On its first meeting under a brand-new structure, the board that sets Australian interest rates did something the old one never could: it published exactly how each member voted. In May 2026, the Reserve Bank of Australia raised its cash rate target to 4.35%, and the minutes recorded that eight members voted in favour while one preferred to hold. That single line, a recorded split rather than a unanimous-sounding consensus, captured the most important institutional change in the bank’s modern history. After a landmark independent review, the body that had governed Australian monetary policy for more than sixty years was split in two, and the way the country’s central bank makes and explains its decisions was rebuilt.

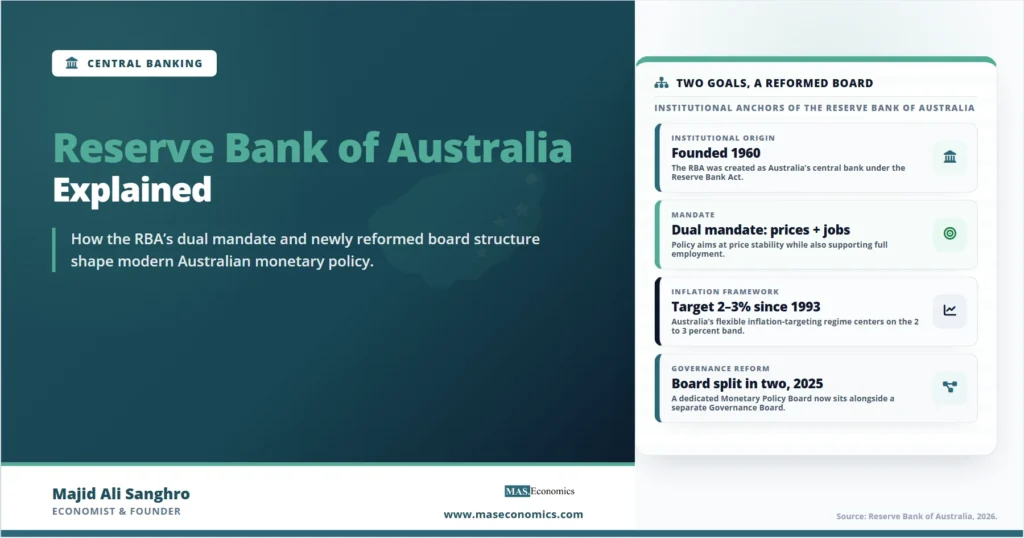

The Reserve Bank of Australia is the central bank of one of the world’s wealthiest economies. Established in 1960, it issues the Australian dollar, sets the cash rate, holds the nation’s reserves, and works to keep the financial system stable. What distinguishes it from many of its peers is the breadth of its mandate. Where the Bank of Canada and the State Bank of Pakistan organize policy around inflation above all else, the Reserve Bank of Australia pursues a genuine dual mandate, charged with delivering both price stability and full employment, and weighing the two against each other in every decision. That balancing act, conducted through a freshly reformed governance structure, is the heart of what the institution does.

From Commonwealth Bank to Central Bank

The Reserve Bank of Australia is younger as a distinct institution than its functions are old. Central banking in Australia was originally carried out by the Commonwealth Bank, a government-owned bank established in 1911 that gradually accumulated central banking responsibilities through the following decades. By the 1950s, an obvious conflict had become untenable: the same institution was both regulating the private banks and competing with them as a commercial lender. The solution was separation.

The Reserve Bank Act 1959 carved the central banking functions out of the Commonwealth Bank and vested them in a new, dedicated central bank, which opened for business on January 14, 1960. The commercial operations were spun off into what eventually became the Commonwealth Bank of Australia as it exists today. The new Reserve Bank inherited its predecessor’s staff, its board, and, importantly, its charter. The driving idea behind the separation was that decisions so central to national prosperity should be made by impartial experts, insulated as far as possible from political and commercial interests.

That charter still defines the institution. The Reserve Bank Act charged the bank with conducting policy so as best to contribute to three goals: the stability of the currency, the maintenance of full employment, and the economic prosperity and welfare of the people of Australia. These words, inscribed on the wall of the bank’s Sydney head office, have survived every amendment since. The modern dual mandate, price stability and full employment, is the contemporary expression of that founding charter rather than a departure from it. Australia’s central bank was built from the start around employment as well as money, and that inheritance shapes it to this day.

The 1993 Inflation Target

For its first three decades, the bank pursued its charter without an explicit numerical anchor, and Australia, like most advanced economies, suffered the high and volatile inflation of the 1970s and 1980s as a result. The modern framework began, almost casually, with a speech.

In March 1993, Governor Bernie Fraser told a gathering of Sydney economists that holding inflation to an average of 2 to 3% over a period of years would be a good outcome. It was one of the earliest statements to combine a general commitment to low inflation with a specific number, which is the essential feature of an inflation target. Australia came to the idea slightly later than New Zealand, which had pioneered formal inflation targeting, and the adoption was evolutionary rather than a single dramatic announcement. The target was progressively made more explicit through subsequent speeches, endorsed by the Treasurer, and formalized in 1996 in the first Statement on the Conduct of Monetary Policy, an agreement between the Treasurer and the Governor that has been renewed ever since.

Two features of the Australian target distinguish it. The first is its formulation as an average over the cycle rather than a rate to be hit at every moment, which builds in flexibility to look through temporary shocks, the logic explored in our explainer on inflation targeting. The second is that the target was always pursued alongside the employment goal rather than to its exclusion, consistent with the charter. The credibility this framework brought is widely credited with giving Australian policy the flexibility to absorb the Asian financial crisis and later shocks without a domestic recession, part of the record traced in our profile of the economies we cover.

2023 Review and Split Board

The most significant recent development in the institution is not a rate decision but a structural reform. In 2023, an independent Review of the Reserve Bank of Australia, the first comprehensive external examination of the bank in a generation, recommended a sweeping modernization of how it is governed and how it makes decisions. The government accepted the recommendations, and the amended Reserve Bank Act came into force on March 1, 2025.

The central change was splitting the single Reserve Bank Board into two separate bodies. For over sixty years, one board had been responsible for everything: setting interest rates and also running the institution as an organization. The review judged that these were distinct tasks requiring distinct expertise, and divided them.

The new Monetary Policy Board is now solely responsible for setting the cash rate. A separate Governance Board handles the running of the institution: staffing, budgets, and organizational strategy. The reform also changed how decisions are communicated. The Monetary Policy Board meets less frequently than the old board but for longer, publishes the votes of its members rather than presenting an undifferentiated consensus, and holds a press conference after every decision. The May 2026 record of an eight-to-one vote is the visible product of this change: a degree of transparency about internal disagreement that the bank had never previously offered, and that brings it closer to the practice of the United States Federal Reserve.

Dual Mandate in Practice

The defining analytical feature of the Reserve Bank of Australia is its dual mandate. The bank is charged with delivering both price stability, expressed as the 2 to 3% inflation target, and full employment, the maximum level of employment consistent with stable inflation. Unlike a pure inflation targeter, which treats employment as a consideration subordinate to the price goal, the Reserve Bank treats the two as genuine co-equal objectives, a structure it shares with the Federal Reserve but not with most other inflation-targeting central banks.

This dual mandate is the source of the hardest decisions the bank faces, because the two goals frequently pull in opposite directions. When inflation is high, the textbook response is to raise rates and cool the economy, which tends to raise unemployment. When unemployment is high, the response is to cut rates and stimulate demand, which risks higher inflation. A pure inflation targeter resolves this tension by giving priority to inflation. A dual-mandate central bank must instead make a genuine judgment about how to balance the two, and that judgment is exactly what the Monetary Policy Board debates. The trade-off is the one described by the relationship between inflation and unemployment that economists have studied for decades.

The board that makes this judgment combines insiders and outsiders. It is chaired by the Governor, who since September 2023 has been Michele Bullock, the first woman to lead the institution, alongside the Deputy Governor, the Secretary to the Treasury, and external members appointed for their expertise. The mix is designed to bring independent judgment to bear while keeping the bank’s own analysis at the centre, and the published votes now make the balance of opinion visible.

Cash Rate and Transmission Channel

The bank’s primary instrument is the cash rate, the interest rate on overnight loans between banks. By moving this single rate, the Reserve Bank influences the entire structure of interest rates in the economy: mortgage rates, business lending, deposit rates, and the exchange rate. The cash rate is set by the Monetary Policy Board and announced after each meeting, and it is the number that dominates Australian economic news.

What makes the cash rate unusually powerful in Australia is the structure of the mortgage market. Most Australian home loans carry variable interest rates, which adjust almost immediately when the cash rate changes, in contrast to the United States, where long-term fixed-rate mortgages shield most borrowers from rate moves for years. Combined with household debt levels among the highest in the developed world, this means a change in the cash rate reaches household budgets quickly and forcefully, the dynamic examined in our profile of the Australian economy. The transmission of policy to spending is therefore faster and stronger than in most peer economies, the general mechanism set out in our explainer on the monetary transmission mechanism. The recent cycle illustrated this vividly: the bank raised the cash rate sharply from near zero to a peak of 4.35% to combat post-pandemic inflation, then began easing as inflation moderated, before the pressures of 2026 forced it to tighten again.

Beyond the cash rate, the bank’s toolkit is that of a modern central bank. It conducts open market operations to keep the cash rate at target, manages the foreign reserves and the floating dollar that has served as Australia’s principal shock absorber since 1983, and acts as lender of last resort in a crisis. Bank supervision, once a Reserve Bank function, was transferred to a dedicated prudential regulator in 1998, leaving the bank focused on monetary policy and overall financial stability. The review also tasked the bank with developing a clearer framework for additional policy tools, such as those used when the cash rate approaches its lower bound, a piece of work now underway.

Pressures Ahead

Three challenges will define the Reserve Bank’s work through the rest of the decade.

The first is embedding the new framework. A governance reform looks clean on paper, but its value depends on whether the split boards, the recorded votes, and the more deliberate communication actually improve the quality and credibility of decisions. The early meetings under the new structure, including the divided vote of May 2026, are the first real tests of whether greater transparency strengthens the bank or merely exposes disagreement in ways that complicate its message.

The second is managing supply-driven inflation under a dual mandate. Much of the inflation pressure Australia has faced recently has come from sources the cash rate cannot directly address: global fuel prices, capacity constraints, and external shocks. Raising rates to fight supply-driven inflation imposes a real cost on employment while doing little to reverse the price shock itself, which sharpens the dual mandate’s central tension. The bank’s challenge is to keep inflation expectations anchored without sacrificing more employment than necessary, a judgment with no formulaic answer.

The third is the heavily indebted household sector that makes its policy so potent. The same fast transmission that gives the cash rate its power also means the bank operates with a narrow margin for error: a rate path that would be merely restrictive elsewhere can squeeze Australian households hard and quickly. The bank must weigh the financial stability of a population deeply exposed to mortgage costs against its inflation and employment goals, a constraint that runs through every decision and ties its work directly to the structure of the housing market.

Explains

Four ideas behind the Reserve Bank of Australia

Connect these ideas to the wider library of central banking and inflation articles.

Explore the MASEconomics BlogConclusion

The Reserve Bank of Australia is a central bank defined by two things: a dual mandate inherited from its 1960 charter, and a governance structure rebuilt in 2025. The charge to pursue both price stability and full employment, rather than ranking inflation above all else, gives the bank a harder balancing act than most of its peers and places genuine judgment at the centre of every decision. The 2023 review and the split into a Monetary Policy Board and a Governance Board modernized how that judgment is made and, through recorded votes and regular press conferences, how it is explained to the public.

The decade ahead will test both inheritances. The bank must prove that its reformed structure produces better and more credible decisions, manage inflation shocks that originate outside its control without sacrificing more employment than necessary, and do all of this while wielding a cash rate that bites Australian households faster and harder than rate changes do almost anywhere else. The floating dollar and a credible inflation-targeting record remain powerful assets. Whether the new framework lives up to the ambition of the review will be judged not in calm periods but in the next moment when price stability and full employment pull sharply against each other.

Frequently Asked Questions

What is the Reserve Bank of Australia?

The Reserve Bank of Australia is Australia’s central bank, established in 1960 and headquartered in Sydney. It issues the Australian dollar, sets the cash rate, manages the nation’s reserves, and works to keep the financial system stable. Its mandate is to deliver both price stability and full employment.

What is the RBA’s inflation target?

The Reserve Bank aims to keep consumer price inflation between 2 and 3% on average over the cycle. The target was first articulated by Governor Bernie Fraser in 1993 and formalized in the 1996 Statement on the Conduct of Monetary Policy, an agreement between the Treasurer and the bank that has been renewed since.

Who sets interest rates in Australia?

Since March 2025, interest rates are set by the Monetary Policy Board, created when the 2023 review split the old Reserve Bank Board in two. The board is chaired by the Governor and includes the Deputy Governor, the Treasury Secretary, and external members. It publishes the votes of its members with each decision.

Why does the RBA have a dual mandate?

The dual mandate of price stability and full employment comes from the bank’s founding charter in the Reserve Bank Act, which has charged it with both goals since 1960. Unlike pure inflation targeters, the Reserve Bank treats the two as co-equal objectives and must balance them, a structure it shares with the US Federal Reserve.

Why are RBA rate changes felt so quickly in Australia?

Most Australian mortgages carry variable interest rates, so a change in the cash rate flows through to household repayments almost immediately, rather than being locked in for years as with US fixed-rate loans. Combined with very high household debt, this makes monetary policy unusually fast and powerful in Australia.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics