The global monetary system is undergoing its most significant transformation since the end of the gold standard. Two competing visions for the future of digital money are rapidly taking shape: Central Bank Digital Currencies (CBDCs), the state-backed digital equivalent of cash, and stablecoins, privately issued digital assets pegged to fiat currencies. Both promise faster, cheaper payments, greater financial inclusion, and a more efficient financial system. Yet they represent fundamentally different philosophies about who should control the money of the future.

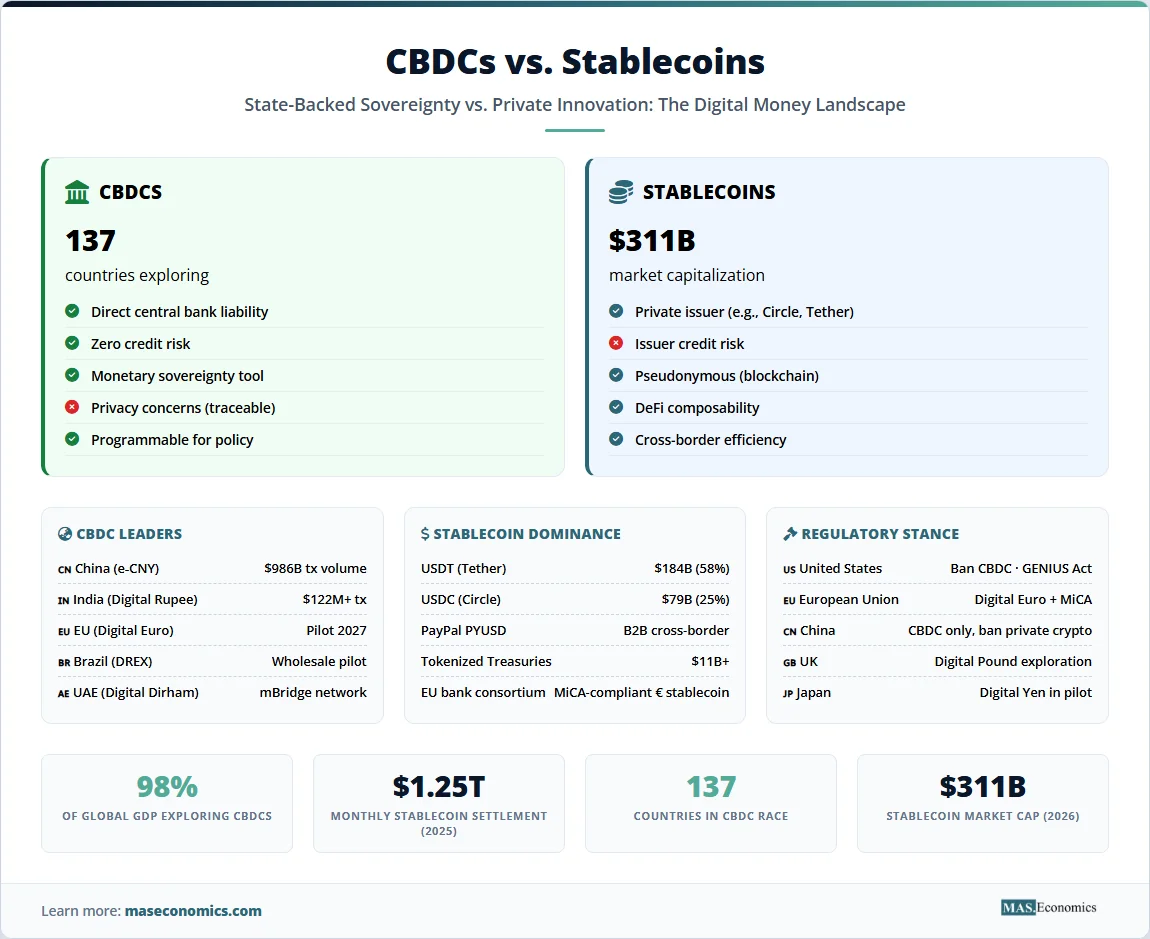

As of mid-2025, 137 countries and currency unions, representing 98% of global GDP, are researching or piloting CBDCs, a dramatic increase from just 35 countries in 2020. Meanwhile, the total market capitalization of stablecoins has surged past $311 billion, with daily transaction volumes routinely exceeding $25 billion and annual settlement volumes now surpassing those of major payment networks. The battle lines are drawn: will the future of money be controlled by central banks or by private innovators operating within new regulatory frameworks?

Let’s explore the fundamental differences between CBDCs and stablecoins, examine the global race to launch sovereign digital currencies, analyze the explosive growth of stablecoins and the regulatory frameworks designed to govern them, and assess what this competition means for the global monetary system.

What Are CBDCs and Stablecoins?

Both CBDCs and stablecoins are digital representations of fiat currency. But the similarities end there. A CBDC is a direct liability of the central bank, meaning it carries the same sovereign backing as physical cash. When you hold a digital euro or a digital yuan, you hold a claim directly on the European Central Bank or the People’s Bank of China. A stablecoin, by contrast, is a liability of a private issuer. When you hold USDC or USDT, you hold a claim on Circle or Tether, backed by reserves of cash, cash equivalents, and other assets that the issuer holds.

This distinction is fundamental. A CBDC is sovereign money, carrying no credit or liquidity risk because the central bank can always create more of it. A stablecoin carries the credit risk of its issuer. If the issuer’s reserves are mismanaged or if the assets backing the stablecoin lose value, the stablecoin can break its peg, as happened spectacularly with TerraUSD in May 2022. The entire stablecoin ecosystem has been shaped by the lessons of that collapse.

Central banks are pursuing CBDCs for several reasons. The rise of private digital currencies, including stablecoins and cryptocurrencies, threatens to erode monetary sovereignty. If citizens and businesses increasingly use privately issued digital dollars instead of sovereign currency, central banks lose their ability to conduct monetary policy effectively. CBDCs also offer tools to modernize payment systems, reduce the costs of cash management, expand financial inclusion, and provide a programmable platform for fiscal policy, including the ability to distribute stimulus payments directly to citizens. For many developing economies, CBDCs also represent a path to reducing reliance on the U.S. dollar for domestic transactions.

Stablecoins, meanwhile, have emerged as the preferred digital dollar for the crypto economy. They provide the on-ramp and off-ramp between fiat and crypto assets, serve as the primary trading pair on decentralized exchanges, and increasingly function as a medium of exchange for cross-border payments and remittances. Their growth has been explosive precisely because they solve a genuine problem: moving money across borders through traditional banking channels remains slow and expensive. Stablecoins offer settlement in minutes rather than days, with fees measured in cents rather than percentage points. This utility has attracted not just crypto-natives but also institutional giants like Visa, Stripe, and BlackRock, all of which have integrated stablecoin capabilities into their payment infrastructure.

Table 1: CBDCs vs. Stablecoins: A Comparison

| Feature | CBDC | Stablecoin |

|---|---|---|

| Issuer | Central bank (sovereign) | Private company (e.g., Circle, Tether) |

| Liability | Direct claim on central bank | Claim on issuer’s reserves |

| Credit Risk | None (sovereign backing) | Issuer credit risk |

| Primary Use Cases | Domestic payments, monetary policy | Crypto trading, cross-border payments, DeFi |

| Privacy Model | Varies; often traceable by design | Pseudonymous (blockchain transparency) |

| Programmability | Potential for policy-driven controls | Smart contract composability |

| Global Adoption (2025-26) | 137 countries exploring; few launched | $311B+ market cap; widely adopted in crypto |

|

||

137 Countries and Counting

The numbers tell a story of remarkable ambition. According to the Atlantic Council’s CBDC Tracker, as of July 2025, 137 countries and currency unions are actively researching, developing, or piloting CBDCs, up from just 35 in 2020. Forty-nine countries are in advanced stages of development or pilot programs. Yet only a handful have actually launched fully functional retail CBDCs: the Bahamas (Sand Dollar), Nigeria (eNaira), Jamaica (JAM-DEX), and Zimbabwe (ZiG). China’s digital yuan remains the largest pilot globally, with over $986 billion in cumulative transaction volume as of mid-2024.

China’s early mover advantage in CBDCs is strategic. The digital yuan, or e-CNY, is designed not just as a domestic payment rail but as a potential tool for internationalizing the renminbi. On January 1, 2026, China introduced interest-bearing e-CNY wallets, making the digital currency more competitive with traditional savings accounts and signaling a long-term ambition to challenge dollar dominance. The People’s Bank of China has also spearheaded the mBridge project, a cross-border CBDC platform developed in collaboration with the central banks of Hong Kong, Thailand, and the United Arab Emirates. The UAE’s Digital Dirham, which began pilot testing in November 2025, is built on the mBridge architecture, demonstrating the potential for CBDC networks to bypass the traditional correspondent banking system.

India’s digital rupee represents the second-largest CBDC pilot globally. By March 2025, transactions had surpassed 10 billion rupees ($122 million), and the Reserve Bank of India is expanding the pilot to include programmable payments and offline functionality. Brazil’s DREX project, the digital real, is advancing toward a wholesale CBDC model designed to facilitate tokenized asset settlement and interbank transactions. The Bank of Japan, after years of cautious experimentation, is now moving toward a potential launch of a digital yen, driven by concerns over the dominance of private stablecoins in cross-border payments.

The European Union is pursuing a more deliberate path. In October 2025, the European Central Bank announced that the digital euro project would move to its next phase, with a pilot exercise planned for 2027 and readiness for a potential first issuance by 2029, contingent on the adoption of enabling legislation in 2026. The digital euro is designed to preserve European monetary sovereignty in an era of digital payments, complement cash rather than replacing it, and provide a European alternative to U.S.-dominated payment networks and stablecoins. ECB President Christine Lagarde has emphasized that the digital euro will protect privacy, ensure resilience, and foster innovation in European payments.

Source: Atlantic Council CBDC Tracker (2025), ForkLog (2026), Antier Solutions (2025) | MASEconomics.com

The Stablecoin Surge

While central banks deliberate, stablecoins have scaled with astonishing speed. The total market capitalization of stablecoins surpassed $311 billion in early 2026, with Tether’s USDT accounting for approximately $184 billion (58% market share) and Circle’s USDC at $79 billion. Together, these two issuers control more than 80% of the stablecoin market. In 2025, USDC grew 73% year-over-year, outpacing USDT’s 36% growth, reflecting increasing institutional preference for regulated, transparent issuers.

The transaction volumes are even more striking. In 2025, stablecoins settled over $1.25 trillion in monthly adjusted volume, surpassing the combined transaction volume of Visa and Mastercard. USDC alone processed $17.3 trillion in transferred value in 2025, compared to $12.9 trillion for USDT. For context, stablecoin settlement volumes now rival or exceed those of major payment networks, underscoring their emergence as de facto digital payment infrastructure.

Several factors have driven this explosive growth. First, stablecoins have become the essential plumbing of the crypto economy. They account for approximately 75% of all liquidity in decentralized finance (DeFi) protocols, serving as the primary trading pair on decentralized exchanges and the dominant form of collateral in lending markets. Second, stablecoins have proven remarkably effective for cross-border payments and remittances, offering settlement times measured in minutes rather than days and fees that are a fraction of traditional remittance costs, which average 6.6% globally. Third, institutional adoption has accelerated as major financial players integrate stablecoin capabilities. PayPal’s PYUSD stablecoin facilitates B2B cross-border flows with up to 90% lower fees. Stripe’s $1.1 billion acquisition of the stablecoin platform Bridge in 2025 signaled strategic confidence in stablecoin-enabled payment rails. Nine European banks have formed a consortium to launch a MiCA-compliant euro stablecoin by 2026.

The stablecoin ecosystem is also evolving beyond the duopoly of USDT and USDC. A new generation of regulated, yield-bearing stablecoins is emerging, offering holders interest on their balances. Tokenized U.S. Treasury products, which function similarly to stablecoins but with explicit yield, have grown to over $11 billion in market value, with Circle’s USYC product surpassing BlackRock’s BUIDL fund. This convergence of stablecoins and tokenized real-world assets suggests that the future of digital money may be a spectrum of instruments ranging from pure payment tokens to interest-bearing digital cash equivalents.

The success of stablecoins is not accidental. They solve genuine economic frictions that the traditional banking system has failed to address. Sending money across borders remains slow, expensive, and opaque. Access to dollar-denominated savings instruments is limited in many emerging markets. Small and medium-sized enterprises struggle with the costs and delays of international trade finance. Stablecoins offer a technological solution to these frictions, and their adoption reflects real economic demand rather than mere speculation.

Banning CBDCs, Embracing Stablecoins

Perhaps the most consequential development in the digital money landscape is the stark divergence in U.S. policy. In January 2025, President Trump issued an executive order halting all federal CBDC development. The House of Representatives subsequently passed the Anti-CBDC Surveillance State Act (H.R. 1919) in July 2025, which would permanently prohibit the Federal Reserve from offering retail bank accounts or issuing a CBDC directly or indirectly. The bill’s sponsors argue that a retail CBDC would create an unprecedented surveillance apparatus, enabling the government to monitor, control, or even “deplatform” individual spending. The Senate passed a parallel bill in March 2026 that would ban a Federal Reserve CBDC through 2030.

Having rejected a sovereign digital dollar, the United States has instead embraced a policy of promoting regulated private stablecoins as the digital extension of dollar dominance. The GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins), signed into law on July 18, 2025, establishes the first comprehensive federal regulatory framework for payment stablecoins. The Act restricts stablecoin issuance to permitted payment stablecoin issuers, imposes strict 1:1 reserve requirements, mandates monthly audits and Bank Secrecy Act compliance, and creates three pathways to licensure: through federal banking regulators, state regulators, or as a federally qualified issuer. The Office of the Comptroller of the Currency issued proposed implementing regulations in February 2026, with the Act expected to take full effect in early 2027.

This policy pivot is strategic. U.S. lawmakers and regulators have concluded that promoting dollar-denominated stablecoins is a more effective way to extend the dollar’s global reach than creating a government-controlled digital currency. Stablecoins, particularly those issued by U.S.-regulated entities like Circle, effectively export the dollar to markets where access to dollar banking is limited. Every stablecoin transaction settled in USDC or USDT increases global demand for dollars and reinforces the dollar’s status as the world’s reserve currency. As Senator Bill Hagerty, a key architect of the GENIUS Act, has argued, regulated stablecoins represent “the next chapter of American dollar dominance.”

This U.S. strategy stands in stark contrast to the European approach. The European Union is advancing both a digital euro and a comprehensive regulatory framework for stablecoins under the Markets in Crypto-Assets (MiCA) regulation. The EU’s vision is one of coexistence: a sovereign digital euro for domestic payments and monetary sovereignty, alongside regulated private stablecoins operating under strict prudential standards. This dual-track approach reflects Europe’s more cautious stance toward private money and its determination to preserve strategic autonomy in payments. China, meanwhile, is pursuing the most aggressive CBDC strategy of any major economy, viewing the digital yuan as both a tool of domestic financial modernization and a potential instrument for challenging dollar dominance in international trade and finance.

Geopolitics and the Future of Money

The competition between CBDCs and stablecoins is not merely a technological or regulatory debate. It is a geopolitical contest over the architecture of the future global monetary system. The current dollar-based system, built around the correspondent banking network and the SWIFT messaging system, has served as the backbone of international finance for decades. But this system is increasingly seen as inefficient, exclusionary, and vulnerable to weaponization through sanctions.

CBDCs and stablecoins offer alternative architectures. A network of interoperable CBDCs, such as the mBridge platform linking China, Hong Kong, Thailand, and the UAE, could enable cross-border payments that bypass the dollar-based correspondent banking system entirely. If scaled, such networks could reduce global demand for dollars as a vehicle currency and erode the dollar’s privileged position. Stablecoins, by contrast, reinforce dollar dominance by creating a global, digital-native dollar that operates outside the traditional banking system but remains ultimately tethered to U.S. monetary policy and regulatory oversight. The U.S. policy of promoting dollar-backed stablecoins while banning a sovereign CBDC is a deliberate choice to extend dollar influence through private rather than public channels.

This dynamic has profound implications for global financial flows and the balance of payments. Countries that successfully deploy CBDCs may gain new tools for monitoring capital flows, enforcing capital controls, and insulating their economies from external shocks. Stablecoin adoption, meanwhile, accelerates dollarization in emerging markets, potentially undermining the effectiveness of domestic monetary policy. Central bankers in developing economies face a difficult choice: embrace stablecoins and cede monetary control, or accelerate CBDC development and risk falling behind in the digital payments race.

The monetary policy implications are equally significant. A widely adopted retail CBDC would give central banks new tools for implementing policy, including the ability to pay interest directly on digital balances, implement negative rates without physical cash constraints, and execute helicopter drops of stimulus directly to citizens. Stablecoins, by contrast, operate largely outside the direct control of central banks, potentially complicating the transmission of monetary policy. If a significant share of dollar-denominated transactions migrates to stablecoins issued by non-bank entities, the Federal Reserve’s ability to influence financial conditions through traditional interest rate channels could be diminished.

The Economics Behind the Headlines

Key Takeaway and Conclusion

The battle between CBDCs and stablecoins is not a zero‑sum contest. Both forms of digital money will likely coexist, each serving distinct functions within an increasingly complex global financial system. CBDCs will likely dominate domestic retail payments in countries with strong central bank credibility and advanced digital infrastructure. Stablecoins will continue to thrive in cross‑border payments, crypto‑native finance, and markets where access to dollar banking is constrained. The real question is not which form of digital money will “win” but how the boundaries between them will be drawn and who will set the rules.

The United States has made a decisive strategic choice: no retail CBDC for the foreseeable future, but a robust regulatory framework for dollar‑backed stablecoins that effectively extends the dollar’s global reach through private channels. Europe is pursuing a dual‑track approach, advancing the digital euro while regulating stablecoins under MiCA. China is betting heavily on the digital yuan as a tool for domestic modernization and international influence. The rest of the world is watching, experimenting, and adapting.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.