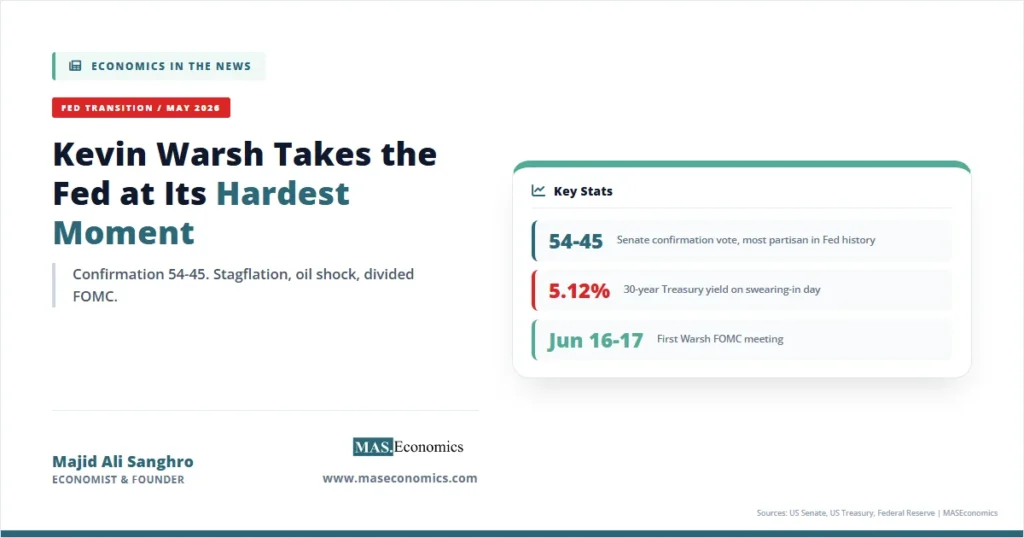

Kevin Warsh Fed chair arrived on May 15, 2026, two days after a 54-45 Senate vote made him the 17th leader of the Federal Reserve, and the same week Jerome Powell’s eight-year term expired. The transition coincided with the largest oil supply shock on record, an April CPI print pushing inflation back above the Fed’s 2 percent target for a sixth straight year, and a 30-year Treasury yield closing at 5.12 percent, its highest level since May 2025.

The combination is unforgiving. Warsh inherits a divided Federal Open Market Committee, a White House that publicly demands rate cuts, and a stagflationary backdrop that argues against them. His first policy meeting is set for June 16-17. Markets are pricing a 97 percent probability that the federal funds target range stays at 3.50-3.75 percent, with rate-hike odds rising to 20 percent for October and 30 percent for December. The man who once called for “regime change” at the central bank now has to run it.

How the Confirmation Unfolded

The path to confirmation was the most contested in the modern history of the Fed. The Senate voted on Wednesday, May 13, splitting almost entirely along party lines. Only Senator John Fetterman of Pennsylvania crossed over from the Democrats, giving Warsh a 54-45 margin. As CNBC reported on the day of the vote, this was the closest confirmation tally for a Fed chair in the modern era.

The bottleneck was Senator Thom Tillis of North Carolina, who blocked the nomination from advancing until the Department of Justice withdrew an investigation into Powell tied to testimony Powell had given Congress on cost overruns at the Fed’s Eccles Building renovation. The probe, originally led by US Attorney Jeanine Pirro, was widely interpreted as political pressure on a sitting chair who had refused to cut rates on the White House’s preferred schedule. Pirro dropped the case but signalled she could reopen it if the Fed’s inspector general found cause. The episode is now part of the public record on the threats to central bank independence that have defined this transition.

Warsh’s previous government service informed the contest. He served on the Board of Governors from 2006 to 2011, became the youngest governor in Fed history at 35, and was the principal liaison between the central bank and Wall Street during the 2008 financial crisis. He resigned over disagreements with Ben Bernanke’s second round of quantitative easing, an objection he has repeated for fifteen years. He spent the intervening period at the Hoover Institution and on multiple corporate boards, accumulating personal wealth of roughly $100 million, which made him the wealthiest incoming Fed chair in the institution’s history and required an extensive divestiture programme before he could take the chair.

Powell’s term as chair ended Friday, May 15. Powell himself signalled at his final press conference on April 29 that he would remain on the Board of Governors as a regular member, a position he is entitled to hold until January 31, 2028. This is highly unusual. The last sitting chair to remain on the board after stepping down was Marriner Eccles in 1948, and that decision was treated at the time as a direct rebuke of White House pressure. Eccles’s confrontation eventually produced the 1951 Treasury-Fed Accord, the foundational document of modern Fed independence. The parallel is not subtle.

| Date | Event | Significance |

|---|---|---|

| Late January 2026 | Trump nominates Kevin Warsh | Shifts prediction market odds; 10-year yield rises above 4.20% |

| Apr 21, 2026 | Senate Banking Committee confirmation hearing | Warsh discloses ~$100M asset divestiture requirement; testifies on Fed framework reform |

| Apr 29, 2026 | Powell’s final FOMC press conference | FOMC holds at 3.50-3.75%; 8-4 split, the most dissents since October 1992 |

| May 8, 2026 | April Jobs Report released | Labour market signals slowdown ahead of leadership change |

| May 12, 2026 | April CPI released | Headline up 0.6% MoM; sixth year above 2% target |

| May 13, 2026 | Senate confirms Warsh 54-45 | Most partisan Fed chair vote on record; Fetterman the sole Democratic yes |

| May 13, 2026 | April PPI released | Wholesale prices up 6% YoY; sharpest reading since 2022 |

| May 15, 2026 | Powell’s term as chair expires; Warsh sworn in | Powell retains governor seat through Jan 2028 |

| May 15, 2026 | Treasury yields surge | 30-year reaches 5.12%, 10-year 4.60%, 2-year 4.08% |

| Jun 16-17, 2026 | Warsh’s first FOMC meeting | 97% market probability of hold; rate-hike odds rising for Q4 |

| ||

The Stagflationary Inheritance

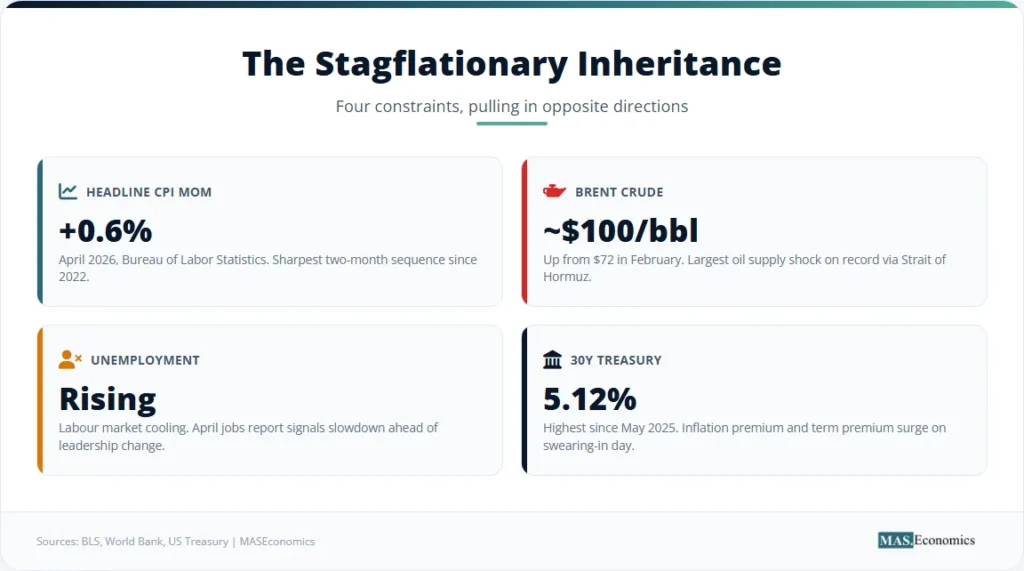

The macroeconomic situation Warsh inherits is harder than the one Powell handed Volcker in 1979 in one specific respect. Volcker faced inflation alone. Warsh faces inflation plus a supply shock that is still active, plus a labour market that has begun to cool, plus a Treasury market signalling concern about fiscal sustainability through the term premium. The four constraints pull in different directions.

The inflation problem starts with the data. According to the Bureau of Labor Statistics’ April CPI release, headline consumer prices rose 0.6 percent month over month in April, following a 0.9 percent increase in March. That is the sharpest two-month sequence since 2022. Wholesale prices, measured by the Producer Price Index, rose 6 percent year over year. The PCE deflator, which the Fed prefers, has remained above the 2 percent target every year since 2021, the longest sustained overshoot since the early 1980s. Our detailed US CPI April 2026 analysis walks through how much of the print is energy pass-through and how much is genuine stickiness in services.

The energy component is the new shock. Brent crude, which traded near $72 a barrel at the end of February, surged to a peak of $120 in March before settling near $100 as Warsh took office. The cause is the US-Israeli war with Iran, which began on February 28 and has disrupted shipping through the Strait of Hormuz. The World Bank Commodity Markets Outlook for April 2026 documents the initial supply disruption at roughly 10 million barrels a day, the largest single oil shock on record. Energy prices are forecast to rise by 24 percent for 2026 in the baseline and as much as 35 percent in the World Bank’s stressed scenario.

The labour market complicates the picture in the opposite direction. The April jobs report, covered in detail in our labour market slowdown read, showed unemployment edging higher with weak nonfarm payroll gains. The classic stagflationary mix is now in place: rising prices, weakening employment, and a supply shock outside the Fed’s control. The textbook prescription is to hold rates, because cutting fuel prices, inflation, and hiking rates deepens the labour weakening. That is exactly the path the FOMC chose in April.

The fiscal constraint is the third dimension. The federal debt is approaching $39 trillion. Treasury auctions through the spring have absorbed steadily larger issuance against a backdrop of foreign reserve managers reducing duration. The 30-year yield closing at 5.12 percent on May 15 is the highest since May 2025 and reflects a combination of inflation premium and term premium. As CNBC reported on the day of Warsh’s swearing-in, the move was sharp and broad-based: 10-year yields rose 14 basis points to 4.595 percent, 2-year yields rose 9 basis points to 4.079 percent, and the long end did most of the heavy lifting. The market is asking, in real time, what the new chair believes.

Warsh’s Stated Framework

Warsh’s policy framework is documented in fifteen years of Hoover Institution lectures, op-eds, and CNBC appearances. The shorthand is that he is hawkish on inflation, dovish on the labour market, sceptical of the balance sheet, and uncomfortable with the Fed’s expanded role in financial stability. A more precise reading distinguishes four positions that will shape his chairmanship.

First, Warsh believes the Fed’s preferred inflation gauge is inadequate. In his April 21 confirmation hearing, he argued that the Personal Consumption Expenditures index, even excluding food and energy, gives only a rough read of price pressures. He has called for a different framework that places more weight on market-based prices, asset price inflation, and forward-looking expectations. The implication is that he could be willing to look through energy-driven inflation spikes that he judges transitory, while taking a harder line on services components that show genuine stickiness.

Second, Warsh views the Fed balance sheet as too large. He has consistently argued that the central bank should accelerate quantitative tightening rather than tolerate the $7 trillion holdings it inherited from the pandemic period. The full case sits in our piece on quantitative tightening explained, but the policy implication is concrete: under Warsh, the balance sheet runoff cap could be increased, or the reinvestment of agency mortgage-backed securities into Treasury bills could be reconsidered. Either would tighten financial conditions independently of the funds rate.

Third, Warsh has been openly critical of the Fed’s flirtation with average inflation targeting, the framework adopted in 2020. He views it as having locked the Fed into a tolerance for overshoots that proved catastrophic when the post-pandemic inflation surge hit. He has hinted he will use the Fed’s quintennial framework review to abandon the AIT regime in favour of a flexible inflation targeting approach closer to the pre-2020 standard.

Fourth, Warsh wants what he calls “messier” FOMC meetings. He told the Senate Banking Committee that a “good family fight” produces better economic decisions than consensus pressure. He is unlikely to attempt the unanimity that Powell maintained for most of his tenure. The April meeting already showed the model breaking down: the 8-4 split was the most dissents since October 1992, with three regional bank presidents and one governor voting against language that hinted at further cuts. Warsh will inherit that fracture and is unlikely to suppress it. The lay of the existing fault lines is documented in our coverage of Powell’s final rate decision.

The Independence Question

The single largest market concern is not Warsh’s policy preferences. It is whether he will defend the Fed’s institutional independence against an administration that has openly demanded rate cuts. The pattern of pressure is now extensive and on the record.

Trump has called Powell a series of unflattering names since 2025, repeatedly demanded rate cuts on social media, attempted to fire Governor Lisa Cook on mortgage-fraud allegations that a federal judge ruled were pretextual, and publicly hinted he would “sue Warsh if he doesn’t cut rates.” The DOJ probe into Powell’s renovation testimony, which Tillis used as leverage during confirmation, has been characterized by a federal judge as a transparent attempt to pressure resignation. Powell’s decision to remain on the Board of Governors rather than depart entirely is the Eccles precedent: a sitting institution defending its legal architecture.

The textbook case for independence is set out in our explainer on central banking and monetary policy. Empirically, central banks that operate under political control deliver higher and more variable inflation, weaker currencies, and higher borrowing costs over time. The market understands this. The 30-year yield is in many ways a vote on the question of independence, since long-duration assets are most sensitive to inflation risk premia. The 5.12 percent reading on the day of Warsh’s swearing-in is the bond market pricing the risk that the new chair, whatever his hawkish instincts, may eventually fold to White House pressure.

Warsh’s own statements on independence are deliberately ambiguous. In the April 21 hearing, he stated that the Fed must remain independent in the conduct of monetary policy, while also conceding that the institution had earned scrutiny through what he called overreach into financial regulation, climate analysis, and fiscal backstopping. The distinction matters. Independence in rate-setting is a constitutional doctrine. Independence in regulatory mandate is a political settlement that Congress can adjust. Warsh appears prepared to defend the first while permitting the second to be reopened.

The first test will come at the June FOMC. If Warsh leads the committee to a hold despite presidential pressure for a cut, the bond market will likely reward him with a moderation of the term premium. If he leads to a cut that the underlying data do not support, the Treasury reaction could be severe. The Eccles parallel of 1948-1951 is instructive: it took two and a half years of escalating market pressure before the Treasury-Fed Accord re-established the principle of monetary policy independence. The system tolerates encroachment for a time. The system also breaks.

How Markets Are Pricing the Transition

The Treasury curve carries the most direct read on what investors think the Warsh chairmanship means. The picture as of mid-May is a curve that has bear-steepened: short rates have risen modestly, long rates have risen sharply. That pattern is the classic market response to an inflation regime in which the central bank is expected to maintain real rates restrictive, but the long-run inflation expectation has drifted higher.

The curve steepening tells a story. If the market expected Warsh to deliver aggressive rate cuts under political pressure, the 2-year yield would have fallen, since cuts compress the short end first. Instead, the 2-year rose by roughly 23 basis points across the confirmation week, signalling that traders see no near-term cut. If the market believed the Fed would hold the line on inflation indefinitely, the 30-year yield would have fallen, since restrictive policy controls long-run inflation expectations. Instead, the 30-year rose by 34 basis points, signalling that traders are demanding a higher inflation risk premium for holding long duration.

Translated, the bond market view is this: the Fed will probably hold in the short run, but the long-run inflation regime is now perceived as more uncertain than it was under Powell. The yield curve is the cleanest single indicator of this shift. Our explainer on what bond markets tell us walks through how to read these signals in detail.

Equities have responded differently. The S&P 500 reached an intraday high above 7,230 on May 1 and has remained near that level through the confirmation week. Bank stocks, in particular, have rallied on the expectation that Warsh’s regulatory framework will be lighter than Powell’s. That equity strength is what some analysts have called the “Warsh trade.” The disconnect between equities and bonds is unusually wide, and at least one credible analyst at Energy Aspects has characterized the equity calm as “misplaced euphoria” given the underlying oil shock. The standard pattern after every major oil disruption since 1973 has been a delayed but predictable contraction. The current cycle has been characterized by what we describe in our piece on global economic resilience as repeated underestimation of supply-side shocks until the data forces revision.

The June FOMC Test

Warsh’s first meeting as chair takes place June 16-17. It is also a Summary of Economic Projections meeting, meaning the FOMC will publish updated dot plot forecasts for growth, inflation, unemployment, and the federal funds rate path. The June SEP will be the first formal document of the Warsh era and will be read with extreme care.

Three outcomes are plausible at the June meeting. The first is a hold at 3.50-3.75 percent with a dot plot showing one cut by year-end. This is consistent with current market pricing and would represent continuity from Powell’s April framework. The risk of this outcome is that it disappoints the White House without satisfying the inflation hawks, leaving Warsh exposed to political pressure with no policy victory to point to.

The second outcome is a hold with a hawkish dot plot showing no cuts in 2026 and the long-run rate revised higher. This would be the most consistent path with Warsh’s stated framework, which views the current funds rate as still below neutral. It would likely produce a rally in the dollar, a flattening of the curve from the long end, and a sharp negative reaction from the White House. The full discussion of monetary divergence across major central banks during this period is in our piece on central bank divergence in 2026.

The third outcome is a cut of 25 basis points, justified by the labour market slowdown and dismissing the recent inflation print as an energy pass-through. This would align Warsh with the White House. It would also produce an immediate spike in long-end yields as the bond market re-prices its inflation expectations. The 30-year is already near 5.12 percent. A cut deemed political could push it through 5.50 percent, with cascading effects on mortgage rates, corporate credit, and emerging-market debt.

The historical analogue worth keeping in mind is the 1972 Arthur Burns precedent. Burns cut rates ahead of the 1972 election under documented pressure from the Nixon White House, the subsequent inflation surge required Volcker’s response in the early 1980s, and the cost was a deep recession. Warsh has read this history. Whether his framework or his political position dominates is the question the June meeting will answer.

Reading the Warsh Era

Several propositions follow from the conditions Warsh has inherited and the framework he has articulated. None are predictions of certainty. All are testable against the next twelve months of policy and price action.

The first proposition is that the balance sheet will become a more active policy lever. Warsh’s long-standing scepticism of quantitative easing suggests that QT will accelerate rather than ease, and that the reinvestment of agency MBS into Treasury bills may be reviewed. This would tighten financial conditions in mortgage markets independently of the funds rate, an option that gives Warsh political cover for holding the policy rate steady while still pursuing a hawkish overall stance.

The second proposition is that the Fed’s regulatory mandate will narrow. Warsh has been consistently critical of what he calls mission creep, particularly into climate, financial-stability backstopping of non-bank intermediaries, and the post-2008 bank stress-test regime. Expect proposed simplifications to stress tests, a roll-back of climate analysis at the Fed, and renewed Congressional debate about the perimeter of Fed authority. Banks have already priced in some of this through the equity rally.

The third proposition is that average inflation targeting is dead. The 2020 framework that allowed inflation to run above 2 percent to compensate for prior undershoots is widely understood at the Fed to have contributed to the slow response of 2021-2022. Warsh will use the 2026 framework review to abandon AIT and return to a symmetric inflation target with no backward-looking averaging. This is a small technical change with a large signalling effect: it tells markets that future overshoots will be met with faster tightening.

The fourth proposition is the one that matters most. The independence of the Federal Reserve is now a continuous test, not a binary state. Each FOMC decision under Warsh will be read in two registers, one for policy substance and one for institutional posture. Powell’s decision to remain on the board makes the Eccles parallel explicit. The 1951 Accord did not come easily, and the current pressure on the Fed has not yet reached the intensity of the 1948-1951 episode. But the trajectory is the same. The market is watching whether the institutional architecture holds.

MASEconomics Explains

Four concepts behind the 2026 Fed transition

These concepts are explored in depth across our educational articles library.

Explore the MASEconomics BlogConclusion

Kevin Warsh Fed chair begins his term on May 15, 2026, inheriting the most difficult macroeconomic position any incoming chair has faced since Paul Volcker took office in 1979. The Senate confirmation vote of 54-45 was the most partisan in the history of the office. The federal funds rate sits at 3.50-3.75 percent. April CPI came in at 0.6 percent month over month against a backdrop of Brent crude trading near $100. The 30-year Treasury yield closed at 5.12 percent on the day of his swearing-in, the highest since May 2025. His first FOMC meeting is set for June 16-17.

The constraints on his chairmanship are well defined. The administration wants rate cuts. The inflation data argue against them. The labour market is cooling. The bond market is demanding a higher term premium. Powell remains on the Board of Governors, a fact that frames every future vote. The framework Warsh has articulated over fifteen years suggests a hawkish bias on the policy rate, an accelerated balance sheet runoff, and a narrower regulatory mandate. Whether that framework survives contact with political pressure is the question of the next twelve months.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics