguishable in markets from any other dollar reserve. A bank rolling LIBOR-funded positions does not care whether the dollar arrived from a money market fund or via a swap-line auction; either dollar settles the debt.

Note. A swap line is sometimes confused with an FX swap done by private banks. The difference is that the swap line is between two central banks, the price is set administratively rather than by market quotes, and the counterparty risk is borne by the foreign central bank, not the Fed.

Ad Hoc Tool to Crisis Architecture

Central bank swap arrangements are not new. The Federal Reserve operated a network of swap lines through the 1960s under the Bretton Woods system to defend dollar parities and recycle official dollar balances. Those arrangements lapsed after the 1973 move to floating exchange rates. For three decades, swap lines were a historical curiosity.

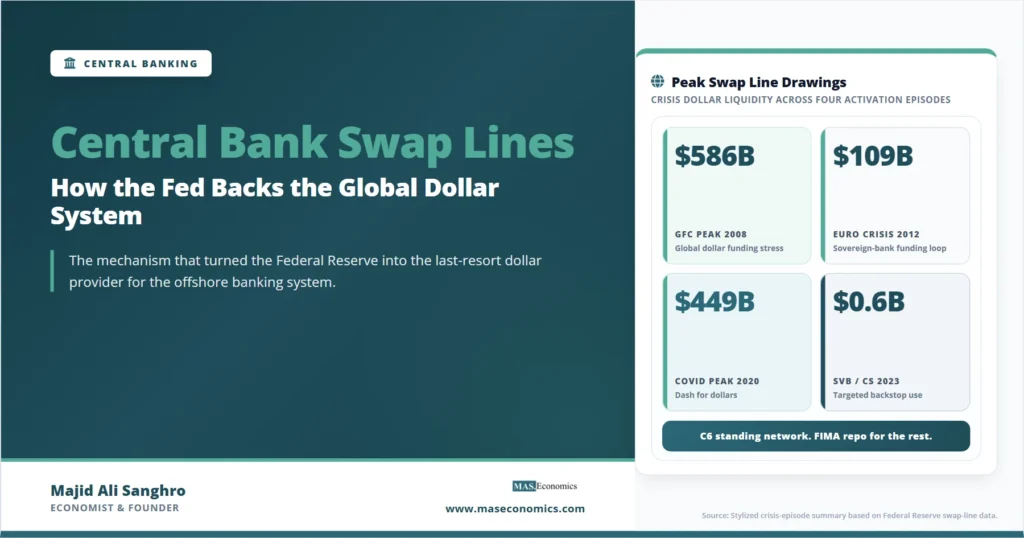

The modern architecture was built during the global financial crisis. In December 2007, the Fed announced temporary dollar liquidity swap arrangements with the ECB and the Swiss National Bank, with initial amounts of $20 billion and $4 billion, respectively. As the crisis deepened, the program expanded relentlessly. By October 2008, in the weeks after the Lehman Brothers failure, the Fed had set the swap-line caps with the ECB, Bank of England, Bank of Japan, and Swiss National Bank at “unlimited,” and had extended dollar swap arrangements to ten more central banks, including the Bank of Korea, Banco de Mexico, Reserve Bank of Australia, and the Monetary Authority of Singapore.

Peak swap-line balances reached about $586 billion in December 2008, equivalent at the time to roughly a quarter of the Federal Reserve’s total assets. The ECB alone drew over $290 billion. As panic receded through 2009, balances declined; by late 2010, all swap lines had returned to near zero.

| Episode | Trigger | Counterparties at Peak | Peak Outstanding | Resolution |

|---|---|---|---|---|

| Global Financial Crisis | Interbank market freeze, Lehman failure | 14 central banks | ~$586 bn (Dec 2008) | Full repayment by Feb 2010 |

| European Sovereign Debt Crisis | Euro area bank dollar funding stress | ECB, BoE, BoJ, SNB, BoC | ~$109 bn (Feb 2012) | Wound down by mid-2014 |

| COVID-19 Funding Shock | Dash for dollars, FX basis blow-out | 5 standing + 9 temporary | ~$449 bn (May 2020) | Almost fully repaid by year-end 2020 |

| March 2023 Banking Stress | SVB failure, Credit Suisse rescue | 5 standing partners | ~$0.6 bn (modest) | Resolved without major drawdowns |

|

Source: Federal Reserve H.4.1 statistical releases; Federal Reserve Bank of New York central bank liquidity swap data; BIS Quarterly Review.

|

||||

The crisis-response framework was made semi-permanent in October 2013, when the Federal Reserve, ECB, Bank of England, Bank of Japan, Swiss National Bank, and Bank of Canada converted their bilateral dollar swap arrangements into “standing” lines with no expiry date and no fixed maximum. These six central banks form what market participants call the C6 dollar swap network. The arrangement is also reciprocal: each of the C6 partners has access to dollars from the Fed and, in principle, the Fed has access to the partner currencies, although the foreign currency direction has rarely been used.

COVID-19 Response Effectiveness

The COVID-19 dollar funding shock in March 2020 looked initially like a replay of 2008. As global investors raced into cash, the FX swap basis widened to crisis levels, money market funds saw heavy redemptions, and dollar funding costs spiked. The Fed’s response was faster and more aggressive than in 2008.

On March 15, 2020, the Fed cut the pricing on the standing C6 swap lines and lengthened maturities. On March 19, it added nine temporary swap lines with Australia, Brazil, Denmark, Korea, Mexico, New Zealand, Norway, Singapore, and Sweden. On March 31, it announced the Foreign and International Monetary Authorities Repo Facility (FIMA Repo), which allowed central banks not on the swap-line list to obtain dollars against their holdings of US Treasuries, a complementary backstop for the broader group of monetary authorities.

The result was a textbook stabilization. Within roughly six weeks, the FX basis collapsed back toward zero. Total swap-line outstandings peaked in May 2020 around $449 billion and were almost fully repaid by year-end. A 2021 New York Fed staff report estimated that the FX basis would have remained elevated for substantially longer absent the swap-line expansion, and that the spillover to global asset prices was meaningful. Both the policy response and the recovery played out faster than in any earlier dollar liquidity event.

Two-Tier Architecture and Partner Selection

The current swap-line architecture has two formal tiers and one informal backstop. The first tier is the C6 standing network: the ECB, Bank of England, Bank of Japan, Swiss National Bank, Bank of Canada, and Federal Reserve. These arrangements are permanent, with no preset maximum drawing, and pricing is reviewed periodically. The second tier is the activated-on-demand temporary swap lines, used in 2008 and 2020 for selected emerging markets and small advanced economies. Each temporary line carries a stated cap and a stated expiry.

The informal third backstop is the FIMA Repo Facility, made permanent in July 2021. Through FIMA, any foreign central bank or international monetary authority with an account at the New York Fed can borrow dollars overnight against US Treasury collateral. This is operationally a repo rather than a swap, and it changes the character of the liquidity provision: the foreign central bank must already hold Treasuries, and the rate is set as a penalty rate above the standing repo rate. FIMA is more universal but less generous than a swap line.

The selection of swap-line partners has long been controversial. Decisions are made by the Federal Open Market Committee, with input from Federal Reserve staff and the New York Fed’s Markets Group. Officially, the criteria are based on the systemic importance of the partner economy, the depth of its financial linkages to the US dollar system, and the policy credibility of its central bank. In practice, the list of countries that received temporary swap lines in 2008 and 2020 was nearly identical, which suggests an institutional shortlist exists.

| Tier | Counterparties | Status | Maximum | Pricing |

|---|---|---|---|---|

| Standing C6 | ECB, BoE, BoJ, SNB, BoC, Fed | Permanent, no expiry | Unlimited in practice | OIS + 25 bp (since March 2020) |

| Temporary (when activated) | Selected EMEs and small AEs | Time-bound, renewable | Stated cap per counterparty | OIS + spread, case-by-case |

| FIMA Repo | Any foreign monetary authority with NY Fed account | Permanent standing facility | Limited by Treasury collateral held | IORB + 25 bp |

|

Source: Federal Reserve Board; Federal Reserve Bank of New York Markets Group; FOMC statements 2013 and 2021.

|

||||

Conspicuously absent from both the standing and temporary lists are China, India, Russia, Saudi Arabia, and most of the BRICS-plus countries. The People’s Bank of China has never had a Fed dollar swap line, although it has built its own renminbi swap network with over thirty central banks. For countries outside the Fed network, the alternative liquidity backstops are accumulating large dollar reserves, the IMF, or, in the worst case, fire sales of US Treasuries to raise dollars in the open market.

Fed’s Swap Line Rationale

The economic case for the Fed’s role rests on two propositions. First, dollar funding stress in offshore markets transmits back to US financial conditions through the same channels that transmitted the 2008 panic. When foreign banks dump US Treasuries and corporate bonds to raise dollars, the prices of those assets fall, US borrowing costs rise, and the Fed’s own monetary transmission deteriorates. Stabilizing offshore dollar markets is partly self-defense. Federal Reserve staff studies, including a series from the New York Fed’s Liberty Street Economics, have estimated that the spillback from offshore dollar stress to US conditions can be of similar magnitude to a direct policy shock.

Second, swap lines reinforce the dollar’s reserve-currency position. If foreign banks could not access dollar funding in a crisis, the rational response would be to fund less in dollars in the first place, hold smaller dollar inventories, and price more cross-border trade in alternative currencies. The swap-line network is one of the institutional features that makes the dollar’s incumbent advantage durable. The international monetary system has many components, but on the funding-of-last-resort question, there is currently no alternative provider.

The Fed gets several things in return. Its standing lines earn a positive spread on every drawing. Stable offshore dollar markets keep US monetary transmission predictable. And the swap-line network gives the Fed leverage over the design of post-crisis financial regulation: a foreign central bank that wants reliable access to dollars in the next crisis has reasons to align its bank supervision and resolution frameworks with US preferences. The Bank for International Settlements has documented how the post-2008 reform agenda was negotiated in part through central bank cooperation that the swap-line network helped institutionalize.

The Limits and the Critics

The criticisms come from three directions. The first is a domestic political objection: the Fed is using federal authority to lend dollars to foreign central banks without explicit congressional approval, in amounts that exceeded $580 billion in 2008. Critics in Congress, especially after 2008, argued that this was a backdoor bailout of foreign banks. The Fed’s response is that swap lines are not loans to banks but currency exchanges with central banks, that the Fed bears no credit risk on the underlying lending, and that the operations are profitable to the Fed.

The second criticism is geopolitical selectivity. Why does Korea get a swap line and Indonesia does not? Why is there no facility for Turkey, India, or Saudi Arabia? The answer the Fed gives, that swap-line access reflects systemic importance and policy credibility, is roughly defensible at the margin, but the absence of any transparent rule means that the line between qualified and unqualified is drawn by FOMC judgment. For excluded countries, the message is that they need to self-insure with reserves, which has its own macroeconomic costs.

The third criticism comes from the academic literature on global liquidity. Researchers, including Hyun Song Shin, formerly of Princeton and now at the BIS, have argued that the offshore dollar system has become so large that any backstop short of unlimited access risks underprovision. The 2020 expansion was generous, but a still-larger shock could expose the same selectivity problem on a worse scale. The Fed has resisted formalizing a universal facility, partly because doing so would be politically infeasible and partly because the discretion is itself part of the policy.

Caveat. Swap lines work because the dollar is the dominant funding currency. If global trade and finance gradually moved to a multipolar currency system, the centrality of the Fed’s swap network would erode. There is no near-term evidence this is happening at scale, but the question is open.

Swap Lines in the Broader Toolkit

It is useful to place swap lines alongside the Fed’s other crisis tools. Domestic lender-of-last-resort facilities like the discount window and the new Bank Term Funding Program address dollar liquidity needs of US banks and depository institutions. The FIMA Repo addresses the dollar needs of foreign monetary authorities with Treasury collateral. Swap lines address the dollar needs of foreign banks via their home central banks. Asset purchase programs address the price of duration and credit in domestic markets. Each tool targets a specific failure mode in a specific market.

The intellectual lineage of all this is Walter Bagehot’s 1873 rule: in a crisis, lend freely, at a penalty rate, against good collateral. The Fed’s swap-line program is the international extension of that doctrine: lend dollars freely to foreign central banks, at a small but real penalty above OIS, against the credit of the borrowing central bank. Bagehot wrote about a domestic banking crisis in a single currency. The dollar’s global role required someone to extend the doctrine across borders, and the Fed, by virtue of issuing the world’s funding currency, was the only institution that could.

Explains

Three concepts that make swap lines work

Continue exploring how central banks operate during periods of market stress.

Explore the MASEconomics BlogConclusion

Central bank swap lines are not a recent innovation, but their role as the central liquidity backstop of the offshore dollar system is a feature of the post-2008 world. The architecture has three layers: a permanent C6 standing network, a discretionary set of temporary lines activated in major crises, and the FIMA repo facility for monetary authorities with Treasury collateral. The mechanism is technically clean. Foreign central banks pay an interest spread for dollars they on-lend to their banks, the Fed bears no FX or credit risk on the foreign banks, and the exchange rate of the unwinding leg is fixed at inception.

The deeper point is that the dollar’s role as the world’s funding currency is sustained in part by an institutional commitment that the Fed will provide dollars when offshore markets cannot. That commitment is selective, not universal, and the selection is governed by Federal Open Market Committee judgment rather than a transparent rule. For countries inside the network, the implicit insurance reduces the cost of operating in dollars. For those outside it, the cost of self-insurance shows up in reserve accumulation, in exchange controls, and in the slow incentive to develop non-dollar funding alternatives. As long as the offshore dollar system remains as large as it is and the Fed remains its only credible backstop, swap lines will keep being activated. The 2020 and 2023 episodes suggest the framework now works well within the perimeter it covers. The remaining policy debate is mostly about the perimeter itself.

Frequently Asked Questions

Who can borrow from a Federal Reserve dollar swap line?

Only foreign central banks borrow from the Fed under a swap arrangement. The foreign central bank then auctions those dollars to commercial banks in its own jurisdiction. The Fed does not lend directly to foreign commercial banks, governments, or private institutions.

What is the difference between a swap line and the FIMA Repo Facility?

A swap line is a currency exchange between two central banks, with no collateral other than the foreign currency delivered in the trade, and is open only to selected partner central banks. The FIMA Repo Facility is a dollar repo against US Treasury collateral that is available to any foreign monetary authority with an account at the New York Fed. FIMA is broader but smaller in effective capacity, since it depends on the Treasury holdings of each user.

Why did the Fed not give China a dollar swap line in 2008 or 2020?

Selection of swap-line partners is made by the Federal Open Market Committee. Public criteria emphasize systemic importance and policy credibility, but the final decisions are discretionary. China has not been on the list during any major swap-line activation. The People’s Bank of China has built its own renminbi swap network with other emerging-market and advanced-economy central banks instead.

Do swap lines cost US taxpayers money?

The Fed’s swap-line operations have historically been profitable. The Fed charges the foreign central bank a spread above the OIS rate, bears no FX risk because the unwinding exchange rate is fixed at inception, and bears no credit risk on the underlying lending, which is taken by the foreign central bank. Net interest earnings from the program are remitted to the US Treasury along with other Fed earnings.

Could swap lines become unnecessary if the dollar loses reserve-currency status?

In principle, yes. If offshore funding moved meaningfully toward the euro, renminbi, or a basket arrangement, the Fed’s swap-line network would matter less. Current data show the dollar’s share of global trade invoicing, FX reserves, and cross-border bank claims has been broadly stable or declining only slowly. The system as it exists today depends on the dollar remaining dominant.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics