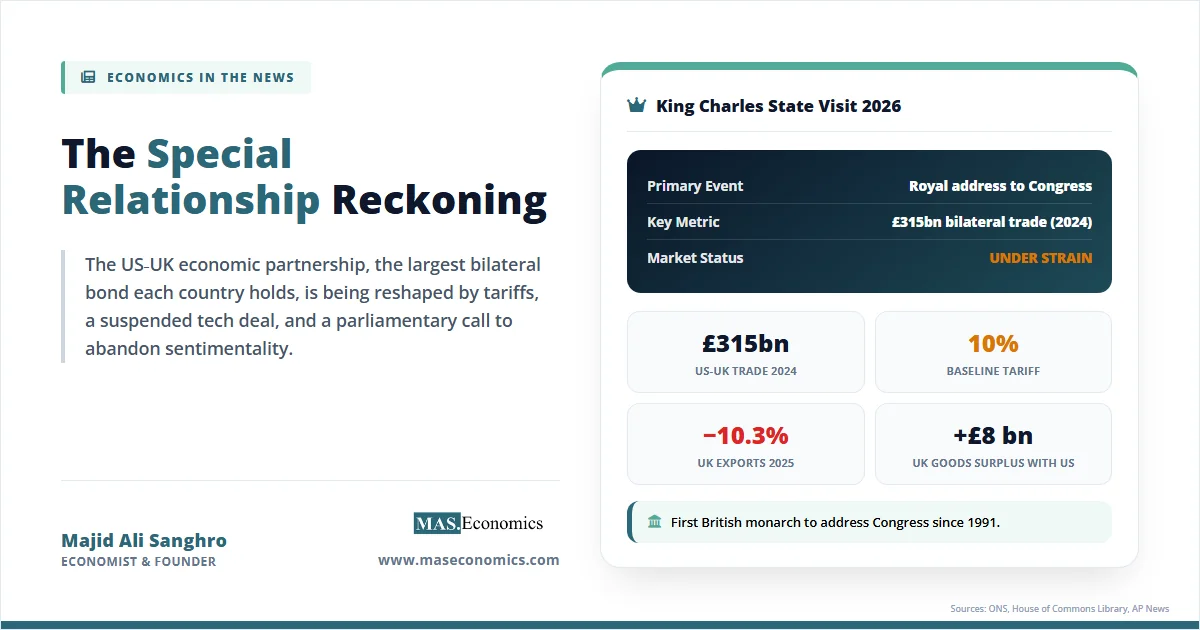

On Tuesday, 28 April 2026, King Charles III stood in the United States Capitol and received standing ovations from a joint session of Congress. Hours later, at a state banquet in the East Room of the White House, President Donald Trump leaned into the microphone and broke a 250-year convention. Speaking of Iran’s nuclear ambitions, he turned to the British monarch beside him and announced that “Charles agrees with me, even more than I do.” Buckingham Palace, which never confirms what the King says in private, was forced to issue a clipped statement noting that the monarch is “naturally mindful of his government’s long-standing and well-known position on the prevention of nuclear proliferation.”

The contrast captures the moment. The US UK economic relationship is the largest single bilateral commercial bond either country maintains, with goods and services trade running at around £315 billion in 2024 and US firms employing more than a million Britons. Yet the political architecture sitting on top of that economic base is being remade in real time. A monarch addresses Congress to plead for the open trading order his five-times great-grandfather, George III, lost in 1776. A president weaponises a private royal conversation to score a foreign policy point. And in the background, UK exports to the United States have just posted their first annual decline since the pandemic.

This is the economic anatomy of a partnership under strain. The pageantry is real. So are the numbers. Both deserve a serious reading.

Pageantry and Political Reality

The choreography of the visit was meticulous. Charles and Camilla landed at Joint Base Andrews on Monday, 27 April, the first British monarch to make a state visit to the United States since Queen Elizabeth II in 2007. The trip was timed to the 250th anniversary of American independence and was hand-delivered as an invitation by Prime Minister Keir Starmer during Trump’s own unprecedented second UK state visit in September 2025. The strategy was explicit: use the one piece of soft power Britain still possesses uniquely, the Crown, to woo a president who openly admires monarchs and openly disdains the prime minister.

On day one, the Trumps welcomed the royal couple at the South Portico for tea in the Green Room, toured the new South Lawn beehive, and hosted a garden party at the British ambassador’s residence. The program proceeded despite a shooting at the White House Correspondents’ Dinner on Saturday, 26 April, which Charles addressed at the start of his Congressional speech with the line: “Such acts of violence will never succeed.”

Day two was the centrepiece. Charles became only the second British monarch ever to address a joint session of Congress, after his mother in 1991. His prepared remarks opened with what he called “A Tale of Two Georges” and stretched across themes that, on closer reading, were a careful catalogue of disagreements with the host. He praised NATO. He urged continued support for Ukraine. He warned against isolationism and called for action on climate change. He acknowledged “times of great uncertainty” while noting that the destinies of the two countries “have been interlinked”. The implication, addressed to a Republican administration that has questioned each of those positions, was unmistakable.

Then came the state dinner. Charles invoked his mother’s 1957 Washington visit, which had been organised “to put the special back into our relationship after a crisis in the Middle East”, a reference to the Suez rupture. “Nearly 70 years on,” he joked, “it is hard to imagine anything like that happening today.” The room laughed. He gifted Trump the bell from HMS Trump, a British submarine that served in the Pacific in 1944.

And then Trump took the microphone. Speaking of the Iran war that Britain had pointedly refused to join, the president declared: “We have militarily defeated that particular opponent, and we’re never going to let that opponent ever – Charles agrees with me, even more than I do – we’re never going to let that opponent have a nuclear weapon.” The reference to a private conversation breached one of the oldest conventions of constitutional monarchy. The British media noted it with controlled understatement. Buckingham Palace’s response was a model of diplomatic minimalism. Day three saw the royal couple visit the 9/11 Memorial in New York and meet Bank of America, JP Morgan, Blackstone, Citigroup, Comcast, and Alphabet executives at Rockefeller Center for a UK-US trade reception. Today, Thursday, 30 April, they conclude with a stop in Virginia before departing.

The friction the visit was designed to ease has not eased quietly. Trump has repeatedly criticised Starmer over the Iran war, declaring: “This is not Winston Churchill that we’re dealing with”, and pushed Britain to issue new oil and gas drilling licences in the North Sea. Last week, he threatened a “big tariff” on UK goods unless the digital services tax on US technology firms is scrapped, accusing Britain of trying “to make any easy buck”. He has also questioned UK plans to cede the Chagos Islands to Mauritius, a deal that affects the joint US-UK military base on Diego Garcia.

The £315 Billion Trade Backbone

Stripped of the pageantry, the commercial relationship the King came to defend is the largest single bilateral bond either country maintains. The United States is the UK’s largest single export market, taking 17% of all UK goods exports in 2024, worth £66 billion. The next largest, Germany, accounted for £33 billion. The UK exported £137 billion of services to the United States in 2024, equivalent to 27% of all UK services exports, with “other business services” (£61.2 billion) and financial services dominating the mix. From the American side, the United Kingdom is the United States’ fourth-largest trading partner, with $341.7 billion in two-way goods and services trade in 2024.

The investment relationship runs even deeper than the trade flows suggest. The two countries have £1.2 trillion invested in each other’s economies. The United States is the single largest source of foreign direct investment into the UK, generating 376 FDI projects in 2023-24 that created 19,340 jobs, and the UK, in turn, is one of the largest single-country investors in America. The headline figure regularly cited by both governments is that US firms employ more than a million people in Britain and British firms employ a similar number in the United States.

That is the size of the prize. The current trajectory of trade tells a different story.

| Indicator | UK with US | UK with EU | Notes |

|---|---|---|---|

| Total trade (2024) | £315 billion | £781 billion (2025) | EU is bloc-wide; US is single country |

| Share of UK goods exports (2024) | 17% | 47% | US is largest single-country market |

| Share of UK services exports (2024) | 27% | 37% | Services dominate UK-US trade |

| UK goods exports (2024, £bn) | £66 | £184 | HMRC data |

| UK services exports (2024, £bn) | £137 | £203 | ONS data |

| Goods balance (UK perspective) | +£8 bn | -£90 bn approx. | UK runs goods surplus with US |

| Tariff regime (April 2026) | 10% baseline + sectoral | Single market access | Post-EPD residual tariffs |

| |||

Sources: ONS UK Trade February 2026; House of Commons Library research briefing CBP-10240; UK Department for Business and Trade.

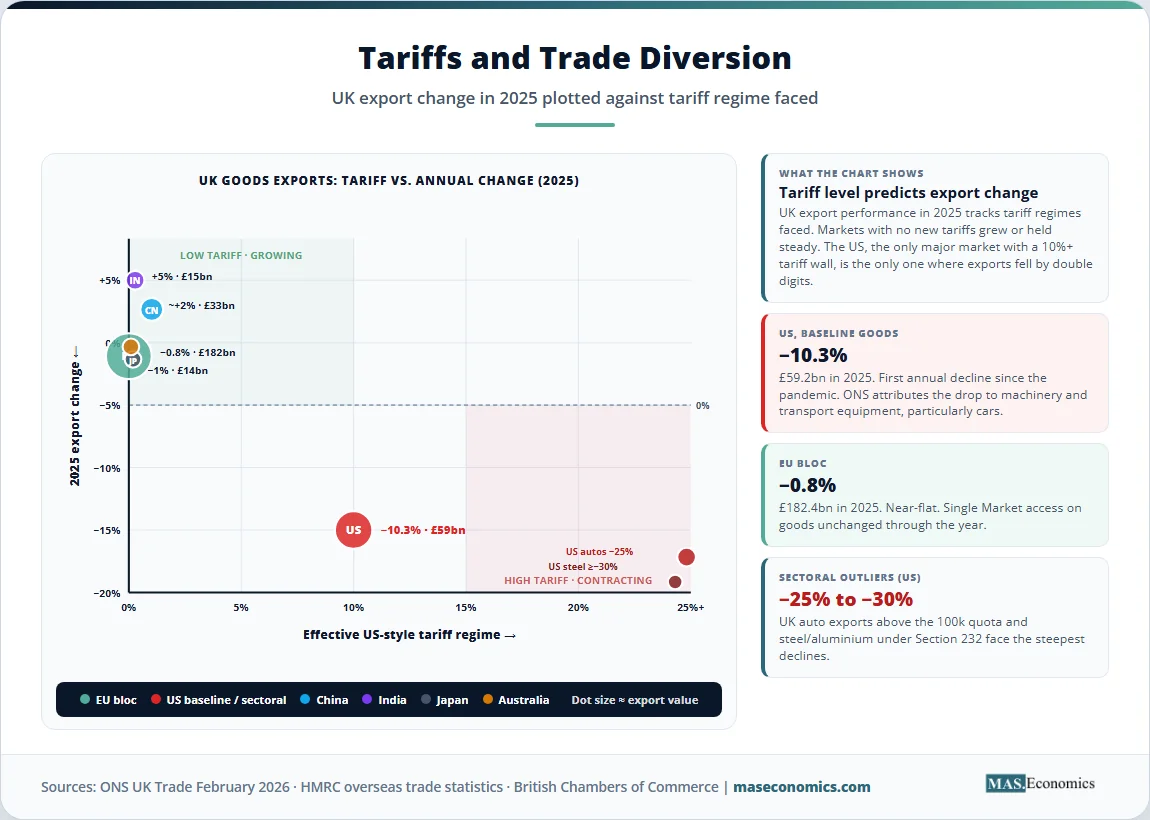

Recent monthly data are clearer than the annual averages. UK goods exports to the US fell 10.3% to £59.2 billion for the year ending December 31, 2025, the first annual decline since the pandemic. In January 2026, UK goods exports to the US dropped 11.3% in a single month, led by declines in machinery and transport equipment, particularly cars. February 2026 saw a partial bounce of 11.3%, but ONS noted that “the value of goods exports to the United States has remained relatively low since the introduction of trade tariffs in April 2025”. The 10% baseline tariff regime introduced after Trump’s Liberation Day announcement is doing what tariffs do: it is raising costs at the border, and exporters are responding by selling less.

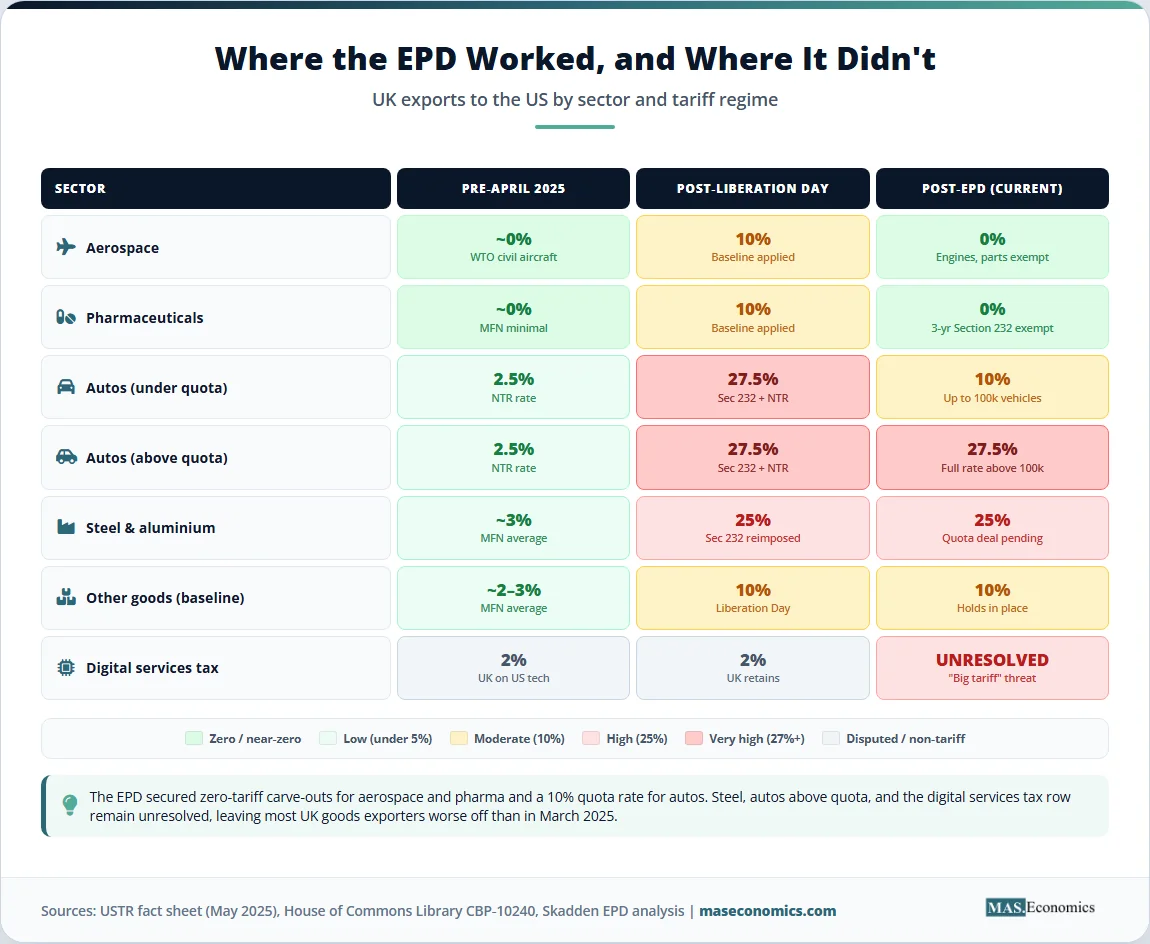

What the Economic Prosperity Deal Achieved

The diplomatic answer to the new tariff regime is the Economic Prosperity Deal (EPD), the framework signed by Trump and Starmer on 16 June 2025 at the G7 summit in Canada, after general terms had been announced on 8 May 2025. The EPD is not a free trade agreement. It is a set of selective tariff carve-outs that buys time for further talks. The terms matter because they show what each side could actually agree to in 2025, and what remains stuck.

On automobiles, the United States established an annual quota of 100,000 vehicles imported from the UK at a 10% tariff, down from 27.5%; vehicles exceeding the quota face the full 27.5% rate. UK auto parts qualify for the same 10% combined tariff. In aerospace, products covered by the WTO Agreement on Trade in Civil Aircraft are tariff-free, removing a 10% universal tariff on jet engines and aircraft components. On steel and aluminium, the position is more uncertain: the UK could see the current 25% rate on steel, aluminium, and derivative goods removed, contingent on meeting US supply chain security requirements, but other countries face a 50% rate. UK negotiators told Parliament that the Trump administration made clear China was the intended target of those security conditions.

The UK conceded ground, too. The deal includes mutual quotas on beef and a UK commitment to import 1.4 billion litres of US bioethanol tariff-free, and the UK has eliminated its 20% tariff on US ethanol imports. Pharmaceuticals secured exemptions from potential Section 232 tariffs for at least three years.

What did not happen is as important as what did. The US Trade Representative’s own fact sheet noted that “the United States is disappointed that the UK was unwilling to agree to fully address its discriminatory Digital Services Tax”. The 2% UK levy collected $3.1 billion between 2001 and 2024, almost entirely from US companies, and Washington views it as a tax on American firms rather than British activity. In December 2025, the US suspended implementation of the linked Tech Prosperity Deal, frustrated with what officials saw as slow UK progress on digital trade and food safety standards. The autumn UK budget confirmed the digital services tax would continue.

This is the deal that British exporters now trade under. The Business and Trade Committee’s September 2025 report described it bluntly: “the very best deal that the UK could have hoped for under the circumstances,” but also acknowledged that “UK exporters are now trading with our most significant single trading partner on terms which are worse than before President Trump came to office”. On 13 April 2026, the Committee launched a follow-up inquiry citing concerns that the EPD “is not yet delivering for growth”.

Lords Report: End of Sentimentality

Six days before Charles touched down at Andrews, the House of Lords International Relations and Defence Committee published a report whose central recommendation framed the entire visit. Titled Adjusting to new realities: rebalancing the UK-US partnership, it was published on 22 April 2026 after taking evidence from all four living former British ambassadors to Washington.

The conclusion was not soft. The committee urged the UK to “dismiss previous sentimentality about a ‘special relationship'” and to recognise that future US ties will be “far more transactional and interest-based”. Lord Robertson, the committee chair and a former NATO secretary general, told reporters that “the UK must move beyond the sentimental notion of a ‘special relationship’… Overall, the United States is becoming more transactional and interest-based, with likely shifts between administrations holding markedly different views raising questions about the consistency of US commitments”.

The committee’s economic chapter is the one that matters for trade analysts. Its diagnosis was that “economic ties are being severely tested with the re-emergence of economic nationalism in the US manifesting in the form of tariffs, export controls and supply chain re-shoring,” and that “the UK must recalibrate its approach and develop a more balanced trade strategy with European partners and beyond to provide greater resilience”. Translated, that is a recommendation to hedge: keep the US relationship working, but stop pretending it will deliver the deep market access the post-Brexit pivot was supposed to produce.

The report is one of two parliamentary findings pointing in the same direction. The Joint Committee on the National Security Strategy reached a similar conclusion in March 2026, arguing the UK should “move away” from over-reliance on Washington for defence and security, given “demonstrable areas of tension” between London and the White House. The Lords committee was simply more explicit about the economic implications.

From Empire to Economic Interdependence

Some history clarifies what is and is not new. Britain was the world’s leading economy for most of the nineteenth century. By the 1880s, the United States had overtaken it in industrial output. By the 1920s, New York had displaced London as the centre of global finance, accelerated by Britain’s First World War debts. Bretton Woods in 1944 formalised the changing of the guard: an American-anchored dollar system replacing the sterling-anchored gold standard that had structured global trade for almost a century. Lend-Lease shipped American materiel across the Atlantic to keep Britain in the war and tied the postwar order to Washington in a way that has not loosened since.

The phrase “special relationship” comes from Winston Churchill’s 1946 Fulton speech in Missouri. It was always more a British description than an American one. Sir Christopher Meyer, who served as British ambassador in Washington from 1997 to 2003, observed that among younger Americans “the mythology of the ‘special relationship’ and its history were terra incognita”, and that demographic shifts were producing an America less instinctively oriented towards Britain with each census. That observation, made in the early 2000s, is now the consensus diagnosis in the Lords’ report.

The high points of the modern era were the Thatcher-Reagan alignment of the 1980s, when ideological convergence on deregulation and the Cold War made London and Washington effectively co-pilots of free-market economics, and the 1990s coordination on financial liberalisation. The low points include Suez in 1956, when President Eisenhower forced Britain and France to abandon the canal operation by threatening to dump UK debt; the Wilson government’s refusal to send troops to Vietnam in the 1960s; and now Starmer’s refusal to commit British forces to the Iran war. Each rupture revealed the asymmetry in cold relief: the US can act without Britain, Britain cannot act against the US.

For more on the global financial architecture this history produced, see our companion article on the evolution of the international monetary system and the gold standard era.

Soft Power and Hard Trade Numbers

Royal visits have a measurable economic record, even if causal attribution is messy. When Trump made his second UK state visit in September 2025, the British government secured £150 billion in inward investment commitments from US firms, the largest commercial package ever announced during a state visit. Blackstone alone pledged £100 billion over a decade, with Microsoft committing £22 billion to AI infrastructure and Google £5 billion to expand its UK data centre. Palantir, CoreWeave, BlackRock, Salesforce, and OpenAI added further pledges. The package was timed precisely to coincide with the royal banquet at Windsor.

What is investment, what are recycled commitments, and what is genuinely new is harder to disentangle. Independent analysts noted that “the numbers are inconsistent and thin on detail”, with much of the Blackstone figure aggregating existing data centre projects with new commitments. But the political signal was unambiguous: the United Kingdom was the first significant economy to absorb the new tariff architecture, sign a framework deal, and convert state pageantry into headline-grade investment commitments.

Charles’s Washington visit operates by similar logic in reverse. The King cannot directly negotiate trade terms or address the digital services tax. He can, however, anchor the meeting in a frame that the president responds to: ceremony, history, monarchy. The Wednesday business reception at Rockefeller Center, where Charles met chief executives from Bank of America, JP Morgan, Blackstone, Citigroup, Comcast, and Alphabet, was the practical follow-through. None of those meetings will produce announcements rivalling the September 2025 package, because the asymmetry runs the other way: Britain wants something from the US that the US is not currently inclined to give, namely a fuller free trade agreement and resolution of residual tariffs.

This is what economists mean by soft power having declining returns in a transactional environment. The currency of the ceremony is influenced at the margin. Where the underlying commercial logic is mutually attractive, ceremony lubricates a deal. Where the underlying logic has shifted, ceremony cannot reverse it.

Ripples Beyond the UK‑US Relationship

The strain on the UK-US relationship matters beyond the two countries because both have, since 1945, been the principal architects of the rules-based international economic order. The Bretton Woods institutions, the GATT-WTO system, the freedom of navigation regime, the dollar-sterling clearing infrastructure, and even the modern accounting and corporate governance norms used in capital markets globally all carry Anglo-American fingerprints.

The Lords’ report makes this point explicitly. “Confidence in sustained US international engagement has dissipated as the gulf between the UK and US on the relevance of the rules-based system and international law has widened under the current administration”. When the largest and fifth-largest economies that built that system stop coordinating on its maintenance, the system itself becomes less stable. We have explored related themes in our coverage of the global tariff war of 2025-2026, the strain on global supply chains, and the broader pattern of five shocks in five years.

The Iran war of 2026 sharpened this point. The United States and Israel struck Iranian targets without British military participation. The Lords committee noted that the conflict, far from being a departure from the broader trends, fits the pattern: “the conflict in Iran, not necessarily a departure from these trends”. Britain bore the economic costs of the Strait of Hormuz disruption (we covered this in detail in our Hormuz analysis) without the agency of having shaped the decision that produced them. That dynamic, exposure without agency, is why the parliamentary committees recommend hedging towards Europe.

For Brussels, a Britain looking to diversify away from over-reliance on Washington is welcome news for the EU’s own bargaining position with the United States. For other US allies (Canada, Australia, Japan), the British template of accepting a 10% baseline tariff in exchange for a partial deal is now the working benchmark. The September 2025 US-UK Tech Prosperity Deal, signed at Chequers and now suspended, was designed to be replicable. Whether it gets unsuspended will tell us whether the EPD framework still has political momentum or has effectively stalled.

Trade Trends in One Chart

The chart below tracks UK goods trade with the United States from 2010 through early 2026, with markers for the events that shaped each phase.

UK goods exports to the United States, monthly £ billions. Vertical markers show: Brexit referendum (June 2016), Trump tariffs round one (March 2018), COVID shock (March 2020), Liberation Day tariffs (April 2025), EPD signed (May 2025), Tech Prosperity Deal suspended (December 2025). Source: ONS UK Trade in Goods data and HMRC overseas trade statistics.

Two patterns stand out. First, goods trade grew almost continuously from 2010 through 2024, weathering the Brexit vote, the first round of Trump-era tariffs in 2018, and even the COVID disruption with relative resilience. The bilateral relationship had absorbed shocks before. Second, the post-April 2025 inflection is sharper than any previous episode. UK exports to the US in the quarters following Liberation Day are running well below their 2024 trajectory, and the EPD has not yet reversed the slide. The trend is consistent with what economists would predict from a 10% baseline tariff plus selective sectoral exemptions: aggregate volumes contract because the carve-outs do not cover the full mix of goods that previously flowed.

Diplomatic Milestones and Economic Deals

To put the current moment in context, the table below catalogues the major US-UK diplomatic milestones of the past century alongside their economic outcomes.

| Year | Event | Economic Outcome |

|---|---|---|

| 1941 | Atlantic Charter (Roosevelt-Churchill) | Framework for postwar Bretton Woods order |

| 1944 | Bretton Woods Conference | Dollar replaces sterling as anchor currency |

| 1956 | Suez Crisis (UK-US split) | US Treasury threats force UK retreat; sterling devalued |

| 1957 | Queen Elizabeth II first Washington visit | Restoration of trust after Suez |

| 1991 | Queen Elizabeth II addresses Congress | Reaffirms alliance after Cold War; Gulf War coalition |

| 2003 | Iraq War coalition | £8 billion+ direct UK military cost; political damage |

| 2007 | Queen Elizabeth II final state visit | Pre-financial-crisis; trade running at then-record levels |

| 2020 | UK leaves EU; FTA talks open | Atlantic Declaration (2023) limited; full FTA stalls |

| Sept 2025 | Trump second UK state visit | £150 billion US investment package; Tech Prosperity Deal |

| May 2025 | Economic Prosperity Deal signed | 10% baseline tariff; auto quota; aerospace zero |

| Dec 2025 | Tech Prosperity Deal suspended | Digital services tax dispute halts implementation |

| April 2026 | King Charles III state visit | Pending; reception with US CEOs in New York |

| ||

Sources: UK National Archives; House of Commons Library research briefings; UK Government press releases; Reuters, BBC News, AP News reporting.

One observation runs across the timeline: every period of high-stakes UK-US economic coordination has been preceded or followed by a serious diplomatic rupture. The 1956 Suez split produced the 1957 royal restoration. The 2003 Iraq cooperation produced the long bilateral chill of the late Bush and early Obama years. The current moment may follow the same cyclical logic, or it may not. The Lords committee’s argument is that the structural drivers (China-focused US strategy, economic nationalism, demographic shift) are no longer cyclical but secular. If they are right, the cycle has broken.

What a Royal Visit Can and Cannot Achieve

The honest assessment of the visit’s economic impact is constrained by what a constitutional monarch is permitted to discuss. Charles cannot negotiate tariff schedules. He cannot offer concessions on the digital services tax. He cannot open or close North Sea drilling licences. He cannot publicly disagree with the prime minister or the president on any matter of contested policy. What he can do is reinforce the legitimacy of the broader alliance frame within which negotiators operate, signal continuity of values where there is consensus (NATO, Ukraine, climate science, condemnation of political violence), and provide a setting in which business leaders meet government counterparts in productive informality.

His Congressional address did exactly this. It praised democratic traditions stretching back to Magna Carta, named NATO and AUKUS, and made a specific reference to Ukraine without addressing Iran. The careful omission of Iran respected the constitutional convention of not commenting on contested foreign policy, while the inclusions made his disagreements with the Trump administration’s positions clear by their selection. The Wednesday CEO meetings at Rockefeller Center were the operational complement: a King’s Trust event followed by direct engagement with the chief executives of firms whose investment decisions move the needle on UK growth.

What the visit cannot do is reverse the structural drivers identified by the Lords committee. The 10% baseline tariff was not designed for the UK specifically; it is a feature of the new American trade architecture that the UK happens to face alongside most other partners. The digital services tax is a fiscal instrument rooted in domestic UK policy, not a diplomatic gesture. The reluctance to join the Iran war reflects parliamentary politics in a country where the legacy of the 2003 Iraq vote still constrains the executive. None of these will move because Charles addressed Congress.

MASEconomics Explains

4 economic concepts behind the US UK economic relationship

Conclusion

The US UK economic relationship remains the largest single bilateral commercial bond either country maintains, with around £315 billion in annual two-way trade and £1.2 trillion in mutual investment. The visit of King Charles III to Washington, New York, and Virginia from 27 to 30 April 2026 has reaffirmed the symbolic architecture of that relationship at a moment when its economic substance is under measurable strain. UK goods exports to the United States fell 10.3% in 2025, the first annual decline since the pandemic. The Economic Prosperity Deal of May 2025 secured selective tariff carve-outs but left a 10% baseline tariff in place and the digital services tax dispute unresolved. The Tech Prosperity Deal has been suspended since December 2025. The House of Lords committee report of 22 April 2026 concluded that future relations will be “transactional and interest-based” and urged Britain to dismiss “previous sentimentality” about a special relationship.

The pageantry of the King’s address to Congress and the awkwardness of the president’s protocol breach at the state dinner are two faces of the same underlying fact. The relationship retains enormous economic mass and significant institutional depth. Its political superstructure has been remade. The two countries now operate within tariff schedules, regulatory disputes, and strategic divergences that did not exist five years ago.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.