Why do people buy lottery tickets when the odds of winning are astronomically low? Why do they pay more for insurance than the expected value of the loss they are insuring against? Why does a gambler who is ahead take greater risks, while one who is behind becomes timid? And why do we feel the pain of losing $100 far more acutely than the pleasure of gaining the same amount?

These questions haunted economists for decades. The standard theory of rational choice, built on the foundations of expected utility, offered elegant mathematical answers but struggled to explain how people actually behave. Enter Daniel Kahneman and Amos Tversky. Their collaboration, beginning in the late 1960s, would fundamentally alter how economists understand decision‑making under uncertainty, earning Kahneman the Nobel Prize in 2002 and launching the field of behavioural economics.

Their most enduring contribution, prospect theory, provided a systematic account of how people evaluate risky prospects. It showed that the way choices are framed, the reference point from which gains and losses are measured, and the psychological weights people assign to probabilities all matter in ways that traditional theory could not capture.

What Did Economists Believe?

For decades, the dominant framework for understanding decision‑making under uncertainty was expected utility theory. First formulated by Daniel Bernoulli in 1738 and later axiomatized by John von Neumann and Oskar Morgenstern in 1944, expected utility theory posits that individuals make choices by maximizing the expected value of a utility function. In its simplest form, the value of a gamble that offers outcome \(x\) with probability \(p\) and outcome \(y\) with probability \(1-p\) is:

U(x,p,y) = p\,u(x) + (1-p)\,u(y)

$$

where \(u\) is a concave utility function that captures diminishing marginal utility of wealth. The concavity of \(u\) explains risk aversion: people prefer a sure thing to a gamble with the same expected value.

Expected utility theory was elegant, mathematically tractable, and normatively appealing. It became the foundation of modern microeconomics, finance, and game theory. Yet from its earliest days, there were cracks in the edifice. In 1953, Maurice Allais presented a famous paradox showing that people systematically violate the independence axiom of expected utility. Consider two pairs of gambles:

- Choice A: $100 with certainty vs. a gamble offering $500 with probability 0.10, $100 with probability 0.89, and $0 with probability 0.01.

- Choice B: A gamble offering $500 with probability 0.10 and $0 with probability 0.90 vs. a gamble offering $100 with probability 0.11 and $0 with probability 0.89.

Most people choose the sure thing in the first pair but the risky gamble in the second, a pattern that violates expected utility theory. Allais’s paradox was treated as a curiosity for decades, but it pointed to a deeper truth: people do not treat probabilities linearly, and they are particularly sensitive to the difference between certainty and near‑certainty.

Kahneman and Tversky took these anomalies seriously. They set out to build a descriptive theory that could explain not only Allais’s paradox but a host of other puzzles about how people make decisions under risk.

Kahneman and Tversky

Daniel Kahneman was born in Tel Aviv in 1934 and grew up in France before moving to Israel. He earned his PhD in psychology from the University of California, Berkeley, in 1961 and returned to Israel to teach at the Hebrew University of Jerusalem. Amos Tversky was born in Haifa, Israel, in 1937. He also earned his PhD in psychology from the University of Michigan and joined the Hebrew University faculty. The two met in the late 1960s and began a collaboration that would become legendary.

Their partnership was remarkable not only for its intellectual productivity but also for its complementary nature. Kahneman described himself as the pessimist, Tversky as the optimist. Kahneman was drawn to puzzles about judgment and decision‑making; Tversky was a master of mathematical rigour and experimental design. Together, they produced a series of papers that revolutionized psychology and, eventually, economics.

Their first major breakthrough came in 1974 with a paper in Science titled “Judgment under Uncertainty: Heuristics and Biases.” They identified systematic mental shortcuts, heuristics, that people use to make judgments, and the biases that these shortcuts produce. This work established them as leading figures in cognitive psychology.

But it was their 1979 paper, “Prospect Theory: An Analysis of Decision under Risk,” published in Econometrica, that would have the most profound impact on economics. The paper laid out a new model of choice under uncertainty that departed from expected utility in three fundamental ways:

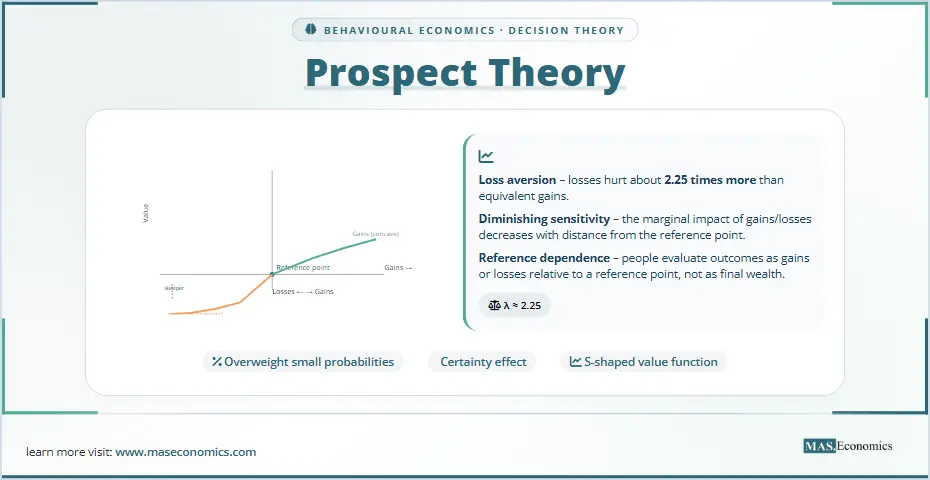

- Reference dependence: Utility is defined over gains and losses relative to a reference point, not over final states of wealth.

- Diminishing sensitivity: The value function is concave for gains and convex for losses, meaning that the marginal impact of a change diminishes with distance from the reference point.

- Loss aversion: The value function is steeper for losses than for gains; losses loom larger than equivalent gains.

Tversky died in 1996. Kahneman was awarded the Nobel Prize in Economic Sciences in 2002 for their work, a prize that Tversky would have shared had he been alive. In his Nobel lecture, Kahneman paid tribute to their collaboration: “Amos Tversky and I were both fortunate to have found in each other a mind that was interested in the same problems, a mind that was good enough to catch mistakes and to provide excellent ideas, and a mind that was sufficiently different to make the collaboration exciting.”

The Core Idea Explained

Prospect theory begins with a simple observation: people think about outcomes as gains and losses relative to a reference point, not as absolute levels of wealth. This reference point is typically the status quo, but it can also be shaped by expectations, social comparisons, or framing.

Consider a simple gamble: a 50% chance to win $100 and a 50% chance to lose $100. In expected utility theory, the value of this gamble depends on the curvature of the utility function over final wealth. But in prospect theory, the value depends on the shape of the value function over gains and losses.

The Value Function

Kahneman and Tversky proposed a value function with three key properties:

- Reference dependence: The function is defined over deviations from a reference point, denoted as \(x\) for gains and \(-x\) for losses. The reference point is usually the status quo, but it can shift.

- Diminishing sensitivity: The marginal value of gains decreases as they get larger, and the marginal disvalue of losses also decreases as they get larger. This implies that the value function is concave for gains and convex for losses. In mathematical terms:

v(x) = x^\alpha \quad \text{for } x \ge 0

$$

v(x) = -\lambda (-x)^\beta \quad \text{for } x < 0

$$

where \(\alpha\) and \(\beta\) are parameters between 0 and 1, and \(\lambda > 1\) is the coefficient of loss aversion.

- Loss aversion: The function is steeper for losses than for gains. Empirically, \(\lambda\) is typically around 2.25, meaning that the pain of losing $100 is about 2.25 times the pleasure of gaining $100.

The S‑shaped value function has a kink at the origin: a small loss feels much worse than a small gain feels good.

The Weighting Function

The second innovation of prospect theory is the probability weighting function. People do not treat probabilities linearly. Instead, they overweight small probabilities and underweight moderate and high probabilities. The weighting function \(\pi(p)\) has the following properties:

- \(\pi(p) > p\) for small \(p\) (overweighting of rare events)

- \(\pi(p) < p\) for moderate and large \(p\) (underweighting)

- The function is not linear, and it exhibits a “certainty effect”: the difference between probability 0.99 and 1.0 looms larger than the difference between 0.50 and 0.51.

A common functional form, proposed by Tversky and Kahneman (1992), is:

\pi(p) = \frac{p^\gamma}{\bigl(p^\gamma + (1-p)^\gamma\bigr)^{1/\gamma}}

$$

with \(\gamma \approx 0.65\) for gains and 0.69 for losses.

The weighting function explains why people both buy lottery tickets (overweighting the small chance of a big win) and buy insurance (overweighting the small chance of a large loss).

The Prospect Theory Equation

Putting these together, the value of a prospect \((x, p; y, q)\) is:

V = \pi(p) v(x) + \pi(q) v(y)

$$

where \(v\) is the value function and \(\pi\) is the weighting function. When choosing between gambles, people select the one with the highest \(V\).

A MASEconomics Example

Consider a Pakistani household deciding whether to buy earthquake insurance for their home. The probability of a damaging earthquake in a given year is 1 in 1,000. If an earthquake occurs, the damage is estimated at $5,000,000. The insurance premium is $10,000 per year.

In expected utility theory, a rational risk‑averse person might or might not buy insurance depending on the curvature of their utility function. But prospect theory offers a different explanation. The decision is framed as a choice between:

- A certain loss of $10,000 (the premium)

- A gamble with a 0.001 probability of losing $5,000,000 and a 0.999 probability of losing nothing

The small probability of a large loss is overweighted, making the gamble seem much worse than its expected value. The household buys insurance not because they are risk‑averse in the expected utility sense, but because the weighting function magnifies the fear of the unlikely catastrophe.

This same logic explains why people buy lottery tickets. A small chance of a large gain is overweighted, making the gamble seem more attractive than its expected value.

From Prospect Theory to Cumulative Prospect Theory

The original version of prospect theory was limited to gambles with at most two non‑zero outcomes. In 1992, Tversky and Kahneman published “Advances in Prospect Theory: Cumulative Representation of Uncertainty,” which extended the theory to any number of outcomes and to uncertain as well as risky prospects.

The key innovation was the cumulative weighting function, which transforms the cumulative distribution rather than individual probabilities. This ensures that the model respects stochastic dominance, a property the original version did not always satisfy. The cumulative version also allows different weighting functions for gains and losses, capturing the fact that people treat probabilities differently in the two domains.

The cumulative prospect theory value of a prospect with outcomes \(x_{-m}, \dots, x_n\) (ordered from worst to best) is:

V = \sum_{i=-m}^{n} \pi_i v(x_i)

$$

where the decision weights \(\pi_i\) are derived from the cumulative probabilities, and where the weighting functions for gains and losses can differ.

Myopic Loss Aversion and the Equity Premium Puzzle

One of the most influential applications of prospect theory in finance comes from Shlomo Benartzi and Richard Thaler (1995). They introduced the concept of myopic loss aversion to explain the equity premium puzzle, the fact that stocks have historically earned a much higher return than bonds, implying that investors are extremely averse to risk.

Consider an investor choosing between stocks and bonds. If the investor evaluates her portfolio frequently, she will experience many losses (since stocks go down about half the time on a daily basis). Loss aversion makes these losses painful, so she demands a high premium to hold stocks. But if she evaluates her portfolio only once a year, she will experience fewer losses, and the required premium will be lower.

Benartzi and Thaler showed that with the loss aversion parameter estimated from experimental studies (\(\lambda \approx 2.25\)), the historical equity premium can be explained if investors evaluate their portfolios about once a year, a plausible evaluation period. This combination of loss aversion and frequent evaluation is what they called myopic loss aversion.

Is Prospect Theory Normative?

Prospect theory is a descriptive theory; it aims to explain how people actually behave, not how they should behave. This raises a normative question: should policymakers and decision analysts use prospect theory to guide decisions? The answer is nuanced.

One line of criticism argues that the deviations from rationality captured by prospect theory are errors that people would correct if they had better information or more time to think. In this view, the normative benchmark remains expected utility theory, and the goal of policy should be to help people overcome their biases.

But Kahneman and Tversky were careful to distinguish between two types of utility: decision utility (the utility inferred from choices) and experienced utility (the actual hedonic experience of outcomes). They argued that prospect theory may better capture experienced utility because it reflects the way people actually perceive gains and losses. A loss of $100 truly feels worse than a gain of $100 feels good, and a truly rational person would take this into account.

A related critique comes from the observation that the parameters of prospect theory, the degree of loss aversion, the curvature of the value function, and the shape of the weighting function vary across individuals and contexts. There is no single set of parameters that describes everyone. This complicates applications, but it does not invalidate the theory as a description of average behaviour.

Perhaps the most fundamental challenge is that prospect theory, like expected utility theory, assumes that people have well‑defined preferences over gambles. Yet as Kahneman and Tversky themselves showed, preferences can be manipulated by framing. This suggests that preferences are not stable but are constructed in the process of decision‑making. This insight has led to a deeper critique of the entire rational‑choice framework, one that goes beyond prospect theory to question whether the concept of utility is even meaningful.

Nudges, Policy, and Beyond

Perhaps the most visible impact of prospect theory has been in the domain of public policy. The insights of Kahneman and Tversky inspired Richard Thaler and Cass Sunstein to develop the concept of nudges, small changes in the choice architecture that can steer people toward better decisions without restricting their freedom.

The Nudge Revolution

Thaler and Sunstein’s 2008 book, Nudge: Improving Decisions About Health, Wealth, and Happiness, drew directly on prospect theory. The key insight is that because people are influenced by framing, default options, and reference points, policymakers can use these insights to design environments that make it easier for people to make good choices.

Examples of nudges include:

- Automatic enrollment: Instead of requiring employees to opt into retirement savings plans, automatically enroll them and allow them to opt out. This uses the status quo bias (a form of loss aversion) to increase savings rates.

- Salient information: Presenting energy consumption information in a way that compares a household’s usage to neighbours’ usage has been shown to reduce energy consumption.

- Default options: Organ donation rates are much higher in countries where the default is to be a donor (opt‑out) than where the default is not to be a donor (opt‑in).

Governments around the world have established “nudge units” to apply these insights. The UK’s Behavioural Insights Team, founded in 2010, was the first, followed by similar units in the US, Australia, Germany, and many other countries. These teams have applied prospect theory to everything from tax compliance to public health.

Health and Dietary Choices

One of the most active areas of nudge research is health and dietary choices. Studies have shown that placing healthier foods at eye level in cafeterias, reducing portion sizes, and using smaller plates can significantly influence what people eat. These interventions leverage the reference‑point effects and salience that are central to prospect theory.

Financial Decision‑Making

In finance, prospect theory has been used to design better products. For example, the “Save More Tomorrow” program, developed by Thaler and Shlomo Benartzi, allows employees to commit in advance to saving a portion of future raises. This uses loss aversion (people are reluctant to reduce current take‑home pay) and the reference‑point effect (future raises are perceived as gains, making it easier to allocate part of them to savings).

Critiques of Nudging

Despite its popularity, the nudge approach has critics. Some argue that nudges are paternalistic and that governments should not manipulate citizens’ choices, even for their own good. Others argue that nudges are too weak to solve major problems like climate change or inequality, and that more substantial regulation is needed. Still others point out that the effectiveness of nudges often declines over time as people adapt.

Nevertheless, the nudge agenda has transformed how policymakers think about behavioural interventions. It has also created a bridge between academic research and practical policy, demonstrating that insights from psychology and economics can be applied to real‑world problems.

Prospect Theory in the Age of AI

As artificial intelligence and machine learning become more pervasive, prospect theory is finding new applications. Algorithms that make recommendations, whether for movies, products, or medical treatments, are themselves a form of choice architecture. Understanding how people respond to framing and defaults is essential for designing AI systems that serve human values.

Moreover, as machines take over more decisions, the question of how to incorporate human preferences into algorithmic decision‑making becomes increasingly urgent. Prospect theory offers a language for describing those preferences that may be more realistic than the rational‑choice framework.

Why Does Prospect Theory Still Matter?

More than four decades on, prospect theory remains the leading alternative to expected utility theory, reshaping how economists think about risk, how governments and officials design interventions, and how we understand choice. Its endurance rests on three things: it captures robust, replicable patterns such as loss aversion, the certainty effect, and overweighting of small probabilities; it is flexible enough to be applied across fields like finance and public health; and it connects to deeper psychological and evolutionary principles, such as sensitivity to changes near a reference point and the urgency of avoiding harm.

Yet it is not the final word; researchers continue to refine it and explore its limits. We are not the rational calculators classical economics once imagined. We are influenced by framing, reference points, and loss aversion, and understanding these tendencies can help us make better decisions while enabling governments and officials to design environments that support us in doing so.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.