A government can pass a large spending package, watch the central bank hold rates steady, and still see no lasting rise in output, not because the policy was too small, but because the open economy quietly undid it. The same can happen in reverse: a central bank eases aggressively and the stimulus drains away through the balance of payments. These are not policy failures in the ordinary sense. They are the predictable result of how open economies absorb shocks, and the study of policy ineffectiveness open economy models is the study of exactly when and why a correctly executed policy produces nothing.

The result is not a single proposition but a pattern that depends on the exchange‑rate regime and the degree of capital mobility. The Mundell‑Fleming model shows that fiscal policy is neutralized under one set of conditions and monetary policy under another, and the mechanism in each case is an offsetting flow that the closed‑economy IS‑LM framework never anticipates. Understanding which policy fails, and through which channel, is what separates a working grasp of open‑economy macro from a memorized list of results.

Two Routes to Policy Ineffectiveness

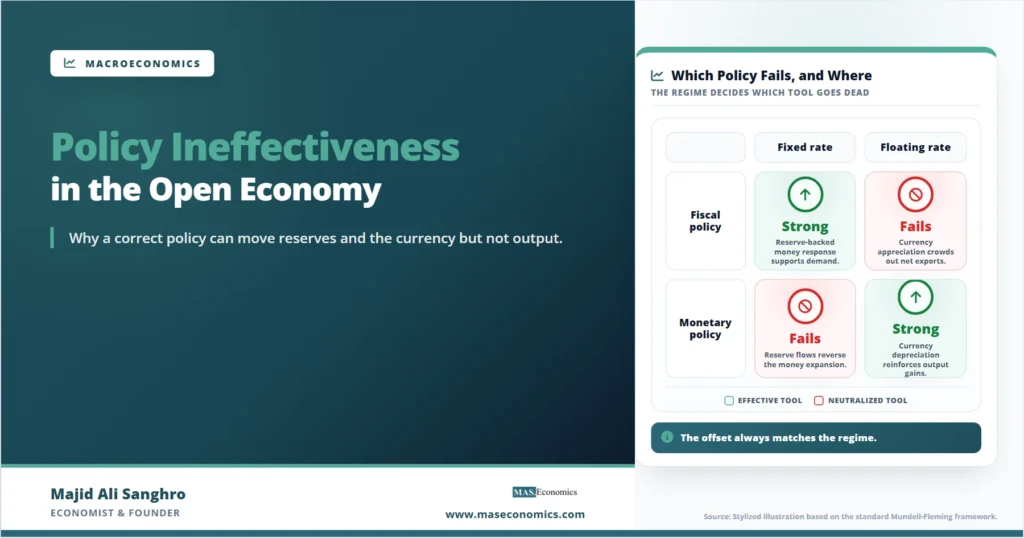

Policy ineffectiveness in the open economy comes in two forms that look opposite but share a structure. Under a fixed exchange rate, monetary policy is the instrument that fails. Under a floating exchange rate, fiscal policy is the one that fails. In both cases, the failing instrument sets off an external imbalance, and the economy’s response to that imbalance cancels the original policy.

The shared structure is an offsetting flow triggered by the interest-rate movement the policy creates. When a policy pushes the domestic interest rate away from the level consistent with external balance, capital moves, and the system responds in a way that reverses the policy’s effect on output. What differs between the two regimes is the variable that does the offsetting: reserves and the money supply under a peg, the exchange rate and net exports under a float.

The chain reads the same regardless of which policy fails. An expansionary policy moves the domestic interest rate, the rate gap drives a capital flow, the flow forces an offsetting adjustment, and output returns to where it began. The branch at the third step is the only difference: under a fixed rate the money supply adjusts to defend the peg, and under a float the exchange rate adjusts to clear the foreign exchange market. The outcome at the end of the chain is identical.

Monetary Policy Failure: Fixed‑Rate Case

Under a fixed exchange rate with high capital mobility, monetary policy cannot move output. Suppose the central bank expands the money supply to stimulate the economy. The immediate effect is a lower domestic interest rate and, briefly, higher output. But the lower rate sends capital abroad, the balance of payments moves into deficit, and the peg comes under downward pressure.

Defending the peg forces the central bank to sell foreign reserves and buy back domestic currency, which contracts the money supply. The contraction continues until the money supply returns to where it started and the interest rate is back at the world level. The attempted expansion has been completely reversed, and the only lasting trace is a fall in reserves. The central bank has, in effect, swapped reserves for nothing, because under a credible peg with open capital markets it does not control its own money supply.

The fixed-rate result. Monetary policy is ineffective under a fixed exchange rate with capital mobility because the money supply is endogenous. Any monetary expansion is reversed by the reserve flows required to defend the peg.

Fiscal Policy Failure: Floating‑Rate Case

Under a floating exchange rate with high capital mobility, the instrument that fails is fiscal policy. Suppose the government expands spending. Output and the domestic interest rate rise, and the higher rate attracts foreign capital, pushing the balance of payments toward surplus. Under a float, there is no peg to defend, so instead of accumulating reserves, the currency appreciates.

The appreciation makes domestic goods more expensive abroad and foreign goods cheaper at home, so net exports fall. The decline in net exports offsets the fiscal expansion, shifting the goods market back toward its starting point. Under perfect capital mobility, the offset is complete: the fall in net exports exactly cancels the rise in government spending, and output ends unchanged. The fiscal expansion shows up entirely as a stronger currency and a worse trade balance, a clean example of crowding out operating through the exchange rate rather than through the interest rate.

The floating-rate result. Fiscal policy is ineffective under a floating exchange rate with capital mobility because the appreciation it triggers crowds out net exports. The stronger currency cancels the demand the spending was meant to add.

Full Pattern Across Regimes

Setting the cases side by side shows that ineffectiveness is not a property of one instrument but of the match between an instrument and a regime. Each policy is powerful in one regime and powerless in the other, and the degree of capital mobility sharpens or softens the result.

| Setting | Fiscal policy | Monetary policy | Channel that neutralizes |

|---|---|---|---|

| Fixed rate, perfect mobility | Fully effective | Ineffective | Reserve flows reverse money supply |

| Floating rate, perfect mobility | Ineffective | Fully effective | Appreciation crowds out net exports |

| Fixed rate, imperfect mobility | Strong | Weak, partial | Partial reserve offset |

| Floating rate, imperfect mobility | Weak, partial | Strong | Partial exchange-rate offset |

| Pattern | Fails under floating | Fails under fixed | Offset matches the regime |

|

Source: MASEconomics editorial synthesis of the Mundell-Fleming framework.

|

|||

The summary row captures the symmetry: fiscal policy fails under a float, monetary policy fails under a peg, and the neutralizing channel always matches the variable the regime leaves free to move. The imperfect-mobility rows show that the ineffectiveness results are sharpest at the perfect-mobility extreme and soften as capital becomes less responsive. A steeper BP curve means the offsetting flow is weaker, so the failing instrument recovers some traction rather than being fully canceled.

Distinct from Rational‑Expectations Ineffectiveness

The phrase policy ineffectiveness also names a different and more famous proposition in closed-economy macroeconomics, and the two should not be confused. In the closed-economy version associated with rational expectations, anticipated monetary policy has no real effect because agents adjust their expectations and prices in advance, leaving only unanticipated policy able to move output. That mechanism runs through expectations and price-setting, and it applies even in a closed economy with no external sector at all.

The open-economy ineffectiveness described here is a different animal. It does not depend on expectations or on prices adjusting; it works even with fixed prices and backward-looking agents, because the offsetting flow comes from the balance of payments rather than from anticipation. The contrast is worth holding clearly: the rational-expectations result is about what agents know, while the open-economy result is about how capital and the exchange rate move. The expectations-based proposition is treated in the discussion of rational expectations theory, which addresses a separate channel entirely.

Caveat. Open-economy ineffectiveness and rational-expectations ineffectiveness share a name but not a mechanism. One works through balance-of-payments flows under a given regime; the other works through anticipated policy and forward-looking expectations. Treating them as the same result leads to wrong conclusions about when each applies.

Reliability of the Results

The clean ineffectiveness results rest on assumptions that rarely hold in full. Perfect capital mobility is the sharpest case, and real capital is mobile but not perfectly so, which means both instruments usually retain some effect. A credible peg is assumed when monetary policy is judged powerless, but pegs can lose credibility, and an expected devaluation breaks the clean reversal. The exchange rate is assumed to move freely under a float, when many countries manage their currencies and dampen the appreciation that would otherwise neutralize fiscal policy.

Fixed prices are assumed throughout, which confines the results to the short run. Over longer horizons, prices adjust, the real exchange rate can move even under a nominal peg, and the static mapping from regime to ineffectiveness becomes less reliable. None of this overturns the core insight, which is that an open economy contains automatic channels that can cancel domestic policy. It does mean the results are best read as tendencies that are strongest at the extremes, not as guarantees that a particular policy will do nothing.

Explains

Two ideas behind open-economy ineffectiveness

See how these channels fit the wider open-economy model.

Explore the MASEconomics BlogConclusion

The lesson of policy ineffectiveness open economy models is that the open economy contains its own automatic stabilizers against domestic policy, and which policy they cancel depends entirely on the exchange‑rate regime. Under a fixed rate, the money supply is endogenous, so monetary policy is reversed by the reserve flows that defend the peg. Under a float the exchange rate is free, so fiscal policy is crowded out by the appreciation it triggers. The same offsetting logic produces opposite results in the two regimes.

The unifying mechanism is the interest‑rate movement that any expansionary policy creates. That movement drives a capital flow, the flow forces an adjustment in whichever variable the regime leaves free, and the adjustment cancels the policy’s effect on output. The neutralizing channel always matches the regime: reserves and the money supply under a peg, the currency and net exports under a float.

Read with its assumptions in mind, this is one of the most durable insights in open‑economy macroeconomics. The results are sharpest under perfect capital mobility and a clean regime, and they soften when mobility is limited or the regime is managed. But the underlying point holds across the range: a country that opens its capital account cannot treat domestic policy as if the rest of the world were absent, because the external accounts will respond, and that response is what decides whether a policy moves output or merely moves reserves and the exchange rate.

Frequently Asked Questions

What is policy ineffectiveness in open economy models?

It is the result that a correctly executed monetary or fiscal policy can produce no lasting change in output, because the open economy generates an offsetting flow that cancels it. Under a fixed exchange rate monetary policy is neutralized by reserve flows; under a floating exchange rate fiscal policy is neutralized by an offsetting exchange-rate movement.

Why is monetary policy ineffective under a fixed exchange rate?

A monetary expansion lowers the domestic interest rate, which sends capital abroad and pushes the balance of payments into deficit. Defending the peg forces the central bank to sell reserves and buy back domestic currency, contracting the money supply back to its starting point. With capital mobile and the money supply endogenous, the expansion is fully reversed.

Why is fiscal policy ineffective under a floating exchange rate?

A fiscal expansion raises the domestic interest rate, attracting capital and pushing the balance of payments toward surplus. Under a float the currency appreciates instead of accumulating reserves, which makes domestic goods less competitive and reduces net exports. The fall in net exports offsets the spending increase, and under perfect mobility the offset is complete, leaving output unchanged.

Is this the same as the rational expectations policy ineffectiveness?

No. The rational-expectations proposition is a closed-economy result in which anticipated policy has no real effect because agents adjust expectations and prices in advance. The open-economy result works through balance-of-payments flows under a given exchange-rate regime and applies even with fixed prices and no forward-looking expectations. They share a name but not a mechanism.

Does capital mobility change the ineffectiveness results?

Yes. The results are sharpest under perfect capital mobility, where the offsetting flow is strong enough to cancel the policy completely. With imperfect mobility the BP curve is steeper, the offset is only partial, and the failing instrument recovers some effect on output rather than being fully neutralized.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics