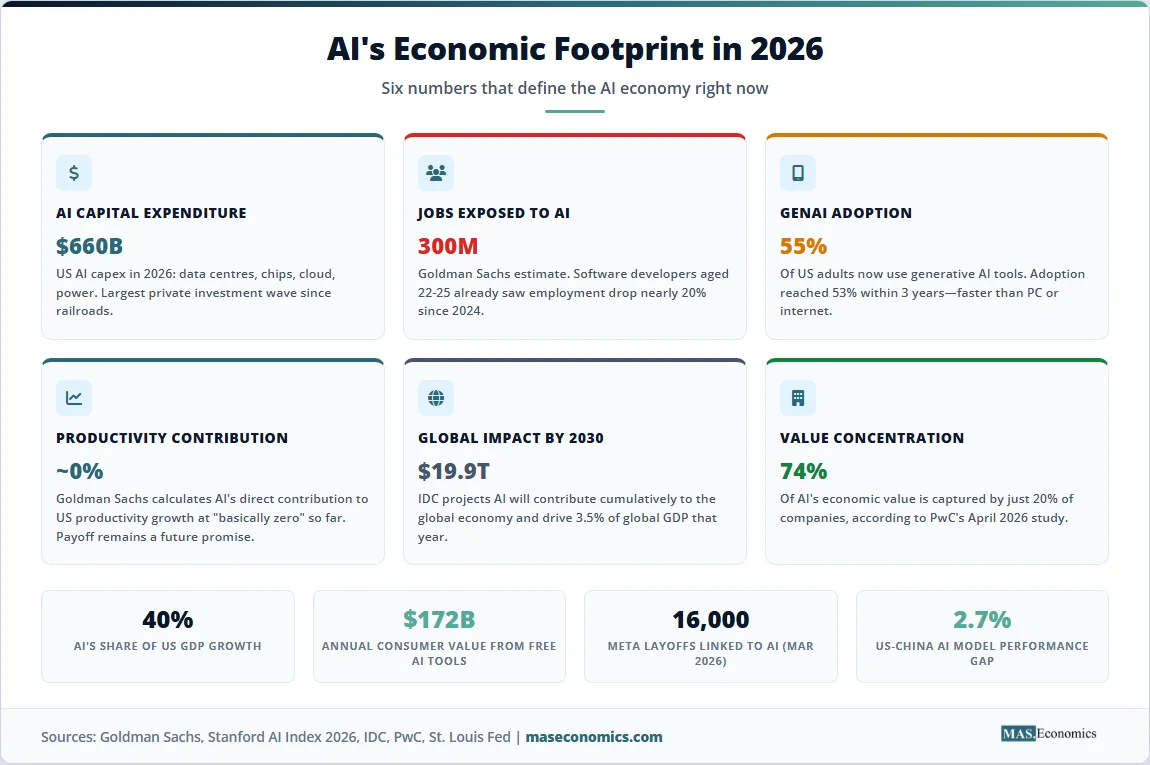

AI and the economy are now inseparable. In 2026, US firms will spend an estimated $660 billion on artificial intelligence infrastructure: data centres, semiconductors, cloud computing, and the power systems to run them. That figure, drawn from corporate capital expenditure filings compiled by multiple analysts, represents the largest private investment wave in a single technology since the construction of the American railroad network in the 19th century. AI-related investment is now driving approximately 40% of US GDP growth, according to estimates from Goldman Sachs.

And yet, when Goldman’s economists calculated how much AI has contributed to actual US productivity growth, the answer was striking: “basically zero.” The St. Louis Federal Reserve confirmed that while AI investment has surpassed the contribution of IT components during the dot-com boom in both levels and share of GDP, the productivity gains that would justify this spending have not yet materialised in macroeconomic data.

This is the central paradox of AI and the economy in 2026: the investment is real, massive, and measurable, but the productivity payoff remains a future promise rather than a present reality. Whether that promise is fulfilled will determine whether the AI boom becomes the foundation of a new era of growth or the largest misallocation of capital in modern economic history.

Latest Developments

Table 1: AI and the Economy – Key Events Timeline

| Date | Event |

|---|---|

| Feb 2025 | DeepSeek-R1 (China) briefly matches top US AI model performance, narrowing US-China gap to 2.7% |

| Q3 2025 | US investment in information-processing equipment and software grows 16.5% year-over-year (BEA) |

| Aug 2025 | Generative AI adoption reaches 55% of US population and 37% of workers (Stanford AI Index) |

| Oct 2025 | Meta cuts 600 AI unit roles; cites internal AI productivity monitoring dashboards |

| Jan 2026 | St. Louis Fed confirms AI investment has surpassed dot-com era IT contribution to GDP |

| Feb 2026 | Goldman Sachs calculates AI’s direct contribution to US productivity at “basically zero” |

| Mar 2026 | Meta announces 16,000 layoffs linked to $600B AI capex plan through 2028 |

| Apr 2026 | Stanford AI Index 2026: entry-level software developer employment down nearly 20% since 2024 |

| Apr 2026 | PwC study: 74% of AI’s economic value captured by just 20% of companies |

|

|

Sources: St. Louis Federal Reserve, Stanford HAI AI Index 2026, PwC, Goldman Sachs.

The Economics of AI: Investment, Productivity, and the J-Curve

Understanding AI and the economy requires distinguishing between three channels through which AI affects economic growth.

The investment channel is the most visible. When Microsoft builds a $10 billion data centre, that spending shows up immediately in GDP as nonresidential fixed investment. The steel, concrete, copper wiring, cooling systems, and construction labour all generate economic activity. The servers, GPUs, and networking equipment purchased from NVIDIA, AMD, and others add further. The St. Louis Fed’s analysis shows that software, R&D, information processing equipment, and data centre construction collectively contributed more to real GDP growth in 2025 than IT components did at the peak of the dot-com boom. This is the channel that accounts for AI driving approximately 40% of US GDP growth.

The productivity channel is where the promise lies. General-purpose technologies like electricity, the internal combustion engine, and the internet eventually raised output per worker across the economy. AI has the same potential. Economists Erik Brynjolfsson, Daniel Rock, and Chad Syverson have theorised a “Productivity J-Curve”: new general-purpose technologies initially require massive complementary investments (in training, reorganisation, new processes) before productivity gains materialise. The dot-com era showed a similar pattern: massive IT investment in the 1990s produced measurable productivity gains only from 1995 to 2005, with a significant lag.

This framework explains the paradox. The AI productivity paradox is not evidence that AI does not work. It may be evidence that the complementary investments, organisational changes, and skill adaptations required to unlock AI’s productivity potential are still in their early stages. As the IMF noted, “the most compelling economic effects of AI are still likely to come from productivity gains and organisational change rather than from capital spending itself.”

The displacement channel is where AI’s economic impact becomes most contentious. AI does not merely augment human workers; in certain tasks and roles, it replaces them. The economics of automation follows a pattern that Joseph Schumpeter described as “creative destruction”: new technologies destroy existing jobs while creating new ones. The question is whether the creation keeps pace with the destruction, and whether the workers displaced can transition to the new roles.

The AI Investment Boom in Data

The scale of AI-related investment in 2026 is unprecedented. The chart below compares the estimated AI capital expenditure of the five largest US technology companies, illustrating the concentration of spending.

Source: Corporate filings, Goldman Sachs Research, DWU Consulting. Estimated 2026 AI-related capital expenditure in billions of USD. Figures include data centres, cloud infrastructure, chip purchases, and related R&D.

The concentration is striking. Five companies account for the majority of AI-related capital spending globally. Meta alone plans to invest $120 billion as part of a $600 billion AI infrastructure plan through 2028. This concentration has macroeconomic consequences: if even one of these companies pulls back on spending, the impact on GDP growth would be measurable. JPMorgan analysts have described the current phase as “Hyper-Capex,” which will eventually need to justify itself through measurable efficiency gains in the broader economy.

The Centre for Economic Policy Research (CEPR) has provided one of the most rigorous assessments, noting that AI’s macroeconomic footprint rests on three interdependent actors: hardware vendors (NVIDIA, AMD, TSMC), cloud infrastructure providers (AWS, Azure, Google Cloud), and AI labs (OpenAI, Anthropic, Google DeepMind). The health of the entire ecosystem depends on each layer functioning, and a disruption at any level can cascade through the economy.

The Labour Market Impact

The Stanford AI Index 2026 report, published on April 8, 2026, contains the most detailed evidence yet of how AI is reshaping the labour market. The findings are nuanced and worth examining carefully.

Employment among software developers aged 22 to 25 has fallen nearly 20% since 2024, even as employment among older developers continues to grow. The pattern repeats across other roles with high AI exposure, including customer service, translation, and data analysis. Firm surveys indicate that executives expect this trend to accelerate, with planned headcount reductions outpacing recent cuts. As the Stanford report summarised: “The disruption is targeted and just beginning.”

Meta’s March 2026 announcement of 16,000 layoffs, explicitly linked to its AI capital expenditure plan, marked an inflection point. Unlike previous tech layoffs driven by market downturns or missed targets, Meta’s cuts were driven by measured productivity displacement identified through internal AI monitoring systems. The company’s willingness to publish this rationale represented a new level of transparency about AI-driven job replacement.

Goldman Sachs has estimated that 300 million jobs globally are exposed to AI automation. The word “exposed” is important: it does not mean these jobs will disappear. It means that a significant portion of the tasks within these roles can be performed by AI. As our article on AI as a factor of production explores, the historical pattern of technological disruption has been that new technologies transform jobs rather than eliminate them entirely, though the transition period can be extremely painful for affected workers.

The displacement is concentrated. The PwC 2026 AI Performance Study, published on April 13, found that 74% of AI’s economic value is captured by just 20% of companies. These leading firms are not simply deploying more AI tools; they are using AI as a catalyst for business reinvention. The remaining 80% of firms are largely still in “pilot mode.” This concentration of gains has profound implications for income inequality: the benefits of AI accrue disproportionately to capital owners and highly skilled workers, while the costs fall on entry-level knowledge workers and routine-task employees.

The labour mismatch is growing. Demand for data centre technicians, power engineers, AI researchers, and semiconductor specialists is intense, driving wage growth of 30 to 50% in these fields. Meanwhile, workers displaced from knowledge-work roles face a skills gap that traditional retraining programmes have not yet bridged. As we explored in The Future of Work, this mismatch between declining and growing occupations is one of the defining structural challenges of the AI transition.

The US-China AI Race and Global Implications

The geopolitics of AI is inseparable from its economics. The Stanford AI Index 2026 confirms that China has nearly erased the US lead in AI model performance. US and Chinese models have traded places at the top of performance rankings multiple times since early 2025. As of March 2026, the gap between the leading US model and the leading Chinese model is just 2.7%.

The two countries lead in different dimensions. The US produces more top-tier AI models and higher-impact patents, while China leads in publication volume, citations, total patent output, and industrial robot installations. The US is home to the most AI researchers by far, but the flow of AI talent into the country is slowing dramatically, partly due to immigration policy changes.

US export controls on advanced semiconductors (restricting NVIDIA and AMD chip sales to Chinese companies) and the Dutch government’s restrictions on ASML lithography equipment are designed to slow China’s AI development. China has responded by investing heavily in domestic chip production and developing more efficient models that require less advanced hardware. DeepSeek-R1, a Chinese model that matched US frontier performance in February 2025, demonstrated that the US chip advantage can be partially offset by algorithmic innovation.

For emerging markets, the AI revolution creates a bifurcation identified by the IMF and the Institute of International Finance: economies with “digital depth” (the ability to produce and export digital goods, not just consume imported tools) attract stable foreign direct investment linked to AI-era production. Economies with only “digital participation” remain consumers of imported technology, vulnerable to volatile capital flows. This distinction may become as important as fiscal credibility or exchange-rate regime stability in determining which countries thrive in the AI era.

Scenarios for AI and the Economy

Table 2: AI Economic Impact Scenarios (2026 – 2030)

| Scenario | What Happens | Economic Impact |

|---|---|---|

| Productivity breakthrough (Bull) | AI diffuses broadly across industries; complementary investments in training and reorganisation pay off; productivity gains materialise | US GDP growth approaches 3%+; real wages rise; global growth lifts; AI contributes 3.5% of global GDP by 2030 (IDC projection) |

| Slow diffusion (Base) | AI gains remain concentrated in 20% of firms; investment continues but productivity payoff is gradual; J-Curve plays out over 5 – 10 years | GDP growth supported by capex but not by broad productivity; inequality widens; labour market disruption accelerates in specific sectors |

| Capex fatigue / bubble (Bear) | Hyperscalers pull back on spending before productivity gains justify costs; AI stock valuations correct; data centre construction slows | GDP growth decelerates sharply as the 40% AI contribution to growth evaporates; tech sector employment declines further; parallels to dot-com bust |

|

|

||

Sources: IMF, IDC, Vanguard, Goldman Sachs.

MASEconomics Explains

Four economic concepts behind AI and the economy

Automation and Labour Displacement

Automation is the replacement of human labour with machines or software. AI represents a new wave of automation that extends beyond physical tasks (which earlier machines automated) into cognitive and creative work. The economic impact depends on whether displaced workers can transition to new roles. When they cannot, the result is structural unemployment, a persistent mismatch between workers’ skills and available jobs.

Creative Destruction

Joseph Schumpeter coined this term to describe how innovation destroys existing industries while creating new ones. The automobile destroyed the horse-drawn carriage industry but created the automotive, petroleum, and highway construction industries. AI is following the same pattern: destroying entry-level knowledge work while creating demand for data centre technicians, AI engineers, and power infrastructure specialists. The net effect on employment depends on the speed and scale of both processes.

General Purpose Technology (GPT)

A general purpose technology is one that transforms multiple industries and sectors across the economy. Electricity, the internal combustion engine, and the internet are historical examples. AI qualifies because it can enhance productivity in virtually every sector. The economic literature shows that GPTs follow a predictable pattern: massive early investment, a productivity lag (the J-Curve), and then broad-based gains once complementary investments and organisational changes catch up. The productivity payoff from electricity took approximately 30 years.

Structural Unemployment

Structural unemployment occurs when workers’ skills do not match the requirements of available jobs. Unlike cyclical unemployment (which falls when the economy recovers), structural unemployment persists regardless of economic conditions. AI is creating a new form of structural unemployment: experienced knowledge workers whose roles are being automated cannot easily retrain for the highly technical roles that AI creates. The Stanford AI Index 2026 documented this pattern across software development, customer service, and translation.

Explore our full library of AI and economics explainers, from AI as a factor of production to the AI productivity paradox.

Explore the MASEconomics Blog →Conclusion

AI and the economy are locked in a relationship defined by extraordinary investment, concentrated gains, and unresolved contradictions. The $660 billion in AI capital expenditure is real and is driving a significant share of US economic growth. But the productivity payoff that would justify this spending has not yet appeared in the macroeconomic data. Entry-level knowledge workers are losing jobs to AI at a measurable rate, while the benefits accrue to a small number of firms and highly skilled specialists. The US-China AI competition is intensifying, with the performance gap between frontier models narrowing to less than 3%.

Whether AI becomes the foundation of a new era of broad-based prosperity, or a technology that enriches capital owners while displacing workers, depends on decisions being made right now: in corporate boardrooms choosing whether to invest in retraining or simply in replacement; in legislatures debating regulation, taxation, and social safety nets; and in educational institutions racing to close the skills gap between what AI eliminates and what it creates. The economics of AI is no longer a theoretical discussion. It is the defining structural story of the global economy in 2026.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.