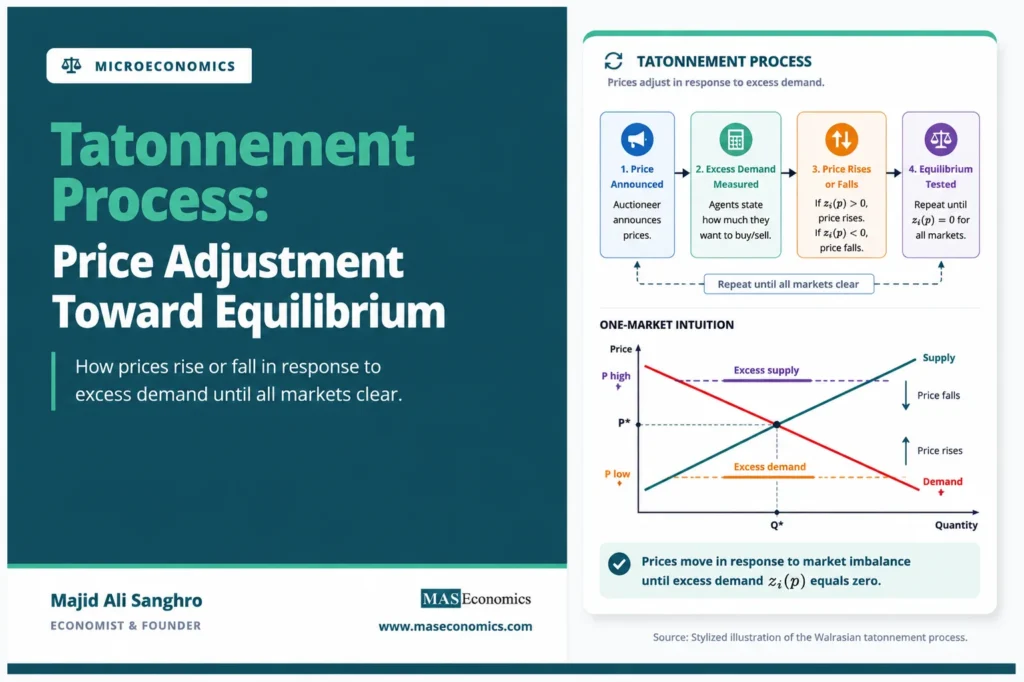

A competitive market can face excess demand at one price and excess supply at another, but equilibrium requires a price vector that clears all markets at the same time. The tatonnement process describes a theoretical price-adjustment mechanism in which prices rise when excess demand is positive and fall when excess demand is negative.

The word is usually written as tatonnement in English-language economics, with tâtonnement as the French spelling. The idea comes from Léon Walras’s auctioneer-style picture of markets groping toward equilibrium before trades are finalized.

The process is important because it separates two questions in general equilibrium. One question asks whether an equilibrium price vector exists. The tatonnement question asks whether price adjustment can move the economy toward that equilibrium.

Prices respond to excess demand

The tatonnement process begins with a price vector. At those prices, each market may have excess demand, excess supply, or balance. Excess demand means buyers want more than sellers offer. Excess supply means sellers offer more than buyers want.

The adjustment rule is simple. If a market has positive excess demand, its price rises. If a market has negative excess demand, its price falls. If excess demand is zero, the price has no reason to move in that market.

Basic Adjustment Rule

Here, \(p_i\) is the price of good \(i\), \(z_i(p)\) is excess demand for good \(i\) at the current price vector, and \(\lambda\) measures the speed of price adjustment. The formula is stylized. It does not describe a literal market institution in most modern economies. It describes a clean theoretical mechanism linking imbalance to price movement.

When \(z_i(p) > 0\), buyers are competing for a scarce good. The price rises. When \(z_i(p) < 0\), sellers are trying to dispose of excess supply. The price falls. When \(z_i(p)=0\), the market clears at that price.

The auctioneer blocks false trades

Walras’s classic version of tatonnement uses an auctioneer. The auctioneer announces prices, agents state how much they want to buy or sell at those prices, and the auctioneer adjusts prices before actual trades occur. Trading begins only after all markets clear.

This “no false trading” assumption is the key abstraction. It prevents agents from making transactions at disequilibrium prices. Without that assumption, early trades could change endowments, income, and future demands. The adjustment path would then depend not only on prices but also on who traded before equilibrium was reached.

The auctioneer device keeps the model clean. It lets the theory study price adjustment while holding the underlying endowments and preferences fixed. Prices change in response to announced excess demands, but allocations do not change until equilibrium prices are found.

This is why tatonnement is best understood as a stability device, not as a realistic description of every market. It asks whether a price system guided by excess demand signals moves toward equilibrium when trades are postponed until market clearing.

Core idea. Tatonnement is a price-adjustment process without disequilibrium trading. Prices move first; trades occur only after markets clear.

Market clearing becomes the target

The destination of the tatonnement process is a price vector \(p^*\) at which every market clears. In formal terms, equilibrium requires:

Market-Clearing Target

If this condition holds, there is no excess demand and no excess supply. Buyers’ planned purchases match sellers’ planned supplies in every market included in the model.

The adjustment process can be described in three steps. First, prices are announced. Second, excess demands are calculated. Third, prices are adjusted according to the sign and size of excess demand. The process repeats until the excess demand vector becomes zero.

The diagram shows the one-market intuition behind the broader general equilibrium process. When the price is below equilibrium, quantity demanded exceeds quantity supplied, so price rises. When the price is above equilibrium, quantity supplied exceeds quantity demanded, so price falls. At equilibrium, excess demand is zero and the adjustment pressure disappears.

General equilibrium adds many markets

In partial equilibrium, price adjustment can be shown with one demand curve and one supply curve. In general equilibrium, the same logic becomes more complex because every price can affect every market. A change in the price of one good changes real wealth, substitution patterns, and the excess demand for other goods.

This means tatonnement is not simply a collection of separate one-market corrections. The price of good \(i\) responds to \(z_i(p)\), but \(z_i(p)\) itself depends on the whole price vector. Food demand may depend on wages. Labor supply may depend on goods prices. Asset demand may depend on expected returns and income. The market system is connected.

A compact way to write this is:

Vector Form

Here, \(\dot{p}\) represents the movement of the whole price vector over time. The equation says that prices adjust together, not one by one in isolation. This is why tatonnement belongs to general equilibrium theory rather than ordinary single-market analysis.

The link to market balance is especially clear when combined with Walras law. The total value of excess demand across all markets must balance when budget constraints are respected. Tatonnement then describes how the price vector might move in response to those excess demands.

Stability requires more than existence

An equilibrium price vector can exist without being stable under tatonnement. Existence means there is at least one price vector where markets clear. Stability means the adjustment process moves prices toward that vector after a small disturbance.

The distinction is central. A model can prove that equilibrium exists and still fail to show that ordinary price adjustment will reach it. If prices move in the wrong direction, overshoot, cycle, or amplify the imbalance, the tatonnement process may not converge.

In the simplest one-market diagram, stability looks almost automatic. Excess demand raises price, excess supply lowers price, and price moves toward the crossing point. In a many-market economy, the same rule can generate complicated feedback. Raising one price may reduce excess demand in that market but increase excess demand somewhere else. The adjustment path depends on the entire excess demand system.

For this reason, tatonnement is closely related to the stability problem in general equilibrium. It provides a rule of motion, but the rule does not guarantee convergence under all possible preferences and endowments.

| Concept | Main question | Economic meaning |

|---|---|---|

| Equilibrium existence | Does a clearing price vector exist? | A solution is possible within the model. |

| Tatonnement stability | Do prices move toward that vector? | The adjustment rule converges after imbalance. |

| Disequilibrium trading | Do trades occur before clearing? | Endowments and demands may change during adjustment. |

| Core distinction | Existence is not convergence. | A clearing price can exist even when adjustment fails. |

|

Source: MASEconomics editorial synthesis based on standard general equilibrium theory.

|

||

False trading changes the path

The no-false-trading assumption is useful but restrictive. Real markets often trade before all prices have fully adjusted. A worker may accept a wage before goods prices settle. A firm may sell inventory before input prices update. A household may buy assets before labor income is known with certainty.

Once these trades occur, the starting point changes. Agents no longer have the same endowments or wealth positions they had before disequilibrium trading. The later excess demand functions may differ from the original ones. The market does not merely move along a fixed adjustment path; it rewrites the path as trades occur.

This matters because tatonnement isolates a pure price-discovery process. It asks what happens when markets announce prices, record intended trades, and adjust prices without executing those trades. That abstraction is useful for theory, but it cannot capture all institutional details of real markets.

Financial markets may resemble tatonnement more closely in some moments because orders can be revised quickly before final execution. Labor markets, housing markets, and long-term contract markets usually do not. In those markets, disequilibrium trades, search frictions, and contracts shape the adjustment path.

Speed can create overshooting

The adjustment parameter \(\lambda\) affects how aggressively prices respond to excess demand. If \(\lambda\) is small, prices move slowly. Slow movement may delay convergence, but it can also reduce the risk of large overshooting. If \(\lambda\) is large, prices respond strongly. Strong responses may correct shortages quickly, but they can push prices beyond equilibrium.

In a one-market setting, excessive adjustment speed can create oscillation around equilibrium. A low price produces excess demand, price rises sharply, the new price produces excess supply, and price falls sharply. The market keeps moving around the equilibrium instead of settling smoothly.

In a many-market setting, overshooting can be more complicated because one market’s price movement changes other markets’ excess demands. Fast adjustment in one market can create new imbalance elsewhere. Stability depends on both the adjustment speed and the structure of cross-market substitution.

Caveat. Tatonnement convergence is not automatic. It depends on the shape of excess demand functions, the speed of price adjustment, and whether disequilibrium trades are excluded.

The process clarifies market coordination

Tatonnement remains useful because it turns equilibrium into a coordination problem. An economy is not in equilibrium simply because each market has a price. Equilibrium requires a system of prices that makes all individual plans mutually compatible.

The process also clarifies the role of prices. Prices are not only numbers attached to goods. They are signals that summarize scarcity, opportunity cost, and feasible trade. When excess demand is positive, the price signal says the good is underpriced relative to current plans. When excess supply is positive, the signal says the good is overpriced relative to current plans.

This interpretation helps separate market adjustment from market perfection. Tatonnement does not assume that real markets are frictionless in practice. It provides a benchmark for thinking about how prices would have to move if excess demand signals were the only adjustment force and if trades waited until the system cleared.

That benchmark is valuable even when the real economy departs from it. Sticky prices, contracts, money, credit, inventories, and institutions can all modify price adjustment. The tatonnement process gives general equilibrium theory a clean starting point before those complications are added.

Explains

Three concepts behind tatonnement

Related equilibrium concepts are developed across the MASEconomics microeconomics library.

Explore the MASEconomics BlogConclusion

Tatonnement process analysis explains price adjustment as a response to excess demand. Prices rise when buyers want more than sellers offer, fall when sellers offer more than buyers want, and stop adjusting when markets clear.

The process is important because it separates equilibrium from convergence. A market-clearing price vector can exist, but a particular price-adjustment rule may or may not lead the economy toward it. Stability depends on the structure of excess demand, cross-market feedback, and the assumptions made about trading before equilibrium.

Tatonnement is therefore best read as a theoretical benchmark. It does not describe every real market, but it identifies the price-discovery logic behind Walrasian general equilibrium and highlights why market coordination requires more than isolated supply-and-demand crossings.

Frequently Asked Questions

What is the tatonnement process?

The tatonnement process is a theoretical price-adjustment mechanism in which prices rise when excess demand is positive and fall when excess demand is negative. Trading occurs only after markets clear.

Who introduced tatonnement in economics?

The concept is associated with Léon Walras and his auctioneer-style model of price adjustment in general equilibrium theory.

Does tatonnement always reach equilibrium?

No. Tatonnement reaches equilibrium only under conditions that make the price-adjustment process stable. In many-market systems, feedback across markets can prevent convergence.

What is false trading in tatonnement?

False trading means transactions occur before equilibrium prices are reached. Standard tatonnement excludes false trading so that prices can adjust without changing endowments during the adjustment process.

Why is tatonnement important in general equilibrium?

Tatonnement shows how prices might adjust toward a market-clearing vector in a connected system of markets. It links excess demand, price movement, and equilibrium stability.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics