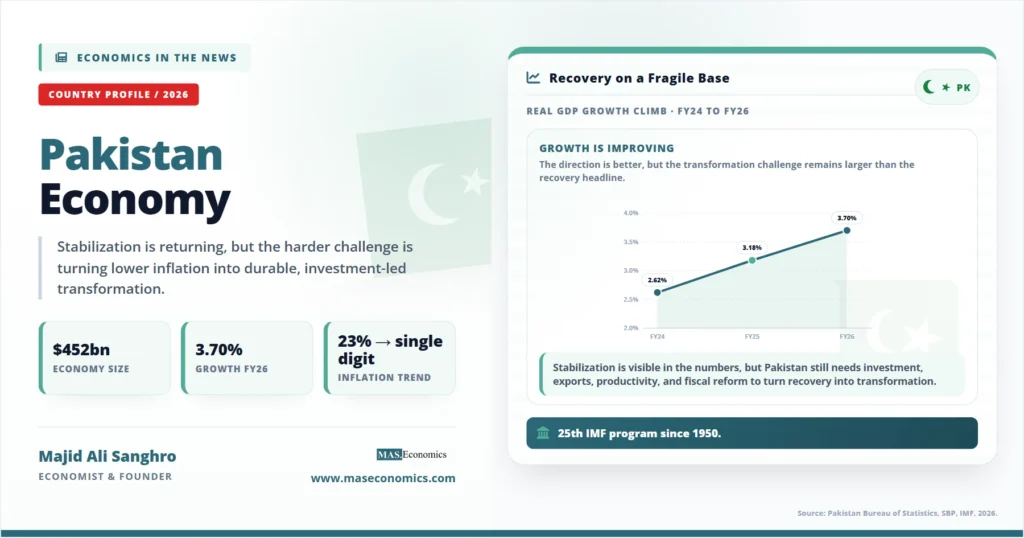

In May 2026, Pakistan’s economy crossed $452 billion in nominal terms for the first time, with provisional growth of 3.70% for the 2025-26 fiscal year. It was the third consecutive year of acceleration, following a near-default in 2023 that had brought the country within weeks of running out of the foreign currency it needed to pay for imports. The Pakistan economy had engineered one of the more striking macroeconomic reversals in the region: inflation cut from above 23% to a single digit, real growth rebuilding, foreign reserves climbing back, and the State Bank able to cut its policy rate from a record 22% to 10.5%. On paper, this is a recovery worth taking seriously.

The harder question is whether it is a turning point or another lap of a familiar circuit. With the 2024 program, Pakistan entered roughly its twenty-fifth arrangement with the International Monetary Fund since joining in 1950, a number that describes the central feature of its economic history better than any single growth figure. For more than half a century, the country has cycled through booms financed by external inflows and debt, followed by balance-of-payments crises and bailouts. Understanding Pakistan means holding two truths at once: the stabilization underway is genuine, and the structural traps that defeated every previous recovery are still in place.

Shape of a $452 Billion Economy

Pakistan is a lower-middle-income economy of roughly 240 to 250 million people, the fifth-most-populous country in the world. At market exchange rates, its output is around $452 billion, giving a per capita income near $1,900. Measured by purchasing power parity, which adjusts for the lower cost of locally produced, non-traded goods and services, the economy ranks among the 25 to 30 largest in the world. That gap between the market and PPP rankings is itself informative: the domestic market is far larger and more dynamic than the dollar figure implies, but the country earns relatively few dollars per unit of activity, which is the root of its external fragility.

The structure of output follows the path of a developing economy partway through transformation. Services are now the largest sector, generating close to 58% of GDP, spanning wholesale and retail trade, transport and logistics, telecommunications, and financial services. Industry, including manufacturing, construction, and utilities, accounts for roughly 18 to 19%, with textiles alone making up a large share of manufacturing output. Agriculture contributes around 23% of GDP but employs close to 40% of the workforce, a mismatch that captures one of the economy’s deepest problems: a huge share of Pakistanis work in low-productivity farming, which holds down average incomes and leaves rural households exposed to every flood and drought.

The demand side is where Pakistan diverges most sharply from comparable economies. Growth is driven overwhelmingly by household consumption, which accounts for over 80% of GDP, while investment is low and net exports are persistently negative. An economy that consumes this much and invests this little cannot easily build the productive capacity, factories, infrastructure, and skills that would let it grow faster without importing more than it sells. This consumption is sustained to an unusual degree by inflows from abroad rather than by domestic earnings, and that single fact shapes almost everything that follows.

Young Population and Slow Job Market

Pakistan’s most important long-run economic fact is its age structure. The 2023 census counted roughly 241 million people, and the population continues to grow at close to 2% a year, among the highest rates in any large economy. Around 64% of Pakistanis are under the age of 30. Each year, on the order of two million young people enter the labour force, and estimates suggest the country needs to generate well over a million new jobs annually just to absorb them.

In development economics, this configuration is known as a potential demographic dividend: a period when the working-age share of the population is large relative to dependents, which can accelerate growth if those workers are educated, healthy, and employed productively. The economies of East Asia converted exactly this kind of age structure into decades of rapid growth. The dividend is not automatic, however. It requires investment in schooling, skills, and job creation ahead of the bulge. Where those investments are missing, a young population becomes a source of unemployment, underemployment, and emigration rather than growth.

Pakistan sits on the knife-edge between these outcomes. Youth unemployment runs near 10%, skills mismatches are widely reported by employers, and a significant share of the country’s most capable young workers emigrate, particularly to the Gulf. That emigration is double-edged. It relieves domestic labour-market pressure and generates the remittances that keep the external accounts afloat, but it also drains human capital that a transforming economy would otherwise use at home. Whether Pakistan invests enough in its young people over the next decade is, in the long run, a more important question than any single year’s growth rate.

Remittance Lifeline and Export Gap

If the demographic story is the long-run question, the balance of payments is the recurring short-run crisis, and it turns on two numbers: what Pakistan earns from exports and what it receives in remittances.

Remittances are the country’s financial lifeline. Money sent home by the large Pakistani diaspora, concentrated in Saudi Arabia, the United Arab Emirates, and other Gulf states, reached records in the $30 billion to $35 billion range in recent years. This single inflow finances a large part of the import bill and is the most stable source of foreign exchange the country has, more reliable than exports, foreign investment, or borrowing. When remittances flow strongly through formal channels, the external accounts breathe; when they divert to informal channels because of an overvalued official exchange rate, the accounts tighten quickly. Much of the policy effort to keep the rupee at a market-determined level, including the structural reforms covered in our piece on Pakistan’s exchange companies sector, is ultimately about protecting this channel.

The weakness that mirrors the remittance strength is exports. Pakistan’s exports have fallen from around 16% of GDP in the 1990s to roughly 8 to 10% by the mid-2020s, an erosion that leaves the country chronically short of the foreign currency it needs. Total merchandise exports sit around $40 billion against imports well above $70 billion, a structural trade gap that remittances must fill. Where successful developing economies grew by selling more to the world, Pakistan has increasingly grown by consuming more at home on borrowed and remitted money.

The export base is also dangerously narrow. Textiles and apparel, a legacy of the cotton economy, account for the single largest share, on the order of $16 billion, leaving total export earnings hostage to one sector’s competitiveness, to global cotton prices, and to the energy costs that determine whether Pakistani mills can undercut rivals in Bangladesh and Vietnam. The most encouraging recent development is the rise of information technology and software exports, growing at double-digit rates from a base of several billion dollars and representing the clearest example of a new, higher-value industry emerging. The government’s medium-term plan, branded Uraan Pakistan, explicitly targets export-led growth of around 6% by 2028, prioritizing textiles, IT, agriculture, and pharmaceuticals. Broadening this base is the single most important structural task the economy faces, because an economy that earns its foreign exchange does not need a bailout every few years.

Energy, Circular Debt, and State Drain

Behind the external fragility sits a domestic problem that quietly bleeds the public finances: the power sector. Pakistan generates a large share of its electricity from imported fuel, which ties the cost of keeping the lights on directly to global oil and gas prices and to the value of the rupee. When either moves against the country, the cost of generation rises faster than the regulated prices charged to consumers.

The gap between what it costs to supply power and what is actually collected from users accumulates into what Pakistan calls circular debt, a chain of unpaid obligations running through generators, distributors, and the government. It builds because tariffs do not fully cover costs, because a significant share of electricity is lost to theft and non-payment, and because chronically loss-making distribution companies cannot collect what they bill. Circular debt has become a permanent feature of the fiscal landscape, absorbing public money that could fund schools, hospitals, or infrastructure, and reforming it, through higher tariffs, better collection, and restructuring, is one of the hardest conditions in every IMF program.

The power sector is the most visible example of a wider drain: loss-making state-owned enterprises. From the national airline to the railways to the steel mills, a portfolio of public companies requires continuous government subsidy to cover persistent losses while employing relatively few workers. These subsidies, together with circular debt and a heavy interest bill, are why Pakistan’s fiscal deficit has so often run in the range of 6 to 8% of GDP, and why the state has so little room for productive spending. The narrow tax base compounds the problem from the revenue side: a large informal economy, widespread exemptions, and weak enforcement leave the country collecting too little to cover its commitments, the challenge examined in our piece on digitalizing Pakistan’s tax system. The result is chronically thin fiscal space, the room a government has to spend or invest without endangering its solvency.

CPEC and the China Relationship

No account of Pakistan’s recent economic history is complete without the China-Pakistan Economic Corridor, the flagship of China’s Belt and Road Initiative in South Asia. Launched in 2015, CPEC channeled tens of billions of dollars into Pakistani infrastructure and energy, with the first phase concentrated on power generation that added more than 10,000 megawatts to a grid that had been crippled by load-shedding, alongside roads, ports, and the development of Gwadar on the Arabian Sea.

The corridor’s effect on the economy has been genuinely large. The energy projects helped turn Pakistan from a country defined by daily blackouts into one with adequate, if expensive, generation capacity, removing a constraint that had cost the economy an estimated couple of percentage points of GDP each year. Construction and related activity provided a meaningful growth impulse, and bilateral trade and investment with China expanded substantially.

CPEC also deepened Pakistan’s dependence and its debt. The infrastructure component was financed largely through government-to-government loans that Islamabad must service, adding to external repayment obligations, while the energy projects built under independent power producer arrangements contributed to the capacity payments that feed circular debt. The relationship binds Pakistan’s economic fortunes more tightly to Beijing, and the second phase has shifted rhetorical emphasis toward industrial cooperation and special economic zones rather than headline infrastructure. CPEC is best understood as having relaxed one binding constraint, energy supply, at the cost of tightening two others, external debt and the power-sector cost structure.

Why the Cycle Keeps Repeating

Pakistan’s economic history is not a story of steady, cumulative development. It is a sequence of booms followed by busts, a pattern that economists who study the country treat as its defining characteristic. The mechanism is remarkably consistent across cycles.

A period of strong growth, often fueled by external inflows or geopolitical rents tied to Pakistan’s strategic location, pushes up domestic demand. Because the economy cannot supply enough from its own production, imports surge faster than exports can match. The current account deficit widens, foreign reserves drain as the State Bank defends the rupee, and the country reaches a balance-of-payments crisis. An IMF program follows, bringing fiscal austerity, currency depreciation, and sharply higher interest rates. Growth collapses, the external imbalance corrects through compressed imports, reserves rebuild, and the stage is set for the next boom. The diagram below traces one full turn of this loop.

This dynamic is the textbook illustration of an external constraint on growth, where the speed limit on the economy is set not by its productive capacity but by its ability to pay for imports. The recurring crises show up in the balance of payments, and they have repeatedly forced the kind of stabilization that trades short-term pain for external survival. The 2018 to 2024 period was an especially severe version, culminating in the near-default of 2023 when reserves fell to only a few weeks of import cover, and the rupee lost a large share of its value.

Underlying the cycle are the structural problems already described: a narrow tax base, heavy debt service, loss-making state enterprises, circular debt, and a thin export sector. The IMF’s own governance assessment has estimated that the economy loses several percentage points of GDP each year to corruption and elite capture, where influential groups shape policy to protect their interests rather than to broaden growth. Each of these drains the resources or the will needed for the public investment that might lift long-run growth and break the loop.

The Current Stabilization

The recovery underway since 2023 is real, and it rests on a program of macroeconomic stabilization anchored by the IMF. In September 2024, the Fund approved a 37-month Extended Fund Facility of about $7 billion, later complemented by a Resilience and Sustainability Facility addressing climate vulnerability. The program’s conditions follow the now-familiar template: fiscal consolidation through a wider tax base and reduced subsidies, a market-determined exchange rate, tight monetary policy, and reform of the chronically loss-making energy sector.

The results so far have been better than in most past episodes. Inflation, which had peaked above 23%, fell to a multi-year low, allowing the State Bank of Pakistan to cut its policy rate by roughly 1,150 basis points from the record 22% it had reached during the crisis. Growth has climbed for three straight years. The government posted a primary fiscal surplus, the budget balance before interest payments, of around 3% of GDP in FY2025, the strongest in decades, signaling that the state was at least temporarily living within its means on a pre-interest basis. External debt fell as a share of GDP from around 31% two years earlier toward the mid-20s, and reserves rebuilt while the rupee stayed broadly stable. The table below summarizes the turnaround.

| Indicator | FY2023-24 | FY2024-25 | FY2025-26 |

|---|---|---|---|

| Real GDP growth | 2.62% | 3.18% | 3.70% (provisional) |

| Average inflation | Falling from 23%+ peak | 4.49% (nine-year low) | Within 5–7% target range |

| SBP policy rate | Up to 22% (record high) | Cut toward 11% | 10.5% (held) |

| Primary fiscal balance | Improving | ~3% of GDP surplus | Surplus targeted |

| Economy size (nominal USD) | ~$408 billion | ~$408 billion | ~$452 billion |

| Phase | Crisis and stabilization | Disinflation and recovery | Consolidating recovery |

|

Source: Pakistan Bureau of Statistics, State Bank of Pakistan, and IMF, 2024–2026. Figures provisional and subject to revision.

|

|||

The pairing of falling inflation with recovering growth is the clearest signal that this stabilization has, so far, avoided the deep recession that often accompanies IMF adjustment. The chart below shows the three variables that matter most, growth, inflation, and the policy rate, moving together through the turnaround.

The structural reforms supporting this, including in the foreign exchange market and the gradual move toward a digital financial system explored in our piece on Pakistan’s digital currency ambitions, are designed to make the stabilization durable rather than temporary. Whether they succeed is the open question.

The Vulnerabilities That Could Undo It

Stabilization is not transformation, and several pressures could pull Pakistan back into the cycle.

The first is debt. Even with external debt falling as a share of GDP, the absolute repayment burden remains heavy, and a large stock of domestic debt keeps interest costs elevated and crowds out other spending. Each year’s financing depends on rolling over maturing obligations and securing fresh inflows from multilateral and bilateral creditors, which leaves the country exposed to any loss of confidence. The mechanics of why this matters are set out in our explainer on debt sustainability.

The second is energy. Pakistan’s heavy reliance on imported fuel ties the economy directly to global oil and gas prices and to supply-route stability. The Middle East tensions of 2025 and 2026 pushed energy costs up and threatened to feed through into inflation and the import bill, the channel we examined in our coverage of how a fuel price hike affects households. An energy shock is one of the fastest routes from stability back to crisis, and it compounds the circular-debt problem at the same time.

The third is climate. Pakistan is among the most climate-exposed countries in the world despite contributing little to global emissions. The catastrophic floods of 2022 and the severe monsoon flooding since have caused enormous damage, displaced millions, and destroyed crops the economy depends on. Climate shocks hit agriculture, raise food inflation, widen the deficit through reconstruction costs, and can derail an entire year’s growth, which is why the IMF program includes a dedicated climate-resilience facility.

The fourth is the reform-execution risk that has defeated every previous stabilization. The current improvement rests on externally enforced discipline. The decisive question is whether Pakistan can convert IMF-mandated stability into homegrown structural change, a wider tax net, a broader and more competitive export base, a solvent energy sector, and reformed state enterprises before the program ends and the temptation to return to debt-financed consumption reasserts itself. The country’s record on this is precisely why its recoveries have so often proved temporary, and why each new program is numbered in the twenties. Pakistan’s place in the wider conversation about emerging-market debt and stabilization was a recurring theme at the recent IMF Spring Meetings.

Explains

Four ideas behind Pakistan’s economy

Connect these ideas to the wider library of global economy and central banking articles.

Explore the MASEconomics BlogConclusion

The Pakistan economy in 2026 is a genuine recovery built on a fragile foundation. Growth has accelerated for a third straight year to a provisional 3.70%, inflation has fallen from above 23% to single digits, reserves are rebuilding, and the country has posted its strongest primary fiscal balance in decades, all under an IMF program that has, for now, restored external viability. These achievements are real, and they pulled the country back from the edge of default it faced in 2023. Beneath them lies an economy of enormous latent potential: a young and growing population, a large domestic market, a proven export industry in textiles, a fast-rising IT sector, and an energy base rebuilt with Chinese investment.

Yet the traps that have defeated every previous recovery remain in place. The export base is too narrow, debt service too heavy, the tax net too thin, the power sector too costly, and the dependence on remittances and external borrowing too deep. Pakistan has stabilized roughly two dozen times before and returned to the boom-bust cycle each time. Whether this episode is different depends on converting IMF-enforced discipline into homegrown structural reform, above all a broader, more competitive export sector that lets the country earn its foreign exchange rather than borrow it, and serious investment in the young population that will define its labour force for decades. That transformation, not this year’s growth figure, is the measure that will determine whether Pakistan finally breaks the cycle or merely pauses within it.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics