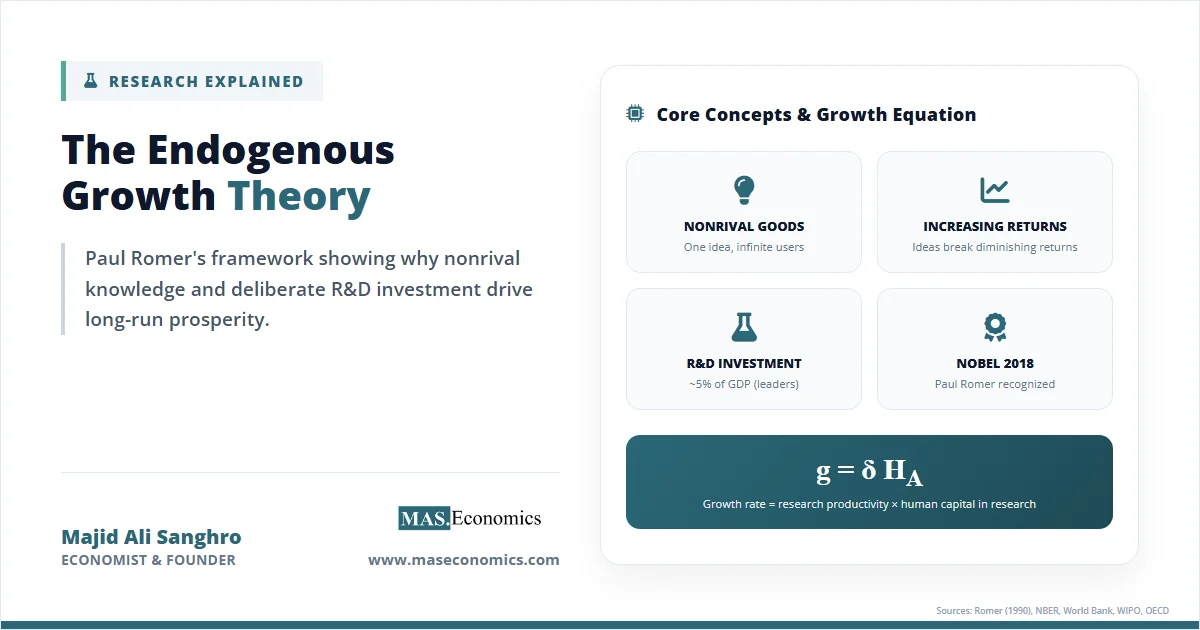

The endogenous growth theory, the Romer framework transformed macroeconomics by explaining what the Solow-Swan model left unexplained: where technological progress actually comes from. Paul Romer’s 1990 paper “Endogenous Technological Change” argued that ideas are produced inside the economy through deliberate investment in research and development, and because ideas are nonrival goods, they generate increasing returns that can sustain growth indefinitely. The work earned Romer the 2018 Nobel Prize in Economic Sciences and reshaped how governments think about innovation policy, intellectual property, and the mathematics of long-run prosperity.

The Core Idea

Neoclassical growth models treated technology as manna from heaven. The Solow-Swan growth model assumed a fixed saving rate, diminishing returns to capital, and an exogenous rate of technological progress labeled \( A \). Growth per worker eventually stalled at a steady state determined entirely by parameters the model could not explain. Two countries with identical preferences and technologies should converge to the same income level, yet the data stubbornly refused to cooperate: South Korea and Ghana had similar incomes in 1960, and by 2020 South Korean GDP per capita was roughly twenty times Ghana’s.

Romer’s breakthrough was to model technology as the output of a separate production sector. Firms hire researchers, purchase laboratory equipment, and produce designs, blueprints, and formulas. These outputs are nonrival, meaning one person’s use of a design does not prevent another person from using it. A chemical formula, a software algorithm, and a manufacturing process can be copied at near-zero marginal cost once discovered. Nonrivalry is the critical property that separates ideas from ordinary goods.

Because ideas are nonrival, the aggregate production function exhibits increasing returns to scale in rivalrous inputs plus ideas. If a firm doubles its capital and labor, it can double output, but if it also doubles its stock of ideas, it can more than double output. This single observation breaks the diminishing-returns engine that drove Solow toward a steady state. When returns to the accumulable factor (ideas) do not diminish, growth does not stop.

Romer’s model also solves the puzzle of why firms would ever invest in research if their discoveries are nonrival and freely copyable. The answer lies in monopolistic competition and patents. A firm that discovers a new design receives temporary market power through intellectual property protection, earns monopoly profits on the goods produced with that design, and uses those profits to fund the research in the first place. The market structure is not perfectly competitive, and that imperfection is essential to the theory’s logic. In perfect competition with free entry, nobody would pay for research that becomes free the moment it exists.

Mathematical Formulation

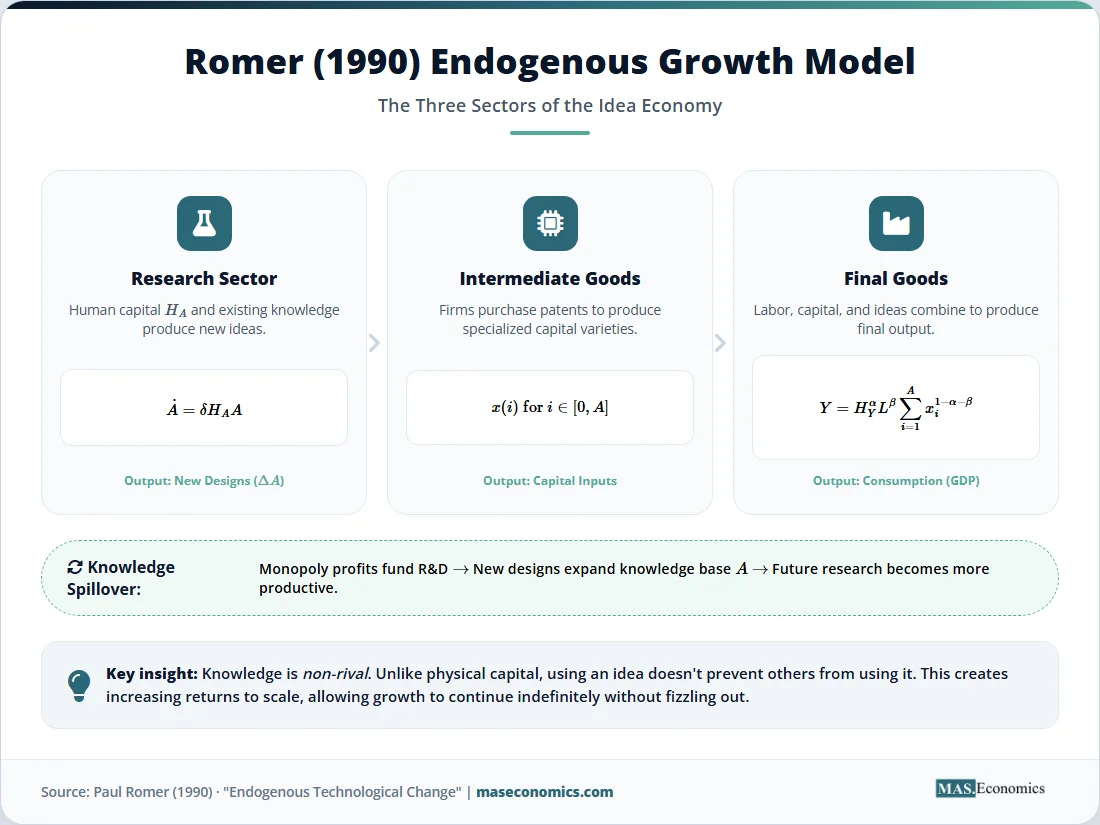

The Romer (1990) model divides the economy into three sectors: a final goods sector producing consumption output, an intermediate goods sector producing capital varieties under monopolistic competition, and a research sector producing new designs. The final goods production function takes the form:

Here \( Y \) is output, \( H_Y \) is human capital employed in final production, \( L \) is unskilled labor, \( x_i \) is the quantity of intermediate good \( i \), and \( A \) represents the stock of available designs (the measure of differentiated intermediate varieties). The exponent \( 1 – \alpha – \beta \) ensures constant returns in the rivalrous inputs \( H_Y \), \( L \), and the \( x_i \) varieties. Because \( A \) appears as the upper limit of the summation rather than as a multiplicative factor, doubling \( A \) while holding other inputs fixed more than doubles output — this is the increasing-returns-to-scale property.

The research sector produces new designs according to a linear technology in human capital:

where \( \dot{A} \) is the rate of new designs created per unit time, \( H_A \) is human capital employed in research, \( A \) is the existing stock of knowledge, and \( \delta \) is a productivity parameter. The presence of \( A \) on the right-hand side captures the “standing on shoulders” effect: past discoveries make future discoveries easier. This specification yields a constant long-run growth rate:

Growth is proportional to the fraction of human capital devoted to research. Doubling the research workforce doubles the growth rate – a “scale effect” that later endogenous growth models (Jones 1995) modified by introducing diminishing returns in the knowledge production function.

Intermediate goods producers each hold a patent on one variety, set prices as monopolists, and earn profits \( \pi \) proportional to the markup over marginal cost. The price of a design \( P_A \) equals the present discounted value of future monopoly profits:

Equilibrium requires that the marginal revenue product of human capital in research equals its wage in final production, linking innovation incentives to the real interest rate \( r \) and the parameters of the demand for intermediate goods. The full details are laid out in the original paper, but the essential mechanics are captured in the following variable table.

| Symbol | Definition | Role in the Model |

|---|---|---|

| \( Y \) | Final output | Aggregate consumption good |

| \( A \) | Stock of designs / knowledge | Nonrival input; source of sustained growth |

| \( H_Y \) | Human capital in final production | Rivalrous input to output |

| \( H_A \) | Human capital in research | Produces new designs |

| \( H \) | Total human capital | \( H = H_Y + H_A \) |

| \( L \) | Unskilled labor | Rivalrous input to output |

| \( x_i \) | Quantity of intermediate good \( i \) | Differentiated capital variety |

| \( \delta \) | Research productivity parameter | Efficiency of idea generation |

| \( \alpha, \beta \) | Output elasticities | Share parameters in production |

| \( g \) | Long-run growth rate | \( g = \delta H_A \) |

| \( \pi \) | Monopoly profit per variety | Incentive to conduct research |

| \( r \) | Real interest rate | Discount rate for future profits |

| \( P_A \) | Price of a design | Present value of monopoly rents |

| ||

The central result follows directly: because the growth rate depends on \( H_A \) rather than on diminishing returns to capital, the economy can grow forever at a positive rate, and the rate itself is determined by decisions inside the economy. Policy can influence growth by shifting human capital toward research through subsidies, education investment, or stronger patent protection.

Assumptions and Limitations

The Romer model rests on several assumptions that subsequent research has scrutinized. First, the linear specification \( \dot{A} = \delta H_A A \) generates a scale effect: larger economies should grow faster because they have more researchers. Empirically, this prediction fails. The United States has had a roughly constant per capita growth rate of around 2 percent for over a century despite a dramatic expansion in the research workforce. Charles Jones (1995) proposed a semi-endogenous variant where \( \dot{A} = \delta H_A^{\lambda} A^{\phi} \) with \( \phi < 1 \), reintroducing diminishing returns to the knowledge stock and eliminating the scale effect.

Second, the model assumes patents provide perfect and permanent protection, allowing innovators to capture the full monopoly rents from their designs. In practice, patents expire, are invented around, leak across borders, and vary enormously in quality. Knowledge spillovers are large and often unpriced, which means the private return to research falls short of the social return and innovation is chronically underprovided.

Third, the model treats human capital as homogeneous and assumes frictionless reallocation between research and production. Real economies face labor market frictions, geographic concentration of talent, and educational bottlenecks that slow the response of research labor to changing incentives. The mapping from the model’s \( H_A \) to the actual flow of scientists and engineers is far from straightforward.

Fourth, the model abstracts from the direction of innovation. All new designs are treated as equally useful additions to \( A \), but in reality research effort flows toward problems that promise commercial return, not toward problems with the highest social value. Daron Acemoglu’s work on directed technical change extends the Romer framework to handle these issues, showing how factor prices and market size shape what kinds of technology get developed.

Finally, the model is silent on institutions. Romer himself emphasized in later writing that rules, norms, and governance shape whether ideas get produced and diffused at all. Countries with weak property rights, corrupt judiciaries, or restrictive labor markets can have high research spending and low effective innovation. The model’s parameters \( \delta \) and the allocation of \( H \) are reduced-form summaries of institutional conditions that deserve their own analysis.

Empirical Evidence

Testing the Romer model against the Solow alternative requires distinguishing countries whose growth is explained by capital accumulation from those whose growth is explained by innovation. The evidence is now substantial. Countries that invest heavily in R&D – South Korea, Israel, Switzerland, Sweden, the United States – show sustained productivity growth that does not decelerate as capital stocks deepen. According to World Bank data on R&D intensity, Israel and South Korea now spend above 5 percent of GDP on research, roughly triple the OECD average in the 1970s.

The distinctive prediction of the Romer model is that growth does not converge to zero even as capital deepens. The Solow model predicts that an economy above its steady state should decelerate; the Romer model predicts continued growth driven by expansion in \( A \). The chart below contrasts the two predicted growth paths for an economy starting with identical initial conditions.

Figure 1. Solow versus Romer: Simulated output per worker over 100 years. Solow converges to a steady state once diminishing returns set in; Romer sustains positive growth through continued idea accumulation. Parameters: saving rate 0.25, depreciation 0.05, capital share 0.33, Romer growth rate 2%.

Cross-country regressions confirm the pattern. Jones (2019) reviews fifty years of growth accounting and concludes that ideas, not factor accumulation, explain most of the variation in long-run growth across advanced economies. The rise of the knowledge economy – software, pharmaceuticals, semiconductors, biotechnology – has been driven by sectors whose output depends almost entirely on past ideas rather than on accumulated physical capital.

Patent data provide another line of evidence. The global stock of utility patents has risen roughly tenfold since 1980, with the World Intellectual Property Organization reporting 3.55 million patent applications filed worldwide in 2022. Bloom, Jones, Van Reenen, and Webb (2020) document that while research effort has risen dramatically, research productivity per scientist has fallen – consistent with the Jones semi-endogenous extension and with declining marginal returns in the idea production function.

Firm-level evidence is also supportive. Studies of R&D tax credits in the United States, United Kingdom, and Canada consistently find that the credits increase research spending and, over longer horizons, increase patenting and productivity. The OECD R&D statistics show that countries offering generous and stable R&D tax incentives have higher business-funded research shares, in line with the Romer prediction that research responds to private returns.

Why It Matters

The practical consequences of endogenous growth theory are felt in every major innovation-policy debate of the past three decades. If growth depends on the accumulation of ideas, and if ideas are chronically underprovided because their social return exceeds their private return, then active government support for research is not optional – it is the mechanism through which the long-run growth rate is set. This logic now underpins the innovation strategies of the United States, the United Kingdom, Canada, and Australia, four advanced economies whose policy choices illustrate the theory in action.

The United States is the archetypal Romer-style economy. Federal research funding through the National Institutes of Health, the National Science Foundation, and the Department of Energy underwrites basic research whose returns are too diffuse for private firms to capture. The CHIPS and Science Act of 2022 committed approximately 52 billion dollars to semiconductor manufacturing and research, an explicit attempt to raise \( H_A \) in a strategic sector. The R&D tax credit, first introduced in 1981 and made permanent in 2015, has been evaluated in dozens of studies and is widely found to raise business research spending roughly dollar-for-dollar. Patent law, venture capital, and research universities together form the institutional scaffolding that converts Romer's equations into measurable growth.

The United Kingdom offers a different case. British productivity growth slowed sharply after 2008 and has failed to recover, a phenomenon economists now call the productivity puzzle. Part of the explanation is weak business investment in R&D, which remained below 2 percent of GDP through the 2010s compared with more than 3 percent in the United States. The Sunak government's 2023 target to raise total research spending to 2.4 percent of GDP and the Starmer government's 2025 follow-up reflected recognition that the Romer lever – the share of human capital in research – had been set too low. British policy now relies heavily on R&D tax credits for small and medium enterprises, direct funding through UK Research and Innovation, and targeted support through the Advanced Research and Invention Agency, modeled on the American DARPA.

Canada has struggled with a long-running innovation gap despite generous tax incentives. The Scientific Research and Experimental Development (SR&ED) tax credit is among the most generous in the OECD, yet Canadian business R&D intensity sits well below the OECD average. Canadian economists point to structural features – concentrated industries, small domestic market, shallow venture capital, and brain drain to the United States – that raise the effective cost of research even when tax treatment is favorable. The Canadian case illustrates that Romer's model parameters are not just chosen by policymakers; they are shaped by the full institutional environment in which research takes place.

Australia relies heavily on natural resources, and its innovation policy must contend with the gravitational pull of mining toward traditional factors of production. The Australian R&D Tax Incentive, reformed repeatedly since 2011, has channeled roughly ten billion Australian dollars annually toward business research. CSIRO, the national research agency, produced the Wi-Fi patent that generated more than 430 million Australian dollars in licensing revenue – a single example of the increasing returns to ideas that Romer's framework predicts. Australian universities, though small by US standards, punch above their weight in medical and agricultural research.

Beyond national policy, the Romer framework clarifies why some sectors grow faster than others. Software and pharmaceuticals exhibit extreme increasing returns: developing a new drug or a new algorithm costs billions but the marginal cost of distribution is near zero. These sectors have delivered the fastest productivity growth of the past thirty years and have produced the largest firms in history. By contrast, sectors dominated by rivalrous inputs – construction, personal services, hospitality – have seen much slower productivity growth, consistent with the theory's prediction that nonrival ideas are the engine of sustained progress.

The framework also illuminates international trade and intellectual property disputes. Because ideas cross borders, the returns to research depend on patent enforcement globally. The TRIPS agreement, trade disputes between the United States and China over technology transfer, and debates over compulsory licensing during the COVID-19 pandemic all involve trade-offs that Romer's model makes explicit: stronger property rights raise the incentive to innovate but reduce the diffusion benefits to users. There is no single optimal policy; the right balance depends on whether a country is closer to the innovation frontier (where stronger IP helps) or further behind (where faster diffusion helps).

Finally, the theory has reshaped how economists think about inequality. If ideas generate increasing returns, the innovators and shareholders of successful firms capture large rents, while workers in routine occupations face automation pressure. The top 1 percent income share in the United States rose from about 10 percent in 1980 to more than 20 percent by the 2020s, a pattern many economists trace partly to the concentration of returns in idea-intensive industries. The Romer framework does not prescribe a policy response, but it clarifies why skill-biased technological change and superstar firms have become defining features of advanced economies.

Romer's insights also connect to broader production theory. Understanding how inputs combine to produce output, and how those combinations change with technology, is essential background for his model. The standard treatment of production functions and isoquant curves provides the microeconomic foundations on which the Romer aggregate production function is built. Similarly, the measurement of national income sets the boundary conditions for what growth accounting can and cannot reveal, and the broader field of macroeconomics situates Romer's contribution in the century-long effort to understand why some nations prosper and others stagnate. Readers interested in the AI revolution should also consult AI as a new factor of production, which applies the Romer lens to the most recent technological wave.

MASEconomics Explains

4 economic concepts behind endogenous growth theory

Conclusion

The endogenous growth theory, the Romer framework, answered the central question the Solow model left open: where technology comes from. By modeling ideas as nonrival goods produced through deliberate investment in research, Romer showed that long-run growth is determined by choices made inside the economy, not by parameters dropped in from outside. The framework earned the 2018 Nobel Prize, reshaped innovation policy across the OECD, and remains the dominant lens through which economists analyze R&D subsidies, patent law, and the rise of knowledge-intensive industries.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.