The numbers tell a strange story. DoorDash lost $667 million in 2019 alone and had not posted a full-year profit since 2013. Uber Eats burned cash for almost a decade. Deliveroo went public in March 2021 at 390 pence per share, then watched its valuation collapse so far that DoorDash bought the entire company for 180 pence in October 2025, less than half the IPO price. Through it all, drivers in New York City earned a median of $7.94 per hour before tips, restaurants saw 20% to 30% commissions eat their already-thin margins, and packaging waste piled up in landfills.

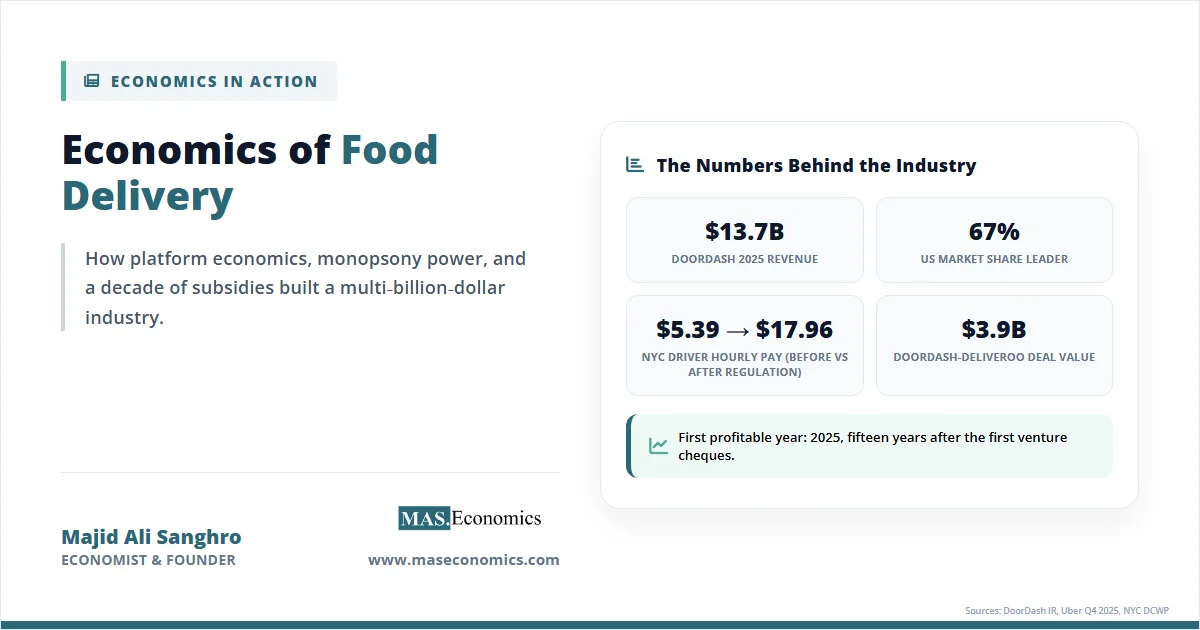

And yet the industry kept growing. The economics of food delivery reveal one of the most expensive scaling experiments in modern capitalism: a multi-trillion-dollar global market built on losses, lawsuits, and a steady transfer of risk from platforms to the people doing the actual work. The global online food delivery market reached roughly $173 billion in 2025 and is projected to keep climbing through 2035. DoorDash finally turned a full-year GAAP profit of $935 million in 2025, fifteen years after the company was founded.

The dilemma is not that food delivery exists. The puzzle is who pays for it, who captures the value, and why the model survived long enough to find out.

From Niche to Global Industry

Food delivery is not new. Pizza shops have been sending mopeds since the 1960s. What changed in the 2010s was the platform layer: a smartphone app sitting between three groups (consumers, restaurants, drivers) and matching them in real time. Grubhub launched in 2004 as a directory. Postmates added couriers in 2011. DoorDash and Deliveroo both launched in 2013. Uber Eats followed in 2014, leveraging an existing fleet of ride-hail drivers and the brand recognition of its parent.

None of these companies made money in the early years. The strategy was straight from the Silicon Valley playbook: subsidize aggressively, capture market share, sort out unit economics later. SoftBank alone poured billions into DoorDash across multiple funding rounds. By the time DoorDash filed to go public in late 2020, the company had raised roughly $2.5 billion in private capital, and the IPO itself raised another $3.4 billion. Critics called it the “most ridiculous IPO of 2020”; supporters called it the future of local commerce.

Then the pandemic hit. Restaurants closed their dining rooms. Consumers ordered everything to their doors. DoorDash’s revenue surged 226% in the first nine months of 2020, and it briefly turned a $23 million profit in Q2 2020 before sliding back into losses. The pandemic did two things at once: it gave platforms a once-in-a-generation tailwind, and it locked in habits that did not fully reverse when restaurants reopened. By 2025, more than half of U.S. consumers will consider food delivery an “essential” part of their lifestyle.

The post-pandemic period has been about consolidation and survival. Uber bought Postmates for $2.65 billion in 2020. Just Eat Takeaway bought Grubhub for $7.3 billion the same year, then sold it for far less. DoorDash bought Wolt in 2022 for €7 billion ($7.9 billion) and finalized its $3.9 billion acquisition of Deliveroo in October 2025, taking the combined entity into 45 markets. The European Union, meanwhile, passed the Platform Work Directive in October 2024, giving member states until December 2026 to presume that platform workers are employees unless platforms can prove otherwise.

Table 1. Food Delivery Timeline: From Launch to Consolidation

| Year | Event | Significance |

|---|---|---|

| 2013 | DoorDash and Deliveroo founded | Smartphone-era platforms launch within months of each other on opposite continents. |

| 2014 | Uber Eats launches in Los Angeles | Ride-hail giant enters delivery using existing driver network and brand. |

| March 2020 | Pandemic lockdowns begin | Order volumes spike as dine-in collapses; platforms become essential infrastructure. |

| December 2020 | DoorDash IPO at $102 per share | Stock jumps 86% on first day to $72 billion valuation despite cumulative losses. |

| March 2021 | Deliveroo IPO at 390 pence | London listing valued the company at £7.6 billion; shares fell sharply post-listing. |

| November 2020 | California Proposition 22 passes | Voters exempt gig platforms from treating drivers as employees under state law. |

| December 2023 | NYC minimum pay rate enforcement begins | Delivery workers’ floor pay rises from $5.39 to $17.96 per hour before tips. |

| October 2024 | EU Platform Work Directive adopted | Rebuttable presumption of employment for platform workers across the bloc. |

| October 2025 | DoorDash completes Deliveroo acquisition | $3.9 billion all-cash deal creates a 45-market global delivery group. |

| February 2026 | DoorDash reports full-year 2025 net income of $935 million | First full year of profitability after twelve years of operation. |

| March 2026 | Uber Eats raises U.S. commission rates | Lite tier rises from 15% to 20%; first rate change in roughly ten years. |

|

||

The story so far has three distinct phases. From 2013 to 2019, platforms competed by burning cash to acquire users. From 2020 to 2022, the pandemic gave them a demand shock that no one had planned for, and order volumes scaled faster than infrastructure could absorb. From 2023 onward, the focus has shifted to extracting profit from a more concentrated industry while regulators try to redistribute the gains.

Key Economic Forces in Delivery

Food delivery sits at the intersection of several economic structures that rarely appear together in one product. To see why the industry behaved the way it did, the model needs to be understood as a two-sided platform, with elements of monopsony power on the labour side and persistent market failure in pricing and externalities.

Two-Sided Markets and Network Effects

A delivery platform is valuable to a consumer only if many restaurants are listed; it is valuable to a restaurant only if many consumers are using it; and it is valuable to both only if enough drivers are available to fulfil orders within twenty or thirty minutes. This is the textbook two-sided market problem with a third side bolted on. Each group has zero reason to join until the others have joined, which is why platforms cannot start small and grow organically. They have to subsidize all three sides at once until the network reaches critical mass.

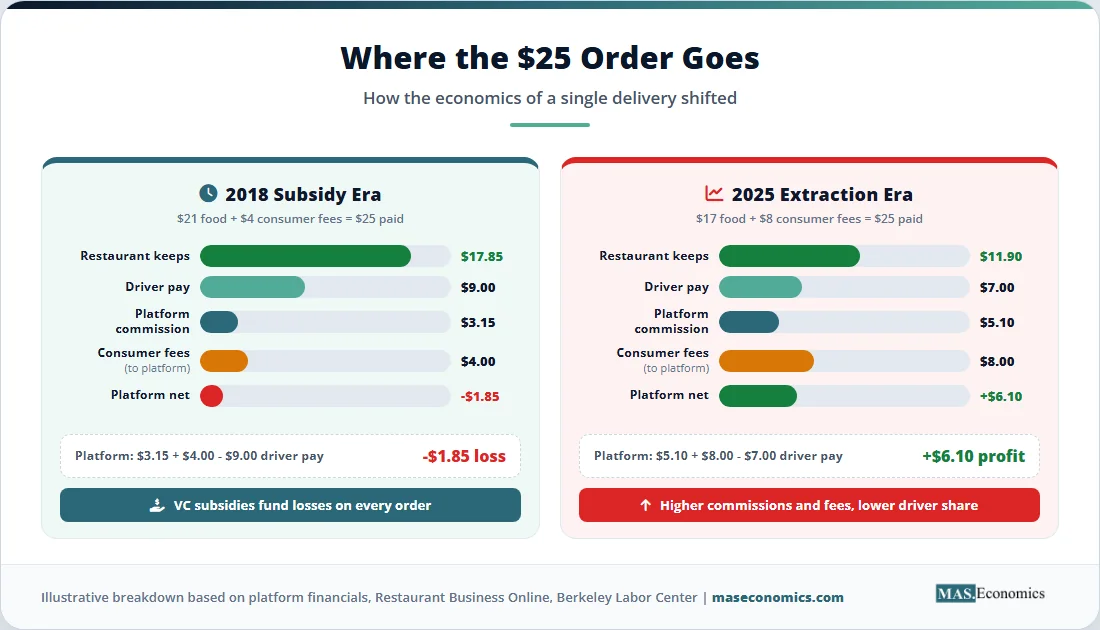

The mathematics of the subsidy strategy is brutal. If a platform pays a driver $8 to deliver a meal, charges the consumer a $4 delivery fee, and takes a 20% commission on a $25 order ($5), the gross margin per delivery is $1 before any overhead. Marketing, technology, payment processing, and customer support then push that into deficit. The bet is that scale eventually compresses fixed costs, advertising revenue from restaurants kicks in, and subscription products like DashPass lock consumers into higher order frequency. DoorDash’s logic was that with enough volume, the per-order economics would flip from negative to positive.

Network effects make this winner-take-most. Consumers using a platform with more restaurants and faster delivery have little reason to switch; restaurants on the platform with the most customers have little reason to leave. The dominant platform in each region tends to keep dominating, which is why the industry is consolidated into roughly two players per major market. DoorDash holds about 67% of the U.S. market. Uber Eats and Grubhub split most of the remainder. In Europe and the Middle East, Deliveroo and Just Eat Takeaway dominated until DoorDash rolled them into its global footprint.

Monopsony Power on the Driver Side

Once a platform achieves dominance on the consumer and restaurant sides, it acquires something economists call monopsony power: the ability to set wages below competitive levels because workers have few alternative buyers for their labour. Drivers in most metros have a realistic choice between two or three apps. Many work for all of them simultaneously, but the algorithms that assign orders, set pay, and handle deactivation are controlled entirely by the platform. There is no collective bargaining, no posted pay scale, and limited transparency about how individual offers are calculated.

The empirical record is unforgiving. Before New York City implemented a minimum pay rate, app-based delivery workers in the city earned a median of $5.39 per hour before tips. The University of California, Berkeley Labor Center studied gig drivers in five U.S. metro areas in 2024 and found that delivery workers’ employee-equivalent net earnings, excluding tips, were $4.98 per hour in California and just $0.40 in the other four metros. Including tips lifted the figure to $11.43 in California and $8.36 elsewhere, still well below local minimum wages. The Berkeley study found that two-thirds of DoorDash drivers in California received Proposition 22 top-up payments because their base earnings fell below the state’s guaranteed floor.

This is what monopsony looks like in the wild. Workers are not simply choosing low pay; they are constrained by the structure of the market. The losers here are clear: drivers absorb most of the cost of vehicle wear, fuel, insurance, and downtime, while the platform extracts the surplus generated by the network effect.

Restaurant Margins and Price Discrimination

Restaurants face a different version of the same squeeze. Independent food service operators run on net margins of roughly 3% to 9%. Commission rates ranging from 15% to 30% compress that to almost nothing on delivery orders. Uber Eats raised its rates in March 2026, lifting the Lite tier from 15% to 20% and adding a 5% surcharge for orders from Uber One subscribers, who account for 60% to 70% of bookings in some markets. The first rate change in roughly ten years was framed as covering rising costs; for restaurants on the margin, it was the moment when delivery moved from low-margin to loss-making.

Platforms also engage in price discrimination, charging different consumers different prices based on observable signals like subscription status, location, and order history. Uber One subscribers receive lower delivery fees but the cost is shifted onto restaurants. Surge pricing during peak hours or bad weather extracts more from inelastic consumers. Restaurants are often contractually prevented from offering lower prices on their own websites, a clause known as a most-favoured-nation provision that limits competition between channels.

The distributional picture is straightforward. Platforms with scale capture the lion’s share of the surplus. Consumers gain convenience, though they pay through delivery fees, service fees, tips, and inflated menu prices. Some independent restaurants benefit from the customer reach, but most lose margin; small operators without bargaining power lose more than national chains that can negotiate custom rates. Drivers, in the absence of regulation, capture little. The growth of ghost kitchens, valued at $76.5 billion globally in 2025, allows some restaurants to side-step the high real estate costs of dine-in, but it also intensifies platform dependency.

Market Failure and Externalities

The model also generates classic market failures. Information asymmetries are everywhere: consumers cannot observe true delivery times, driver pay, or commission rates; drivers cannot see future order density when they decide whether to log on; restaurants cannot tell whether a poor review reflects food quality or a courier who left the bag in the rain. Platforms have access to all three data streams and use them to price discriminate, route orders, and manage performance.

Externalities are equally pervasive. Traffic congestion in dense urban centres has worsened with delivery scooter and bike traffic. Packaging waste from single-use containers, plastic cutlery, and insulated bags is a recognized environmental cost not priced into delivery fees. Road safety risks fall disproportionately on couriers, many of whom work without health insurance, sick pay, or accident coverage. Cities have responded with new rules: NYC’s minimum pay rate, Seattle’s PayUp law, and the EU’s directive are all attempts to internalize costs that platforms had successfully shifted onto workers and the public.

The Numbers Behind the Model

The contrast between platform revenue growth and unit economics is sharper when seen in the numbers. DoorDash booked $13.7 billion in revenue in 2025, up from $10.7 billion the year before, and finally posted a full-year GAAP net income of $935 million. That single profitable year followed twelve years of consistent losses.

Sources: DoorDash and Uber Q4 2025 financial results; Just Eat Takeaway 2024 annual report; Deliveroo 2024 annual report (acquired by DoorDash October 2025).

The platforms differ as much in cost structure as in revenue. The table below compares commission rates, driver pay models, and profitability across four leading platforms in 2025-2026.

Table 2. Platform Comparison: Commissions, Driver Models, and Profitability

| Platform | Commission Range | Driver Model | 2025 Result |

|---|---|---|---|

| DoorDash | 15% to 30% (tiered) | Per-order pay plus tips; Prop 22 floor in California | $935 million net income (first profitable year) |

| Uber Eats | 20% to 30% (raised March 2026) | Per-trip pay; Uber One member surcharges | Profitable as part of Uber group; delivery segment EBITDA positive |

| Just Eat Takeaway | 14% to 30% by market | Mix of employee couriers (Netherlands, UK) and contractors | Adjusted EBITDA positive; sold Grubhub at heavy loss |

| Deliveroo | 14% to 35% (Editions ghost kitchens higher) | Self-employed riders; legal challenges in multiple EU states | Acquired by DoorDash for £2.9 billion equity value, 53% below IPO |

|

|

|||

Two facts stand out. First, the profitable year for DoorDash arrived only after the company had achieved 67% market share in the United States and acquired Wolt and Deliveroo to remove its closest international competitors. Network effects and consolidation, not operational genius, were the proximate cause. Second, the platforms most exposed to European labour regulation, Deliveroo and Just Eat Takeaway, suffered the worst valuation collapses. The market priced in the cost of reclassifying drivers as employees long before any single member state finalized the rules.

Sources: NYC Department of Consumer and Worker Protection; Berkeley Labor Center; restaurant industry surveys 2020 to 2025.

The line chart captures the compression that defines the post-pandemic delivery economy. Consumer fees roughly doubled over five years, while net margins on delivery orders for independent restaurants collapsed toward zero. The shift was not gradual; it accelerated each year as platforms raised commissions, added service fees, and introduced new monetization layers like in-app advertising. Restaurants that depended on delivery for more than 30% of sales found themselves in a structural trap: leaving the platform meant losing customers, staying meant losing margin.

What Food Delivery Teaches Us

The food delivery experiment is now mature enough to draw conclusions. Three of them stand out for what they reveal about platform work, network effects, and venture capital pricing.

The first lesson is that network effects in food delivery are real but weaker than they look. Unlike social networks, where users would need to migrate together to a competing platform, delivery has minimal switching costs for consumers. Most users have two or three apps installed and price-shop between them, especially when promotions are running. The same is true for restaurants and drivers, who multi-home routinely. The “winner takes most” outcome was not driven by lock-in; it was driven by capital. Platforms that could afford to subsidize longer outlasted those that could not. Once the survivors consolidated, prices rose, and subsidies fell, but the fundamental product remained close to a commodity.

The second lesson is that the venture-capital-fuelled pricing of the 2014 to 2020 period systematically misled all three sides of the market. Consumers got used to artificially low delivery fees, restaurants got used to platforms paying for marketing, and drivers got used to pay rates that included signing bonuses and quest payments designed to bring people onto the platform. None of those prices reflected the underlying cost of the service. When the subsidies receded, every side felt squeezed at once, and the political backlash that followed produced everything from NYC’s minimum pay rate to the EU’s Platform Work Directive.

The third lesson is that platform work is not a separate category from regular employment. The legal and regulatory trajectory in California, New York, and the European Union has converged on the same answer: when a company controls how work is assigned, monitored, and compensated, the workers are functionally employees, regardless of contract language. Platforms can either build that cost into their model from the start or face retroactive liability. The 4% of revenue fines available to EU member states under the directive, combined with potential back-pay claims, mean misclassification is no longer a cheap risk. The next decade of platform business models will be designed around labour regulation, not in spite of it.

The broader question is what this teaches about the limits of “growth before profit” as a strategy. Food delivery showed that a multi-billion-dollar business can be built on losses sustained for over a decade. It also showed that the cost of that strategy is borne by workers, small merchants, and eventually consumers, not by venture capital. The path to profitability ran through consolidation, regulatory accommodation, and price increases, not through the technological breakthroughs the founding pitches had promised. Autonomous delivery, robot couriers, and drone fleets remain marginal. The product is still a person on a bike with a thermal bag.

MASEconomics Explains

Four economic concepts behind the economics of food delivery

Conclusion

The economics of food delivery show what happens when two-sided platforms, monopsony power over labour, and venture capital subsidies operate together for more than a decade. The model produced one large profitable platform in the United States, a series of regulatory pushbacks in Europe and major U.S. cities, and a workforce whose pay required legal floors to lift above poverty levels. Restaurant margins on delivery orders compressed toward zero as commissions climbed. The consolidation around DoorDash, Uber Eats, and a handful of regional players locked in pricing power that the early growth phase had concealed.

Profitability arrived in 2025, fifteen years after the first venture cheques and after the industry had absorbed billions in losses. The path to it ran through acquisition (Wolt, Postmates, Deliveroo), commission increases, and subscription products that raised the lifetime value of each consumer. The cost was distributed across workers, independent restaurants, and the public infrastructure that absorbed congestion and packaging waste. The EU Platform Work Directive and the NYC minimum pay rate are the first attempts to redistribute some of that cost back to the platforms.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.