In March 1994, the United States Federal Communications Commission auctioned off 10 nationwide narrowband licenses for personal communications services. The auction raised $617 million, ten times the Treasury’s initial estimate. The rules of that auction did not exist a year earlier. Two Stanford economists, Paul Milgrom and Robert Wilson, had built them from scratch, working backwards from a single question: what bidding rules would force telecom firms to reveal what spectrum was actually worth to them, and put it in the hands of those who valued it most? Mechanism design economics is the field that answers questions like this. It is the engineering arm of microeconomics, and it now shapes everything from kidney transplant queues to the ad auctions that fund Google.

The Vickrey-Clarke-Groves family of auctions, the Gale-Shapley deferred acceptance algorithm, and the Myerson optimal auction are not abstract curiosities. They run school admissions in New York, organ exchanges across hospital networks, and the real-time bidding systems behind every search result. Two Nobel Prizes, in 2007 and 2012, recognised the economists who built this toolkit. The questions they answered were practical: how do you design rules so that self-interested agents, holding information you cannot see, end up producing outcomes that are efficient, fair, and stable?

What Mechanism Design Does

Classical game theory takes the rules of a game as given and predicts how rational players will behave. Mechanism design flips this around. Start with the outcome a planner wants. Work backwards to find rules that, when self-interested agents play strategically, produce that outcome anyway.

Leonid Hurwicz, who shared the 2007 Nobel Prize with Eric Maskin and Roger Myerson, called this the theory of “institutions as games”. The planner is the rule writer. Agents are the players. The mechanism is the institution: an auction format, a voting procedure, a matching algorithm, a tax schedule. The challenge is that the planner does not know what the agents know. Bidders know their private valuations. Doctors know their patients’ medical histories. Students know their school preferences. The planner sees only what agents choose to reveal.

Four concepts anchor the field. A social choice function maps the private information of agents into a collective outcome. Incentive compatibility requires that truth-telling be a best response for every agent. Individual rationality means no agent does worse by participating than by walking away. The revelation principle, formalised by Myerson in 1979, ties these together. It states that any outcome implementable by any mechanism can also be implemented by a direct revelation mechanism in which agents are simply asked to report their types truthfully, and truth-telling is a Bayesian-Nash equilibrium. The principle is a remarkable simplification. It tells the designer to search only over direct truthful mechanisms without losing anything, because every indirect mechanism has a truthful counterpart producing the same outcomes.

The shift from “given the rules, what happens?” to “given the desired outcome, what rules?” changed economics. It moved theory from describing equilibrium to engineering it.

The Vickrey Auction Mechanics

The cleanest illustration is the allocation of one indivisible good among \( n \) bidders. Each bidder \( i \) has a private valuation \( v_i \) drawn independently from some distribution \( F \). The seller does not know \( v_i \). The goal is to allocate the good to the bidder who values it most, while inducing truthful reporting.

Consider three formats. In a first-price sealed-bid auction, the highest bidder wins and pays their bid. Bidders shade down: they bid below \( v_i \) to leave themselves a profit margin. Truth-telling fails. In an English open-outcry auction, bidders raise the price until only one remains. The winner pays roughly the second-highest valuation, but the format is procedurally complex.

William Vickrey’s 1961 insight was the second-price sealed-bid auction. Each bidder submits a bid \( b_i \). The highest bidder wins, but pays the second-highest bid. Let \( b_{(1)} \) and \( b_{(2)} \) denote the highest and second-highest bids. The winner’s payoff is:

Truth-telling, \( b_i = v_i \), is a weakly dominant strategy. The argument is direct. Suppose bidder \( i \) considers reporting \( b_i \neq v_i \). If \( b_i > v_i \), bidder \( i \) wins more often, but in the new winning cases the second-highest bid exceeds \( v_i \), producing negative payoff. If \( b_i < v_i \), bidder \( i \) loses some auctions they would have profitably won. In every state of the world, reporting \( v_i \) does at least as well as any other bid. The auction is incentive compatible in dominant strategies, the strongest solution concept available.

The Vickrey auction also achieves allocative efficiency: the good goes to the bidder with the highest \( v_i \). Roger Myerson generalised this in his 1981 paper “Optimal Auction Design”, showing that with regularity conditions on the value distribution, a modified second-price auction with an optimal reserve price maximises the seller’s expected revenue. The Myerson auction is, in a precise sense, the revenue-optimal mechanism for selling a single good.

The notation matters because it generalises. The same logic, with payments equal to the externality each agent imposes on others, gives the Vickrey-Clarke-Groves (VCG) mechanism for allocating multiple goods or public projects.

| Symbol | Meaning |

|---|---|

| \( n \) | Number of bidders or agents |

| \( v_i \) | Private valuation of agent \( i \) |

| \( b_i \) | Bid (reported valuation) of agent \( i \) |

| \( b_{(1)}, b_{(2)} \) | Highest and second-highest bids |

| \( u_i \) | Payoff to agent \( i \) |

| \( F \) | Distribution from which valuations are drawn |

| \( \theta_i \) | Type (private information) of agent \( i \) |

| \( s_i^* \) | Equilibrium strategy of agent \( i \) |

| |

Table 1. Notation: Symbols Used in Mechanism Design

What the Theory Takes for Granted

The elegance of the Vickrey result rests on assumptions that often break in practice. The first is private values. Each bidder’s valuation \( v_i \) depends only on their own information, not on what others know. In oil-lease auctions or art auctions, valuations are interdependent: what a competitor knows about the field affects what the asset is worth. Under interdependent values, truthful bidding in a second-price auction can lead to the winner’s curse, in which winning systematically signals overpayment. Milgrom and Wilson’s 1982 work extended auction theory to this case, but the simple dominant-strategy result no longer holds.

The second is quasi-linear utility. Agents’ payoffs are assumed to take the form \( u_i = v_i – p_i \), separable in valuation and payment. This rules out wealth effects. A bidder with $1 million treats winning a $500,000 asset the same, whether their net worth is $2 million or $50 million. In high-stakes settings, this is a real distortion.

Risk neutrality is a third assumption. The revenue equivalence theorem, which says first-price and second-price auctions yield the same expected revenue under standard conditions, fails when bidders are risk-averse. Risk-averse bidders bid more aggressively in first-price auctions, raising seller revenue.

The most binding limitation is collusion. Mechanism design typically assumes agents play independently. In repeated auctions, bidders can signal through bid patterns, suppress competition, and split the surplus. The 1990s German GSM spectrum auction was reportedly compromised by exactly such signalling, with bidders using the trailing digits of their bids to communicate preferred allocations. Once collusion enters, the planner’s problem becomes designing a mechanism robust to coalitions, not just individual deviations.

Computational complexity is a separate constraint. The VCG mechanism for combinatorial auctions, where bidders bid on bundles of goods, requires solving an NP-hard winner-determination problem. Theoretical optimality is unhelpful if the rules cannot be run in real time. The FCC’s combinatorial clock auction, used since 2008, is a compromise: not theoretically optimal, but tractable and reasonably truth-revealing.

Mechanism Design in the Wild

The empirical record is strong where the theory has been adapted, and weaker where it has been imposed without modification. Three case studies illustrate the range.

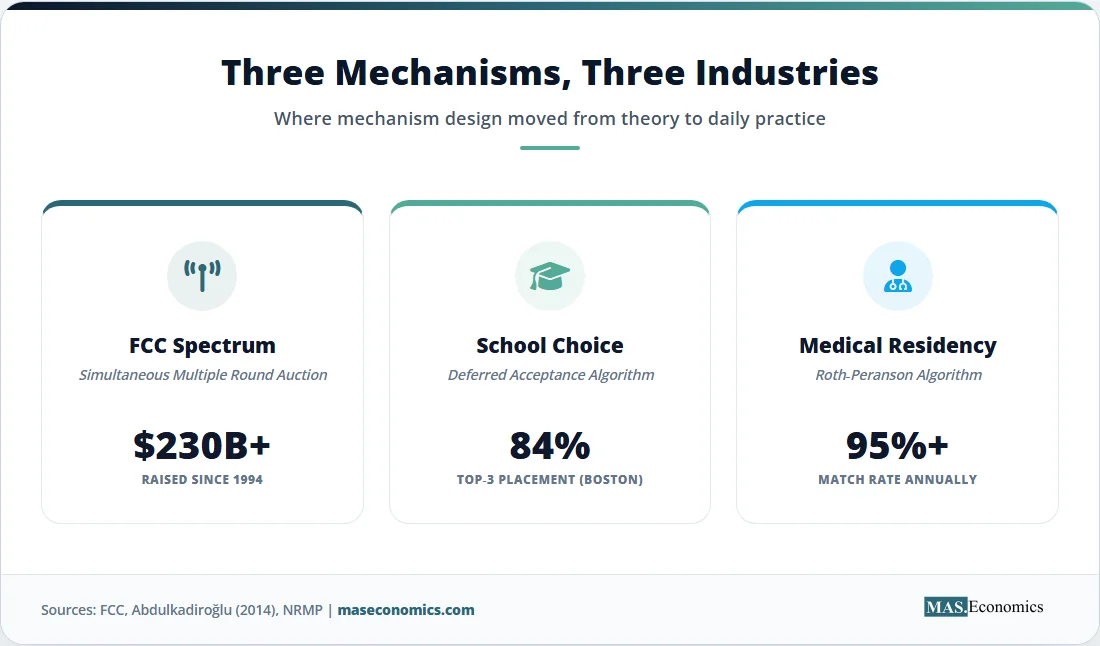

The FCC spectrum auctions are the most-studied application. Between 1994 and 2024, FCC auctions raised more than $230 billion for the U.S. Treasury and reallocated spectrum from broadcasters to wireless carriers. The original simultaneous multiple-round (SMR) auction, designed by Milgrom, Wilson, and Preston McAfee, allowed bidders to learn about competitors’ valuations across rounds while bidding on multiple licenses simultaneously. The 2017 incentive auction, which paid television broadcasters to vacate spectrum and resold it to wireless carriers, used a forward and reverse auction in tandem and raised $19.8 billion. Milgrom and Wilson received the 2020 Nobel Prize in part for this work.

School choice is the second domain. Boston Public Schools used a “first preference first” mechanism for decades. Parents who ranked an oversubscribed school first got priority. The result was that parents had to game their submitted preferences, often hiding their true first choice to protect their second. Atila Abdulkadiroğlu, Parag Pathak, and Alvin Roth showed in 2003 that the deferred acceptance algorithm, originally proposed by David Gale and Lloyd Shapley in 1962, was both stable and strategy-proof for students. Boston switched in 2005. New York City had already switched its high school assignment system in 2003. Stanford economist Roth’s work on this is documented in NBER Working Paper 11965.

The third example is the National Resident Matching Program (NRMP). Since 1952, U.S. medical school graduates have been matched to residency programs through a centralised algorithm. The original algorithm was hospital-proposing, which advantaged hospitals. In 1995, Roth and Elliott Peranson redesigned the system to use a student-proposing variant of deferred acceptance, accommodating couples who wanted to match together. The new algorithm has been used since 1998. Each year, more than 40,000 applicants are matched. Match rates exceed 95%.

Empirical comparisons of auction formats show that revenue and efficiency depend heavily on the mechanism chosen. The chart below summarises results from a 2017 study by Lawrence Ausubel and Oleg Baranov on combinatorial spectrum auctions, comparing average efficiency across formats in laboratory experiments calibrated to FCC environments.

Source: Adapted from Ausubel and Baranov (2017), “A Practical Guide to the Combinatorial Clock Auction.” Efficiency measures the share of total possible surplus realised across simulated auctions.

The combinatorial clock auction reaches roughly 94% of the theoretical efficient surplus, against 88% for the simpler simultaneous multiple round format. Sealed-bid pay-as-bid auctions perform worst, around 79%, because bidders shade their bids substantially when they cannot observe rivals. The pattern in laboratory data tracks the theoretical predictions of Nash equilibrium analysis applied to each format.

School choice data tells a similar story. After Boston switched from the priority-based system to deferred acceptance in 2005, the share of students assigned to one of their top three choices rose from 76% to 84%, according to a 2014 evaluation by Abdulkadiroğlu, Pathak, and Roth published in American Economic Review. Strategic ranking, where parents misrepresent preferences, dropped sharply.

From Spectrum to Search Engines

Mechanism design moved from academic curiosity to industrial infrastructure between 1995 and 2010. The most consequential application is internet advertising. Google’s AdWords auction, launched in 2002, uses a generalised second-price (GSP) auction. Each time a search query produces ad slots, advertisers bid on keywords, and slots are allocated by bid amount weighted by predicted click-through rate. The winner of the top slot pays slightly more than the second bidder’s effective bid.

GSP is not strictly truth-revealing in the Vickrey sense, but Hal Varian and Benjamin Edelman showed in 2007 that it has stable equilibria with intuitive properties. Google generates more than $200 billion annually from ad auctions. Meta uses a similar system. The mechanism is the business. Mechanism design is the engineering of platform economics.

Ride-sharing surge pricing applies the logic to real-time markets. When demand spikes, Uber and Lyft raise prices algorithmically. The price increase serves two purposes: rationing demand among riders and pulling additional drivers onto the road. The pricing rule is a posted-price mechanism, simpler than an auction but designed to clear the market efficiently when private information about driver availability and rider urgency is held by the platform.

Carbon emissions trading is another application. The European Union Emissions Trading System, launched in 2005, allocates emission permits through an auction format. Permits are auctioned quarterly, and firms trade them on a secondary market. The mechanism design challenge is to set the cap stringently enough to drive abatement, while preventing collusion among the largest emitters. The EU ETS now covers 40% of EU greenhouse gas emissions.

Kidney exchange is the most morally weighted application. Patients in need of a transplant often have willing donors who are biologically incompatible. Roth, Tayfun Sönmez, and M. Utku Ünver designed an exchange algorithm, deployed by the New England Program for Kidney Exchange in 2004 and now used by the United Network for Organ Sharing. The system runs cyclic exchanges and chains starting from non-directed donors. By 2023, kidney exchange had enabled more than 10,000 transplants in the United States that would otherwise not have happened.

Two Nobel Prizes anchor the field’s recognition. The 2007 prize went to Hurwicz, Maskin, and Myerson for laying the foundations of mechanism design theory. The 2012 prize went to Roth and Shapley for the theory of stable allocations and the practice of market design. The 2020 prize to Milgrom and Wilson recognised auction theory and the FCC redesign. Three prizes in fifteen years for one set of ideas is unusual. The field has earned them by producing institutions that work.

The connection to Arrow’s impossibility theorem is direct. Arrow showed in 1951 that no voting rule can satisfy a small set of reasonable axioms simultaneously. Mechanism design accepts this as a starting point and asks: given the trade-offs Arrow identified, what mechanisms perform best on the dimensions a society cares about most? The Gibbard-Satterthwaite theorem extends Arrow’s logic to mechanisms, showing that any non-dictatorial social choice function over more than two outcomes is manipulable. Designers respond by restricting domains, like the deferred acceptance algorithm working only over preference rankings, or by using money as a side payment, like VCG auctions.

The field’s reach now extends to digital platforms, environmental policy, and healthcare allocation. Whenever a planner faces self-interested agents holding private information, the mechanism design toolkit is the first place to look.

MASEconomics Explains

4 economic concepts behind mechanism design

Conclusion

Mechanism design economics turned theoretical microeconomics into applied institutional engineering. The Vickrey auction, the deferred acceptance algorithm, and the VCG mechanism demonstrate that rules can be built so that self-interested agents, holding private information, produce outcomes that are efficient, stable, and individually rational. The FCC has raised more than $230 billion through auctions designed using these principles. New York City and Boston use deferred acceptance to assign hundreds of thousands of students. The NRMP matches over 40,000 medical residents annually. Google’s ad auctions, the EU emissions trading system, and kidney exchange networks all rest on mechanism design foundations. Three Nobel Prizes between 2007 and 2020 recognised the architects of this work. The toolkit has limits: collusion, interdependent values, and computational complexity all break the cleanest results. The empirical record nonetheless shows that well-designed mechanisms outperform ad hoc rules by margins that translate into billions of dollars and tens of thousands of lives.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.