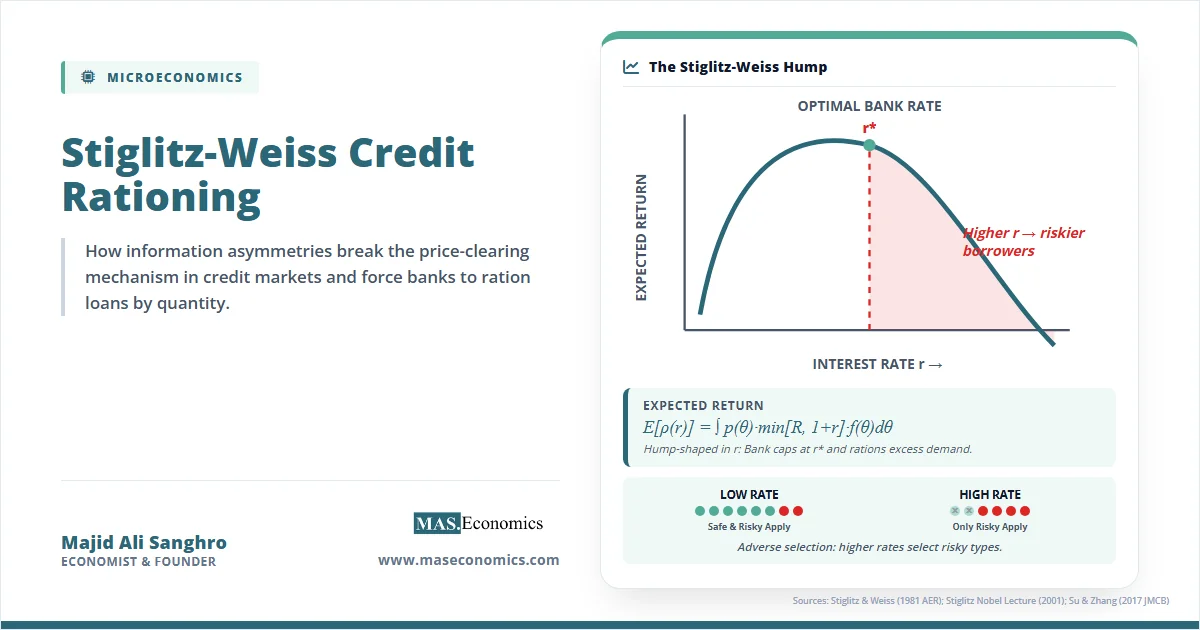

Classical price theory predicts that excess demand for credit should be eliminated by higher interest rates until supply equals demand. Yet banks routinely deny loans to creditworthy applicants who are willing to pay higher rates, rather than simply raising the price of credit. Stiglitz-Weiss credit rationing explains this paradox. In their seminal 1981 American Economic Review paper, Joseph Stiglitz and Andrew Weiss demonstrated that under asymmetric information about borrower risk, banks rationally cap loan interest rates and ration credit through quantity restrictions rather than letting prices clear the market. Because higher rates attract worse borrowers (adverse selection) and induce riskier projects (moral hazard), raising rates beyond a certain point actually reduces the bank’s expected return. This insight fundamentally changed how economists understand credit markets and earned Stiglitz a share of the 2001 Nobel Prize in Economics, alongside George Akerlof and Michael Spence, for foundational work on markets with asymmetric information.

What the Stiglitz‑Weiss Model Shows

The puzzle that Stiglitz and Weiss tackled is ubiquitous in the real world but impossible in a standard supply-and-demand framework. In a classical market, if more borrowers want loans than banks are willing to supply at the current interest rate, the interest rate rises. Some borrowers drop out, some lenders enter, and the market clears. There is no excess demand. Yet anyone who has applied for a mortgage, a small business loan, or a credit card knows that lenders frequently say no, even to applicants who insist they would pay a higher rate.

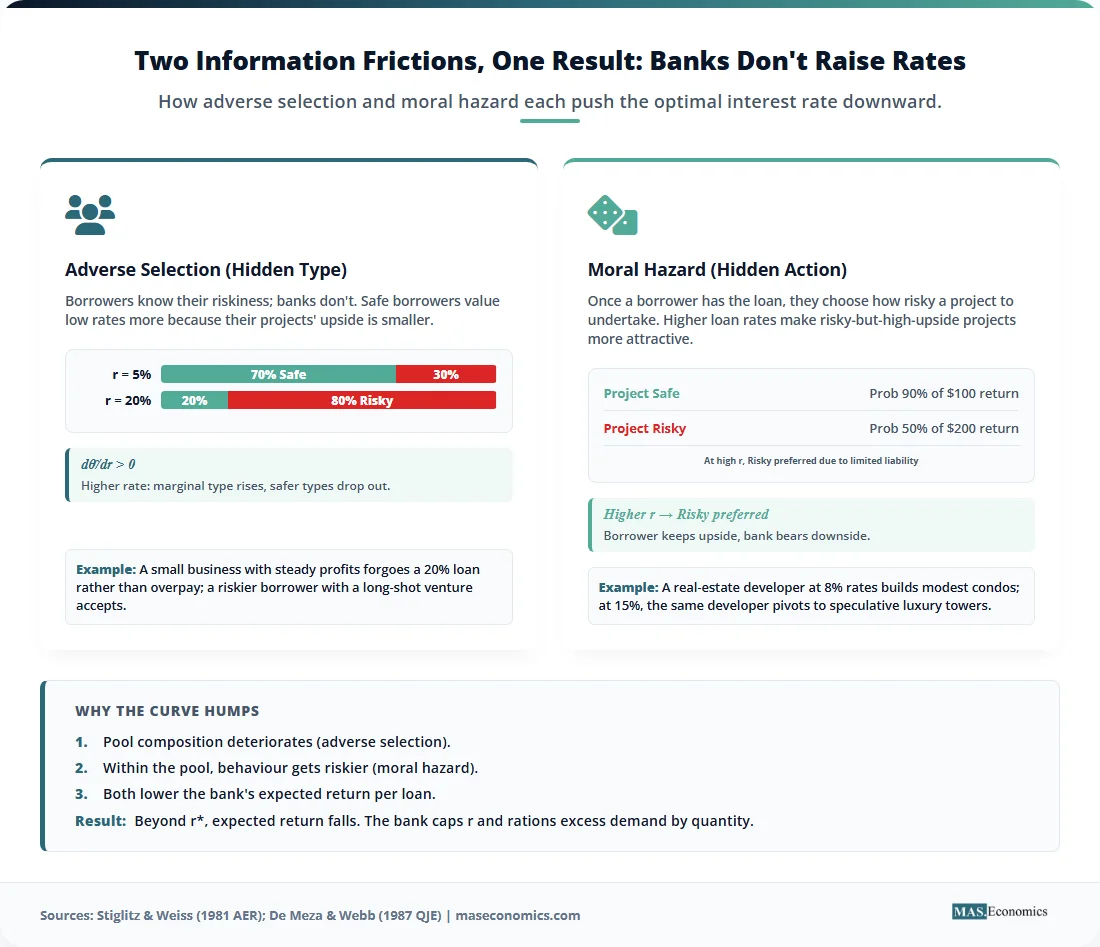

Stiglitz and Weiss provided the definitive answer: when banks cannot perfectly observe the riskiness of borrowers, raising the interest rate has two opposing effects. The direct effect is straightforward: higher rates raise the bank’s revenue per loan. However, the selection effect works in the opposite direction. As the interest rate rises, the pool of applicants changes. Safe borrowers, whose projects have a high probability of success but a modest upside, drop out first because the higher interest rate makes their expected profit negative. Riskier borrowers, whose projects have a low probability of success but a massive upside, are willing to pay higher rates because they capture the upside if the project succeeds but are protected by limited liability if it fails.

The result is a hump-shaped relationship between the interest rate and the bank’s expected return. At low rates, the direct effect dominates, and raising the rate increases expected profit. But beyond a certain point, the selection effect dominates. The pool becomes so contaminated with risky borrowers that the bank’s expected return begins to fall. There exists an interest rate \( r^* \) that maximises the bank’s expected profit. If loan demand exceeds supply at \( r^* \), the bank does not raise the rate further because doing so would lower its expected return. Instead, it rations credit by quantity. Some willing-to-pay borrowers are simply denied.

This mechanism connects directly to the broader information economics revolution. Just as the Akerlof Model showed how asymmetric information can cause markets to collapse, and the Spence Signalling Model showed how agents overcome hidden types through costly signals, the Stiglitz-Weiss model showed how hidden information breaks the price mechanism in credit markets. Prices alone cannot clear the market when the act of raising the price worsens the quality of the transacting pool.

Stiglitz‑Weiss Model in Equations

The Stiglitz-Weiss model formalises the intuition through a careful specification of borrower types, project returns, and the bank’s optimisation problem. The mathematics makes precise why the bank’s expected return is hump-shaped and why collateral cannot fully resolve the problem.

Setup: Borrower Types and Project Returns

Consider a pool of borrowers, each indexed by a riskiness parameter \( \theta \). Each borrower undertakes a project with a random return. Higher \( \theta \) denotes a riskier project. Specifically, projects are ranked by mean-preserving spreads: riskier projects have the same expected return as safer ones but higher variance. A project succeeds with probability \( p(\theta) \) and pays a gross return \( R(\theta) \), or fails with probability \( 1 – p(\theta) \) and pays 0. Crucially, \( p(\theta) \) declines with \( \theta \), meaning riskier projects succeed less often, but they pay off more when they do succeed.

Bank’s Expected Return per Loan

Under limited liability, borrowers cannot lose more than their equity. If the project fails, the bank gets nothing. If the project succeeds, the bank receives the contracted repayment \( 1 + r \), where \( r \) is the interest rate. The bank’s expected return from lending to a borrower of type \( \theta \) at interest rate \( r \) is:

Since the bank will never set \( r \) so high that \( 1+r \) exceeds the maximum possible project return (the borrower would simply not borrow), we typically have \( R(\theta) \geq 1+r \), simplifying the expression to \( \rho(r, \theta) = p(\theta) \cdot (1+r) \).

Borrower’s Expected Profit

The borrower’s expected profit from taking the loan at interest rate \( r \) is the expected return of the project minus the expected repayment to the bank:

A borrower will only take the loan if \( \pi(r, \theta) \geq 0 \). This participation condition is where the selection effect originates.

Critical Insight 1: Adverse Selection

Define \( \hat{\theta}(r) \) as the marginal borrower who is indifferent between borrowing and not borrowing at interest rate \( r \). As \( r \) rises, safe borrowers (low \( \theta \)) find their expected profit turning negative first. Their projects have lower upside \( R(\theta) \), so the fixed repayment \( 1+r \) eats into their profits quickly. Riskier borrowers (high \( \theta \)) have higher upside, so they remain in the market even at high rates. The pool composition shifts toward risky types:

Higher interest rates drive out the safest borrowers, leaving the bank with a worse pool. This is adverse selection in credit markets, directly analogous to the adverse selection Akerlof described in the used car market, but here it is driven by the interest rate itself rather than the price of the good.

Critical Insight 2: Moral Hazard

Conditional on borrowing, a higher interest rate makes risky projects more attractive relative to safe ones. Because of limited liability, the borrower bears the full upside of a risky success but shares the downside (project failure) with the bank. As \( r \) increases, safe projects become unprofitable for the borrower, but risky projects with their high upside remain viable. Borrowers endogenously shift to higher-variance projects. This is moral hazard, as the bank cannot observe or control the borrower’s project choice after the loan is made.

Bank’s Aggregate Expected Return

The bank’s expected return across the entire pool of borrowers at interest rate \( r \) is the integral over all borrower types who choose to borrow:

This function is hump-shaped in \( r \). At low interest rates, the direct effect dominates. Raising \( r \) increases revenue per loan, and the pool quality is still good. But as \( r \) rises past a critical point, the composition effect takes over. The loss in pool quality (adverse selection and moral hazard) outweighs the gain from higher revenue per loan, and expected return falls.

Sources: Stiglitz & Weiss (1981, AER 71:393-410); modern textbook treatments (Tirole 2006).

Optimal Bank Interest Rate and Equilibrium Rationing

The bank chooses the interest rate \( r^* \) that maximises its expected return:

If, at \( r^* \), the demand for loans exceeds the supply of funds the bank has available (or the supply at the prevailing deposit rate), the bank does not raise \( r \) to clear the market. Doing so would lower its expected profit. Instead, it rations credit. Some borrowers who are willing to pay \( r^* \) are denied loans. This is equilibrium credit rationing, a situation where supply does not equal demand, even in a competitive market with flexible prices.

Why Collateral Cannot Fully Resolve the Problem

One might think that requiring more collateral could solve the adverse selection problem by making risky borrowers self-select out. However, Wette (1983) and Stiglitz and Weiss themselves noted that increasing collateral requirements has the same perverse selection effect as raising the interest rate. Wealthy borrowers, who can post large collateral, are not necessarily safer. If safe borrowers are wealth-constrained (a common situation for young entrepreneurs and small businesses), raising collateral drives them out while wealthy risk-takers remain. Even collateral is rationed in equilibrium.

Key Assumptions and Limitations

The Stiglitz-Weiss model rests on several key assumptions. First, borrowers know their risk type, but banks cannot observe it (asymmetric information). Second, borrowers have limited liability; they cannot lose more than their equity. Third, projects are ranked by mean-preserving spreads, meaning riskier projects have higher variance but the same mean return. Fourth, banks compete and earn zero economic profits in equilibrium.

While elegant, the model has faced significant theoretical and empirical challenges. First, De Meza and Webb (1987) showed in the Quarterly Journal of Economics that under different distributional assumptions, specifically if riskier projects have higher mean returns rather than the same mean, asymmetric information leads to over-lending rather than rationing. Safe borrowers cross-subsidise risky ones, and the market features too much credit rather than too little.

Second, Riley (1987) demonstrated in the American Economic Review that with separating contracts (offering menus of collateral and interest rate combinations), rationing can vanish. Banks can screen borrowers by offering high-collateral, low-rate contracts to safe types and low-collateral, high-rate contracts to risky types, eliminating the need for quantity rationing.

Third, Su and Zhang (2017) provided a formal re-examination in the Journal of Money, Credit, and Banking, showing that the Stiglitz-Weiss result requires a specific stochastic-dominance ordering. Under first-order stochastic dominance, neither adverse selection nor moral hazard generates the hump-shaped return function that drives credit rationing. The result is theoretically fragile.

Fourth, modern banking uses extensive credit-scoring technologies, such as FICO scores, cash-flow analytics, and machine-learning models, that mitigate the information asymmetries the model assumes. While screening is imperfect, the opacity assumed in 1981 is less characteristic of today’s data-rich environment.

Fifth, the original model considers only debt contracts. In practice, equity financing, convertible debt, and hybrid securities can bypass the limited-liability distortions that drive the result. Finally, the model is static. In multi-period relationships, reputation effects and the prospect of future lending can substitute for screening, reducing the need for rationing.

Empirical Evidence for the Stiglitz‑Weiss Model

The empirical literature on credit rationing spans four decades and reflects the model’s theoretical ambiguities. Stiglitz and Weiss (1981) did not provide formal empirical tests in their original paper; their contribution was theoretical. However, the subsequent literature has sought to verify whether banks actually ration credit as the model predicts.

Stiglitz and Weiss (1992) extended their framework to macroeconomic implications, arguing that credit rationing amplifies business cycles and explains why monetary policy has real effects beyond the interest-rate channel. The NBER Working Paper 2164 by Stiglitz further formalised the macroeconomic equilibrium with credit rationing.

On the empirical front, Berger and Udell (1995) provided evidence from the US small business sector. Su and Zhang (2017) provided a formal re-examination in the Journal of Money, Credit, and Banking, showing that the empirical existence of credit rationing depends critically on the assumed stochastic-dominance ordering of project returns, confirming the theoretical fragility of the original result. Using data from the National Survey of Small Business Finances, Berger and Udell found that smaller, younger, and more opaque firms face higher denial rates, consistent with Stiglitz-Weiss screening. However, they also found that relationship lending, where banks acquire private information over time, significantly reduces rationing, supporting the theoretical critiques of Riley.

Petersen and Rajan (1994), in a landmark Journal of Finance paper, showed that close bank-borrower relationships increase the availability of credit, particularly for young firms. This finding supports the idea that information asymmetries drive rationing, but also shows that banks can overcome these asymmetries through repeated interaction.

Developing-country evidence is particularly strong. Banerjee and Duflo (2010) exploited a natural experiment in India, where a priority sector lending mandate forced banks to increase credit to small firms. They found that additional credit led to significant increases in output and profits, suggesting these firms were previously credit-rationed. Karlan and Zinman (2009) conducted a randomised experiment in South Africa, offering consumer credit at randomly assigned interest rates. They found that demand was elastic at high rates, but default rates also rose with the interest rate, consistent with the moral hazard channel in Stiglitz-Weiss.

Jiménez et al. (2014) used the Spanish credit registry to show that bank capital affects screening intensity. Better-capitalised banks extended more credit at lower rates, while undercapitalised banks rationed credit tightly. This supports the Diamond-Dybvig and Stiglitz-Weiss view that bank balance-sheet health affects credit availability independently of interest rates.

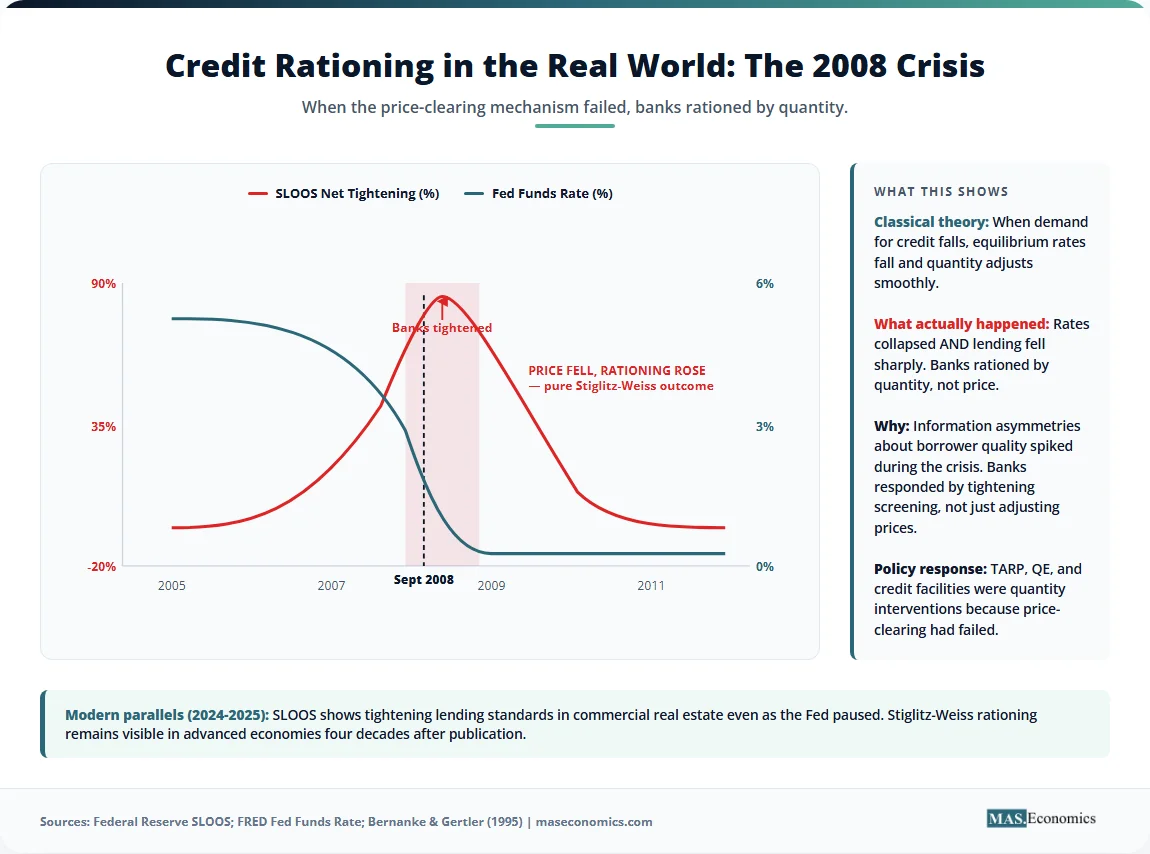

At the macroeconomic level, the Federal Reserve’s Senior Loan Officer Opinion Survey (SLOOS) and the ECB Bank Lending Survey provide systematic evidence that banks adjust lending standards, rationing by quantity in response to economic conditions, often independently of interest-rate movements. During the 2008 financial crisis, for example, net tightening of C&I lending standards reached historic peaks even as the Fed slashed rates to zero, a pattern the 2008 financial crisis made globally visible.

| Setting | Evidence | Magnitude | Source |

|---|---|---|---|

| US Senior Loan Officer Survey (2008) | Banks tightened standards while cutting rates | 80% net tightening at peak | Federal Reserve SLOOS |

| Indian small farms | Priority sector lending raises credit access | +15% access to formal credit | Banerjee & Duflo (2010, AEJ) |

| US small business (firms < 20 employees) | Loan denial rates 2× larger firms even at same rates | Denial gap ≈ 25 pp | NSSBF survey |

| South African consumer credit | Randomised loan offers | Take-up = 14% at market rate | Karlan & Zinman (2009 Eca) |

| Spanish credit registry 2008–2010 | Stronger banks lent more at lower rates | Capital ratio elasticity = 0.7 | Jiménez et al. (2014 AER) |

| Microfinance group lending | Group screening reduces default | Default rates 30% → 5% | Yunus / Grameen data |

|

|||

How the Stiglitz‑Weiss Model Matters

The Stiglitz-Weiss credit rationing model is not merely a theoretical curiosity; it underpins modern banking economics, macroeconomic policy, and development finance. Its implications are vast and deeply embedded in how governments and central banks manage the economy.

First, Stiglitz-Weiss is the foundational model behind every undergraduate and graduate textbook treatment of why credit markets are not standard markets. Every Federal Reserve, ECB, and Bank of England staff paper on credit allocation cites it. Before 1981, the dominant framework assumed credit markets cleared like commodity markets. After 1981, it was impossible to ignore that the price mechanism itself could fail in financial markets.

Second, credit rationing amplifies macroeconomic credit cycles. When loan officers tighten standards during a downturn, the equilibrium adjusts via quantity rationing rather than higher rates. Money multiplier and credit creation dynamics are disrupted not because the central bank raises rates, but because banks stop lending. The Federal Reserve’s SLOOS and the ECB’s Bank Lending Survey directly measure these quantity adjustments. In recessions, the decline in lending is often far larger than the decline in borrower demand, indicating supply-side rationing exactly as Stiglitz-Weiss predicted.

Third, the 2008 financial crisis was a live demonstration of Stiglitz-Weiss dynamics. Stiglitz himself argued that the credit rationing framework explained why the post-Lehman credit freeze did not resolve through higher rates. Information asymmetries spiked; banks could not distinguish solvent borrowers from insolvent ones. The price mechanism failed. The Fed and Treasury responded with quantity policies, such as TARP capital injections, quantitative easing, and emergency credit facilities, precisely because price-clearing mechanisms had broken down. Central banks as lenders of last resort became the essential backstop.

Fourth, the microfinance revolution was explicitly designed to overcome the Stiglitz-Weiss screening problem. Muhammad Yunus’s Grameen Bank and similar institutions like BRAC pioneered group lending, where borrowers collectively guarantee each other’s loans. This leverages local social information to screen out risky borrowers. Villagers know who is reliable, even if the bank does not. Yunus’s 2006 Nobel Peace Prize celebrated an innovation that was, at its core, a response to Stiglitz-Weiss adverse selection.

Fifth, small business lending in the US, UK, and EU operates under a permanent Stiglitz-Weiss shadow. Small firms are opaque; they lack audited financials, long credit histories, and easily collateralisable assets. The US Small Business Administration (SBA), the British Business Bank, and the European Investment Fund operate guarantee programmes precisely because Stiglitz-Weiss rationing falls hardest on these borrowers. By absorbing part of the default risk, government guarantees push the bank’s expected return curve upward, increasing the optimal interest rate and the volume of lending.

Sixth, the 2010s fintech revolution in credit scoring represents a large-scale, Stiglitz-Weiss-motivated entry. Companies like Affirm, Klarna, Upstart, and Ant Financial use alternative data (cash flows, social media, educational background) to reduce the information asymmetry that drives rationing. Risk and uncertainty are more cheaply observed than ever before. Better screening shifts the hump-shaped return curve upward, allowing banks to lend more at the same interest rate.

Seventh, developing-country credit markets are still defined by Stiglitz-Weiss logic. The World Bank’s Doing Business indicators on credit access, the IFC’s SME Finance programmes, and country-level financial-development assessments all use Stiglitz-Weiss as the conceptual frame. In sub-Saharan Africa and South Asia, the majority of smallholder farmers and micro-enterprises remain outside the formal credit system, not because they lack profitable projects, but because banks cannot screen them profitably.

Eighth, the “credit channel” of monetary policy transmission, formalised by Bernanke and Gertler (1995), extends Stiglitz-Weiss to macroeconomics. When monetary transmission mechanisms operate, central bank actions affect not just the price of credit but the volume of lending. A rate cut improves bank balance sheets, reduces screening intensity, and expands credit availability. This is an effect entirely separate from the standard interest-rate channel. The functions of central banks thus extend far beyond setting rates to managing credit quantities.

Ninth, climate-finance frictions are a contemporary frontier for Stiglitz-Weiss. Green start-ups face credit rationing because climate risk is not yet well-priced or well-understood by banks. A solar developer with a 20-year revenue stream may be safer than a fossil-fuel incumbent, but if the bank’s models do not capture this, the developer is screened out. Both EU taxonomies and US SEC climate-disclosure rules aim partly to reduce this asymmetry, enabling credit to flow toward green investments.

Tenth, the Indian and Pakistani agricultural credit policy is a direct application. Both countries operate priority sector lending mandates that require banks to lend a certain percentage of their portfolios to agriculture and small business. These mandates implicitly recognise that Stiglitz-Weiss rationing leaves smallholder farmers without access to formal credit, despite their willingness to pay market rates. The policy response is not to let rates rise, but to force quantity adjustments through regulation.

MASEconomics Explains

4 economic concepts behind the Stiglitz-Weiss model

Conclusion

The Stiglitz-Weiss credit rationing model showed that information asymmetries make credit markets fundamentally unlike commodity markets. Banks rationally cap interest rates and ration loans by quantity rather than letting prices clear because higher rates attract worse borrowers and induce riskier behaviour. This single insight underpins modern banking economics, macroeconomic credit-cycle analysis, microfinance design, and small-business lending policy. While later work by De Meza and Webb, Riley, and Su and Zhang has refined and challenged the strict theoretical result, showing that it depends on specific distributional assumptions and can be circumvented by separating contracts, the core insight remains foundational. Asymmetric information generates non-price rationing, and in credit markets, the price mechanism alone cannot guarantee efficiency. Whether in the 2008 financial crisis, a Bangladeshi village, or a climate-tech start-up seeking capital, the Stiglitz-Weiss logic still shapes who gets credit and who does not.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.