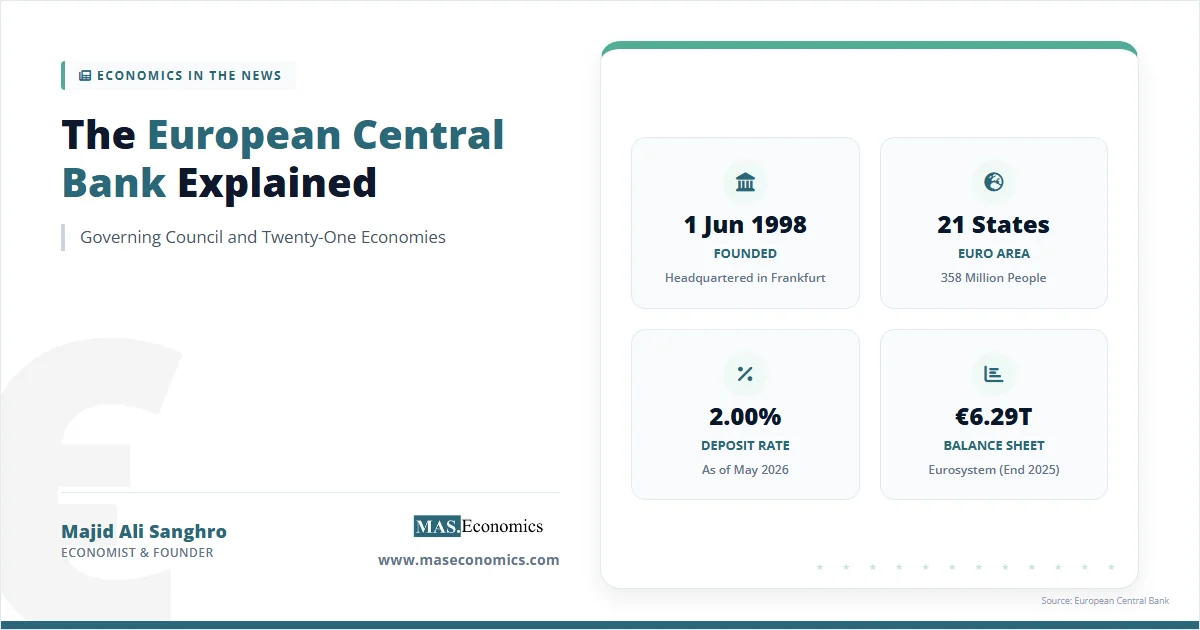

The European Central Bank explained in one sentence that it is the institution that sets monetary policy for 358 million people across 21 countries that share the euro, with a single mandate to keep inflation close to 2% over the medium term. Headquartered in Frankfurt, the ECB became operational on 1 June 1998 and took control of monetary policy on 1 January 1999, when 11 countries irrevocably fixed their currencies to the euro. Bulgaria joined as the 21st member on 1 January 2026, bringing a new seat to the Governing Council and a new shareholder to a balance sheet that still stood at €6,293 billion at the end of 2025.

The ECB sits at the centre of a federated system. Decisions are taken in Frankfurt, but operations are executed by the 21 national central banks of the euro area, which together with the ECB form the Eurosystem. As of May 2026, the deposit facility rate stands at 2.00%, headline inflation in the euro area is 2.6%, and the Governing Council is debating whether the war in the Middle East will force a return to rate hikes or whether stagflation risks will dominate. The institution has gone from a narrow inflation-fighting agency in 1999 to a sovereign-bond buyer, banking supervisor, and increasingly a climate-policy actor all within a treaty-based mandate that has expanded through crisis after crisis.

The Mandate and Operations of the ECB

The ECB’s primary objective, written into Article 127 of the Treaty on the Functioning of the European Union, is to maintain price stability. In its 2021 strategy review, the Governing Council defined that target as 2% inflation over the medium term, symmetric, meaning deviations above and below 2% are equally undesirable. Without prejudice to price stability, the ECB also supports the general economic policies of the Union, including balanced growth, full employment, and environmental sustainability. This is a narrower mandate than the dual mandate of the Federal Reserve, which weighs price stability against maximum employment with no formal hierarchy. Read alongside our piece on central banking and monetary policy, the ECB framework looks legalistic by design, a deliberate choice by treaty drafters who wanted to prevent the ECB from being pulled into fiscal or political objectives.

Beyond setting interest rates, the ECB issues euro banknotes (in cooperation with national central banks), oversees euro-area payment systems including TARGET2 and TIPS, supervises around 110 systemically important banks under the Single Supervisory Mechanism, manages roughly €335 billion in foreign reserves on behalf of the Eurosystem, and increasingly works on a digital euro project that may launch a pilot phase later in 2026. The institution is unique among major central banks in serving 21 sovereign states with separate fiscal authorities, a structural feature that has shaped every major policy episode in its history. The Eurosystem’s governing principle was captured by Christine Lagarde in November 2025 when Bulgaria’s accession was confirmed: the bank now sets monetary policy for “the world’s third-largest economy,” behind only the United States and China by GDP.

Origins and Institutional Evolution

The ECB’s origins lie in the Delors Report of 1989, which proposed economic and monetary union in three stages, and in the Maastricht Treaty signed on 7 February 1992. The treaty entered into force on 1 November 1993, providing the legal basis for a single currency and a single central bank. The European Monetary Institute, the ECB’s direct predecessor, was set up in Frankfurt in 1994 to coordinate national central banks and prepare the technical infrastructure. On 2 May 1998, the European Council confirmed that 11 countries had met the convergence criteria: Belgium, Germany, Spain, France, Ireland, Italy, Luxembourg, the Netherlands, Austria, Portugal, and Finland. The ECB began operating on 1 June 1998 under its first president, Wim Duisenberg of the Netherlands. Greece joined the euro on 1 January 2001, followed by Slovenia (2007), Cyprus and Malta (2008), Slovakia (2009), Estonia (2011), Latvia (2014), Lithuania (2015), Croatia (2023), and Bulgaria (2026).

The early years were marked by orthodoxy. The ECB inherited the Bundesbank’s institutional culture and pursued inflation targeting with monetarist undertones. The first major test came with the 2008 global financial crisis, when the ECB cut rates aggressively and provided unlimited liquidity to banks, but resisted the bond purchases that the Federal Reserve and Bank of England embraced. The 2010-2012 sovereign debt crisis, covered in our European debt crisis case study, almost broke the institution. Spreads on Greek, Portuguese, Irish, Italian, and Spanish bonds widened to levels implying euro break-up. The decisive turning point came on 26 July 2012 when Mario Draghi, the second ECB president, declared that the ECB was ready to do “whatever it takes” to preserve the euro. The accompanying Outright Monetary Transactions programme was never used, but the announcement alone closed peripheral spreads and saved the currency.

The third president, Christine Lagarde, took office on 1 November 2019 and led the institution through the COVID-19 shock and the 2022-2023 inflation surge. The Pandemic Emergency Purchase Programme committed up to €1.85 trillion in asset purchases. When inflation hit 10.6% in October 2022, the deposit rate was raised from -0.50% to 4.00% in just over a year, the fastest tightening cycle in the institution’s history. The cycle reversed in mid-2024 as inflation cooled, with the deposit rate cut to 2.00% by mid-2025 and held there through May 2026.

Structure of the Governing Council

The Governing Council is the principal decision-making body. It has 25 members in 2026: the six members of the Executive Board plus the governors of the 21 national central banks. The Executive Board comprises President Christine Lagarde, Vice-President Luis de Guindos (whose term ends in May 2026, with Croatia’s Boris Vujčić appointed as successor by the European Council), Chief Economist Philip Lane, Piero Cipollone, Frank Elderson, and Isabel Schnabel. Executive Board members are appointed for non-renewable eight-year terms by the European Council acting by qualified majority. National central bank governors are appointed under their own domestic laws, with mandates of at least five years and protections against arbitrary dismissal designed to safeguard independence.

Voting on monetary policy follows a rotation system that came into force when membership exceeded 18 in 2015 and was adjusted again when Bulgaria joined in January 2026. The six Executive Board members hold permanent voting rights. The 21 national governors share a fixed pool of 15 voting rights, divided into two groups: the five governors from the largest economies (Germany, France, Italy, Spain, and the Netherlands) share four votes, and the remaining 16 governors share 11 votes. Voting rights rotate monthly. All governors attend every meeting and participate in deliberations regardless of voting status. Decisions are normally taken by simple majority, with the President’s vote breaking ties.

Meetings happen every six weeks. The pre-meeting documentation is built by the ECB staff, the Eurosystem committees of national experts, and the Monetary Policy Committee that brings together heads of monetary policy from each NCB. The Governing Council meets on Wednesday afternoon and Thursday morning, with a press conference held by the President at 14:45 CET on Thursday following the policy decision at 14:15. Minutes formally called “monetary policy account” are published with a four-week lag.

The General Council includes the President and Vice-President, plus the governors of all 27 EU national central banks, including the six non-euro members. It is a coordination body rather than a decision-making one and will dissolve once all EU members adopt the euro. The Supervisory Board, established in 2014 under the Single Supervisory Mechanism, takes banking supervision decisions that are then formally adopted by the Governing Council under a non-objection procedure.

Monetary Policy Instruments and Transmission

The ECB has two broad policy tools: conventional rate setting and unconventional balance-sheet operations. The three key interest rates are the main refinancing operations rate (2.15% as of May 2026), the deposit facility rate (2.00%), and the marginal lending facility rate (2.40%). Since the 2024 framework review, the deposit facility rate is the operational target, which sets the floor for overnight money-market rates. The MRO rate sits 15 basis points above the deposit rate, narrowing from a wider spread that prevailed during the era of abundant excess reserves. The corridor system gives banks predictable upper and lower bounds for short-term funding costs, and the policy stance is communicated through the level of and forward guidance about the deposit facility rate.

Unconventional tools have expanded steadily since 2008. The Asset Purchase Programme, launched in 2014 and ramped up in 2015, is the ECB’s quantitative easing programme, with cumulative purchases peaking at around €3.3 trillion in 2022. The Pandemic Emergency Purchase Programme, launched in March 2020, added another €1.7 trillion. Both programmes are now in run-off; APP holdings declined to €2,322 billion by end-2025, while PEPP holdings stood at €1,423 billion. Targeted Longer-Term Refinancing Operations provide cheap term funding to banks contingent on lending to households and firms. The Transmission Protection Instrument, announced in July 2022, allows discretionary purchases of bonds from countries facing “unwarranted, disorderly market dynamics,” the doctrinal heir to the OMT programme. For background on these tools, see our explainers on quantitative easing, quantitative tightening, and monetary policy tools.

| Instrument | Mechanism | Active Use |

|---|---|---|

| Deposit Facility Rate | Sets the floor for overnight money-market rates; the operational target since 2024. | Held at 2.00% since June 2025 |

| Main Refinancing Operations | Weekly liquidity injections through repos at 2.15%, against eligible collateral. | Active, smaller volumes than 2008-2014 |

| Asset Purchase Programme (APP) | Outright purchases of public and private sector securities to ease financial conditions. | In passive run-off, holdings €2,322bn |

| Pandemic Emergency Purchase Programme (PEPP) | Flexible bond purchases launched March 2020, up to €1.85 trillion envelope. | In run-off since 2024, holdings €1,423bn |

| TLTRO III | Cheap term loans to banks linked to lending to non-financial private sector. | Final operations matured in 2024 |

| Transmission Protection Instrument | Discretionary, conditional purchases to counter disorderly fragmentation. | Available since 2022, never activated |

| Single Supervisory Mechanism | Direct supervision of around 110 significant banks across the euro area. | Active since November 2014 |

|

||

Source: ECB Monetary Policy Decisions and Annual Report 2025.

The Single Supervisory Mechanism, which became operational in November 2014, is the ECB’s second major function. The ECB directly supervises significant banking institutions with more than €30 billion in assets or that account for more than 20% of national GDP, while national supervisors handle smaller institutions under ECB oversight. The 110 significant banks together hold over 80% of euro-area banking assets. Supervision involves on-site inspections, stress tests in coordination with the European Banking Authority, and formal decisions on capital requirements, governance, and risk management.

The ECB in Crisis Episodes

Three episodes define the ECB’s track record. The first is the sovereign debt crisis of 2010-2012. Spreads between Greek, Portuguese, Irish, Italian, and Spanish bonds and German bunds widened to levels implying possible euro exit, particularly after Greece’s first default in March 2012. The ECB’s initial Securities Markets Programme, launched in May 2010, proved insufficient because its size was perceived as limited. Draghi’s “whatever it takes” speech on 26 July 2012, followed by the announcement of OMT on 2 August, ended the spiral. Research by Acharya and co-authors at Brookings shows that the OMT announcement reduced sovereign yields, recapitalised undercapitalised banks holding GIIPS sovereign debt, and prevented a further wave of forced bank deleveraging. The German Bundesbank president was the only Governing Council member to vote against OMT, a public dissent that signalled the depth of intra-Council disagreement.

The second episode is the 2014-2019 fight against deflation. Headline inflation fell below zero in 2015 and stayed near zero for years. The ECB pushed the deposit rate to -0.50%, launched APP at €60-80 billion of monthly purchases, and provided multiple rounds of TLTROs. The strategy review concluded in 2021 that the previous “below but close to 2%” target had operated asymmetrically, allowing inflation to drift down. The new symmetric 2% target acknowledged that undershooting was as costly as overshooting, an explicit nod to the lessons covered in our piece on liquidity trap economics.

The third episode is the 2022-2023 inflation surge. Energy prices, supply-chain shocks, and post-pandemic demand drove HICP inflation to 10.6% in October 2022. The deposit rate rose from -0.50% in July 2022 to 4.00% in September 2023, the fastest hiking cycle in ECB history. Inflation fell back to the 2% target by mid-2024, and the cutting cycle followed. As of May 2026, headline inflation is 2.6% (up from 1.9% in February amid the Middle East war), core inflation is 2.3%, and growth is projected at 0.9% in 2026 under the ECB baseline. CNBC reports that markets are pricing roughly even odds of a rate hike at the June 2026 meeting if energy prices remain elevated.

Source: European Central Bank, monetary policy decisions database. Deposit facility rate, end-of-year values; 2026 figure as of May 9, 2026.

The chart above tells a single story: the ECB has lived through every regime in modern monetary economics. From positive policy rates in 2008 down to negative rates in 2014-2022, then the sharpest hiking cycle ever, then back down to a neutral 2.00%. The 2025 financial statements show that this rollercoaster left the institution itself with a loss of €1,254 million in 2025, much smaller than the €7,944 million loss in 2024. Losses arose because the ECB held long-duration low-yielding bonds funded by short-term deposits remunerated at the rising policy rate. Losses are absorbed against future profits, and the institution will not distribute profits to national central banks until the cumulative shortfall is recovered.

The Future of the ECB

Three challenges dominate the contemporary debate. The first is the boundary of the mandate. The ECB has expanded its activities to include climate-related disclosure requirements for collateral, green bond purchases tilted within the corporate bond programme, and stress tests that incorporate climate scenarios. Critics argue this stretches the price-stability mandate beyond what the treaties intended; defenders point to the symmetric strategy commitment to incorporate sustainability without prejudice to price stability. Our piece on central banks and climate change covers the legal and economic arguments in depth.

The second is independence under political stress. The ECB’s legal independence is among the strongest of any central bank, written into the Treaty on the Functioning of the European Union and into the Statute of the European System of Central Banks. Treaty change requires unanimity, which makes the framework practically untouchable. Yet political pressure has grown, particularly during fiscal crises when governments resent the ECB’s conditionality on bond purchases. Our piece on threats to central bank independence contrasts the European framework with the contemporary Federal Reserve transition, where statutory protections are weaker and political interference more direct.

The third is governance with 21 (and possibly more) members. The rotation system already prevents one-country-one-vote at every meeting; further enlargement to 25 or 27 members would require additional reforms. The 2027 leadership transition compounds the challenge: four of the six Executive Board seats turn over by late 2027, including the President. National battles over those seats will play out in parallel with the U.S. Federal Reserve transition under the new Chair, Kevin Warsh, a year that may reshape global central banking governance more than any since 1979. The digital euro project, the future of the Capital Markets Union, and the relationship between the ECB and a still-incomplete banking union round out the structural agenda.

MASEconomics Explains

Four economic concepts behind the European Central Bank

Conclusion

The European Central Bank explained in full is the central bank for 21 sovereign states bound together by treaty rather than by a federal government. It runs monetary policy through three key rates and a balance sheet that peaked above €8.8 trillion at the Eurosystem level in 2022 and stood at €6,293 billion at the end of 2025. The Governing Council, with 25 members and a rotating voting system, is the principal decision-making body, supported by an Executive Board of six in Frankfurt. Since 1999, the ECB has set rates from negative levels to 4% and back, supervised over a hundred banks since 2014, and built tools OMT, TPI, PEPP that respond to crises specific to a monetary union without a fiscal union. As of May 2026, the deposit facility rate is 2.00%, headline inflation is 2.6%, and the institution is preparing for a leadership transition that will replace four of six Executive Board members by late 2027.

Frequently Asked Questions

What does the European Central Bank do?

The European Central Bank is the central bank for the euro area. Its main task is to maintain price stability by setting monetary policy for countries that use the euro. It also helps supervise major banks, supports payment systems, provides liquidity during periods of stress, and works with national central banks through the Eurosystem.

What is the ECB’s inflation target?

The ECB aims for inflation of 2% over the medium term. The target is symmetric, which means inflation that is too low and inflation that is too high are both treated as undesirable. This framework is designed to keep prices stable while giving the economy some protection against deflation and weak demand.

Who makes monetary policy decisions at the ECB?

Monetary policy decisions are made by the ECB Governing Council. It includes the members of the ECB Executive Board and the governors of the national central banks of euro-area countries. This structure gives the ECB a euro-area-wide mandate while still bringing national economic information into the decision-making process.

What is the difference between the ECB and the Eurosystem?

The ECB is the central institution based in Frankfurt. The Eurosystem includes the ECB plus the national central banks of the euro-area countries. The ECB sets the common monetary policy, while the Eurosystem helps implement that policy across member states through banking operations, payments, liquidity provision, and financial-market infrastructure.

Why do ECB decisions affect countries differently?

ECB decisions affect countries differently because euro-area economies have different banking systems, debt levels, housing markets, wage structures, and growth conditions. A single interest-rate decision is transmitted through national financial systems that are not identical. This is why the same monetary policy can feel tighter in one country and less restrictive in another.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics