In early 2026, the slow-moving crisis of climate change accelerated into a full-blown economic emergency for homeowners across the United States. State Farm and Allstate, two of the nation’s largest insurers, stopped writing new homeowners policies in California, citing unsustainable wildfire risk and soaring construction costs. They were not alone. Farmers Insurance withdrew from Florida entirely, dropping 100,000 policyholders, while Allstate also pulled back from parts of Louisiana and North Carolina. This was not a regulatory dispute or a temporary market correction. It was a market verdict: climate risk had become uninsurable.

The fallout was immediate. In California, enrollment in the FAIR Plan, the state-run insurer of last resort, surged 43% between September 2024 and December 2025. By early 2026, the FAIR Plan was covering nearly 10% of residential policies in the state, with a striking 14% of those policies now insuring properties in areas classified as having low fire risk, a clear sign that the crisis is spreading beyond the obvious danger zones. The system was stretched dangerously thin, with the FAIR Plan reporting an estimated $4 billion in losses from recent fires.

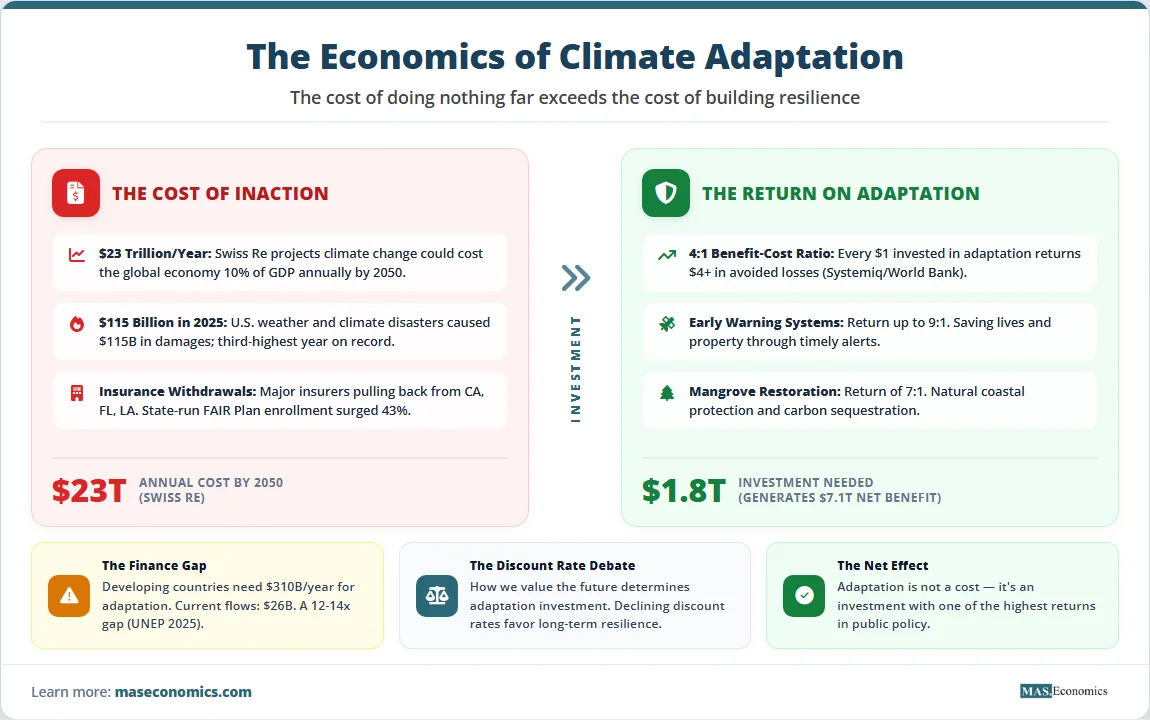

This is not a California problem. It is an economic problem with a global price tag. The reinsurance giant Swiss Re calculates that unchecked climate change could cost the global economy up to $23 trillion annually by 2050, equivalent to a permanent loss of roughly 10% to 14% of global GDP. The United States alone experienced 23 billion-dollar weather and climate disasters in 2025, causing $115 billion in total damage and 276 fatalities. This was the third-highest year on record, following 2023 (28 disasters) and 2024 (27 disasters). The average time between billion-dollar disasters in the U.S. has collapsed from 82 days in the 1980s to just 16 days over the last decade. In 2025, a billion-dollar disaster struck once every 10 days.

Yet for every dollar spent on climate adaptation today, the return is more than four dollars in avoided losses. The question facing policymakers is no longer whether climate change is happening or whether humans are responsible. The question is a cold, hard economic one: given limited resources and competing priorities, what is the optimal response to climate risk? How much should we spend on adaptation now to avoid much higher costs later?

From Warnings to Withdrawals

For decades, the economic case for climate action was framed primarily around mitigation, reducing greenhouse gas emissions to prevent future warming. This was, and remains, essential. But a quieter, equally urgent economic story has been unfolding in parallel: the rising cost of living with the climate change that is already locked in. Even if the world achieved net-zero emissions tomorrow, the carbon dioxide already in the atmosphere would continue to warm the planet for decades. Sea levels will keep rising. Wildfires will keep burning. Floods will keep inundating. Adaptation, building resilience to these unavoidable impacts, has moved from a secondary concern to a core economic imperative.

The timeline below traces how climate adaptation has evolved from a niche scientific concern to a central challenge for insurers, governments, and the global economy.

Timeline: The Evolution of Climate Adaptation Economics

| Year | Event | Economic Significance |

|---|---|---|

| 2006 | Stern Review published | First major economic analysis concluding that the benefits of strong, early climate action far outweigh the costs. |

| 2015 | Paris Agreement adopted | Established global goal for adaptation and committed developed countries to mobilize $100 billion annually in climate finance. |

| 2017 | Hurricanes Harvey, Irma, Maria | Combined damages of $265 billion; highlighted vulnerability of even advanced economies to extreme weather. |

| 2021 | Swiss Re $23 trillion warning | Reinsurance giant calculates climate change could reduce global economic output by 11-14%, or up to $23 trillion annually, by 2050. |

| 2022 | Inflation Reduction Act (US) | Largest climate investment in U.S. history; includes over $50 billion for climate resilience and adaptation. |

| 2023 | State Farm halts new CA policies | Major insurer withdrawal signals that climate risk is now uninsurable in some regions without major adaptation. |

| 2024 | Global adaptation finance flows fall | International public adaptation finance drops to $26 billion, widening the adaptation finance gap. |

| 2025 | UNEP Adaptation Gap Report 2025 | Finds adaptation finance needs in developing countries at $310-365 billion annually 12-14 times current flows. |

| 2025 | U.S. disasters cost $115 billion | Third-highest year on record for billion-dollar disasters; 23 events, 276 fatalities. |

| 2026 | California FAIR enrollment surges 43% | State-run insurer of last resort now covers nearly 10% of residential policies; 14% of policies in low-risk zones. |

|

||

The insurance withdrawals are particularly significant because they represent a market signal that cannot be ignored. When private insurers, whose entire business model depends on accurately pricing risk, conclude that they cannot profitably offer coverage in a region, they are effectively declaring that the risk has become unquantifiable or unaffordable. This is not speculation; it is a market verdict. The consequences ripple outward: mortgages become harder to obtain, property values decline, and local governments face pressure to invest in resilience measures or risk losing their tax base. The insurance crisis is, in effect, a leading indicator of the broader economic costs of climate inaction.

Why Adaptation Is an Investment, Not a Cost

Climate adaptation is not just an environmental or engineering challenge. It is fundamentally an economic problem that can be understood through core principles of cost-benefit analysis, discount rates, externalities, and public goods.

Cost-Benefit Analysis

Cost-benefit analysis (CBA) is the most straightforward tool for evaluating adaptation investments. The principle is simple: list all the costs of a project, list all the benefits (appropriately discounted over time), and compare them. If the benefits exceed the costs, the project creates net economic value.

The evidence from global CBA studies is remarkably consistent. The Returns on Resilience report, coordinated by Systemiq and presented at the 2025 World Bank Annual Meetings, found that every dollar invested in climate adaptation today yields more than four dollars in benefits, with an average annual return rate of 25%. In Germany, a World Bank analysis calculated average benefit-cost ratios of 6 for wildfire, flood, and heat adaptation measures, meaning each euro invested returns six euros in avoided losses. In Somalia, the World Bank found that cost-effective investments in climate resilience could cut long-term economic losses from climate change by half while generating more stable, productive jobs.

These numbers are not theoretical. They reflect the avoided costs of disasters that we can already observe. The $115 billion in U.S. disaster damages in 2025 represents actual economic output destroyed, homes burned, businesses flooded, crops lost, and infrastructure damaged. Adaptation investments reduce these losses. A $10 million investment in a flood barrier that prevents $50 million in flood damage has a benefit-cost ratio of 5. The economic case for adaptation is, in many cases, overwhelming.

The Discount Rate

The discount rate is perhaps the most consequential and controversial parameter in climate economics. It determines how much weight we give to future benefits and costs relative to present ones. A high discount rate says, in effect, “a dollar today is worth much more than a dollar in 30 years.” A low discount rate says, “the future matters almost as much as the present.” This choice has enormous implications for adaptation investments, many of which require high upfront costs but deliver benefits over decades or centuries.

The Stern Review on the Economics of Climate Change, published in 2006, famously used a low discount rate of approximately 1.4%, which led to the conclusion that strong, immediate climate action was economically justified. Critics, including prominent economists like William Nordhaus, argued that this rate was too low and that a rate closer to market returns, around 4-5%, was more appropriate. At a 5% discount rate, $1,000 in benefits 50 years from now is worth only about $87 today. At a 1.4% discount rate, it is worth about $500. The difference is not academic; it determines whether a seawall with a 100-year lifespan is considered a good investment or a waste of money.

There is an emerging consensus that for long-horizon climate decisions, declining discount rates are appropriate, meaning we should use lower rates for benefits that accrue further in the future. This approach reflects both ethical considerations (we should not discount the welfare of future generations as heavily as we discount our own consumption) and uncertainty about future economic growth.

Negative Externalities

Climate change is the ultimate example of a negative externality, a cost imposed on third parties who are not involved in the transaction that generates it. When a factory burns coal to produce electricity, the cost of the coal, labor, and capital equipment is paid by the factory owner and passed on to electricity consumers. But the climate damage caused by the carbon dioxide emitted by the wildfires, floods, crop failures, and health impacts is paid by society at large, including people in other countries and future generations who had no say in the transaction. This is a classic market failure: the price of coal-fired electricity does not reflect its true social cost.

The economic solution to negative externalities is to make the polluter pay to “internalize the externality” through mechanisms like carbon taxes or cap-and-trade systems. A carbon price forces emitters to bear at least some of the climate damage their activities cause, which in turn incentivizes them to reduce emissions. But even with an optimal carbon price, some level of climate change is already locked in due to past emissions. This is where adaptation comes in. Adaptation is, in economic terms, a response to the residual externality, the climate damage that mitigation cannot prevent. Because the market does not naturally provide the optimal level of adaptation, there is a strong economic case for government intervention.

Tragedy of the Commons

The tragedy of the commons describes a situation where a shared resource is depleted or degraded because each individual user has an incentive to exploit it, even though everyone would be better off if the resource were managed sustainably. Climate adaptation often involves a similar dynamic. Consider a coastal community where each homeowner could build a seawall to protect their property. If one homeowner builds a seawall, it may deflect waves onto neighboring properties, increasing their erosion. If everyone builds seawalls, the costs are high, and the collective benefit may be lower than a coordinated solution like a community-wide managed retreat or a single engineered barrier.

At a larger scale, adaptation suffers from a coordination failure between nations. Developing countries, which have contributed the least to historical emissions, face some of the most severe climate impacts. Yet they lack the financial resources to adapt. The UNEP Adaptation Gap Report 2025 estimates that developing countries need $310 billion annually for adaptation by 2035, but current international public adaptation finance flows are only $26 billion, a gap of 12 to 14 times. This is a classic public goods problem: the benefits of adaptation in developing countries accrue globally, but the costs are concentrated. Without coordinated international action, adaptation will be underprovided.

The Rising Cost of Inaction

The chart below shows the total annual cost of billion-dollar weather and climate disasters in the United States from 2015 to 2025, adjusted for inflation. The trend is unmistakable: costs are rising, and the frequency of extreme events is increasing. The 2023-2025 period represents the three highest years on record, with combined damages exceeding $350 billion.

Annual Cost of Billion-Dollar Weather and Climate Disasters in the United States (2015-2025, Inflation-Adjusted)

Sources: Data compiled from Climate Central, which now manages the database previously maintained by NOAA’s Billion-Dollar Weather and Climate Disasters program. Values are inflation-adjusted to 2025 USD.

The second chart compares the benefit-cost ratios of different climate adaptation investments, based on a synthesis of World Bank, Global Commission on Adaptation, and academic studies. The message is clear: many adaptation measures pay for themselves several times over.

Benefit-Cost Ratios of Selected Climate Adaptation Investments

Sources: Systemiq’s Returns on Resilience report (2025); World Bank Country Climate and Development Reports; Global Commission on Adaptation (2019); PNAS study on mangrove restoration (2026). Values represent median estimates from available studies.

The following table summarizes the global adaptation finance gap, highlighting the stark mismatch between what is needed and what is currently being provided.

Global Climate Adaptation Finance Gap (2025 Estimates)

| Metric | Value |

|---|---|

| Annual adaptation finance needed (developing countries, 2035) | $310 – $365 billion |

| Current international public adaptation finance flows (2023) | $26 billion |

| Adaptation finance gap | $284 – $339 billion (12-14x current flows) |

| Estimated global investment needed for resilience (2020-2030) | $1.8 trillion (generating $7.1 trillion in net benefits) |

| Global adaptation market opportunity (by 2030) | $1.3 trillion annually |

| Sources: UNEP Adaptation Gap Report 2025; Global Commission on Adaptation (2019); Systemiq Returns on Resilience (2025) | |

|

|

|

Who Benefits and Who Is Affected by Climate Adaptation

Climate adaptation is not a tide that lifts all boats equally. It creates clear opportunities for some while imposing disproportionate burdens on others. Understanding this uneven distribution is critical for designing equitable and effective policies.

Where the Benefits Accrue

Communities that invest early in resilience will reap substantial economic returns. Cities like Rotterdam, which have spent decades building a comprehensive flood protection system including the Maeslantkering storm surge barrier, have transformed climate risk into a competitive advantage. The Netherlands now exports its water management expertise globally. Similarly, Miami Beach is investing over $500 million in pumps and raised roads to combat sea-level rise, protecting billions in real estate value. The Systemiq report found that targeted adaptation investments could create over 280 million new jobs in emerging economies by 2035, while boosting GDP and unlocking a trillion-dollar market opportunity.

The insurance and reinsurance industry stands to benefit from adaptation investments that reduce insured losses. Swiss Re estimates that the global energy transition and climate adaptation could represent an $80 trillion investment opportunity by 2040. Insurers that develop innovative products such as parametric insurance that pays out automatically when certain climate thresholds are crossed, and those that accurately price climate risk will gain market share. The industry’s shift from simply covering losses to actively promoting resilience could open new revenue streams.

Developing countries that receive adaptation finance could see transformative benefits. The World Bank’s analysis in Somalia found that targeted resilience investments could cut climate-related economic losses by half while creating more stable jobs. In Bangladesh, investments in cyclone shelters, early warning systems, and coastal embankments have dramatically reduced mortality from cyclones, from hundreds of thousands in the 1970 Bhola cyclone to dozens or hundreds in recent storms, despite a much larger population.

Where the Burdens Fall

Homeowners in high-risk areas without adaptation investment face a bleak future. In California, over 1.2 million homes are at extreme wildfire risk, and insurance is becoming unavailable or unaffordable. In Florida and Louisiana, hurricane risk is driving similar dynamics. Without major adaptation investments or government-subsidized insurance, property values in these areas could decline sharply, trapping homeowners in a cycle of falling equity and rising costs. The FAIR Plan’s 43% enrollment surge is a direct reflection of this pressure.

Developing countries with limited fiscal space are the most vulnerable. They contributed the least to climate change but face the most severe impacts and have the fewest resources to adapt. The UNEP report highlights that international adaptation finance is not only insufficient but is often provided as loans, increasing the debt burden of already vulnerable nations. Without a major scale-up in grant-based adaptation finance, the climate divide between rich and poor countries will widen.

Taxpayers in countries that delay adaptation will ultimately bear the cost. When private insurers withdraw, the burden shifts to public programs like the U.S. National Flood Insurance Program (NFIP), which is already over $20 billion in debt, or state-run insurers of last resort like California’s FAIR Plan. These programs effectively subsidize risk-taking in high-hazard areas, encouraging development in places that may become uninhabitable. The longer the adaptation is delayed, the larger the eventual bill for taxpayers.

What Climate Adaptation Teaches Economics

The economics of climate adaptation offers four lessons that extend far beyond environmental policy.

First, the benefit-cost case for many adaptation investments is overwhelming. Returns of 4:1, 6:1, or even 9:1 are rare in public policy. Early warning systems, mangrove restoration, and flood protection infrastructure consistently show high returns. The obstacle is not economic; it is political and institutional. Governments must overcome short-term budget cycles and political incentives that favor ribbon-cutting over resilience.

Second, the discount rate debate is not merely technical; it is ethical. How we value the future determines whether we invest in adaptation today. A high discount rate effectively says that the welfare of future generations matters less than our own. A low discount rate says the opposite. There is no purely “objective” answer; the choice reflects societal values.

Third, adaptation is a complement to mitigation, not a substitute. The world cannot simply adapt its way out of climate change. At some level of warming, perhaps 3°C or 4°C, adaptation becomes prohibitively expensive or physically impossible for many regions. Mitigation reduces the amount of adaptation required. The optimal strategy is a portfolio approach: invest in mitigation to limit future warming, and invest in adaptation to manage the warming that is already unavoidable.

Fourth, the adaptation finance gap is a global market failure. The benefits of adaptation in developing countries, reduced migration pressure, more stable supply chains, and avoided humanitarian crises accrue globally, but the costs are local. Without a mechanism to share the costs, adaptation will be underprovided. The UNEP Adaptation Gap Report’s finding that current finance flows are just one-twelfth to one-fourteenth of what is needed represents one of the largest market failures in the global economy. The fiscal policy implications are profound: governments must plan for adaptation as a core budget priority, not an afterthought.

The Economics Behind the Headlines

Conclusion

As State Farm and Allstate withdraw from California, as New Zealand insurers abandon flood-prone towns, and as the U.S. records its third consecutive year of over $100 billion in climate disaster damages, the economic case for climate adaptation has never been clearer. The cost of doing nothing is not an abstraction. It is measured in billions of dollars of property destroyed, in livelihoods lost, in lives cut short by extreme heat. Swiss Re’s $23 trillion warning is not a prediction; it is a projection of what happens if we continue on the current path.

But the economics of adaptation also offer grounds for cautious optimism. The benefit-cost ratios are among the most favorable in public policy. Every dollar spent on early warning systems, mangrove restoration, and climate-resilient infrastructure returns many times its value in avoided losses. The challenge is not a lack of cost-effective solutions. The challenge is mobilizing the capital, overcoming the political and institutional barriers, and ensuring that the benefits of adaptation reach the communities that need them most. The economics are clear. The question is whether we will act on them.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.