The revival of industrial policy is the most important shift in economic policymaking this century. In 1990, the Washington Consensus told governments a simple thing: stop picking winners. Privatise, deregulate, open trade, and let markets allocate capital. By 2026, that consensus has collapsed. The United States has committed roughly $52.7 billion in direct semiconductor subsidies under the CHIPS and Science Act, with the Joint Committee on Taxation now projecting the Inflation Reduction Act’s clean energy provisions will cost between $660 billion and $790 billion through 2033. The European Union has built a Green Deal Industrial Plan around the Net‑Zero Industry Act and a target of 40% domestic manufacturing capacity for clean technologies by 2030. China, through Made in China 2025, has channelled an estimated $300 billion in initial commitments and another $1.4 trillion in follow‑on funding into ten strategic sectors.

Governments are not just regulating markets. They are building factories, picking technologies, and writing cheques on a scale not seen since post‑war reconstruction. Whether this works, fails, or simply hands subsidies to incumbents that did not need them is now the central question in macroeconomics.

The shift has rolled out in three big experiments. The US CHIPS Act and Inflation Reduction Act use grants, tax credits, and local content rules to onshore semiconductors and clean energy. The EU Green Deal Industrial Plan combines the Net‑Zero Industry Act, the Critical Raw Materials Act, and the Carbon Border Adjustment Mechanism to keep Europe in the clean tech race. China’s state‑led model uses guidance funds, subsidised credit, and local government competition to dominate solar, batteries, and electric vehicles. Each approach has produced both spectacular wins and expensive failures, and the global subsidy race they have triggered now reshapes trade, finance, and geopolitics.

What Industrial Policy Is

Industrial policy is targeted government support for specific sectors, technologies, or firms with the goal of changing the structure of the economy. Tools include direct grants, tax credits, subsidised loans, public procurement, tariffs, local content rules, and state ownership. The aim is not general macroeconomic management. The aim is to push resources towards activities the government believes will deliver higher growth, better jobs, or strategic capabilities than the market would produce on its own.

The textbook definition from Réka Juhász, Nathan Lane, and Dani Rodrik in their influential 2023 paper is “those government policies that explicitly target the transformation of the structure of economic activity in pursuit of some public goal.” That public goal can be productivity growth, technology leadership, supply chain resilience, decarbonisation, or national security.

For four decades, this approach was deeply unfashionable. The free-market consensus that took hold after 1980 treated industrial policy as a relic of failed planning. Governments had backed losers. The British steel industry. The Concorde supersonic jet was retired in 2003 after decades of public losses. Japan’s Fifth Generation Computer project. Mexico’s protected car industry. The intellectual case against picking winners rested on three claims: governments lack the information markets aggregate, political incentives produce capture by incumbents, and free trade with comparative advantage delivers better outcomes than autarky. The IMF, World Bank, and OECD all advised developing countries to keep state intervention narrow.

That consensus broke for four reasons that converged after 2018. First, the COVID-19 pandemic exposed how fragile global supply chains were when concentrated in a few suppliers and choke points. Mask shortages, the 2021 chip famine, and the disruption of medical inputs forced a rethink. Second, the rise of China as a technological competitor created a national security frame around semiconductors, telecommunications, and AI. The free trade promise that economic integration would liberalise China politically did not materialise. Third, climate urgency created a policy logic for accelerating clean technology faster than carbon prices alone could deliver. Fourth, geopolitics added new pressure points. The 2023 confrontation around the Strait of Hormuz and the broader weaponisation of trade routes made supply security a strategic issue, not just a logistics question.

Industrial policy returned because the world that justified its retirement no longer exists.

The Economic Logic

The economic case for industrial policy rests on identified market failures. Private markets, left alone, systematically underinvest in certain activities because the social returns exceed the private returns. The classic categories are research and development spillovers, coordination failures, learning-by-doing, and externalities tied to national security or environmental quality.

R&D spillovers are the strongest case. When a firm invests in basic research, much of the benefit leaks to competitors, customers, and future innovators who pay nothing for it. Standard estimates from the OECD put the social return on R&D at roughly twice the private return. That gap is the core justification for public funding of science, R&D tax credits, and direct subsidies to early-stage technologies. Solar photovoltaics, lithium-ion batteries, and mRNA vaccines all started with public R&D that private investors would not have funded at the scale required.

Coordination failures matter when an industry needs many complementary investments at once. A semiconductor fab needs trained workers, specialised suppliers, reliable power, and downstream customers. If any of those is missing, none gets built, even if all of them together would be profitable. The government can solve this by guaranteeing demand, bundling subsidies, or building shared infrastructure. The CHIPS Act’s combination of fab subsidies, R&D centres, and workforce training programmes is a textbook coordination response.

Learning by doing produces a different kind of failure. In some industries, costs fall as cumulative production rises. Solar panels are the canonical example. Between 2010 and 2024, the cost of utility-scale solar PV fell by roughly 90%. Each doubling of cumulative production has historically cut costs by about 20%. A country that gets in early scales down the learning curve and builds a permanent advantage. A country that waits faces an established competitor producing at a fraction of its costs. China’s solar dominance was built on exactly this dynamic, with state subsidies pushing scale until Chinese producers controlled over 80% of every step of the global solar supply chain.

National security externalities add a non-economic justification. Even if the market would clear at the cheapest price, a country might prefer domestic production of weapons-relevant chips, critical minerals, or pharmaceutical inputs because dependence creates strategic vulnerability. The cost of self-sufficiency is real. The benefit is insurance against supply cut-offs in a crisis.

The semiconductor industry combines all four logics in one sector. Fabs cost $20 billion or more for a leading-edge facility. R&D spillovers are huge. The supply chain requires specialised equipment from a handful of firms in the Netherlands, Japan, and the US. National security depends on chips for everything from missile guidance to AI training. For a deeper treatment of the chip industry’s economics, see our explainer on the economics of the semiconductor industry. The point here is that semiconductors are the test case where industrial policy advocates and sceptics are running their experiment in real time.

The infant industry argument, dating back to Friedrich List and Alexander Hamilton, completes the standard case. New industries in developing economies cannot compete with established foreign producers until they reach scale. Temporary protection, the argument goes, lets them grow up. The historical record is mixed. South Korea’s targeted protection of shipbuilding, steel, and electronics in the 1960s and 1970s produced world-leading firms. Latin American import substitution from the 1950s to 1980s produced inefficient industries that collapsed when protection was removed. The difference, most economists agree, was discipline: Korea tied subsidies to export performance, while Latin America did not.

Three Big Experiments

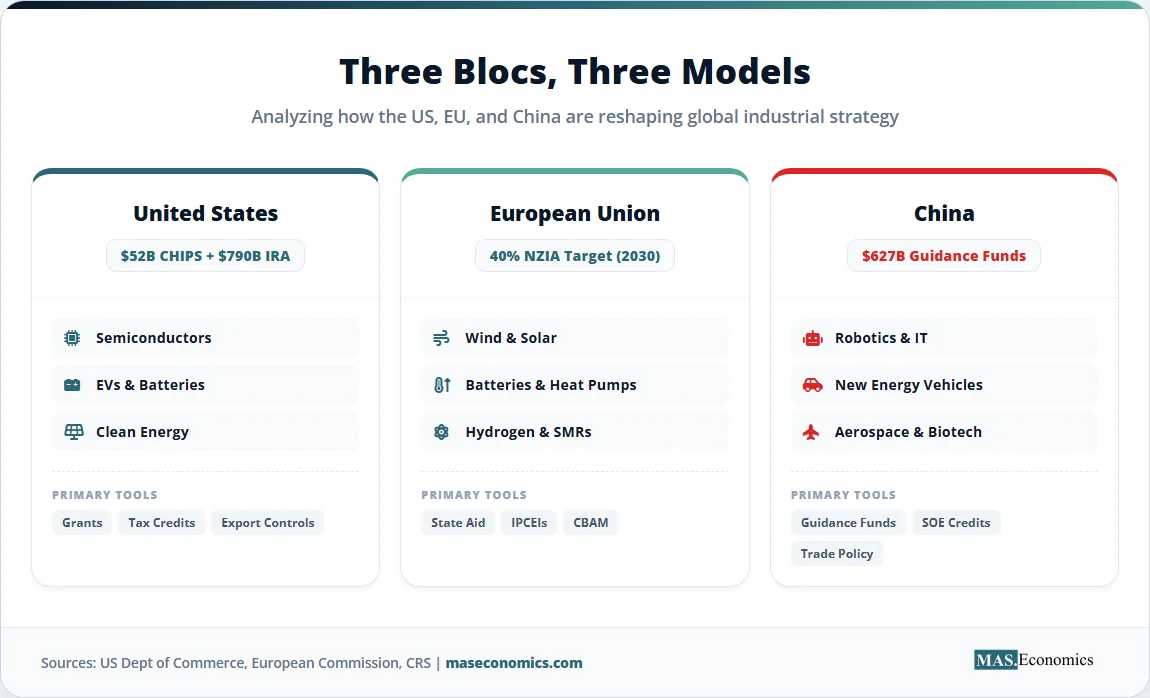

The current revival of industrial policy is concentrated in three blocs that account for the bulk of global manufacturing capacity. Each has chosen different instruments, and each is being watched as a test of what works.

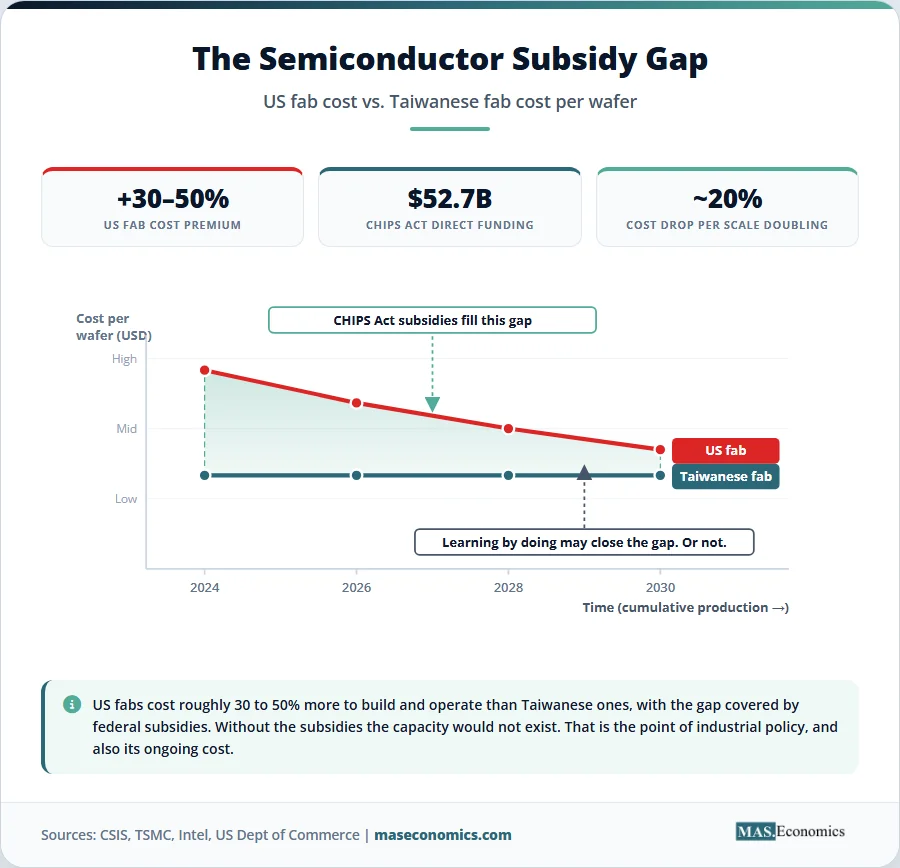

The United States has built its policy on two laws and one set of rules. The CHIPS and Science Act, signed in August 2022, authorised roughly $280 billion in new science and technology funding, of which $52.7 billion was directly appropriated for semiconductors, including $39 billion in manufacturing grants and $13 billion for R&D and workforce. By late 2024, the Department of Commerce had announced over $33 billion in proposed CHIPS incentives across 21 states. Major awards include up to $6.6 billion for TSMC’s Arizona facility, supporting roughly $65 billion in private investment, $8.5 billion to Intel for fabs in four states, and substantial grants to Micron, Samsung, GlobalFoundries, and Wolfspeed. The Inflation Reduction Act of 2022 added a separate clean energy package: tax credits for renewable generation, electric vehicles, hydrogen, advanced manufacturing, and carbon capture, with original cost estimates of around $369 billion that have since been revised upward, with the Joint Committee on Taxation now projecting between $660 billion and $790 billion through 2033. Export controls, particularly the October 2022 and 2023 restrictions on advanced chips and chipmaking equipment to China, complete the package by trying to slow the competitor while subsidising the domestic champion.

The European Union has chosen a different mix. The Green Deal Industrial Plan, launched in February 2023, has four pillars: a simplified regulatory framework, faster access to finance, skills development, and open trade with safeguards. The legislative core is the Net-Zero Industry Act, which entered into force in June 2024 and sets a target that the EU’s manufacturing capacity for strategic clean technologies should reach at least 40% of annual deployment needs by 2030. The Act covers nineteen technologies including solar, wind, batteries, heat pumps, electrolysers, and small modular reactors. The Critical Raw Materials Act addresses upstream dependencies for rare earths and other inputs. Important Projects of Common European Interest, known as IPCEIs, allow consortia of member states to fund cross-border industrial projects in batteries, hydrogen, microelectronics, and cloud infrastructure. The Carbon Border Adjustment Mechanism, the trade-policy arm of the package, will levy carbon costs on imports of steel, cement, aluminium, fertilisers, and electricity from 2026, protecting EU producers operating under the Emissions Trading System. EU funding draws on the Recovery and Resilience Facility, which has already allocated around €250 billion to green measures, the Innovation Fund, and InvestEU, alongside member-state aid.

China’s approach predates the others by a decade and operates on a different scale. Made in China 2025, launched in 2015, identified ten strategic sectors, including next-generation IT, robotics, aerospace, new energy vehicles, biotech, and advanced rail. Funding flows through guidance funds, state-owned banks, local government competition, and direct equity stakes. The Library of Congress Congressional Research Service estimated that nearly 1,800 government guidance funds tied to the programme had targeted $1.5 trillion and secured $627 billion in commitments by 2020. The National Integrated Circuit Industry Investment Fund, the so-called Big Fund, has channelled over $20 billion across multiple rounds into chip design and manufacturing. Subsidies are typically conditional on using domestic intellectual property, on export performance, or on technology localisation. The European Chamber of Commerce in China reported in April 2025 that China had achieved technological dominance in shipbuilding, high-speed rail, and electric vehicles, while still missing targets in aerospace, advanced robotics, and aggregate manufacturing value-added. Self-sufficiency in semiconductors remains around 13%, far below Beijing’s 70% goal, but battery and EV dominance is now structural.

Table 1 lays out the three approaches side by side.

| Table 1. Three industrial policy experiments: A comparison of US, EU, and China approaches | ||||

| Dimension | United States | European Union | China | |

|---|---|---|---|---|

| Headline programmes | CHIPS Act, IRA, export controls | Green Deal Industrial Plan, Net-Zero Industry Act, CBAM | Made in China 2025, Big Fund, guidance funds | |

| Approximate scale | $52.7bn CHIPS direct + $660–790bn IRA energy credits through 2033 | €250bn green RRF + Innovation Fund + member-state aid | ~$300bn initial + ~$1.4tn follow-on; $627bn in guidance funds by 2020 | |

| Priority sectors | Semiconductors, EVs, batteries, hydrogen, solar | Solar, wind, batteries, heat pumps, electrolysers, SMRs | IT, robotics, aerospace, EVs, biotech, advanced rail | |

| Main instruments | Grants, 25% investment tax credits, local content rules, export controls | Eased state aid rules, IPCEIs, CBAM, fast-track permitting | Guidance funds, subsidised credit, SOE coordination, technology transfer pressure | |

| Conditionality | Geographic restrictions, prevailing wage, China expansion ban | Net-zero criteria, EU manufacturing share, Member-state co-financing | Indigenous IP requirements, export targets, local content | |

| Coverage horizon | 10 years for grants, longer for tax credits | Targets to 2030 and 2050 | Targets through 2025 and 2049 | |

| ||||

The differences matter. The US relies heavily on tax credits, which scale automatically with demand and have produced cost overruns as uptake exceeded forecasts. The EU layers state aid through national governments, requiring Brussels approval but giving member states ownership. China combines central direction with competition between provinces, generating duplication but also rapid scaling. None of these is the textbook model. All three are still being tested.

The Spending Race

The chart below tracks announced industrial policy commitments by major economies since 2020. The numbers are not directly comparable because budget windows, accounting methods, and what counts as industrial policy differ across jurisdictions, but the direction is unmistakable.

Sources: US Department of Commerce; Joint Committee on Taxation (2024 update); European Commission; Recovery and Resilience Facility data; Bruegel; Congressional Research Service estimates of MIC2025 guidance fund commitments. Figures are announced or projected commitments through programme horizons, not annual flows. Currency converted at 2024 average rates.

Several patterns stand out. Headline US figures dwarf European ones because the IRA tax credits are open-ended and demand-driven. Chinese figures aggregate over a longer period and a much wider set of instruments, so the headline number is large, but the precise composition is opaque. Europe’s smaller direct figures understate its actual industrial policy footprint because state aid by individual member states, particularly Germany, has expanded sharply since 2022 under the relaxed Temporary Crisis and Transition Framework. The OECD has documented a clear upward trend in industrial policy intensity across all major economies, not just the three blocs covered here. Japan’s Rapidus chip foundry project, India’s production-linked incentive schemes, and South Korea’s K-Chips Act all add to a global subsidy race in which staying out is no longer a credible option for any large economy.

The fiscal cost is part of a broader pressure on government budgets. With debt-to-GDP ratios above pre-pandemic levels in nearly every advanced economy, the room to fund industrial policy is bounded by what bond markets will tolerate. Our piece on sovereign debt sustainability covers the fiscal arithmetic in detail.

What the Evidence Shows

The evidence on whether industrial policy delivers what it promises is more mixed than either advocates or critics admit. Three case studies set the boundaries.

Semiconductors are the highest-stakes test. By early 2026, TSMC, Samsung, Intel, and Micron had committed over $300 billion in announced investment in US fabs, much of it triggered or accelerated by CHIPS Act incentives. TSMC’s Arizona fab began producing 4-nanometre chips in late 2024 and is now scaling toward 3nm and 2nm. Samsung’s Taylor, Texas, facility is on track to open. Intel’s Ohio campus has slipped to 2030 and beyond, raising questions about execution. The race to 2nm production by 2027 is now genuinely multi-polar, where five years ago it was concentrated in Taiwan and South Korea. That is a real policy success measured against the original goal of geographic diversification. Whether it is cost-effective is another matter. CSIS analysts note that US fabs cost roughly 30–50% more to build and operate than Taiwanese ones, with the gap covered by subsidies. Stripping out the subsidies, the fabs would not exist. That is the point of industrial policy, but it is also why the policy will need to keep paying to keep the capacity.

Solar and battery manufacturing tell a different story. German feed-in tariffs in the 2000s created the early demand that pushed solar PV down its cost curve. Then, Chinese subsidies scaled production so aggressively that German manufacturers, including Q-Cells and SolarWorld, were driven out of business by the mid-2010s. Today, China produces around 80% of global solar modules. The German policy worked for the planet by making solar energy cheap. It failed for German industry. The IRA’s manufacturing credits are now trying to rebuild a domestic solar and battery supply chain in the US, but at much higher costs than the established Chinese competition. Whether learning-by-doing closes the gap or whether US producers remain dependent on permanent subsidy is the open question.

The failure cases matter just as much. Concorde lost an estimated £1 billion in 1976 prices over its development and production. The British and French taxpayers covered the bill. Many electric vehicle startups funded by Chinese government funds have collapsed, including high-profile names like Byton and dozens of smaller players. The “1,000 little giants” expansion of the EV sector under Made in China 2025 created chronic overcapacity that is now being exported as a glut of cheap vehicles, triggering tariffs in Europe and the US. Past steel subsidies in Europe and the US sustained obsolete capacity for decades and required restructuring crises in the 1980s and 1990s to clear. Special economic zones have a similarly mixed record. Shenzhen worked, transforming a fishing village into a megacity. Many African and Latin American zones have produced little beyond enclaves of subsidised investment with weak spillovers to the surrounding economy.

Recent academic work by Juhász, Lane, and Rodrik (2023) and Goldberg, Juhász, Lane, Lo Forte, and Thurk (2024) on the global semiconductor sector finds that industrial policy can produce real gains in firm productivity and innovation, but that gains are concentrated in well-designed programmes with clear performance metrics, sunset clauses, and exposure to international competition. Programmes that simply transfer money to incumbents without performance conditions tend to entrench inefficiency. A 2025 IMF working paper by Garcia-Macia and others, using firm-level data from China, found that cash subsidies in priority sectors lowered measured revenue productivity, suggesting overproduction at low margins, while regulatory protection raised it by reducing competitive pressure. The lesson is the design point Korea got right, and Latin America got wrong: discipline and exit rules matter more than the headline number.

Risks and Criticisms

The economic case against the current revival has four pillars.

The first is government failure. Governments do not have private firms’ information about technology, demand, or costs. They are vulnerable to lobbying by incumbents and to political pressure to support visible projects in marginal constituencies. The CHIPS Act’s first major awards went disproportionately to large established firms, not to startups or new entrants. The IRA’s electric vehicle credits have produced complex eligibility rules that lawyers and accountants navigate more easily than small manufacturers. Once subsidies are in place, ending them is politically difficult. Concorde flew for 27 years partly because cancelling it would have meant admitting failure. Today’s clean energy and chip subsidies will face the same dynamic.

The second is rent-seeking. When the government picks winners, firms invest in lobbying as well as production. The economic literature, dating to Anne Krueger’s 1974 paper on rent-seeking, finds that this can dissipate much of the intended public benefit. The proliferation of trade associations, lobbying groups, and consultancies around the CHIPS Act and the Green Deal Industrial Plan suggests this dynamic is operating at scale. Studies of Chinese guidance funds find substantial duplication and waste as provinces compete to attract the same firms.

The third is international retaliation. The US export controls on chips to China prompted Beijing to accelerate domestic substitution and to restrict exports of gallium, germanium, and other critical minerals. The IRA’s Buy American provisions provoked European and Korean complaints and accelerated the EU’s own subsidy push. The Carbon Border Adjustment Mechanism is already drawing legal challenges at the WTO. The cumulative effect is a fragmenting trading system where each major bloc subsidises its own producers and taxes everyone else’s. This is the world traced in our pieces on the global tariff war of 2025–2026, on economic sanctions, and on supply chain economics. The risk is that the global subsidy race produces lower aggregate welfare than the system it replaced, even if individual countries appear to benefit.

The fourth is distributional. The countries with deep pockets to run industrial policy at scale are the rich ones plus China. Developing economies cannot match $50 billion in fab subsidies or $660 billion clean energy programmes. They lose policy space twice over: first because the WTO rules against industrial policy were written when developed countries had already industrialised, and now because the new norm of large subsidies advantages whoever has fiscal room. Pakistan, Brazil, Indonesia, and most of Africa cannot run a CHIPS Act or a Green Deal Industrial Plan. They can only watch as the rules of global production get rewritten in capitals where the subsidies are paid. Some of the productivity gains documented in the rich-country revival may simply be reallocations away from poorer producers who were perfectly capable of supplying the same goods at lower cost.

A separate concern, raised by sceptics including the OECD’s 2024 review by Millot and Rawdanowicz, is that industrial policy may be running ahead of the productivity gains it is supposed to produce. The AI productivity paradox, where hundreds of billions in investment have so far produced minimal measurable GDP impact, hangs over the broader subsidy story. Cheap money plus large subsidies plus strategic urgency is a combination that produces investment, but not necessarily productive investment.

MASEconomics Explains

Four economic concepts behind the revival of industrial policy

Conclusion

The revival of industrial policy is the defining shift in macroeconomic thinking of this decade. Trillions of dollars are now flowing into chips, clean energy, and strategic technologies under the active direction of states. The economic logic rests on real market failures: R&D spillovers, coordination problems, learning-by-doing, and national security externalities that private markets do not internalise. The historical record shows that targeted, disciplined programmes with performance conditions and exit rules can deliver large productivity and capability gains. It also shows that programmes without those conditions burn money on incumbents and white elephants. The US, EU, and Chinese experiments will be judged on which side of that line they fall. The fragmentation of the trading system, the squeeze on developing-country policy space, and the fiscal cost of open-ended tax credits are real prices already being paid. Whether the benefits exceed the costs depends on the details of programme design that are still being written.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.