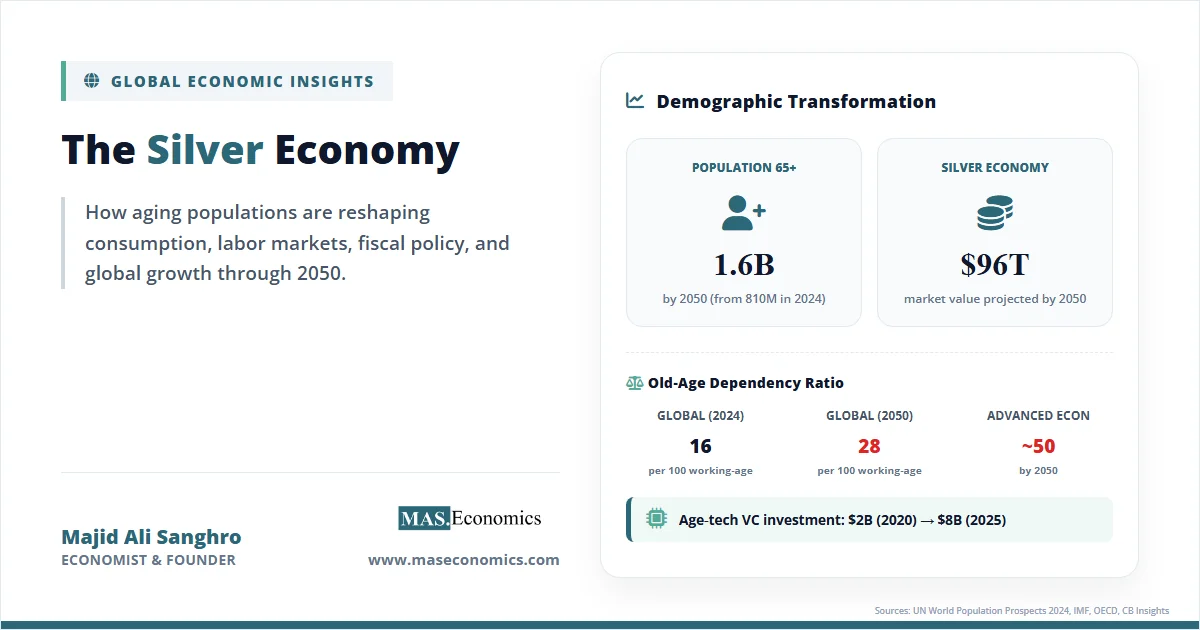

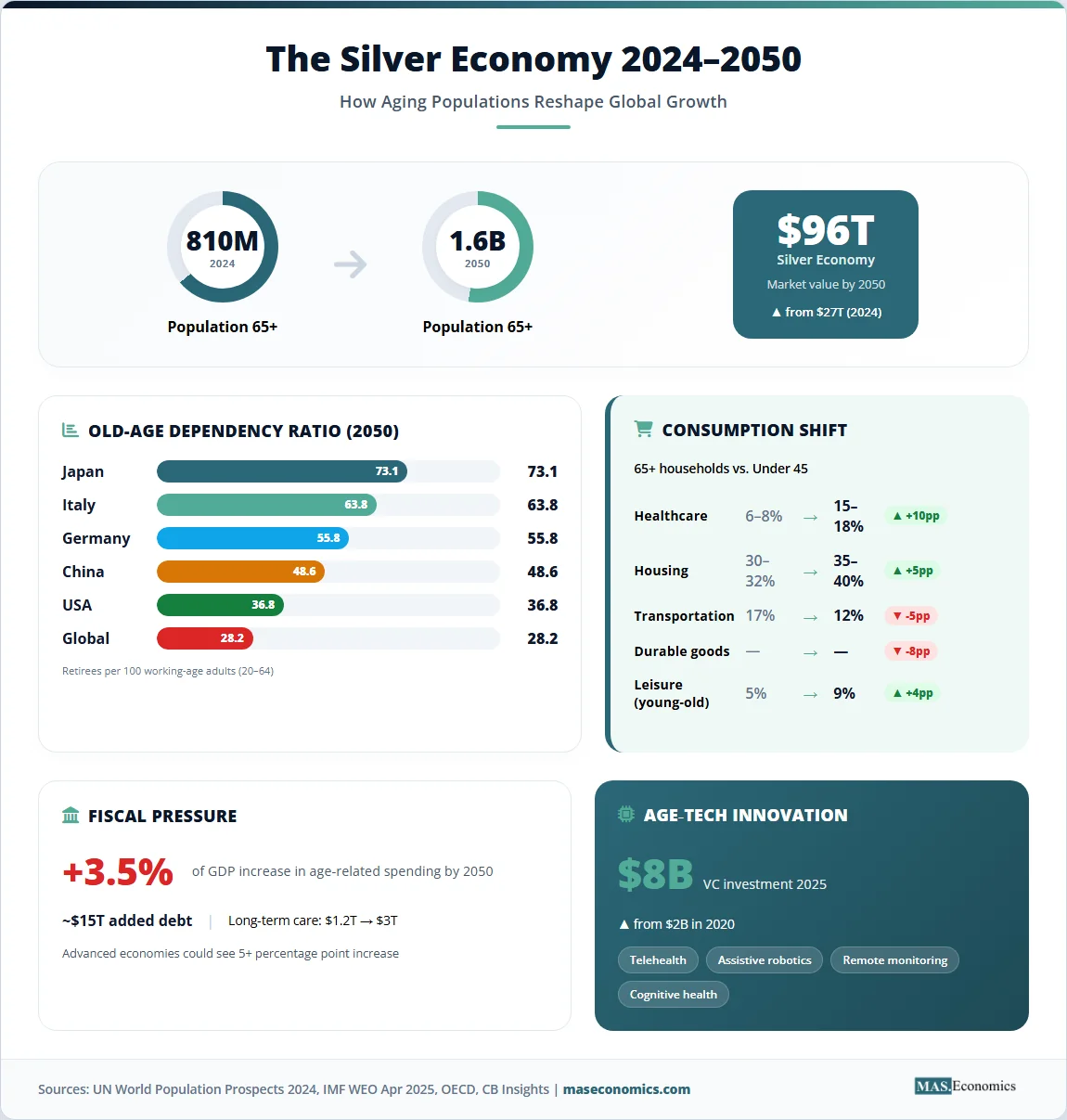

By 2050, the number of people aged 65 and older will exceed 1.6 billion, nearly double the 2020 figure. In Japan, nearly 30% of the population is already over 65. In Italy, that figure exceeds 24%. South Korea, Spain, and Germany are not far behind. China’s working-age population peaked in 2014 and is now in structural decline. The United Nations projects that by mid-century, one in six people globally will be over 65, and the old-age dependency ratio will have doubled in most advanced economies.

The silver economy encompasses all economic activity linked to the needs and preferences of older adults. It spans healthcare and pharmaceuticals, financial services and retirement planning, housing and assisted living, travel and leisure, technology and age‑tech, and consumer goods adapted for aging consumers. The global silver economy was valued at approximately $27 trillion in 2024 and is projected to reach $96 trillion by 2050. The IMF’s April 2025 World Economic Outlook dedicated an entire chapter to the macroeconomic implications of aging, noting that demographic change will be a primary driver of potential growth, savings rates, and fiscal sustainability for decades to come.

Older households spend differently than younger ones: more on healthcare, housing, and leisure services; less on durable goods, education, and transportation. This shift in the composition of consumption has implications for sectoral capital allocation, labor market structure, and the design of fiscal and monetary policy.

The Demographic Shift

The aging of the global population is one of the most consequential demographic shifts in human history. Two forces are driving it: rising life expectancy and falling fertility rates. Global life expectancy at birth has increased from 47 years in 1950 to 73 years in 2024, a gain of more than two and a half decades. Over the same period, the global total fertility rate has fallen from approximately 5.0 children per woman to 2.3, below the replacement rate of 2.1 in most advanced economies and increasingly in middle‑income countries. The result is a structural increase in the share of older people in the population and, in many countries, an absolute decline in the working‑age population.

The United Nations World Population Prospects 2024 provides the authoritative baseline. The global population aged 65 and over stood at approximately 810 million in 2024 and is projected to reach 1.6 billion by 2050. The number of people aged 80 and over will triple, from 160 million to nearly 460 million. The old‑age dependency ratio, the number of people aged 65 and over per 100 people of working age (20 to 64), will rise from 16 in 2024 to 28 in 2050 globally. In advanced economies, the ratio will approach 50, meaning that for every two working‑age adults, there will be one retirement‑age adult to support.

Regional variation is substantial. Japan is at the frontier, with an old‑age dependency ratio already above 50 and a median age of 49. Italy, Germany, and Finland are close behind. South Korea is aging faster than any other OECD country, with a fertility rate of 0.72 in 2024, the lowest in the world. China’s demographic transition is particularly abrupt: decades of one‑child policy have produced a rapidly aging society before reaching high‑income status, a phenomenon some economists describe as “getting old before getting rich.” The working‑age population peaked in 2014 and is now declining by approximately 4 million annually. By 2050, China will have more people over 65 than the entire current population of the United States.

Emerging economies are aging later but often faster. Brazil’s old‑age dependency ratio is projected to rise from 13 to 32 by 2050. India’s elderly population will exceed 300 million by mid‑century, though its dependency ratio will remain lower due to a still‑young demographic profile. Sub‑Saharan Africa remains the global exception, with a median age below 20 and the world’s fastest‑growing working‑age population. This demographic divergence between aging advanced and emerging economies will reshape global capital flows, migration patterns, and comparative advantage in labor‑intensive industries. The implications for inflation and price levels are already becoming visible, as labor scarcity in aging economies exerts upward pressure on wages and service prices.

| Country/Region | Population 65+ (2024, %) | Population 65+ (2050, % projected) | Old-Age Dependency Ratio (2024) | Old-Age Dependency Ratio (2050 projected) |

|---|---|---|---|---|

| Japan | 29.3 | 37.7 | 52.0 | 73.1 |

| Italy | 24.3 | 34.5 | 38.5 | 63.8 |

| Germany | 22.7 | 32.1 | 36.1 | 55.8 |

| China | 14.5 | 28.2 | 20.8 | 48.6 |

| United States | 17.4 | 22.8 | 27.2 | 36.8 |

| Brazil | 10.1 | 21.9 | 13.2 | 32.3 |

| India | 7.1 | 13.8 | 10.5 | 20.6 |

| World | 10.3 | 16.4 | 16.0 | 28.2 |

|

||||

Consumption Reallocation

The aging of the global population is not merely changing the number of workers and retirees; it is fundamentally altering the composition of global demand. Older households spend differently than younger households, and as the share of older households rises, aggregate consumption patterns shift in predictable and economically significant ways.

Research from the OECD and the U.S. Bureau of Labor Statistics Consumer Expenditure Survey documents these differences in detail. Households headed by someone aged 65 and over allocate approximately 15% to 18% of their spending to healthcare, compared to 6% to 8% for households under 45. They spend roughly 35% to 40% on housing, significantly more than younger households, reflecting the tendency to remain in owned homes and the rising cost of property taxes, maintenance, and utilities. Spending on food at home increases as a share of the budget, while spending on food away from home (restaurants) declines. Transportation spending falls sharply, from roughly 17% for prime‑age households to 12% for older households, driven by reduced commuting and less frequent long‑distance travel.

Leisure and hospitality present a more nuanced picture. Older households, particularly the “young old” (65 to 74), spend heavily on travel, cruises, cultural activities, and dining out. This cohort controls a disproportionate share of wealth and has both the time and financial resources for discretionary consumption. The leisure sector has increasingly pivoted to serve this demographic, with cruise lines, tour operators, and luxury hotel chains designing products specifically for older travelers. The economic impact is substantial: the global travel market for travelers aged 60 and over is projected to exceed $2 trillion annually by 2030.

The shift in consumption has profound implications for sectoral allocation of capital and for the structure of labor markets. Sectors that serve older consumers, healthcare, assisted living, financial services, leisure and hospitality, age‑tech will attract a rising share of investment and employment. Sectors dependent on younger consumers, durable goods, education, apparel, and entertainment targeted at young adults, will face structural headwinds in aging economies. This reallocation is already visible in the divergence of equity market performance between healthcare and consumer staples (which have benefited from aging) and traditional retailers and durable goods manufacturers (which have faced slowing demand growth). For a broader perspective on how demographic shifts affect inflation dynamics, see our analysis of inflation and demographics.

Pensions, Healthcare, and Sovereign Debt

The most immediate and politically salient consequence of population aging is the pressure on public finances. Pay‑as‑you‑go pension systems, in which current workers’ contributions fund current retirees’ benefits, are actuarially unsustainable in an aging society. As the ratio of workers to retirees falls, either contributions must rise, benefits must fall, or the retirement age must increase. Most advanced economies are confronting some combination of these difficult choices.

The IMF’s April 2025 World Economic Outlook quantifies the fiscal challenge. In advanced economies, age‑related spending, primarily pensions and healthcare, is projected to rise by an average of 3.5 percentage points of GDP by 2050 under current policies. In some countries, including Japan, Italy, and Germany, the increase could exceed 5 percentage points. Without offsetting policy adjustments, this would add approximately $15 trillion to global public debt by mid‑century. The OECD Pensions Outlook 2025 estimates that the average OECD country would need to increase the retirement age by approximately 4 years, raise pension contributions by 20%, or reduce replacement rates by 15% to stabilize pension finances over the next three decades.

Healthcare costs present an even more intractable challenge. Per capita healthcare spending rises sharply with age, particularly after age 75. Long‑term care, including nursing homes, assisted living, and home health aides, is the fastest‑growing component of health spending in advanced economies. The World Health Organization projects that global spending on long‑term care will rise from approximately $1.2 trillion in 2024 to over $3 trillion by 2050. In most countries, these costs are borne primarily by governments through Medicaid‑style programs or national health services, creating structural upward pressure on public spending.

Source: United Nations World Population Prospects 2024, IMF World Economic Outlook April 2025, OECD Pensions Outlook 2025 | MASEconomics.com

Age‑Tech and the Longevity Economy

The challenges of an aging society are also generating substantial opportunities for innovation. The age‑tech sector, comprising technologies designed to improve the quality of life, health outcomes, and independence of older adults, is one of the fastest‑growing segments of the global technology industry. Venture capital investment in age‑tech exceeded $8 billion in 2025, up from $2 billion in 2020, according to CB Insights. The addressable market spans telehealth and remote monitoring, assistive robotics, cognitive health platforms, social connectivity tools, and financial technology tailored to retirement planning and wealth decumulation.

Telehealth and remote patient monitoring have matured rapidly. Devices that track vital signs, detect falls, monitor medication adherence, and enable virtual consultations with healthcare providers are reducing the need for in‑person visits and enabling older adults to age in place. The McKinsey Global Institute estimates that widespread adoption of remote monitoring could reduce healthcare costs by $300 billion annually in the United States alone by 2030, primarily by reducing preventable hospitalizations and delaying transitions to institutional care.

Assistive robotics and home automation are expanding the range of tasks that older adults can perform independently. Robotic vacuum cleaners, voice‑activated home assistants, automated medication dispensers, and mobility aids are increasingly affordable and user‑friendly. Japan, facing the most acute labor shortages in elder care, has invested heavily in care robots, including lifting devices, mobility assistants, and companion robots designed to reduce social isolation. The global market for elder care robotics is projected to exceed $10 billion by 2030.

Financial technology for the silver economy is another rapidly expanding niche. Digital platforms that help retirees manage decumulation, optimize Social Security claiming strategies, and navigate Medicare choices are attracting substantial capital. So‑called “retirement income tech” addresses a genuine market failure: the financial services industry has historically focused on accumulation (saving for retirement) while neglecting decumulation (spending in retirement). As the baby boom generation enters retirement, demand for these tools is surging. The intersection of aging and technology also connects to broader questions about the future of work and productivity. As explored in our article on automation and the future of work, labor‑saving technologies may help offset the decline in working‑age populations in aging economies.

Labor Markets and Migration

The decline in working‑age populations in advanced economies creates powerful incentives for automation, increased labor force participation among older workers, and immigration. Each of these responses is already visible in the data.

Labor force participation among older workers has risen steadily across OECD countries. In the United States, the participation rate for workers aged 65 and over increased from 17% in 2000 to 24% in 2025. In Japan, the rate exceeds 35%. Several factors are driving this trend: rising life expectancy and health improvements enable longer careers; the shift from physically demanding manufacturing jobs to service and knowledge work makes extended employment more feasible; and inadequate retirement savings compel many older adults to continue working. Policy changes have reinforced these trends. The United States raised the full retirement age for Social Security from 65 to 67. Many European countries have eliminated mandatory retirement ages and introduced flexible retirement options that allow workers to combine part‑time employment with partial pension benefits.

Immigration offers a demographic buffer, but its political viability is contested. Canada and Australia have embraced high‑skilled immigration as an explicit policy response to aging, maintaining working‑age population growth and favorable dependency ratios. The United States has a more mixed record, with immigration policy increasingly politicized. Japan and South Korea have historically maintained restrictive immigration policies but are gradually opening to foreign workers in specific sectors, including elder care, agriculture, and construction, as labor shortages intensify. The European Union faces a complex landscape, with some member states (Germany, Sweden) pursuing relatively open policies and others (Hungary, Poland) resisting immigration. The economic evidence is clear: immigration can significantly mitigate the fiscal pressures of aging, but the distributional consequences and cultural anxieties make it one of the most difficult policy levers to deploy.

Automation and artificial intelligence represent a third, and potentially most transformative, response. If robots and AI can substitute for labor in elder care, manufacturing, and services, the economic constraints imposed by a shrinking workforce could be substantially relaxed. Japan has invested heavily in this vision, funding research and development in care robots and automated manufacturing. However, the productivity benefits of AI and automation have so far been concentrated in a narrow set of industries, and the broader economic impact remains uncertain. The degree to which technology can offset demographic decline is one of the most consequential questions in long‑run economic forecasting.

Monetary Policy and the Neutral Rate

Population aging also has profound implications for monetary policy. A substantial body of research, summarized by the Bank for International Settlements and the Federal Reserve, finds that aging populations put sustained downward pressure on the neutral rate of interest, the rate consistent with full employment and stable inflation. The mechanisms are straightforward: older households save more and borrow less than younger households, increasing the supply of savings relative to investment demand. Slower labor force growth reduces the demand for business investment, as firms need less capital to equip a shrinking workforce. Rising life expectancy increases desired retirement savings, further boosting the supply of savings. The combined effect is a structural decline in equilibrium interest rates.

This demographic drag on interest rates complicates the task of central banks. In an aging economy, the neutral rate may be persistently low, limiting the scope for conventional interest rate cuts during recessions and increasing the likelihood that central banks will need to rely on unconventional tools such as quantitative easing or negative rates. The Bank of Japan’s decades‑long struggle with deflation and the zero lower bound is, in significant part, a demographic story. As aging spreads to other advanced economies and eventually to emerging markets, the monetary policy challenges that Japan has faced for a generation may become increasingly common.

Fiscal policy and monetary policy interact in this demographic context. In a low‑neutral‑rate environment, the cost of servicing public debt is lower than historical norms, potentially creating fiscal space for age‑related spending. However, this fiscal space is contingent on the persistence of low rates, which in turn depends on the credibility of central bank independence and the anchoring of inflation expectations. The fiscal‑monetary nexus in aging societies is likely to be a central theme of macroeconomic policy for decades to come.

MASEconomics Explains

Four concepts behind the silver economy

Old-Age Dependency Ratio

The number of people aged 65 and over per 100 people of working age (typically 20–64). This ratio is the most widely used measure of demographic pressure on pension systems, healthcare, and public finances. In advanced economies, the ratio is projected to rise from approximately 30 in 2024 to nearly 50 by 2050.

Neutral Rate of Interest (r*)

The real interest rate consistent with full employment and stable inflation. Research from the BIS and Federal Reserve finds that aging populations reduce the neutral rate by increasing the supply of savings relative to investment demand. A lower neutral rate limits the scope for conventional monetary easing during recessions.

Consumption Reallocation

The shift in the composition of aggregate demand as the share of older households rises. Older households allocate a larger share of spending to healthcare, housing, and leisure services, and a smaller share to durable goods, education, and transportation. This reallocation has profound implications for sectoral employment and investment.

Age‑Tech

Technologies designed to improve the quality of life, health outcomes, and independence of older adults. The sector includes telehealth, remote monitoring, assistive robotics, cognitive health platforms, and retirement income technology. Venture capital investment in age‑tech exceeded $8 billion in 2025.

Key Takeaway and Conclusion

The global population aged 65 and over will nearly double to 1.6 billion by 2050. The old‑age dependency ratio will rise from 16 to 28 globally, and to nearly 50 in advanced economies. The silver economy is projected to reach $96 trillion by 2050, reshaping consumption, labor markets, and fiscal policy. Demand shifts toward healthcare, housing, and leisure services, and away from durable goods and education, reallocating capital and employment across sectors. Fiscal pressures from rising pension and healthcare costs will add approximately $15 trillion to global public debt by mid‑century under current policies.

Labor force participation among older workers is rising. Age‑tech innovation is improving health outcomes and enabling independent living. Immigration and automation offer potential offsets to declining working‑age populations, though both face political and technological constraints. The neutral rate of interest is likely to remain low, creating fiscal space but limiting the scope for conventional monetary policy. Successful adaptation to demographic aging requires parametric pension and healthcare reforms, policies that extend working lives, high‑skilled immigration where politically feasible, and innovation in age‑tech and automation.

The silver economy is reshaping global growth.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.