In 1987, Nobel Prize-winning economist Robert Solow made an observation that haunted the technology industry for a decade. “You can see the computer age everywhere,” he wrote, “but in the productivity statistics.” Businesses were spending billions on personal computers, corporate networks, and database systems, yet aggregate productivity growth remained stubbornly flat. It took another eight years before the information technology revolution finally showed up in the macroeconomic data, triggering the spectacular productivity boom of 1995 to 2005.

Nearly four decades later, the same paradox has returned, and this time the numbers are far more dramatic.

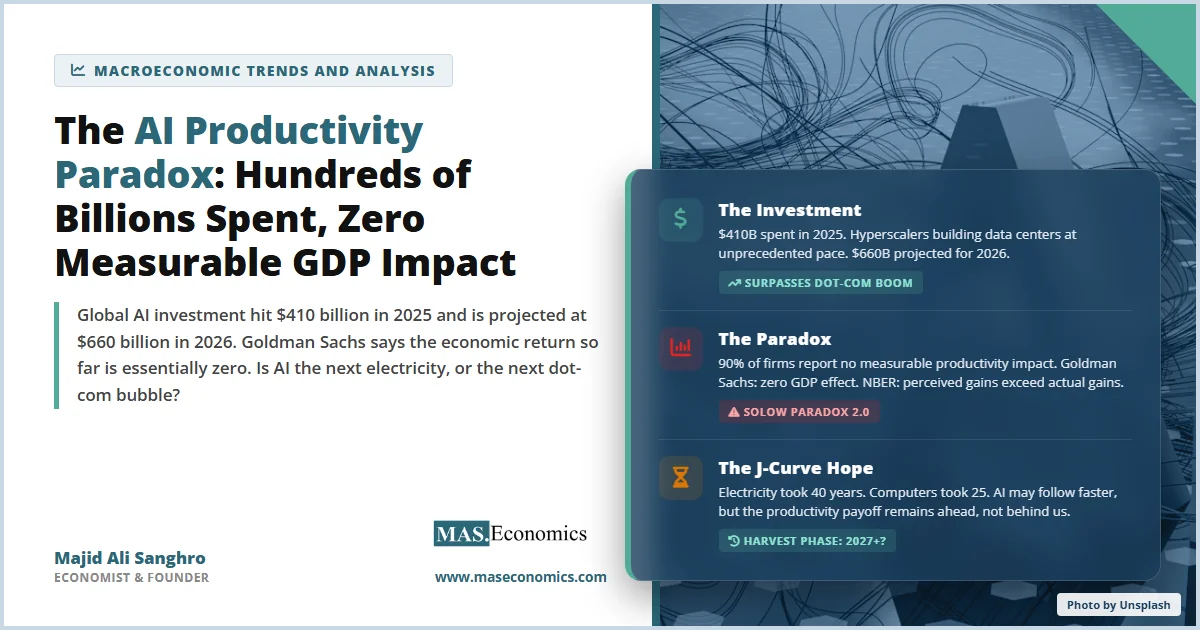

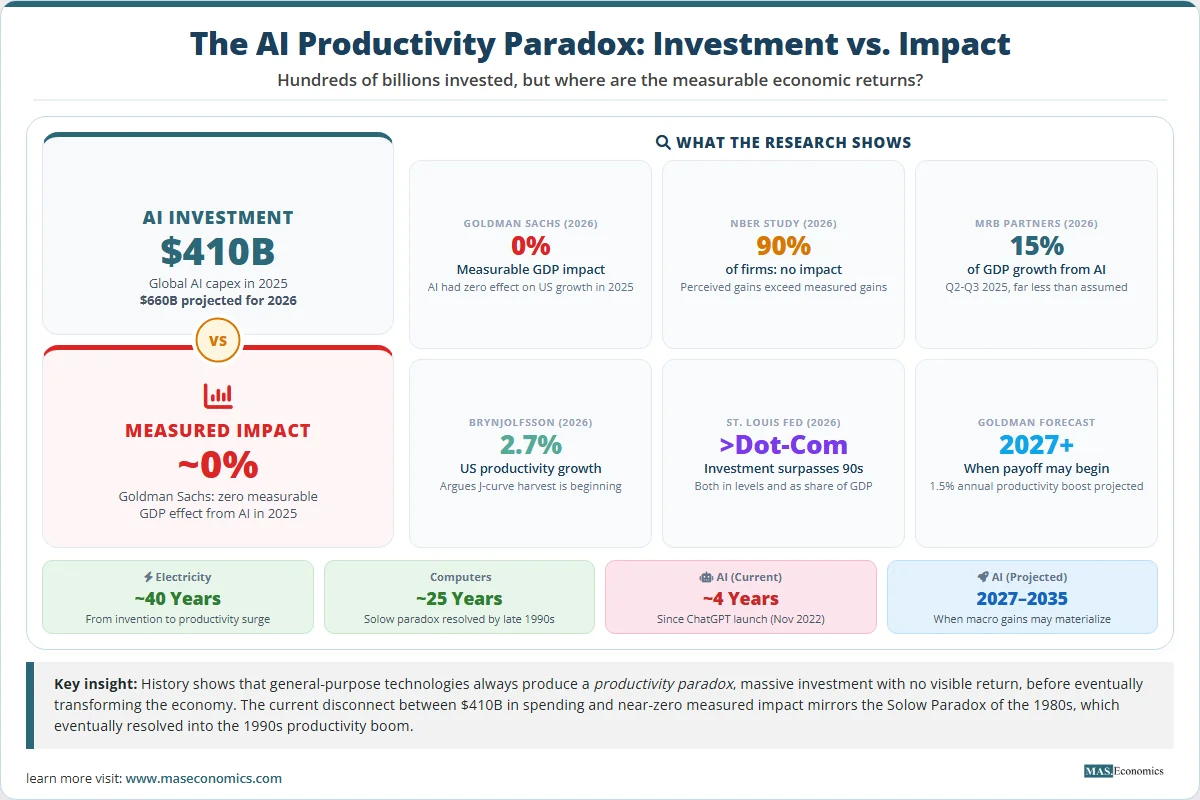

Global businesses spent approximately $410 billion on artificial intelligence in 2025. Hyperscalers like Nvidia, Microsoft, Amazon, Alphabet, and Meta poured record sums into data centers, chips, and AI infrastructure. Harvard economist Jason Furman calculated that AI-related investment accounted for a staggering 92% of US GDP growth in the first half of 2025. Yet when Goldman Sachs analysts looked at the actual economic output generated by all that spending, their conclusion was stark: AI has had zero measurable impact on US economic growth.

Meanwhile, a February 2026 study by the National Bureau of Economic Research, surveying nearly 6,000 CEOs and CFOs across the US, UK, Germany, and Australia, found that the vast majority reported little impact from AI on their operations. Ninety percent of firms saw no measurable productivity improvement. Perceived gains consistently exceeded measured gains, a phenomenon the researchers explicitly labeled a “productivity paradox.”

The Scale of AI Investment

To appreciate the paradox, you first need to understand the sheer scale of what is being spent. AI-related capital expenditure in 2025 was not just large by historical standards. It was unprecedented.

The St. Louis Federal Reserve published a detailed analysis in January 2026 tracking AI’s contribution to GDP growth. The researchers found that AI-related investment categories, including information-processing equipment, software, research and development, and data center construction, contributed significantly to real GDP growth in 2025. More importantly, this investment has already surpassed the contribution of IT components during the dot-com boom, both in absolute levels and as a share of GDP.

The numbers are staggering. NVIDIA’s Data Center segment alone reported approximately $115 billion in revenue for 2025. TSMC committed $165 billion to its Arizona semiconductor complex. Investors are projected to spend $660 billion on AI by 2026. The five largest US technology companies, sometimes called the “hyperscalers,” collectively spent more on AI infrastructure in a single year than the entire GDP of most countries.

Yet for all this spending, the macroeconomic return has been, to put it diplomatically, elusive.

| Source | Key Finding | Date | Implication |

|---|---|---|---|

| Goldman Sachs | AI had zero measurable effect on US GDP in 2025 | March 2026 | Investment boom without economic return |

| NBER (6,000 CEOs) | 90% of firms report no productivity impact from AI | February 2026 | Perceived gains exceed measured gains |

| MRB Partners | AI accounted for only 15% of GDP growth in Q2-Q3 2025 | January 2026 | Consumer spending, not AI, drove growth |

| ManpowerGroup | AI use up 13%, but confidence in AI down 18% | 2026 | Workers using AI more but trusting it less |

| Erik Brynjolfsson | US productivity grew 2.7% in 2025; J-curve harvest beginning | February 2026 | The optimistic counter-argument |

| Goldman Sachs Forecast | AI could boost productivity 1.5% annually starting 2027 | 2025 | Long-run payoff may still materialise |

|

|||

The Paradox Explained

How is it possible to spend $410 billion and get nothing back in the aggregate statistics? The answer involves three structural issues that traditional economic indicators struggle to capture.

The Import Leakage Problem

GDP measures domestic production. When a US company buys Nvidia chips manufactured by TSMC in Taiwan, that purchase boosts Taiwan’s GDP, not America’s. MRB Partners analyst Shilpa Bhide found that without adjusting for imports, AI-related components appeared to add roughly 0.9 percentage points to real GDP growth in 2025, or nearly 40% of total growth. But when adjusted for the real imports of computers, semiconductors, and telecom equipment, the net contribution shrank to just 0.4 to 0.5 percentage points, or 20 to 25% of growth. The rest leaked out to foreign economies that manufactured the hardware.

This is a critical insight for understanding the macroeconomics of AI. Much of what appears as “AI investment” in corporate accounts is actually an import bill that enriches foreign chipmakers and equipment suppliers while adding relatively little to domestic output.

The Measurement Problem

Traditional GDP accounting struggles to measure the value created by digital technologies. When an AI tool helps a software developer write code 50% faster, or enables a customer service team to handle twice as many inquiries, those gains may show up as cost savings within the firm but not necessarily as additional measured output in the national accounts. The methods used to measure national income were designed for an economy of physical goods, not one where a significant share of value is created by intangible digital services.

The NBER study explicitly identified this gap, documenting a “productivity paradox” in which CFO-perceived productivity gains substantially exceeded measured revenue-based gains. The researchers attributed this to “delayed revenue realisations”: firms invest in AI, restructure workflows, and see internal efficiency improvements, but the revenue benefits take months or years to materialise in the data.

The Complementary Investment Problem

This may be the most important factor. AI is a general-purpose technology, meaning it requires extensive complementary investments in organisational restructuring, worker retraining, new business processes, and management practices before it delivers its full productivity potential. Simply buying AI software and plugging it into existing workflows is, as the San Francisco Federal Reserve eloquently put it, “analogous to replacing a steam-powered motor with an electric one but leaving the factory floor unchanged. Good progress, but not transformative.”

The historical analogy is instructive. When electric motors first replaced steam engines in factories, productivity initially declined because manufacturers simply swapped one power source for another without redesigning the factory layout. It was only when Henry Ford and other innovators realised that electricity allowed factories to be organised around the assembly line, rather than around the central power shaft of a steam engine, that the transformative productivity gains materialised. That process took roughly 40 years.

The Historical Pattern

The AI productivity paradox is not unprecedented. It is, in fact, the standard pattern for general-purpose technologies. Every major technological transformation in economic history has followed the same sequence: massive investment, a period of disappointing returns, and then an eventual productivity explosion that transforms the economy.

Electricity was invented in the 1880s but did not produce measurable aggregate productivity gains until the 1920s, roughly 40 years later. Personal computers entered offices in the early 1980s but did not boost productivity until the late 1990s, about 15 to 20 years later. The internet became commercially available in the early 1990s, but its productivity impact was not visible until around 2000.

Stanford economist Erik Brynjolfsson, who has studied this pattern extensively, calls it the “Productivity J-Curve.” During the initial adoption phase, measured productivity actually declines because firms are investing heavily in new technology, hiring specialists, and reorganising workflows, all of which represent costs with no immediate output. Then, after a lag that can last years or decades, the complementary investments pay off and productivity surges.

Source: BLS, BEA, St. Louis Fed, Man Group research (2026). Electricity lag from David (1990); Computer lag from Brynjolfsson & McAfee (2014) | MASEconomics.com

The chart tells the story in two diverging lines. AI investment (the solid blue line) has surged exponentially from $40 billion in 2019 to $410 billion in 2025, with $660 billion projected for 2026. Yet US productivity growth (the dashed red line) has remained essentially flat, hovering between 1.3% and 2.2%, showing no visible acceleration despite the massive investment surge. This is the visual signature of a productivity paradox: the investment line soars while the output line stays flat.

The Optimistic Counter-Argument

Not everyone agrees with the pessimistic reading. Erik Brynjolfsson, writing in the Financial Times in early 2026, argued that the productivity payoff from AI is already becoming visible in the data. He pointed to new Bureau of Labor Statistics benchmark revisions showing total payroll growth revised downward by approximately 403,000 jobs, while real GDP remained robust at 3.7% in Q4 2025. This decoupling of output from labor input, he argued, is the hallmark of productivity growth.

Brynjolfsson’s updated analysis suggested that US productivity grew roughly 2.7% in 2025, nearly double the 1.4% annual average of the past decade. He framed this through the J-curve hypothesis: general-purpose technologies suppress measured productivity during an initial investment phase before entering a “harvest phase” where the gains accelerate.

Similarly, data from the NBER survey of CFOs showed that while current revenue-based productivity gains are modest, executives expect them to roughly double in 2026. High-skill services and finance show the largest projected effects at over 2%, driven primarily by innovation and demand-oriented channels, specifically developing new products and reaching customers more effectively, rather than simple cost reduction.

Former PIMCO CEO Mohamed El-Erian observed that the decoupling of job growth and GDP growth resembles the pattern of the 1990s, when office automation eventually triggered a structural transformation of the labour market. Apollo’s chief economist Torsten Slok described the future impact of AI as a “J-curve” of initial stagnation followed by exponential improvement.

The Skeptical View

On the other side of the debate, a growing number of analysts are drawing uncomfortable parallels to the dot-com era. Goldman Sachs, after months of carefully worded warnings about the dangers of AI over-investment, has now dramatically escalated its rhetoric. The bank’s analysts argue that the massive capital expenditure is generating returns primarily for foreign chipmakers and data center construction companies, not for the broader US economy.

Dario Perkins, head of macroeconomics at consulting firm TS Lombard, agrees that AI’s effects on productivity are nonexistent. He told the Financial Times that “there is no evidence that AI deployment is either boosting productivity or damaging US employment,” adding that “cyclical forces, not automation, are to blame” for recent productivity trends.

The Yale Budget Lab struck a cautious middle ground, warning against reading too much into short-term data. Productivity statistics are “noisy” and subject to large revisions. The strong productivity numbers that Brynjolfsson cited may partly reflect measurement artifacts: GDP data for 2025 has not yet been through annual benchmark revisions, while employment data has. Comparing revised employment figures to unrevised GDP creates a spurious appearance of productivity gains that may evaporate when the GDP data is also revised.

The Man Group’s analysis added another layer of nuance. While AI adoption is tracking ahead of previous technologies at comparable stages, and nonfarm business productivity did increase 4.9% in Q3 2025, “whether AI contributed remains unclear.” History suggests patience is warranted: previous general-purpose technologies took 20 to 40 years to show aggregate productivity impacts.

What This Means for the Global Economy

The AI productivity paradox has consequences that extend far beyond the technology sector.

For Financial Markets

The valuations of major technology companies are implicitly pricing in massive future productivity gains from AI. If those gains fail to materialise, or arrive far more slowly than expected, a significant correction in technology stock valuations becomes more likely. The dot-com bubble offers a precedent: the internet did eventually transform the economy, but not before $5 trillion in market value evaporated between 2000 and 2002.

For Monetary Policy

If AI investment is inflating GDP growth figures without producing genuine productivity gains, then central banks may be setting interest rates based on misleading signals. Strong headline GDP growth driven by capital expenditure may mask underlying economic weakness, particularly in the labour market, where AI has not yet replaced workers but may be discouraging new hiring.

For Labour Markets

The NBER study found that gains are driven primarily by “innovation and demand-oriented channels,” not by cost reduction or labour displacement. This is encouraging for workers in the short term: firms are using AI to create new products rather than to eliminate jobs. But IBM’s decision to triple its young hires, despite AI’s automation capabilities, reveals a deeper concern. If entry-level tasks are automated without hiring new workers to learn those tasks, companies will eventually face a leadership pipeline crisis as the generation that never learned the fundamentals moves into management roles.

For Developing Economies

The AI investment boom is overwhelmingly concentrated in the United States, China, and a handful of European and Asian economies. If AI eventually delivers the productivity gains that proponents promise, the technology gap between AI-adopting and non-adopting economies could widen dramatically, potentially reshaping global inequality in ways that are difficult to reverse.

Is AI the Next Electricity, or the Next Dot-Com Bubble?

The honest answer is: we do not know yet. But the evidence so far suggests that both extreme positions are wrong.

AI is almost certainly not a bubble in the dot-com sense, where companies with no revenue and no viable business model were valued at billions. The firms leading AI investment, including Nvidia, Microsoft, Google, Amazon, and Meta, are genuinely profitable, their products are being adopted at scale, and the underlying technology is demonstrably powerful. A study from the Penn Wharton Budget Model found that generative AI adoption at work is tracking similarly to personal computers in the early 1980s, ahead of the internet, smartphones, and cloud computing at comparable stages.

But AI is also almost certainly not producing the immediate productivity revolution that its most enthusiastic promoters claim. The macroeconomic data is clear: $410 billion in investment has not yet moved the aggregate productivity needle in any statistically significant way. The NBER “productivity paradox,” where perceived gains exceed measured gains, is real and documented across thousands of firms in four countries.

The most likely outcome is somewhere in between: AI will eventually deliver substantial productivity gains, but those gains will arrive later, more unevenly, and more gradually than current investment levels assume. Goldman Sachs projects that AI could boost US productivity by 1.5% annually over the next decade, with a measurable GDP impact starting around 2027. The OECD projects that AI could increase labour productivity in G7 economies by 0.4% to 1.3% annually over a ten-year horizon. These are meaningful numbers, but they require patience measured in years, not quarters.

MASEconomics Explains

Four economic concepts behind the AI productivity debate

The Productivity Paradox

First identified by Robert Solow in 1987 regarding computers, the productivity paradox describes a situation where massive investment in a new technology fails to produce measurable aggregate productivity gains. The current AI version is strikingly similar: $410 billion invested, near-zero macroeconomic return.

General-Purpose Technology

A technology that transforms the entire economy across multiple sectors, such as electricity, the steam engine, or the internet. GPTs require decades of complementary investment in organisation, skills, and infrastructure before their full productivity potential is realised. AI is widely considered the latest GPT.

The Productivity J-Curve

A concept developed by Erik Brynjolfsson describing how new technologies initially reduce measured productivity (the downward dip of the J) as firms invest in adoption, before producing accelerating gains (the upward sweep). The length of the dip varies: 40 years for electricity, 25 for computers, potentially shorter for AI.

Total Factor Productivity (TFP)

The portion of economic output growth that cannot be explained by increases in labour or capital inputs. TFP captures the efficiency gains from technological innovation, better management, and organisational improvement. It is the ultimate measure of whether AI is making economies more productive, not just more capital-intensive.

Key Takeaway and Conclusion

The AI productivity paradox is not a failure of technology. It is a familiar phase in the adoption of every general-purpose technology in economic history. Electricity, computers, and the internet all produced their own productivity paradoxes before eventually transforming the economy. The question is not whether AI will follow the same path, but how long the journey will take and how many trillions will be invested before the destination comes into view.

For investors, the message is caution: the gap between AI spending and AI returns is real, and history shows that technology investments can destroy enormous wealth before they create it. For policymakers, the message is patience: do not design fiscal or monetary policy around AI-driven GDP growth that has not yet materialised. For workers, the message is nuanced: AI is changing how tasks are done but has not yet displaced jobs at scale, though the landscape could shift rapidly once firms move from experimentation to full deployment.

The San Francisco Federal Reserve captured the essential insight beautifully: “Technology will enable, but ideas will determine when it transforms.” The factories of the AI age have been built. The machines have been installed. Now the economy needs its Henry Ford, someone who will reimagine how work is organised around AI rather than simply bolting AI onto existing workflows. Until that happens, the productivity paradox will persist.

And when it does finally resolve, as history strongly suggests it will, the transformation may be more profound than anything we have experienced since electrification.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.