Two gas stations sit on opposite corners of the same intersection. One drops its price by three cents a gallon to pull cars across the street. The other watches, then matches. By midweek, both stations earn pennies per gallon. A few miles away, two airlines plan their seats on the Chicago to Denver route. Neither cuts fares. Each simply decides how many flights to schedule, knowing the rival will do the same, and prices settle well above cost.

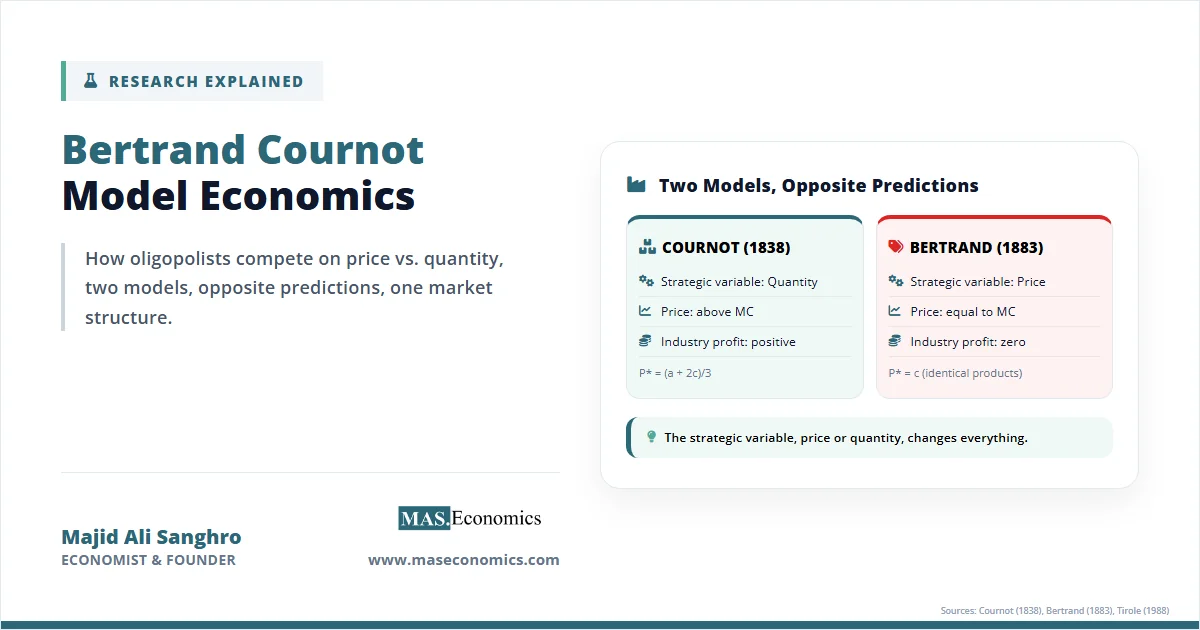

The same industry structure, two firms competing, produces wildly different outcomes. The reason sits at the heart of the Bertrand Cournot model economics debate: do firms compete by setting prices or by setting quantities? That single choice changes whether consumers get something close to a competitive deal or whether two firms split a comfortable margin between them. The two foundational models of oligopoly answer the question in opposite ways, and which one applies to a given market shapes everything from antitrust enforcement to the daily price you pay at the pump.

Cournot and Bertrand Compared

Augustin Cournot wrote his model in 1838, decades before economists had the modern tools of game theory. He pictured two mineral water producers drawing from neighbouring springs. Each chose how much water to send to market. The combined output then set the price through ordinary demand. Cournot’s question was simple: if each producer assumes the rival’s quantity is fixed and optimises against it, where does the system settle?

The answer was a stable point that we now recognise as a Nash equilibrium, more than a century before John Nash formalised the concept. In the Cournot world, total output sits below what perfect competition would deliver but above the monopoly level. Price stays above marginal cost. Each firm earns a positive profit. The market is competitive enough to push prices down from the monopoly level, but not competitive enough to drive them all the way to cost.

Joseph Bertrand attacked the model in an 1883 review. Bertrand argued that real firms set prices, not quantities. If two firms sell identical products and choose prices simultaneously, consumers buy from whoever charges less. The logic then becomes brutal. Any firm pricing above marginal cost can be undercut by a rival willing to take the entire market at a slightly lower price. The undercutting continues until both firms set the price equal to the marginal cost. Two firms produce the perfectly competitive outcome. Profits collapse to zero.

The contrast is stark. Cournot competition with two firms yields prices well above cost. Bertrand competition with two firms yields prices at cost. Same number of firms, same demand, same costs, but opposite predictions. The difference rests entirely on what firms choose. Quantity or price.

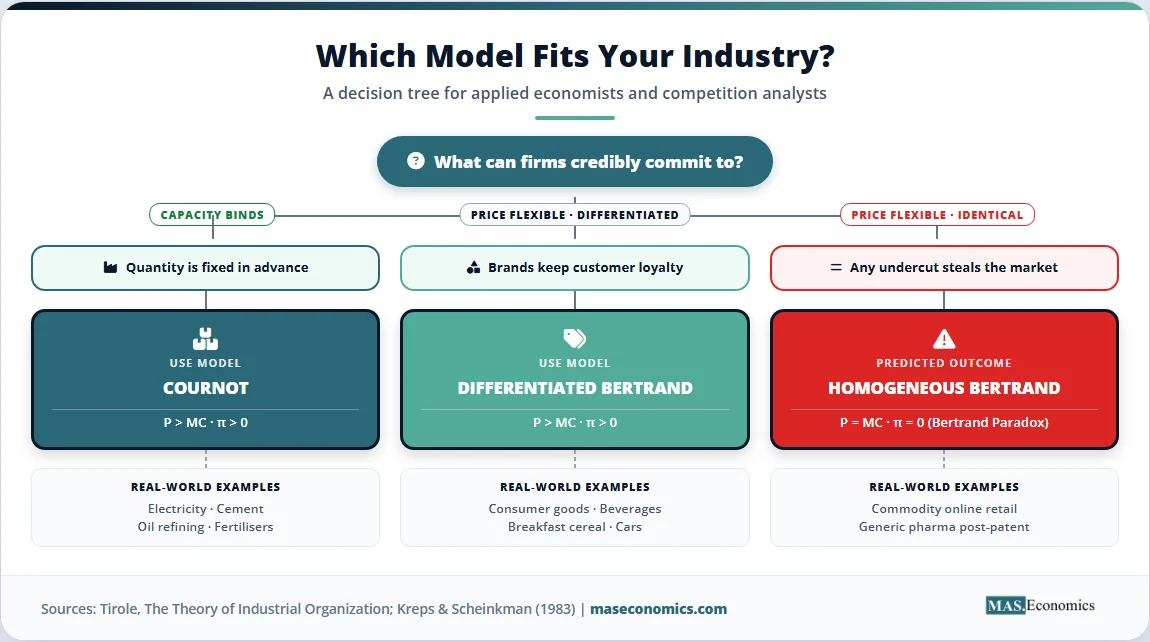

Why the Strategic Variable Matters

The choice of strategic variable is not a technical detail. It reflects what firms can credibly commit to. A power plant cannot adjust its generation capacity overnight. A semiconductor fab cannot retool in a week. In industries where output is set in advance, and price clears the market, Cournot is the natural framework. A supermarket, by contrast, changes prices on the shelf every day. Capacity is rarely binding. Bertrand fits the world of retail pricing, online platforms, and most consumer services.

The historical reception of the two models reflects this insight. Cournot’s work was largely ignored for forty years until Léon Walras and others began building modern economic theory on its foundations. Bertrand’s 1883 critique gave economists the puzzle that drove a century of refinement. The Cournot equilibrium felt natural to nineteenth-century observers because most industries of the era were capacity-constrained. The Bertrand outcome felt suspicious, almost pathological. Yet both models survived because each captures something real about how firms compete, depending on the technology and time horizon involved.

Cournot and Bertrand in Equations

Both models start from the same demand and cost structure, then diverge in what firms choose. Consider a duopoly with linear inverse demand and identical constant marginal costs. The setup is:

Here \( a \) is the demand intercept, \( b \) is the slope, \( q_1 \) and \( q_2 \) are the firm output choices, and \( c \) is the constant marginal cost shared by both firms. The variables and their roles are summarised in the table below.

| Symbol | Meaning | Role in the Model |

|---|---|---|

| \( a \) | Demand intercept | Maximum willingness to pay when quantity is zero |

| \( b \) | Slope of inverse demand | Rate at which price falls as total quantity rises |

| \( c \) | Marginal cost | Constant unit cost of production for both firms |

| \( q_i \) | Firm \( i \) output | Strategic choice in the Cournot model |

| \( p_i \) | Firm \( i \) price | Strategic choice in the Bertrand model |

| \( Q \) | Total market quantity | Sum of firm outputs, sets the market price |

| \( \pi_i \) | Firm \( i \) profit | Revenue minus total cost for each firm |

| ||

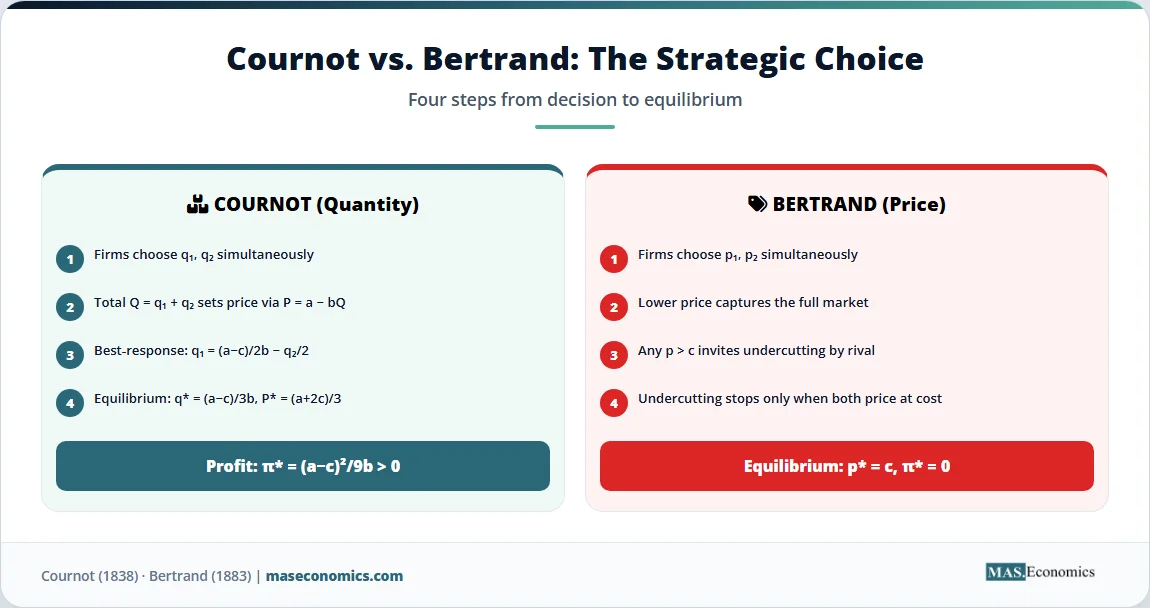

The Cournot Solution Step by Step

Firm 1 chooses \( q_1 \) to maximise its profit, taking \( q_2 \) as given. Profit is revenue minus cost:

The first order condition with respect to \( q_1 \) gives:

Solving for \( q_1 \) yields the best response function, which tells us how firm 1 should react to any quantity firm 2 chooses:

Firm 2 faces a symmetric problem. By symmetry, the Nash equilibrium has \( q_1^* = q_2^* \). Substituting and solving gives the equilibrium quantities, total output, and price:

Each firm earns a positive profit equal to:

The price sits one-third of the way from monopoly down to perfect competition. Total output is two-thirds of what a perfectly competitive industry would produce. The market is competitive but far from cost-based pricing.

The Bertrand Solution and Its Surprise

Now, suppose firms choose prices. With identical products, the firm posting the lower price captures the entire market. If \( p_1 < p_2 \), firm 1 sells everything and firm 2 sells nothing. If \( p_1 = p_2 \), they split the market.

Consider any candidate equilibrium where both firms charge \( p > c \). Firm 1 can drop its price by a tiny amount \( \epsilon \), capture the full market, and earn close to \( (p – c)Q \) instead of half of \( (p – c)Q \). Firm 2 has the same incentive. Each firm undercuts until neither can profitably go lower. The unique pure strategy Nash equilibrium is:

Profits are zero. Output is the perfectly competitive level. Two firms produce the same outcome as perfect competition. This is the Bertrand Paradox, and it is the most striking prediction in oligopoly theory. The model says we do not need many firms to get competitive prices. We need two, provided they sell identical products and can change prices freely.

Key Assumptions and Their Limits

The dramatic gap between Cournot and Bertrand outcomes rests on assumptions that real industries rarely satisfy in full. Both models share four assumptions: identical products, no capacity constraints, simultaneous moves, and complete information. Each one has been relaxed in later work, and each relaxation pulls the predictions toward something more realistic.

The Bertrand Paradox dissolves once products differ. If consumers see firm 1 and firm 2 as imperfect substitutes, a small price cut no longer steals the entire market. Each firm has some pricing power tied to the customers who prefer its product. The Hotelling model formalises this with two firms locating along a line representing consumer tastes. Equilibrium prices end up above marginal cost, with the gap widening as products become more differentiated.

Capacity constraints fix the paradox a different way. Francis Edgeworth pointed out that if firms cannot serve the whole market at the lower price, undercutting stops being profitable. A firm with limited capacity gains nothing from a microscopic price cut because it cannot supply the residual demand the rival would otherwise meet. Once capacity is tight, the equilibrium can resemble Cournot more than Bertrand. Kreps and Scheinkman showed in 1983 that a two stage game where firms first choose capacity and then prices yields the Cournot outcome. Capacity choices effectively pin down quantities, and prices adjust to clear the market.

Repeated interaction also breaks the paradox. Firms that meet again and again can sustain prices above cost through implicit understandings, which we cover in our article on types of collusion in oligopoly. Cooperation becomes a Nash equilibrium of the repeated game, supported by the threat that any deviation will trigger price competition that destroys profits.

When Each Model Fits the Real World

Cournot is the natural fit when capacity decisions precede pricing. Electricity generation is the textbook case. A coal plant takes years to build. Hourly bids in a wholesale electricity auction look like price setting, but the binding constraint is installed capacity. Cement, oil refining, fertiliser, and most heavy industry follow the same logic. Quantity decisions made today determine what is on offer next year, and prices clear residual demand.

Bertrand fits markets where price is the decision variable, and capacity is plentiful. Online retail, software subscriptions, generic pharmaceuticals after patent expiry, and supermarket staples all approximate Bertrand competition. Algorithms now adjust prices in real time on Amazon and across e‑commerce. The capacity to ship one more unit is rarely binding, so the model predicts competitive prices when products are close substitutes.

What Experiments and Data Show

The predictions of both models have been tested extensively. Laboratory experiments give the cleanest comparison because researchers can fix demand, costs, and the strategic variable.

Huck, Normann, and Oechssler reviewed dozens of Cournot experiments in 2004 and found that with two firms, average market output sits close to the Nash prediction or slightly below it, suggesting modest tacit cooperation. With three firms, output rises, and behaviour tracks Nash more tightly. With four or more firms, markets become essentially competitive. The Cournot model performs well as a description of what subjects actually do in controlled experiments.

Bertrand’s experiments tell a different story. With identical products, two-firm Bertrand markets do collapse to prices near marginal cost, matching the paradox. But once experimenters add even mild product differentiation, prices settle well above cost. The Bertrand model with differentiated products is a better description of most real markets than the homogeneous goods version, and the experimental record confirms it.

Field studies match the lab. Borenstein, Bushnell, and Wolak found that California wholesale electricity prices during the 2000 to 2001 crisis were consistent with strategic withholding of capacity, an outcome predicted by Cournot models with capacity. Supermarket pricing studies, by contrast, show patterns closer to Bertrand with differentiation. Stores compete on price across thousands of items, but local market power and product variety keep margins positive. The chart below summarises how the four benchmark market structures compare on price, output, profit, and consumer surplus, using a stylised linear demand example.

The empirical record on differentiated Bertrand markets is especially rich. Studies of the US ready-to-eat cereal industry, the European car market, and bottled beverages have all used variants of the differentiated Bertrand framework to estimate demand elasticities and predict the price effects of mergers. The fit between model predictions and observed outcomes is generally good once differentiation is taken into account. Studies that ignore differentiation, by contrast, predict competitive prices that the data flatly contradict. The lesson is that the simple Bertrand model is not wrong. It just applies to a narrower set of industries than its critics first assumed.

Figure 1. Equilibrium outcomes across market structures, normalised to the perfect competition benchmark. Source: Standard linear demand duopoly model with \( a = 100 \), \( b = 1 \), \( c = 20 \).

Policy Relevance of Both Models

The Cournot and Bertrand models are not historical curiosities. They are the working tools of modern competition policy, used every day by antitrust agencies and merger economists. When two firms in the same market propose to combine, regulators do not estimate the new entity’s behaviour from scratch. They run merger simulations built on either Cournot or Bertrand foundations, depending on which fits the industry.

Bertrand simulations dominate consumer goods analysis. The model with differentiated products has been the standard tool for evaluating mergers in beer, breakfast cereal, soft drinks, and most retail markets since the 1990s. The technique, often called Upward Pricing Pressure, asks how much a merged firm would be tempted to raise prices once it internalises competition between its own brands. Antitrust agencies in the United States and the European Union both use variants of this approach. The 2010 US Horizontal Merger Guidelines formalised the role of these simulations and made them the centrepiece of unilateral effects analysis.

Cournot simulations are the tool of choice in commodity and capacity-constrained industries. Mergers in cement, steel, fertiliser, and electricity are typically analysed with Cournot models because the strategic decision is how much to produce, and capacity constraints are real. The European Commission’s review of the 2008 EDF acquisition of British Energy used a Cournot framework to assess wholesale electricity competition in Britain.

The choice between the two frameworks is itself a substantive question. Get it wrong, and merger predictions can be off by a factor of two or more. A Bertrand simulation applied to a Cournot industry will understate post-merger price increases because it ignores the binding capacity constraints. A Cournot simulation in a Bertrand market will overstate market power because it assumes firms commit to quantities they would never actually fix.

Beyond Mergers: Regulation and Market Design

The models also inform sector regulation. Energy regulators in Britain and the Nordic countries use Cournot benchmarks to assess whether wholesale electricity prices reflect competitive bidding or strategic withholding. Telecommunications regulators run Bertrand-inspired models to evaluate whether mobile network operators are competing on price or coordinating tacitly. Tax policy on platforms, the design of spectrum auctions, and the regulation of pharmaceutical generics all draw on the same toolkit.

The link to broader oligopoly behaviour also matters. Models of limit pricing and entry deterrence build directly on Cournot and Bertrand foundations, asking how incumbent firms can use quantity or price commitments to keep rivals out. The branch of economics that studies how firms interact strategically, covered in our article on game theory and strategic behaviour, treats these two models as the canonical applications of the Nash equilibrium to industry.

The broader question of how prices form across different competitive settings is the subject of our piece on price determination in different market structures, and the underlying classification of those structures is laid out in exploring market structures in microeconomics. The Bertrand and Cournot models are what fills in the cells between monopoly and perfect competition. They explain why some industries with few firms behave almost competitively while others extract substantial rents.

Modern industrial organisation has extended both models in directions Cournot and Bertrand never imagined. Dynamic versions allow firms to invest in capacity over time and compete repeatedly. Asymmetric information versions ask what happens when one firm knows more about costs or demand than its rival. Network effect models adapt the Bertrand framework to platforms where the value of using a service depends on how many others use it. Each extension keeps the underlying logic of best response and Nash equilibrium intact while relaxing one of the original assumptions. The 1838 and 1883 papers remain the points of departure.

The two models also shape the regulation of new technology. Algorithmic pricing on Amazon, Uber surge pricing, and dynamic airline fares are all forms of Bertrand competition with rapid price adjustment. Antitrust agencies have started to ask whether pricing algorithms can sustain Cournot-like outcomes through tacit coordination, even without explicit communication between firms. The European Commission, the US Department of Justice, and the UK Competition and Markets Authority have all opened investigations into algorithmic pricing in recent years. The framework for analysing these cases sits squarely on the Cournot and Bertrand foundations laid almost two centuries ago.

MASEconomics Explains

Four economic concepts behind the Bertrand and Cournot models

Conclusion

The Bertrand Cournot model economics framework gives competition policy and industrial organisation their most basic prediction tools. Cournot competition assumes firms commit to quantities and lets price clear the market, producing outcomes between monopoly and perfect competition. Bertrand competition assumes firms set prices directly, and with identical products, it drives margins to zero with as few as two firms. The two models bracket the range of duopoly outcomes, and the choice between them depends on what firms can credibly fix in advance.

Real industries rarely match either model exactly. Capacity constraints, product differentiation, and repeated interaction pull outcomes away from the textbook predictions. Yet the underlying logic still applies. Wholesale electricity markets behave like Cournot competition because capacity is the binding choice. Online retail behaves like differentiated Bertrand competition because price is the daily decision. Antitrust agencies pick the framework that fits the industry and run merger simulations from there.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.