Why do used cars sell for so much less than nearly identical new cars? Why do the elderly struggle to find affordable health insurance? Why do small businesses in developing countries often face exorbitant interest rates from moneylenders? And why, despite the apparent gains from trade, do some markets seem to shrink or even disappear?

At the heart of these dilemmas is a simple but profound idea: sometimes the seller knows more about the product than the buyer. When this happens, when information is asymmetric, the market can malfunction in ways that standard economic theory never anticipated. Good products may be driven out by bad ones, mutually beneficial trades may never occur, and the invisible hand may freeze, leaving buyers and sellers worse off.

This was the startling insight of George A. Akerlof, a young economist who, in 1970, published a paper titled “The Market for ‘Lemons’: Quality Uncertainty and the Market Mechanism.” The paper was initially rejected by several journals for being “trivial.” Yet it went on to become one of the most cited and influential works in economics, earning Akerlof a Nobel Prize in 2001. It launched the field of information economics and reshaped how economists think about markets, institutions, and the role of trust.

What Did Economists Believe?

Before Akerlof’s paper, mainstream economics rested on a powerful assumption: that markets, left to themselves, would allocate resources efficiently. The first welfare theorem taught that competitive equilibrium is Pareto optimal. The logic was simple: buyers and sellers, armed with full information about prices and qualities, would strike mutually beneficial deals until no further gains were possible.

Of course, economists knew that information was not always perfect. But they treated it as a secondary issue. George Stigler had written about the costs of search; Kenneth Arrow had explored the economics of uncertainty. Yet the conventional wisdom held that even with imperfect information, markets would still clear. Prices would adjust to balance supply and demand, and the usual tools of supply and demand analysis would suffice.

Akerlof challenged this orthodoxy. He showed that when quality is uncertain, and sellers know more than buyers, the price mechanism can break down entirely. The market may not just fail to be efficient; it may fail to exist. This was a radical departure from the standard paradigm, and it opened the door to a new way of thinking about market institutions, signaling, and the role of government.

The Man Behind the Idea

George Akerlof was born in 1940 in New Haven, Connecticut. He studied at Yale and then at MIT, where he earned his PhD in 1966. After a stint at the University of California, Berkeley, he spent the 1969–1970 academic year at the Indian Statistical Institute in New Delhi. It was there that he wrote his now‑famous paper.

The idea came from his observations of the Indian economy. He noticed the enormous variation in the quality of goods sold in local bazaars, rice mixed with stones, hand‑loomed textiles of uncertain durability, and the difficulty that buyers faced in distinguishing good from bad. He also saw how credit markets in rural India were dominated by moneylenders who charged exorbitant rates, not because they were monopolists, but because they were the only ones who knew their borrowers personally.

Akerlof began to think about the economics of quality uncertainty. He realized that the problem was not confined to India; it was everywhere. Used cars, insurance, and labor markets all suffered from similar asymmetries. The key insight was that when buyers cannot observe quality, they must form an expectation based on the average quality in the market. That average, in turn, depends on which sellers choose to participate. As the price falls, the average quality falls, and the market can unravel.

The paper was rejected by the American Economic Review and the Review of Economic Studies before being accepted by the Quarterly Journal of Economics in 1970. It was initially met with skepticism, but within a decade, it had spawned a vast literature on adverse selection, signaling, and screening. In 2001, Akerlof shared the Nobel Prize with Michael Spence and Joseph Stiglitz for their work on markets with asymmetric information.

The Core Idea Explained: Lemons, Adverse Selection, and Market Unraveling

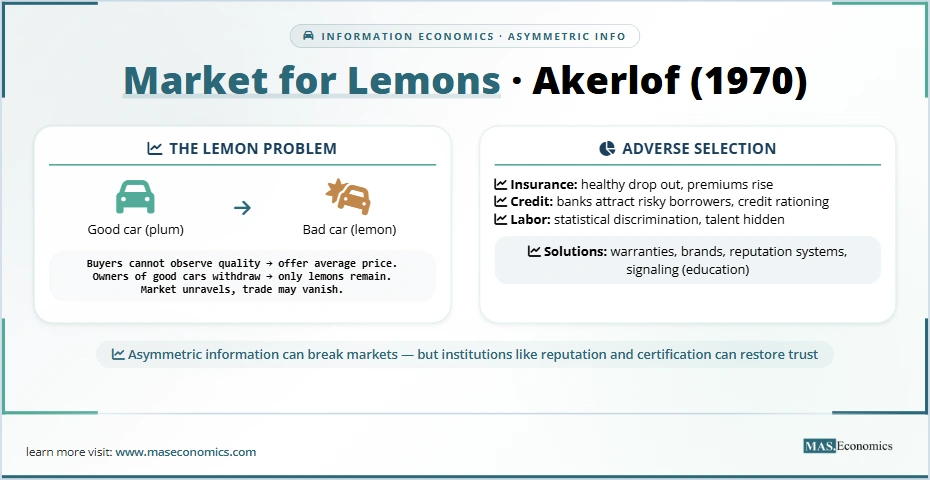

To understand Akerlof’s model, we need to start with a concrete example. Consider the market for used cars. In the United States, a “lemon” is a defective car. But in Akerlof’s model, lemons are not just defective; they are the low‑quality end of a continuum.

Suppose there are two types of used cars: good cars (“plums”) and bad cars (“lemons”). Sellers know which type they have; buyers do not. Buyers only know that a fraction \(q\) of the cars are good and \(1-q\) are lemons. How much will a buyer be willing to pay? They will base their offer on the expected quality. If the value of a good car is \(V_g\) and a lemon is \(V_b\) (with \(V_g > V_b\)), the buyer’s maximum price is \(q V_g + (1-q) V_b\).

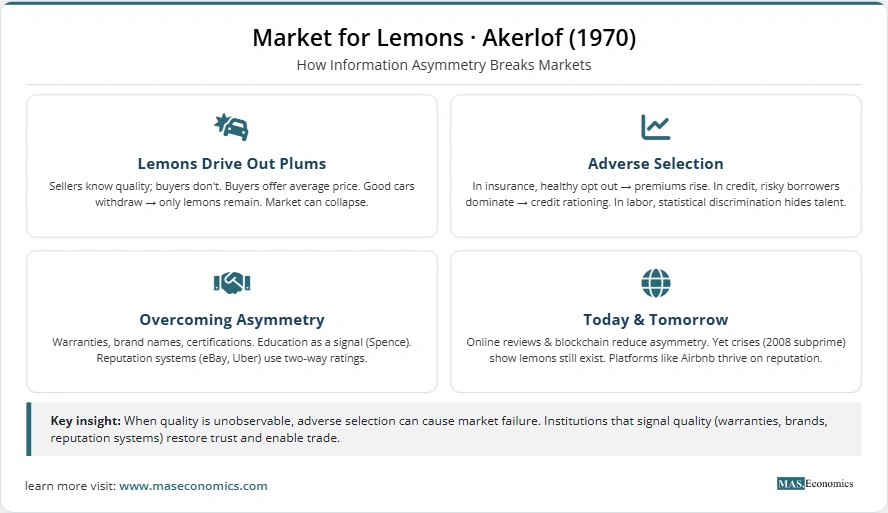

Now consider the sellers. Owners of good cars know their car is worth \(V_g\) to them. If the market price is below \(V_g\), they will not sell. Owners of lemons, however, are happy to sell if the price is above \(V_b\). So as the market price falls, the proportion of good cars offered for sale declines, and the average quality of cars on the market drops. This is adverse selection: the pool of sellers becomes increasingly composed of low‑quality goods.

The crucial point is that there may be no price at which both types of sellers are willing to sell and buyers are willing to buy. In Akerlof’s stylized example, with linear utility and uniform quality distribution, he shows that no trade occurs at any price, even though there are potential buyers who value even the lowest quality cars more than the sellers value them. The market simply vanishes.

This is the lemon problem: asymmetric information can cause market failure, not because of monopoly or externalities, but because the very process of price adjustment destroys the conditions necessary for trade.

Akerlof called this a “generalized Gresham’s law”: bad goods drive out good goods, but unlike Gresham’s law of money, the mechanism is not a fixed exchange rate but the informational opacity that prevents buyers from distinguishing quality.

A MASEconomics Example

Consider a typical scenario in a Pakistani city. A used car market, say in Karachi, has both well‑maintained cars and those that have been poorly treated. Sellers know the history; buyers do not. If buyers assume the worst, they will only offer a low price. Sellers of good cars then withdraw, leaving only lemons on the market. The market may persist, but only at a price that reflects the lowest quality, and many potential transactions that would have benefited both parties never occur.

This is not just a theoretical curiosity. In many developing countries, the used car market suffers from severe information problems, leading to thin trading and high markups for intermediaries who can certify quality. The same logic applies to many other goods, from electronics to property, where quality is hard to observe at the point of sale.

Where Else Do Lemons Lurk?

Akerlof’s insight was not limited to used cars. He applied it to three other major markets: insurance, labor, and credit. Each illustrates a different facet of the adverse selection problem.

Insurance

Consider health insurance for the elderly. As people age, their health risks increase. Insurance companies would like to charge premiums that reflect individual risk, but they cannot perfectly observe the health status of each applicant. The elderly themselves know their health better. As premiums rise, only the least healthy, those most likely to need insurance, will apply. This adverse selection forces insurers to raise premiums further, eventually driving the healthy out of the market entirely. In Akerlof’s words, “no insurance sales may take place at any price.” This is why, before Medicare, many elderly Americans could not obtain affordable private health insurance.

Labor Markets

Now consider employment. Employers often have imperfect information about a job applicant’s productivity. They may rely on observable characteristics such as education, race, or previous employment history as proxies. But if a group, say, a minority community, has been historically disadvantaged, its average productivity may be lower, or perceived to be lower. Employers, using group averages as a statistic, may be reluctant to hire individuals from that group for skilled positions, even if some individuals are highly qualified. This is a form of statistical discrimination, and it can lead to a self‑fulfilling prophecy: because individuals cannot credibly signal their quality, they are denied opportunities, and the group’s average remains low.

Akerlof cited George Stigler’s poignant remark: “In a regime of ignorance, Enrico Fermi would have been a gardener, Von Neumann a checkout clerk at a drugstore.” The lemons principle shows how markets can fail to recognize talent, leading to inefficient allocation of human resources.

Credit Markets in Developing Countries

The third application is credit. In rural areas, a moneylender may have intimate knowledge of the character and reliability of local borrowers. A formal bank, lacking such knowledge, would attract only the riskiest borrowers if it tried to lend at competitive rates. Thus, credit is often rationed, and the only loans available come from informal lenders who charge high interest rates, not because of monopoly power, but because they are the only ones who can overcome the adverse selection problem. Akerlof’s model thus provides a theoretical foundation for the persistent credit market segmentation observed in many developing countries.

The Challenge

Akerlof did not conclude that markets always fail. He recognized that private institutions can arise to counteract the effects of quality uncertainty. Guarantees, brand names, chains, and licensing are all examples. A used car dealer who offers a warranty signals confidence in his cars and shifts the risk from buyer to seller. A brand name like Mercedes‑Benz tells buyers that the company has a reputation to protect and will not sell lemons.

But these institutions are not costless, and they may not work perfectly. Moreover, the very existence of such institutions is a response to the informational problem, not a refutation of its importance. The Lemons model shows why we have these institutions, and why markets without them may fail.

Over the years, economists have extended and refined Akerlof’s insights. Michael Spence (1973) showed how education can serve as a signal of ability, even if it adds no real productivity. Joseph Stiglitz and Andrew Weiss (1981) applied adverse selection to credit markets, showing how banks may ration credit rather than raise interest rates, because higher rates attract riskier borrowers. This is a direct application of the lemons logic to the loan market.

The Grossman‑Stiglitz paradox (1980) further challenged the notion of perfect markets: if markets were perfectly efficient, no one would have an incentive to acquire costly information, yet without information, markets cannot be efficient. The lemon problem is thus not a mere curiosity but a fundamental feature of economies with costly information.

How the Internet and the Sharing Economy Solve the Lemon Problem

Fast forward to the 21st century. Information asymmetries are still with us, but technology has dramatically changed the landscape. The internet, online reviews, and reputation systems have given consumers tools that were unimaginable in 1970.

Reputational Feedback Mechanisms

Consider Airbnb, Uber, or eBay. Each transaction is accompanied by a rating. After a stay, a host and guest rate each other. After a ride, the driver and passenger rate each other. These ratings accumulate into a reputation score that is visible to all future trading partners. A seller with a high rating is unlikely to be a lemon; a buyer with a poor rating may be avoided.

Economists have begun to study how these platforms solve the lemon problem. In a 2016 paper, Adam Thierer and colleagues argued that “the sharing economy, through the use of the Internet and real-time reputational feedback mechanisms, is providing a solution to the lemons problem that many regulators have spent decades attempting to overcome.” The key is that these systems make information about past behavior easily accessible, aligning incentives for honest dealing and allowing high‑quality sellers to signal their quality without relying on costly third‑party certifications.

Two‑Sided Ratings

Akerlof’s original model assumed one‑sided information asymmetry: sellers know more than buyers. In many online platforms, the asymmetry is reduced because both sides can evaluate each other. A driver can refuse a passenger with a low rating; a host can decline a guest who has previously caused damage. This two‑way feedback creates a self‑enforcing mechanism: to remain in the market, both parties must maintain a good reputation.

Blockchain and Cryptocurrencies

Even newer technologies are being deployed. Non‑fungible tokens (NFTs) and blockchain‑based provenance systems aim to provide verifiable records of authenticity and ownership history. While these technologies are still evolving, they offer the promise of reducing information asymmetry in markets for art, collectibles, and digital goods. As Kagan Okatan noted in a 2023 review, “cryptocurrencies stand out especially with their ability to handle more efficient online transactions, lower costs, and simplified payment processes.” The underlying blockchain technology can serve as an immutable ledger of quality‑related information, potentially mitigating lemon problems in new markets.

The Persistence of Asymmetry

Yet the lemon problem has not disappeared. In markets for complex goods like financial services or in areas where online reputation systems are not fully developed, adverse selection remains a serious issue. The 2008 financial crisis was, in part, a lemon problem: mortgage‑backed securities were sold with opaque quality, and buyers could not distinguish good from bad until it was too late. And in many developing countries, the informal institutions that once solved the lemon problem, like the moneylender’s personal knowledge, are being disrupted without being replaced by effective modern alternatives.

Why Does the Akerlof Model Still Matter?

When Akerlof wrote his paper, he was challenging the idea that markets always work. He showed that asymmetric information can cause markets to unravel, and that the institutions we take for granted, warranties, brand names, licensing, are not just decorations but essential solutions to deep informational problems.

Today, the Akerlof model is as relevant as ever. It underpins our understanding of financial crises, labor market discrimination, credit rationing, and the rise of the sharing economy. It reminds us that information is not free, and that when it is costly, markets may need help, either from private institutions or, in some cases, from government, to function properly.

For the ordinary investor or consumer, the lesson is twofold. First, be wary of deals that seem too good to be true; if you cannot verify quality, you may be buying a lemon. Second, trust the mechanisms that have evolved to solve these problems: reputation systems, independent certification, and brands with a stake in their reputation.

The market for lemons is not a niche topic. It is a window into how markets really work, messy, imperfect, but constantly adapting. And as technology continues to evolve, new solutions will emerge, perhaps reducing the cost of information to the point where the lemon problem becomes a relic of the past. Until then, Akerlof’s insight remains a powerful lens.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.