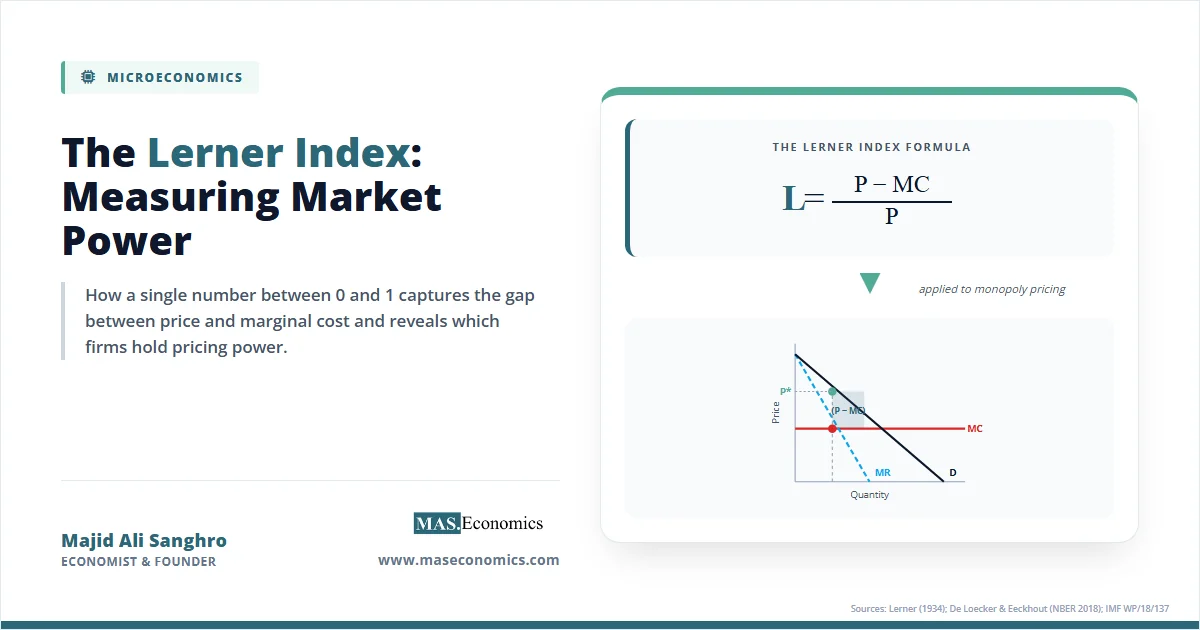

The Lerner index is the most widely used numerical measure of market power in economics. Formalised by Abba Lerner in 1934 and defined as the gap between price and marginal cost expressed as a fraction of price, it gives a single number between 0 and 1 that captures how far a firm is from competitive pricing. A perfectly competitive firm prices at marginal cost and scores 0; a pure monopolist with zero marginal cost scores 1. Eight decades after its publication, the index remains the workhorse statistic in antitrust economics, banking supervision, and the empirical study of corporate concentration.

The index has gained renewed importance in the past decade because of mounting evidence that markups have risen across advanced economies. An IMF study covering 74 economies found that the sales-weighted average markup factor rose from 1.12 in 1980 to 1.59 in 2016, an increase of 42 percent. Translated into Lerner index terms, that is a shift from roughly 0.11 to 0.37 across the global firm distribution. Understanding what the index measures, how it is estimated, and where it succeeds or fails has become central to debates about competition policy, productivity growth, and inequality.

What the Lerner Index Measures

Abba Lerner published “The Concept of Monopoly and the Measurement of Monopoly Power” in The Review of Economic Studies in 1934. The paper solved a precise problem: economists needed a way to quantify how much a firm deviates from the competitive ideal without having to specify the entire structure of the industry, count rivals, or measure market shares. Lerner’s answer was elegant. A profit-maximising firm equates marginal revenue with marginal cost. Under perfect competition, price equals marginal revenue equals marginal cost, so the wedge \( P – MC \) is zero. Any positive wedge reveals pricing power.

The formula is simple:

Here \( P \) is the price the firm charges and \( MC \) is its marginal cost at the profit-maximising output. The index is bounded between 0 and 1. At \( L = 0 \), price equals marginal cost and the firm has no market power within its market structure. As \( L \) rises towards 1, the firm captures a larger share of each sale as a markup over its incremental cost.

The deeper insight comes when the formula is combined with the firm’s profit-maximising condition. A standard result in microeconomic theory is that the Lerner index equals the inverse of the absolute value of the price elasticity of demand the firm faces:

where \( \varepsilon \) is the firm’s own-price elasticity of demand. This relationship – often called the inverse-elasticity rule – ties pricing power directly to consumer responsiveness. A firm whose customers can easily substitute away faces elastic demand and cannot sustain a high markup. A firm whose customers are insensitive to price faces inelastic demand and can charge well above cost. The link to price elasticity of demand and supply is what makes the index more than an accounting ratio: it embeds a behavioural theory of pricing.

Lerner Index Mathematical Formulation

The formal derivation begins with a profit-maximising firm choosing output \( Q \) to solve:

The first-order condition sets marginal revenue equal to marginal cost:

Rearranging gives \( P + Q \frac{dP}{dQ} = MC \). Dividing by \( P \) and using the definition of the price elasticity of demand \( \varepsilon = \frac{dQ}{dP} \cdot \frac{P}{Q} \) (so \( \frac{dP}{dQ} \cdot \frac{Q}{P} = \frac{1}{\varepsilon} \)) yields:

This is the inverse-elasticity rule. For a profit-maximising monopolist, demand at the optimum must be elastic (\( |\varepsilon| > 1 \)), since \( L \) cannot exceed 1.

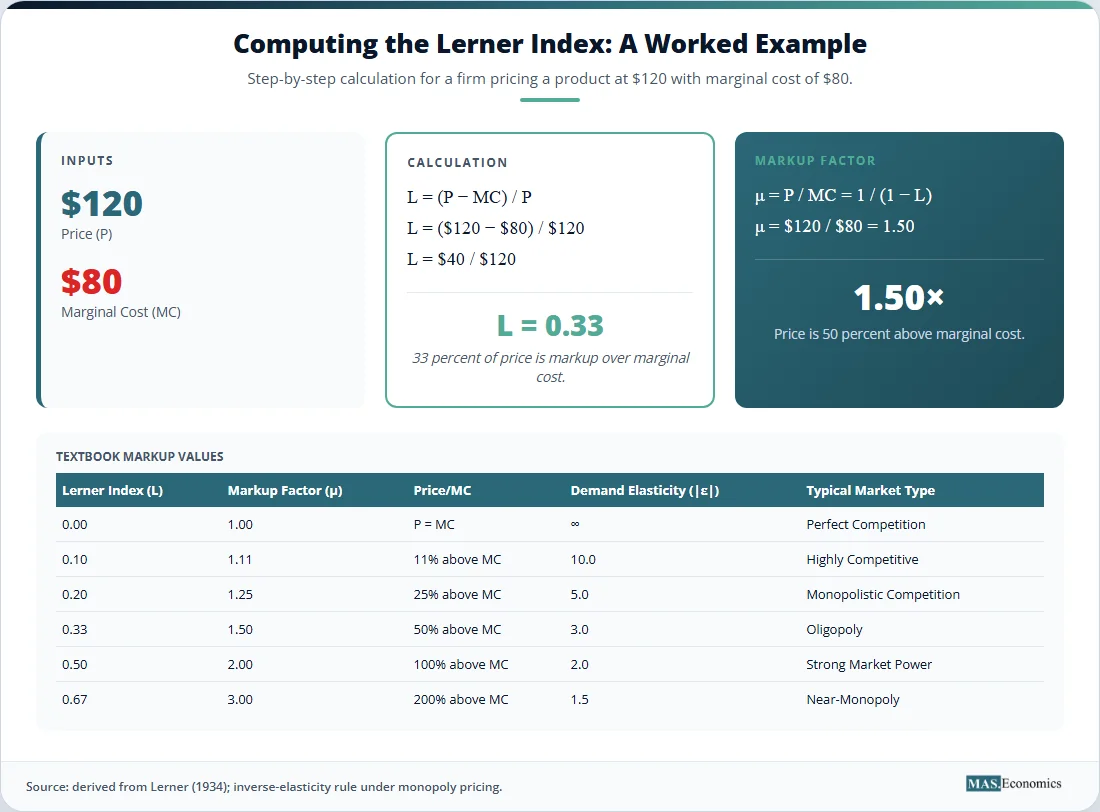

The Lerner index has a direct relationship to the firm’s markup factor \( \mu \), defined as the ratio of price to marginal cost:

So \( L = 0.20 \) corresponds to a markup factor of 1.25, \( L = 0.33 \) corresponds to 1.50, and \( L = 0.50 \) corresponds to 2.00. The two measures carry the same information, but the markup factor is what most empirical work since De Loecker, Eeckhout, and Unger’s 2020 paper in the Quarterly Journal of Economics reports.

Under Cournot competition with homogeneous products, the firm-level Lerner index has a particularly useful form:

where \( s_i \) is firm \( i \)’s market share. The sales-weighted average Lerner index across the industry then equals \( \frac{HHI}{|\varepsilon|} \), where \( HHI \) is the Herfindahl-Hirschman Index. This connects the Lerner index to structural concentration measures used in antitrust enforcement and provides a bridge between behavioural and structural diagnostics.

Variables and Notation

| Symbol | Meaning | Typical Range |

|---|---|---|

| L | Lerner index | 0 to 1 |

| P | Output price | Positive |

| MC | Marginal cost at the optimal output | Positive, ≤ P |

| ε | Firm’s own-price elasticity of demand | |ε| > 1 at the monopoly optimum |

| μ | Markup factor, P/MC | 1 to ∞ |

| si | Firm i‘s market share | 0 to 1 |

| HHI | Herfindahl-Hirschman Index, Σ si2 | 0 to 1 |

|

||

Key Assumptions and Limitations

The Lerner index rests on a clean theoretical foundation, but its assumptions are restrictive. Three matter most.

First, the formula assumes the firm prices to maximise short-run profit on a single homogeneous product. Multi-product firms, firms with binding capacity constraints, firms pursuing market share over current profit, and firms operating under regulation all violate this premise. An IMF working paper from 2021 showed that the conventional Lerner index for advanced-economy banks rose sharply after the global financial crisis, but this was largely an artefact of falling policy rates rather than a genuine increase in pricing power. When interest rates collapsed, banks’ marginal funding costs fell faster than their loan rates, mechanically inflating the index.

Second, marginal cost is rarely observable. Accounting systems track average variable cost, total cost, or fully absorbed unit cost, none of which equals \( MC \) at the profit-maximising output. Empirical studies infer marginal cost from estimated cost functions, production functions, or the first-order conditions of an assumed pricing model. A 2017 paper in the Journal of Banking & Finance argued that in industries with significant economies of scale, a positive Lerner index can simply reflect the firm’s need to cover fixed costs and earn non-negative profit, not market power. The authors proposed a scale-corrected Lerner index that subtracts the contribution of returns to scale.

Third, the inverse-elasticity rule applies to the firm’s own-product elasticity, which depends on consumer substitution patterns and competitor responses. In differentiated-product markets, demand elasticities must be estimated from a discrete-choice or random-utility model. The estimation choices materially affect the result. Stochastic-frontier estimates of the bank Lerner index show coefficient-of-variation values five times smaller than conventional estimates, indicating that the standard method introduces large measurement error.

Other limitations include the index’s silence on dynamic competition, innovation, and entry threats. A firm facing a high Bain-style entry barrier may price below the static profit-maximising level to deter entrants, producing a low Lerner index even though it holds substantial latent power. Conversely, a firm with a high index may simply be enjoying a temporary innovation rent that competition will erode. The index is a snapshot, not a structural assessment.

Empirical Evidence for the Lerner Index

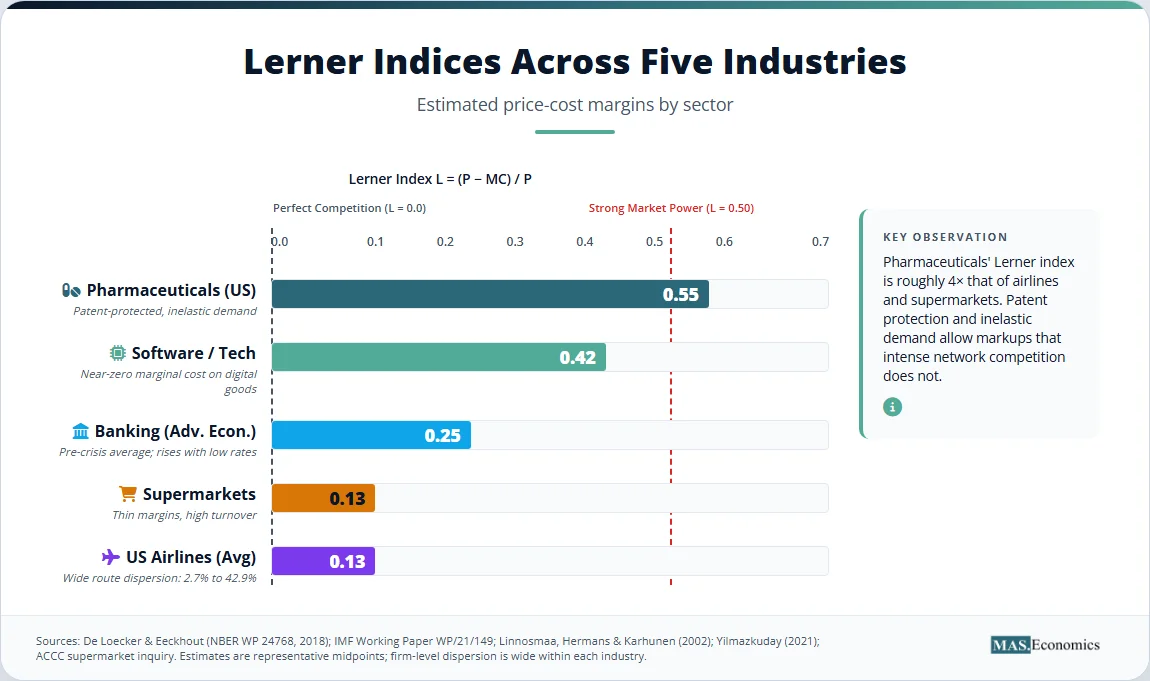

Cross-industry estimates of the Lerner index reveal a wide spread. Pharmaceuticals consistently rank near the top. A study of US and Finnish pharmaceutical firms estimated Lerner indices in the 0.43 to 0.58 range, depending on whether R&D inputs are included in the cost base. The high values reflect patent protection, inelastic demand for prescription drugs, and substantial fixed R&D outlays per successful molecule. Banking shows a different pattern. An estimate covering 148 countries from 1997 to 2010 found that bank Lerner indices typically lie between 0.20 and 0.30, with sub-Saharan Africa and low-income countries showing the highest values and OECD economies the lowest. The US airline industry sits lower still. Route-level estimates using the Lerner markup rule in a structural VAR model find an average annual profit margin of 13.3 percent across US domestic routes, with route-level dispersion ranging from 2.7 percent to 42.9 percent.

The most influential aggregate estimate is the De Loecker-Eeckhout series. Using financial statements from over 70,000 firms across 134 countries, they document a rise in the average global markup factor from close to 1.1 in 1980 to around 1.6 in 2016, with North America and Europe showing the largest increases. The implied Lerner index at the global mean has roughly tripled, from about 0.09 to 0.37. The increase is concentrated at the top of the firm distribution: the median firm has seen a much smaller change, while the 90th-percentile markup has expanded sharply. This reallocation of profits towards a few high-markup firms has become the central empirical fact in the rising-market-power literature.

The figure below summarises representative Lerner index estimates across five major industries.

Figure 1. Estimated Lerner indices, selected industries. Sources: De Loecker and Eeckhout (NBER 2018); Diez, Leigh and Tambunlertchai (IMF 2018); Linnosmaa et al. (pharmaceuticals); Anginer et al. (banking, IMF datasets); Yilmazkuday (US airlines).

Two patterns deserve attention. The cross-industry spread is large, with pharmaceuticals registering values four times those of airlines. And within each industry, dispersion across firms is also wide. De Loecker and Eeckhout’s firm-level data show that the rise in aggregate markups since 1980 is driven by the upper tail of the distribution rather than a uniform shift. The Lerner index is therefore most informative when reported as a distribution, not a single average.

How the Lerner Index Matters

The Lerner index drives concrete decisions in three policy domains: antitrust enforcement, financial supervision, and macroeconomic analysis.

In antitrust, the US Department of Justice and the Federal Trade Commission rely on price-cost margin evidence – effectively, Lerner-index-style calculations – to assess unilateral effects in merger reviews. The 2023 Merger Guidelines explicitly identify markups above competitive levels as a primary diagnostic for market power. When two firms producing close substitutes propose to merge, regulators estimate the diversion ratio between their products and combine it with each firm’s pre-merger Lerner index to compute the upward pricing pressure. The same logic applies in cartel and collusion cases: a sustained Lerner index well above industry historical norms is treated as circumstantial evidence of coordination. The European Commission applies similar reasoning under Article 102 abuse-of-dominance investigations, where price-cost tests determine whether a dominant firm has engaged in margin squeeze or predatory pricing.

Financial supervisors use the bank Lerner index as a competition diagnostic. The Bank of England’s Staff Working Paper No. 631 estimated Lerner indices for UK deposit-taking institutions and combined the results with Panzar-Rosse and Boone indicators to assess whether retail banking competition had weakened. The Federal Reserve, the European Central Bank, and the Bank of Canada all maintain internal series on bank-level markups for the same purpose. The IMF’s Financial Stability Reports use the index to compare cross-country banking competition and to evaluate whether post-crisis consolidation has reduced consumer welfare.

In macroeconomics, rising aggregate Lerner indices have become central to the debate over slowing wage growth and falling labour shares in advanced economies. The IMF working paper by Diez, Leigh, and Tambunlertchai linked rising markups to declines in the labour share, lower investment, and reduced business dynamism. The mechanism is intuitive: when firms charge a higher markup over marginal cost, a smaller share of revenue flows to the workers and suppliers who provide that marginal input. Productivity growth slows because high-markup incumbents face less pressure to innovate. The Bank of Canada has documented similar markup increases in Canadian non-financial industries since 2000, with the largest rises concentrated in services.

The index also informs sector-specific regulation. In the US pharmaceutical industry, where the Inflation Reduction Act of 2022 introduced negotiated drug prices for Medicare, the Centers for Medicare and Medicaid Services use markup analysis to identify drugs whose prices most exceed therapeutic-value benchmarks. In Australia, the Australian Competition and Consumer Commission has used Lerner-style margin analysis in its supermarket inquiries, finding price-cost margins consistent with a moderate level of market power despite the high concentration in the Coles-Woolworths duopoly. In the United Kingdom, the Competition and Markets Authority has deployed the same toolkit in its review of mobile telecoms and cloud services. The common thread is a recognition that structural measures like concentration ratios are necessary but not sufficient: the Lerner index provides the behavioural confirmation that concentration has translated into pricing power.

Beyond enforcement, the index shapes how firms design their own pricing. Companies with sophisticated revenue-management systems – airlines, hotels, software vendors, e-commerce platforms – set prices using estimated demand elasticities at the segment level, applying the inverse-elasticity rule directly. Reuters has reported on the spread of segment-level dynamic pricing in US aviation, and the technique has migrated into ride-sharing, ticketing, and consumer subscription services. Lerner’s 1934 framework has become the operating logic of platform pricing in the digital economy.

MASEconomics Explains

Three economic concepts behind the Lerner Index

Conclusion

The Lerner index remains the standard mathematical measure of market power because it converts the abstract concept of pricing power into a single, bounded number derived from a clear theoretical foundation. The formula \( L = (P – MC)/P \) ties directly to the inverse-elasticity rule, links naturally to the Herfindahl-Hirschman Index under Cournot competition, and translates into the markup factor used in modern macroeconomic research. Empirical estimates show wide cross-industry variation – from roughly 0.13 in US airlines to 0.55 in US pharmaceuticals – and a documented rise in average global markups from about 1.12 in 1980 to 1.59 in 2016. The index has known limitations around marginal cost measurement, scale economies, and dynamic competition, but it continues to anchor antitrust merger review, banking supervision, and the macroeconomic analysis of competition and labour shares.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.