Introduction

Imagine a world where cash is no longer king, where payments are instantaneous, transparent, and powered by central banks digitally. As countries race to develop Central Bank Digital Currencies (CBDCs), the future of money is closer than ever. But what does this mean for you, the global economy, and the financial landscape? Let’s dive into the fascinating world of CBDCs and discover how they may reshape the way we think about money.

The digitalization of payments has grown rapidly over the past few decades, thanks to technological advancements that shifted the focus from Fintech to central bank digital currency (CBDC). Unlike private digital currencies like Bitcoin, CBDCs are issued and backed by central banks, providing more stability and security.

With global cash use declining and digital transactions growing, central banks are responding by researching and piloting CBDCs. A 2021 survey by the Bank for International Settlements (BIS) found that 86% of central banks are investigating CBDCs, with over 60% experimenting with the technology, and 14% running pilot projects. Several key factors drive this shift, including the rise of blockchain technology, the growth of cryptocurrencies, and the need to reduce illicit activities linked to unregulated digital assets.

While CBDCs could bring about more efficient payment systems, they also raise concerns over privacy, financial stability, and monetary control. This post explores the potential impact of CBDCs on the global economy, how they differ from cryptocurrencies, and the ways in which they might reshape monetary policy.

Cryptocurrencies vs. Stablecoins vs. CBDC

To fully grasp the transformative potential of CBDCs, it is important to differentiate them from existing forms of digital currencies, such as cryptocurrencies and stablecoins. These three types of digital currencies represent distinct approaches, each with its own benefits and drawbacks.

Cryptocurrencies

Cryptocurrencies (e.g., Bitcoin) are decentralized digital currencies not backed by any central authority. Their value is highly speculative, which makes them unstable as a medium of exchange or a store of value. Furthermore, because of their anonymity, cryptocurrencies are often linked to illicit activities such as money laundering and ransomware attacks. While cryptocurrencies promote independence from government control, their speculative nature undermines their use as a reliable monetary system.

Stablecoins

Stablecoins aim to address the volatility of cryptocurrencies by being backed by real-world assets, such as fiat currencies or commodities. This asset backing provides stability, making stablecoins more practical for transactions. However, stablecoins are still tied to the risks of the financial system they rely on, including the possibility of losing their peg during market instability.

CBDCs

CBDCs are digital currencies issued by central banks, combining the security and trust of government-backed currency with the technological innovations of cryptocurrencies. CBDCs offer the benefits of stability and regulatory oversight while utilizing blockchain technology for efficiency. By being directly backed by central banks, CBDCs avoid the volatility of cryptocurrencies and the reliance on external assets seen in stablecoins.

A Closer Look at CBDC Models

CBDCs come in various forms, depending on how they are designed and issued. Central banks are exploring several models, each with distinct features that could reshape how money is used, stored, and transferred.

Account-Based vs. Token-Based CBDCs

One of the primary distinctions between CBDC models is whether they are account-based or token-based.

Account-Based CBDC

In this model, transactions occur by verifying the identity of the participants and confirming whether they have the funds in their accounts. This system is similar to how traditional bank transfers work today, where financial institutions check the sender’s and recipient’s account balances before processing the transaction.

Token-Based CBDC

In contrast, a token-based CBDC does not require verifying the identity of the parties involved. Instead, the authenticity of the digital token is checked. This model allows for offline payments, making it ideal for remote or underserved areas with limited internet access.

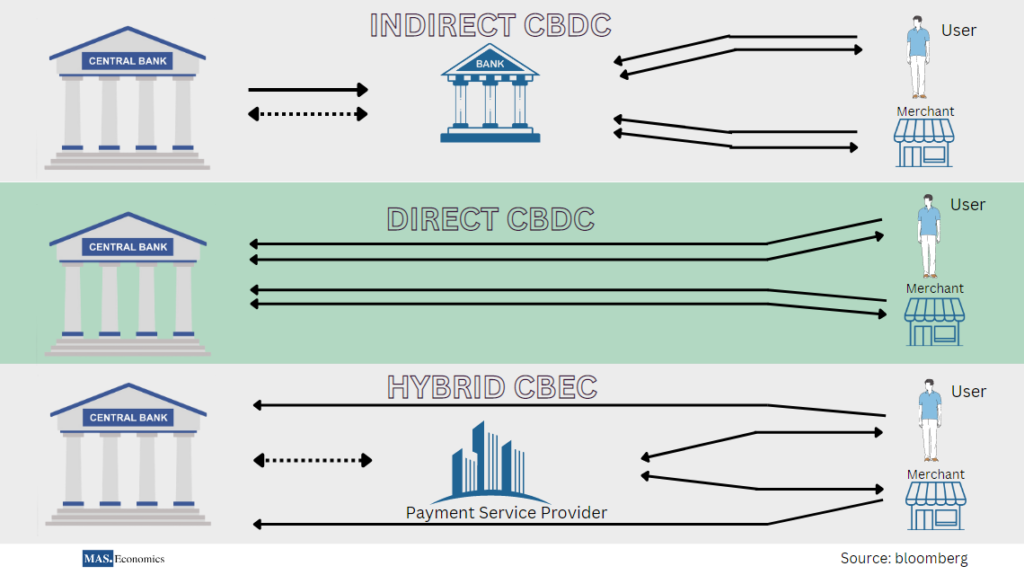

Direct, Indirect, and Hybrid Models

Several models dictate how CBDCs could be implemented across the economy. Here’s a look at the three primary models central banks are exploring:

Direct Model

In the direct model, all transactions occur directly between the central bank and users. Central banks would be responsible for issuing digital currency, holding accounts, processing payments, and ensuring regulatory compliance. This model centralizes monetary control but requires the central bank to handle all transactional data and security concerns.

Example: In a direct CBDC system, you could have a digital account with your central bank, much like you have an account with your current bank. Payments and transfers would be processed directly through this account.

Indirect Model

Also known as “synthetic CBDC,” in the indirect model, the central bank issues digital currency to commercial banks or financial institutions, which then distribute the digital currency to users. The central bank remains the currency issuer but outsources distribution to the private sector.

Hybrid Model

The hybrid model blends elements of the direct and indirect models. In this case, commercial banks or intermediaries distribute the CBDC, but the central bank retains control over the currency and can intervene if necessary. This model provides the benefits of decentralized distribution while maintaining central oversight.

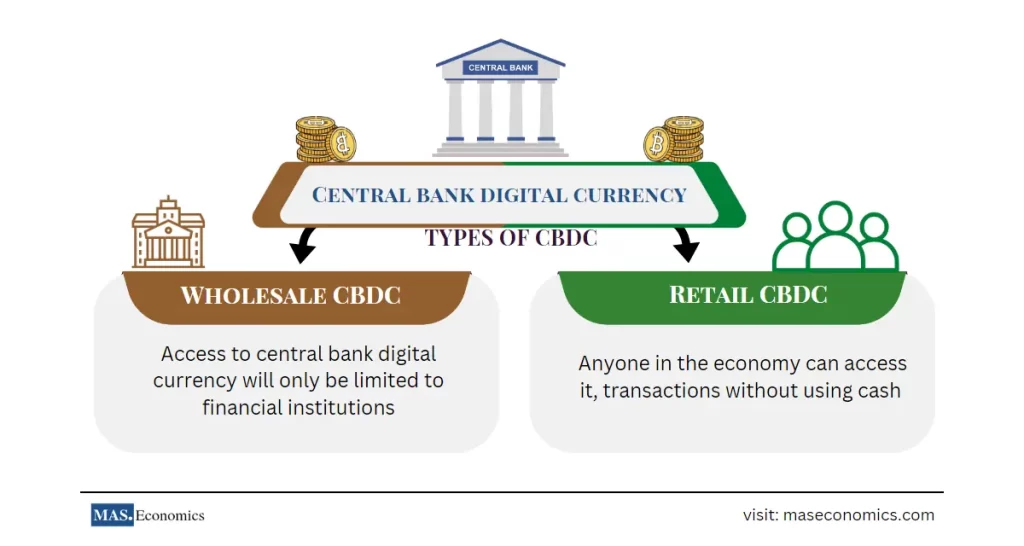

Wholesale vs. Retail CBDCs

The wholesale and retail distinctions further clarify how CBDCs could be implemented in the economy.

Wholesale CBDC

Wholesale CBDCs are intended for financial institutions and are designed to improve the efficiency of interbank payments. Central banks already issue reserve accounts for financial institutions, and wholesale CBDCs could streamline large transactions between banks by using digital currencies for interbank settlements.

Use Case: Wholesale CBDCs could significantly reduce the costs and time associated with cross-border payments between large banks. In 2015, the Bank of England tested a wholesale CBDC with several commercial banks, and although the results were positive, concerns over scalability and privacy still need to be addressed.

Retail CBDC

Retail CBDCs, on the other hand, would be available for the general public, providing a digital alternative to cash. This model would allow users to make transactions using a central bank-backed digital currency for everyday purchases, much like using a digital wallet or mobile payment service.

Use Case: In Sweden, where cash use has plummeted, the Riksbank is exploring a retail CBDC known as the eKrona. This would provide a safe, government-backed alternative to cash, ensuring that citizens can still access central bank money in a digital economy.

How CBDCs Could Reshape Monetary Policy

CBDCs could fundamentally change how central banks conduct monetary policy by offering more precise tools to control money supply, interest rates, and inflation. Here’s how:

Enhanced Monetary Policy Transmission Mechanism

One of the key challenges of traditional monetary policy is the reliance on commercial banks to transmit central bank policy changes (e.g., interest rate changes) to the broader economy. CBDCs could provide a more direct link between central banks and the public, enabling faster and more efficient policy adjustments.

Example: With CBDCs, central banks could implement negative interest rates more effectively during a recession by directly adjusting the rates on digital accounts, encouraging people to spend rather than hoard money.

Real-Time Economic Data

CBDCs offer the potential for central banks to access real-time data on economic transactions, giving them a clearer picture of consumer behavior, spending patterns, and inflationary pressures. This data would enable central banks to make more informed decisions regarding interest rates and monetary expansion.

Mitigating the Risk of Bank Runs

One concern with CBDCs is that they could facilitate bank runs during financial crises. In times of uncertainty, people may transfer funds from commercial banks to CBDCs en masse, destabilizing the banking system. Central banks will need to carefully design CBDCs to mitigate this risk, perhaps by limiting the amount of CBDC that individuals can hold.

Will CBDCs Replace Cash?

While the rise of digital payments has reduced cash usage in many countries, cash remains the only form of central bank money available to the public. CBDCs are unlikely to completely replace cash, at least in the short term. Instead, they will likely complement it, providing a digital alternative that can be used alongside physical currency.

Key Statistics:

- In the United States, cash transactions accounted for 19% of all payments by 2020, down from 40% in 2012.

- In China, cash use is even lower, with mobile wallets such as Alipay and WeChat Pay dominating the market, accounting for 50% of point-of-sale (POS) transactions.

While CBDCs could provide a digital alternative to cash, especially in emergencies, cash will continue to play an important role, particularly in regions with limited internet access or for users who prefer anonymity in transactions.

Global CBDC Developments: The IMF’s Comprehensive CBDC Handbook

Recognizing the importance of CBDCs in the evolving financial landscape, the International Monetary Fund (IMF) is taking an active role in guiding countries through the process of designing and implementing digital currencies. The IMF is developing a CBDC Handbook, which will serve as a comprehensive resource for policymakers worldwide. The handbook covers several critical areas, including:

Technological Requirements: Guiding the technical infrastructure required to implement a robust and scalable CBDC system.

Framework and Objectives: Introducing CBDCs conceptually and discussing their benefits over other forms of payment.

Readiness and Legal Framework: Evaluating a country’s legal and technical capacity to issue a CBDC.

Design Considerations: Exploring the impact of various design choices on privacy, adoption, financial stability, and cross-border use.

Case Studies: India and Pakistan’s Push Towards CBDCs

Several countries are leading the way in the development and testing of CBDCs, including India and Pakistan. Both nations are exploring CBDCs as a way to modernize their financial systems, promote financial inclusion, and compete on the global stage.

India’s Digital Rupee

In December 2022, India launched a pilot for its digital rupee (e₹-R), with trials initially rolled out in four cities. The Reserve Bank of India (RBI) envisions the digital rupee as a legally recognized digital token, serving as a direct replacement for physical cash. The pilot project aims to evaluate the digital rupee’s impact on efficiency, transparency, and security in the payments ecosystem.

Pakistan’s CBDC Ambitions

Similarly, Pakistan is preparing to introduce its own CBDC by 2025. The State Bank of Pakistan (SBP) has already enacted regulations for Electronic Money Institutions (EMIs), which will play a key role in distributing digital currency. By embracing CBDCs, Pakistan hopes to combat corruption, foster financial inclusion, and make its financial system more transparent and efficient.

Conclusion

As central banks worldwide explore the potential of Central Bank Digital Currencies (CBDCs), the financial landscape is poised for a transformative shift. CBDCs offer numerous advantages, including enhanced security, improved transparency, and more control over personal information and transactions compared to private digital currencies.

However, the introduction of CBDCs also raises significant challenges, from ensuring financial stability to protecting user privacy. The road to CBDC implementation will require careful consideration of these factors by central banks and policymakers.

One thing is clear: the future of money is digital. While cash and CBDCs will likely coexist for the foreseeable future, the rise of digital currencies will reshape how we think about money, payments, and the role of central banks in the global economy.

We will keep monitoring this trend to see how things shake out; for now, I think cryptocurrencies are worth keeping an eye on.

(The information in the article cannot provide the basis for any investment decision or other transaction. Appropriate professional advice should be sought before making any investment decision.)