Monetary policy in different countries affects the economy differently, depending on that country’s economic and financial structure, size, and degree of openness.

So it is crucial to study how the monetary transmission mechanism works in different countries and understand its theories. This will help reduce any uncertainty about the impact of monetary policy on the economy.

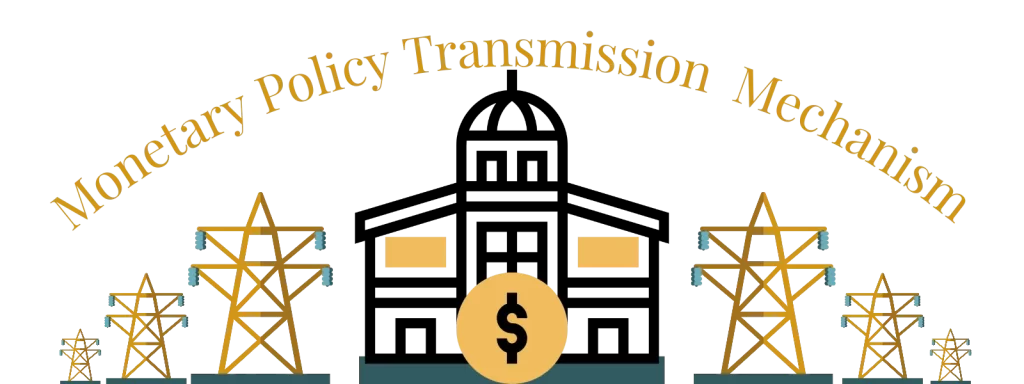

What is the Monetary Transmission Mechanism

The monetary transmission mechanism (MTM) is the process through which monetary policy influences economic activity.

The monetary transmission mechanism has been the subject of many theoretical and empirical studies since the 1960s, when general monetary policy studies began to gain momentum.

However, over time, the limitations in the financial markets have decreased, and monetary policies have gained importance within economic policies (especially after the 1980s). As a result, there has been a sudden spurt in the number of studies about the operation of the monetary transmission mechanism.

Theories that have been developed in order to understand how a central bank can influence economic activity are based on two main assumptions.

- One theory assumes that there exists an equilibrium between supply and demand for money and that this equilibrium depends only on the interest rate. This means that if the central bank increases or decreases policy rates, then the quantity of money will increase or decrease accordingly.

- Second, the assumption implies that when the central bank raises or lowers its policy rates, the market participants react by adjusting their expectations about future inflation to bring them back into line with what they believe would happen under normal circumstances.

As a result, any change in the expected path of nominal variables such as wages, profits, etc., which depend directly on the current value of money, should also reflect the new expectation regarding future inflation.

Theories of the Monetary Transmission Mechanism

The theory of monetary transmission assumes that the central bank’s actions affect both short-term and long-term interest rates. It further assumes that the central bank has no direct control over either output or employment. Instead, it controls the flow of funds from banks to households and firms.

These flows determine aggregate spending decisions, while the central bank influences the interest rate at which those funds are lent out. To determine how changes in interest rates affect output and inflation in both short-term and long-run effects.

There are two channels that impact real GDP when it comes to monetary policy:

- by affecting aggregate demand;

- and by influencing expectations about future money market conditions.

Moreover, there is an indirect channel through which monetary policy influences inflation via its effect on expected future inflation.

Monetarism view MTM

Monetarism is the belief that government must use monetary policy to manage the business cycle. Monetarist economists argue that governments cannot effectively regulate markets but rely on independent institutions like central banks.

They claim that the free banking system created after World War II led to high unemployment due to excessive credit creation during recessions.

According to monetarists, the answer to this problem is to reduce the money supply during periods of recession. Then, when the economy recovers, the central bank reduces the money supply again until total capacity is reached.

Monetarists state that changes in the money supply lead to variances in the general level of prices.

Keynesian view on MTM

According to Keynesian economics, the primary purpose of monetary policy is to maintain full employment. The idea of the approach is that if people have jobs, they will spend most of their income, thus increasing economic activity.

This increase in consumer spending leads to increased production, leading to higher incomes and lower unemployment.

In contrast, monetarists think that the primary function of monetary policy is to keep inflation below target levels. If the price level rises too quickly, consumers may not afford goods produced using newly available resources.

Four Monetary Transmission Mechanism Channels

After understanding different theories, let us explore transmission mechanism that operates through various channels, including interest rates, asset prices, credit conditions, and exchange rates.

The interest rate channel

It is the most direct way monetary policy affects economic activity. Changes in the federal funds rate (by FED) influence other interest rates, including treasury securities, mortgages, and corporate bonds.

These changes affect spending on capital goods (such as business investment in equipment and structures), housing, and durable consumer goods (such as automobiles). Higher interest rates reduce spending by making borrowing more expensive; lower interest rates stimulate spending by making borrowing cheaper.

The asset price channel

It also operates through changes in interest rates. When asset prices (such as stock prices or the price of a home) rise, households feel wealthier and spend more.

Conversely, when asset prices fall, households feel poorer and spend less. Thus, changes in asset prices can amplify or offset the effects of changes in interest rates on spending.

The credit conditions channel

It is another crucial link between monetary policy and economic activity. Changes in interest rates affect borrowing costs for both households and businesses.

For example, higher rates make it more expensive for firms to invest in new plants and equipment; lower interest rates reduce the cost of such investment.

Similarly, changes in mortgage rates affect housing demand: higher mortgage rates reduce demand by making home purchases more expensive; lower mortgage rates stimulate demand by making home purchases cheaper.

The credit conditions channel also operates through the effects of changes in asset prices on collateral values and credit availability. For example, a fall in house prices can lead to tighter lending standards for home mortgages, which would reduce spending on housing.

The exchange rate channel

It is the final link between monetary policy and economic activity. A weaker dollar makes U.S. exports and imports cheaper, stimulating spending on domestically produced goods and services.

Conversely, a stronger dollar has the opposite effect, dampening spending on domestic goods and services. The exchange rate channel is vital for specific sectors of the economy, instant manufacturing and tourism.

Conclusion

The transmission’s mechanisms to affect economic activity go through various channels. The most direct link between monetary policy and spending is through the interest rate channel, but the other channels are also important. The relative importance of the various channels depends on several factors, including the state of the economy and financial market conditions. Economists have different theories about how monetary policy should be used to achieve full employment and price stability. This information is essential for understanding how changes in the money supply can affect spending and investment decisions by households and businesses.

References:

Bulíř, A., & Vlček, J. (2021). Monetary transmission: Are emerging market and low-income countries different?. Journal of Policy Modeling, 43(1), 95-108.

Schoenmaker, D. (2021). Greening monetary policy. Climate Policy, 21(4), 581-592.Agbonlahor, O. (2014). The Impact of Monetary Policy on the Economy of the United Kingdom: A Vector Error Correction Model (VECM). European Scientific Journal, 10(16), 19-42.

Mohanty, M., & Turner, P. (2008). Monetary policy transmission in emerging market economies: what is new? . BIS papers.

Bernanke, B.S. and Gertler M. (1995). Inside the Black Box: The Credit Channel of Monetary Policy Transmission, Journal of Economic Perspectives 9, 27-48.

Taylor, J. B. (1995). The monetary transmission mechanism: an empirical framework. Journal of economic perspectives, 9(4), 11-26.