Bitcoin went from zero to a $1.5 trillion asset class in fifteen years. The total cryptocurrency market reached $2.6 trillion in capitalisation by early 2026, with over 16,000 distinct tokens trading across 1,400 exchanges. Stablecoins alone now settle more transaction volume daily than Visa. China’s digital yuan has processed $2.37 trillion in cumulative transactions through 3.48 billion wallet operations. Meanwhile, 137 countries representing 98% of global GDP are exploring central bank digital currencies. The economics of cryptocurrency is no longer a fringe topic. It sits at the intersection of monetary theory, financial regulation, and the future architecture of global payments.

Yet most economists remain deeply divided. Bitcoin consumes more electricity annually than Argentina. Roughly 95% of tokens launched since 2017 have lost the majority of their value. The collapse of FTX in 2022 wiped out $32 billion in a matter of days. And the fundamental question that drives all monetary economics, whether cryptocurrency constitutes money, remains unresolved after more than a decade of debate.

From Cypherpunk Manifesto to Trillion-Dollar Asset Class

The origins of cryptocurrency trace to a 2008 white paper published under the pseudonym Satoshi Nakamoto. The paper proposed a peer-to-peer electronic cash system that required no trusted intermediary, no bank, and no central authority to verify transactions. Bitcoin launched on 3 January 2009, when Nakamoto mined the genesis block. Embedded in that block was a headline from The Times of London: “Chancellor on brink of second bailout for banks.” The message was deliberate. Bitcoin was conceived as a response to the 2008 financial crisis, a system where trust was placed in mathematics rather than in institutions that had just demonstrated their capacity for catastrophic failure.

For five years, Bitcoin remained an obscurity. Its first recorded commercial transaction occurred on 22 May 2010, when programmer Laszlo Hanyecz paid 10,000 BTC for two pizzas. At April 2026 prices, those pizzas would have cost roughly $740 million. The period from 2013 to 2017 saw the emergence of thousands of alternative cryptocurrencies (altcoins) and the initial coin offering (ICO) boom, which raised $5.6 billion in 2017 alone before regulators intervened.

Ethereum, launched in 2015, introduced a critical innovation: smart contracts, self-executing programmes that run on a blockchain and enable financial transactions without intermediaries. This created the foundation for decentralised finance (DeFi), a parallel financial system offering lending, borrowing, trading, and insurance without banks. By its peak in late 2021, the total value locked in DeFi protocols exceeded $175 billion.

The institutional era began in 2020 when publicly listed companies, sovereign wealth funds, and asset managers entered the market. MicroStrategy accumulated over 200,000 BTC. The approval of spot Bitcoin exchange-traded funds (ETFs) in the United States in January 2024 opened the floodgates to mainstream investment. Within twelve months, US-listed Bitcoin ETFs attracted over $35 billion in net inflows, making them among the most successful ETF launches in history.

Table 1. Key Milestones in the Economics of Cryptocurrency (2008–2026)

| Year | Event | Economic Significance |

|---|---|---|

| 2008 | Satoshi Nakamoto publishes the Bitcoin white paper | Proposed a peer-to-peer payment system requiring no trusted third party |

| 2009 | Bitcoin network launches; genesis block mined | First practical implementation of decentralised digital scarcity |

| 2014 | Mt. Gox exchange collapses (850,000 BTC lost) | Exposed counterparty risk and absence of deposit insurance in crypto |

| 2015 | Ethereum launches with smart contract functionality | Enabled programmable money and decentralised applications |

| 2017 | ICO boom raises $5.6 billion; Bitcoin reaches $20,000 | First major speculative bubble; subsequent 80% crash in 2018 |

| 2020 | DeFi summer; total value locked surpasses $10 billion | Decentralised lending and trading gain traction as alternative financial rails |

| 2021 | El Salvador adopts Bitcoin as legal tender; BTC reaches $69,000 | First nation-state adoption; second major speculative peak |

| 2022 | FTX collapse; Terra/Luna stablecoin death spiral | $32 billion exchange failure; $60 billion algorithmic stablecoin collapse |

| 2024 | US approves spot Bitcoin ETFs; BTC surpasses $100,000 | $35 billion+ ETF inflows in first year; institutional legitimisation |

| 2025–2026 | EU MiCA regulation in force; US bans retail CBDC; stablecoin regulation advances | Regulatory bifurcation: Europe regulates, US restricts CBDCs but embraces stablecoins |

|

||

What Economic Theory Says About Cryptocurrency

Cryptocurrency challenges and illuminates several foundational concepts in monetary economics. Four theoretical frameworks are essential to understanding what crypto is, what it is not, and why it behaves the way it does.

The Functions of Money: Does Cryptocurrency Qualify?

Economics defines money by three functions: medium of exchange, store of value, and unit of account. Bitcoin fails convincingly on two of the three. As a medium of exchange, Bitcoin processes roughly 7 transactions per second compared to Visa’s 24,000. Transaction fees spike during periods of congestion, reaching over $60 per transaction in late 2024. Very few merchants accept Bitcoin for everyday purchases. As a unit of account, Bitcoin’s price volatility makes it impractical for denominating contracts, wages, or prices. An asset that can move 10% in a single day cannot serve as a stable measuring rod for economic value.

Where Bitcoin has gained traction is as a store of value, specifically as “digital gold.” Like gold, Bitcoin has a fixed supply (capped at 21 million coins), cannot be debased by government policy, and exists outside the control of any single institution. This narrative has proven powerful with institutional investors, particularly in environments of high government debt, expansive quantitative easing, and declining trust in fiat currencies. The counterargument is that gold has 5,000 years of history as a store of value and has intrinsic industrial uses, while Bitcoin’s value is entirely derived from collective belief.

Stablecoins, by contrast, are specifically designed to function as money. Tether (USDT) and USD Coin (USDC), each pegged 1:1 to the US dollar, have a combined market capitalisation exceeding $200 billion. They process tens of billions of dollars in daily settlement volume, primarily for cross-border transfers and crypto trading. Stablecoins satisfy the medium-of-exchange and unit-of-account functions that Bitcoin cannot. They are, in effect, privately issued narrow-bank deposits operating on blockchain rails.

Speculative Bubbles and the Greater Fool Theory

Cryptocurrency markets have exhibited classic speculative bubble dynamics at least three times: 2017, 2021, and the meme coin manias of 2024–2025. The efficient market hypothesis holds that asset prices reflect all available information. In crypto markets, this assumption breaks down spectacularly. Tokens with no revenue, no product, and no identifiable team have reached billion-dollar valuations within hours of launch.

The economic explanation lies in a combination of factors. Prospect theory, the framework developed by Kahneman and Tversky, explains why investors overweight small probabilities of extreme gains, treating crypto as a lottery ticket. Herd behaviour, amplified by social media, creates self-reinforcing feedback loops where rising prices attract new buyers, which pushes prices higher, which attracts more buyers, until the cycle reverses. The absence of fundamental valuation anchors, crypto has no earnings, no dividends, and no cash flows to discount, means there is no theoretical floor to constrain speculative excess.

The Terra/Luna collapse of May 2022 demonstrated these dynamics at catastrophic scale. Terra’s algorithmic stablecoin, UST, maintained its dollar peg through a mechanism that depended on continuous demand for its companion token, Luna. When confidence cracked, the peg broke, and a reflexive death spiral destroyed roughly $60 billion in value within seventy-two hours. The episode was a textbook illustration of what economists call a bank run, except it occurred in a system with no central bank, no deposit insurance, and no lender of last resort.

Seigniorage, Central Bank Digital Currencies, and the State’s Monetary Monopoly

Throughout history, the power to issue money has been a sovereign prerogative. Seigniorage, the profit a government earns from issuing currency at a cost below its face value, is both a revenue source and a tool of economic management. Cryptocurrency threatens this monopoly. If citizens can transact in Bitcoin or stablecoins rather than the national currency, central banks lose control over the money supply, the monetary transmission mechanism weakens, and the government’s ability to conduct monetary policy is diminished.

This is the core economic motivation behind central bank digital currencies. As of early 2026, 137 countries representing 98% of global GDP are exploring CBDCs. Three countries, the Bahamas, Jamaica, and Nigeria, have fully launched retail CBDCs. China’s e-CNY is the furthest advanced among major economies, having processed $2.37 trillion in cumulative transactions across 3.48 billion wallet operations by November 2025. India’s digital rupee pilot has expanded to 19 banks. The European Central Bank is in a two-year preparation phase for a digital euro. The United States, by contrast, issued an executive order in January 2025 prohibiting all work on a retail CBDC.

The economic tension is clear. CBDCs offer governments the ability to maintain monetary sovereignty, improve financial inclusion, reduce cash-handling costs, and programme fiscal transfers directly to citizens’ wallets. But they also raise profound concerns about surveillance, privacy, and the potential for government overreach. The future of the global financial system depends in part on how this tension between decentralised private money and centralised digital state money is resolved.

Financial Inclusion

Proponents argue that cryptocurrency can bring financial inclusion to the 1.4 billion adults worldwide who lack access to a bank account. The logic is straightforward: a smartphone and an internet connection provide access to a global financial system without the need for bank branches, credit checks, or minimum balances. Stablecoins enable cross-border remittances at a fraction of the cost charged by traditional services like Western Union, which typically levy fees of 5–9% on transfers to developing countries.

The evidence is mixed. In El Salvador, where Bitcoin was made legal tender in 2021, government data showed that only 20% of citizens used the official Chivo wallet after the initial adoption incentive expired. In Nigeria, where the eNaira launched in 2021, adoption has been slow despite the central bank’s aggressive promotion. The binding constraint on financial inclusion is not the absence of a digital currency. It is the absence of reliable internet, digital literacy, and trust in financial institutions. Cryptocurrency does not solve these problems.

The Numbers Behind the Crypto Economy

The cryptocurrency market has grown from near-zero to a multi-trillion-dollar asset class in just over a decade. The chart below tracks total cryptocurrency market capitalisation from 2014 to early 2026, showing the boom-bust cycles that define this market.

Total Cryptocurrency Market Capitalisation (2014–2026, Quarterly)

Source: CoinGecko global market cap data. Values in trillions of US dollars at quarter-end.

Stablecoins have emerged as the most economically significant use case for blockchain technology, settling more daily volume than many traditional payment networks. The chart below shows the rapid growth in stablecoin market capitalisation.

Stablecoin Market Capitalisation Growth (2019–2026)

Source: CoinGecko and DefiLlama. Includes USDT, USDC, DAI, and other major stablecoins.

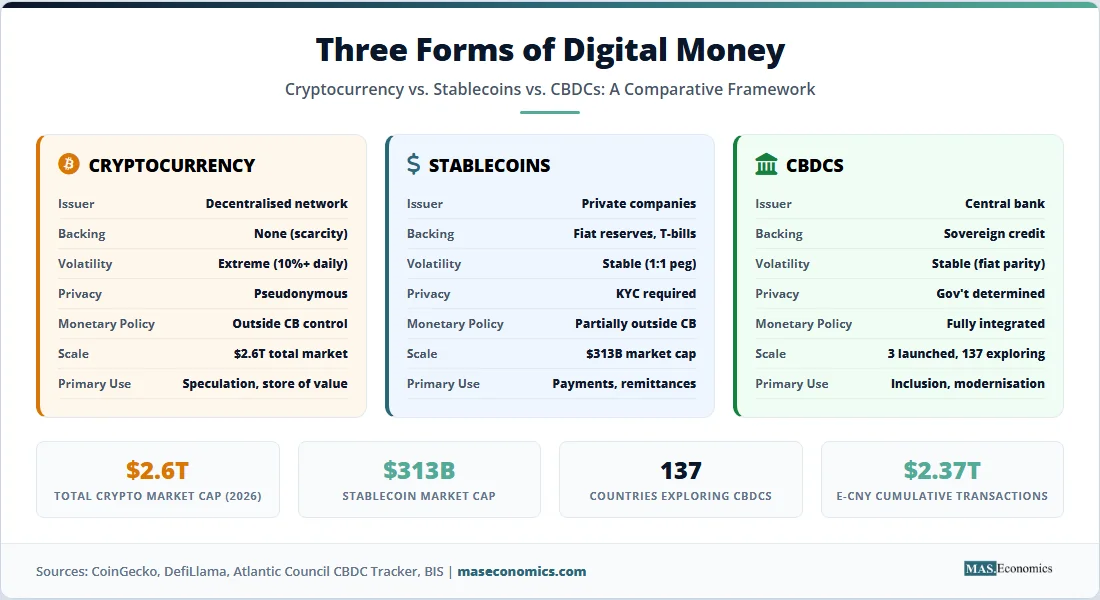

The following table compares the key properties of the three competing forms of digital money: decentralised cryptocurrency, private stablecoins, and government-issued CBDCs.

Table 2. Three Forms of Digital Money: A Comparative Framework

| Property | Cryptocurrency (e.g., Bitcoin) | Stablecoins (e.g., USDT, USDC) | CBDCs (e.g., e-CNY, Digital Euro) |

|---|---|---|---|

| Issuer | No central issuer; decentralised network | Private companies (Tether, Circle) | Central bank / government |

| Backing | None (value from scarcity and demand) | Fiat reserves, treasury bills, cash equivalents | Full faith and credit of the sovereign |

| Price Stability | Extremely volatile (10%+ daily swings) | Stable (designed for 1:1 peg) | Stable (identical value to fiat) |

| Privacy | Pseudonymous (traceable on-chain) | Variable (KYC required on most platforms) | Determined by government; surveillance concerns |

| Monetary Policy Impact | Outside central bank control | Partially outside central bank control | Fully integrated into monetary policy toolkit |

| Current Scale | $1.5T (Bitcoin); $2.6T (total market) | $313 billion market cap | 3 launched; 137 countries exploring |

| Primary Use Case | Speculation, store of value | Payments, remittances, trading settlement | Financial inclusion, payment modernisation |

|

|

|||

Lessons and Takeaways

Four economic lessons emerge from the first fifteen years of cryptocurrency.

First, the market for money is contestable. For centuries, the state held an unquestioned monopoly on currency issuance. Cryptocurrency has demonstrated that private actors can create monetary instruments that attract trillions in demand. Stablecoins, in particular, have proven that privately issued digital dollars can achieve scale, liquidity, and utility that rival state-issued alternatives. The state’s monetary monopoly is no longer guaranteed; it must be defended through superior technology, regulation, and institutional trust.

Second, speculation and innovation are inseparable in nascent markets. The same features that make crypto vulnerable to bubbles, permissionless access, global liquidity, and 24/7 trading are also the features that enabled rapid experimentation in DeFi, smart contracts, and programmable money. The challenge for regulators is to suppress fraud and protect consumers without extinguishing the innovation that the underlying technology enables.

Third, the geography of crypto regulation is diverging. The EU’s Markets in Crypto-Assets (MiCA) regulation provides comprehensive licensing and consumer protection. The United States has moved to embrace stablecoins and ETFs while banning a federal retail CBDC. China has banned private cryptocurrency entirely while building the world’s most advanced CBDC. These divergent approaches will shape which jurisdictions capture the economic benefits of digital finance and which bear the risks.

Fourth, the economic impact of crypto is concentrated in its least glamorous application. The headline-grabbing price swings of Bitcoin attract attention, but the most consequential economic development is the rise of stablecoins as a global settlement layer and the parallel emergence of CBDCs as a government response. The future of money may be less about which coin reaches the highest price and more about which infrastructure processes the most transactions.

MASEconomics Explains

Conclusion

The economics of cryptocurrency encompasses a $2.6 trillion asset class, a $313 billion stablecoin settlement layer, and a global race among 137 countries to develop central bank digital currencies. Bitcoin has proven the concept of decentralised digital scarcity. Stablecoins have demonstrated that privately issued digital dollars can achieve transaction volumes rivalling the largest payment networks. CBDCs represent the state’s response, an attempt to retain monetary sovereignty in an era where the technology to issue money is no longer the exclusive domain of governments.

The fundamental questions remain open. Whether Bitcoin constitutes money or merely a speculative asset. Whether stablecoins are a breakthrough in financial infrastructure or a systemic risk without adequate reserves. Whether CBDCs will enhance financial inclusion or enable surveillance. The answers will depend not on the technology itself, but on the economic incentives, regulatory frameworks, and institutional designs that govern how these instruments are created, traded, and integrated into the global financial system.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.