The Mundell trilemma proves that no country can simultaneously maintain a fixed exchange rate, free capital mobility, and an independent monetary policy; any open economy must give up one of the three. This constraint, also called the impossible trinity, is the key theorem of international macroeconomics. Robert Mundell’s work in the early 1960s on monetary and fiscal policy in open economies, alongside the parallel contribution by Marcus Fleming, established this framework. Their combined Mundell-Fleming model underlies all modern open-economy macroeconomic theory. Mundell received the 1999 Nobel Prize for his analysis of monetary and fiscal policy under different exchange rate regimes, cementing the trilemma’s place in the economic canon. Mundell’s 1963 Canadian Journal of Economics paper and Fleming’s 1962 IMF Staff Papers contribution remain the foundational texts.

What the Mundell Trilemma Means

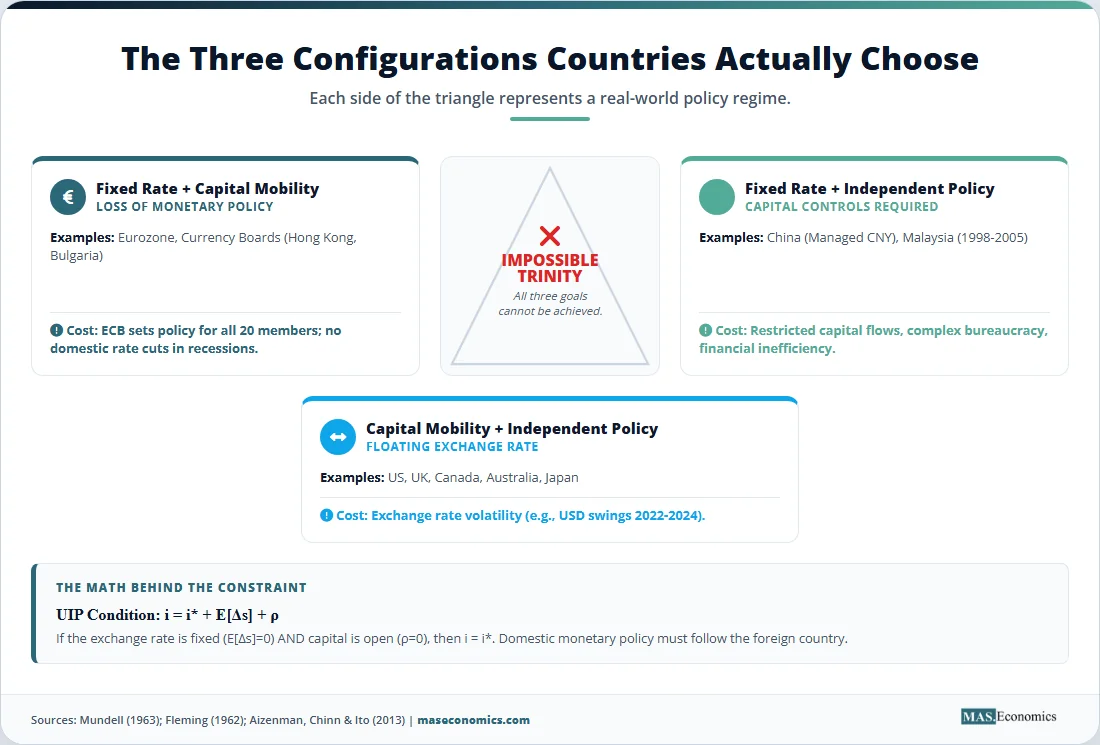

The Mundell trilemma presents a stark policy trade-off: a country choosing two of the three policy goals must abandon the third. The three vertices of the trilemma triangle are a fixed exchange rate, free capital mobility, and an independent monetary policy. A nation can choose any two, but financial arithmetic prevents achieving all three simultaneously.

A country that pegs its exchange rate and allows capital to flow freely across its borders surrenders control over its domestic interest rate. If the central bank attempts to set interest rates differently from the rest of the world, capital flows will immediately arbitrage the difference, forcing the exchange rate to adjust and breaking the peg. To maintain the fixed rate, the central bank must match the foreign interest rate, effectively importing its monetary policy from abroad.

Alternatively, a country that pegs its exchange rate and retains monetary independence must restrict capital flows. Without capital controls, interest rate differentials would trigger destabilising flows, but with capital controls, the domestic interest rate can diverge from the world rate without triggering an exodus of reserves. The third option is a country that allows free capital mobility and maintains an independent monetary policy, which requires letting the exchange rate float. The central bank sets interest rates according to domestic needs, and the exchange rate adjusts to equilibrate the balance of payments.

This logic is not just theoretical; it is a binding arithmetic identity derived from the conditions for international financial equilibrium. The trilemma explains why the Bretton Woods system of fixed exchange rates collapsed when capital mobility increased, why the Eurozone surrendered national monetary autonomy, and why China imposes capital controls to manage its currency. Every major international financial crisis of the past fifty years can be understood as a country attempting to violate the trilemma and being forced back into compliance by market pressures.

Mundell Trilemma in Equations

The mathematical logic of the trilemma rests on the uncovered interest parity (UIP) condition, the equilibrium relationship that constrains policy choices in open economies.

Uncovered Interest Parity

Under UIP, the domestic interest rate equals the foreign interest rate plus the expected rate of depreciation of the domestic currency, plus a risk premium:

where \( i_t \) is the domestic nominal interest rate, \( i_t^* \) is the foreign nominal interest rate, \( s_t \) is the log nominal exchange rate (domestic currency per foreign currency), and \( \rho_t \) is a time-varying risk premium that reflects transaction costs, default risk, or capital controls. The term \( E_t[\Delta s_{t+1}] \) is the expected change in the exchange rate.

Trilemma Logic from UIP

The trilemma emerges directly from this equation. If a country commits to a fixed exchange rate, the expected depreciation is zero: \( E_t[\Delta s_{t+1}] = 0 \). If capital is perfectly mobile, the risk premium vanishes: \( \rho_t \to 0 \). Substituting these conditions into the UIP equation forces the domestic interest rate to equal the foreign rate: \( i_t = i_t^* \). Domestic monetary policy has no autonomy; it must shadow the foreign central bank.

If the country attempts to set \( i_t \neq i_t^* \) while maintaining the peg and open capital markets, UIP is violated. Capital will flow to the higher-yielding jurisdiction, creating immense pressure on the exchange rate. The central bank must either abandon the peg, impose capital controls to restore \( \rho_t > 0 \), or surrender monetary autonomy by aligning \( i_t \) with \( i_t^* \).

Measuring the Trilemma: Aizenman-Chinn-Ito Indices

Aizenman, Chinn, and Ito (2008) developed quantitative indices to measure the three policy dimensions empirically. Their framework operationalises the trilemma for cross-country analysis.

Monetary Independence (MI): Measured as the inverse of the correlation between domestic and foreign interest rates:

When the correlation is 1, MI equals 0, indicating no monetary independence.

Exchange Rate Stability (ERS): Measured by the inverse of exchange rate volatility:

When exchange rate volatility is zero (a pure peg), ERS equals 1.

Financial Openness (KAOPEN): Constructed from binary IMF AREAER variables on capital-account restrictions, standardised to the [0, 1] interval.

The Trilemma Constraint: Aizenman, Chinn, and Ito (2013) tested whether the sum of the three indices is constant across countries and over time:

Their empirical analysis confirms that the trilemma is binding. An increase in one dimension is systematically offset by a decrease in another.

Mundell-Fleming IS-LM-BP Framework

The trilemma’s policy implications are most clearly seen in the Mundell-Fleming extension of the IS-LM framework. The model adds a Balance of Payments (BP) curve to the standard IS and LM curves. Under a fixed exchange rate and perfect capital mobility, the BP curve is horizontal at \( i = i^* \). Any attempt by the central bank to shift the LM curve through monetary expansion is immediately offset by capital outflows, which reduce the money supply and push the LM curve back to its original position. Monetary policy is completely impotent.

The mechanism operates step-by-step. When the central bank buys domestic bonds to increase the money supply, the LM curve shifts right, pushing the domestic interest rate below \( i^* \). Investors immediately sell domestic assets and buy foreign assets to earn the higher foreign rate. This capital outflow forces the central bank to sell foreign reserves and buy domestic currency to defend the peg. The sale of foreign reserves reduces the domestic money supply, shifting the LM curve back left until the interest rate returns to \( i^* \). Output returns to its original level. The central bank has merely swapped interest-bearing domestic bonds for non-interest-bearing foreign reserves, with no lasting effect on the real economy.

Under a floating exchange rate, the outcome reverses. When the central bank expands the money supply, the LM curve shifts right, pushing the domestic interest rate below \( i^* \). Capital flows out, but instead of intervening, the central bank allows the currency to depreciate. Depreciation makes domestic goods cheaper on world markets, boosting exports and reducing imports. The IS curve shifts right until the domestic interest rate returns to \( i^* \). Output increases. Monetary policy is highly effective because the exchange rate movement reinforces the initial stimulus.

Key Assumptions and Limitations

The Mundell trilemma relies on several key assumptions. First, UIP holds, meaning that risk premia are either absent or unchanging. Second, capital can genuinely flow freely across borders if KAOPEN equals 1. Third, policymakers face relatively binary choices on each axis.

Several important limitations challenge these assumptions. First, Hélène Rey’s “Dilemma not Trilemma” argument, presented at the 2013 Jackson Hole symposium, asserts that the global financial cycle dominated by US monetary policy means even floating exchange rate regimes lose monetary independence. Rey’s evidence shows that capital flows and credit growth in emerging markets correlate strongly with the VIX index and US monetary conditions, regardless of the local exchange rate regime. If Rey is correct, the choice is not between two of three corners but between capital mobility and monetary autonomy, with the exchange rate regime being secondary.

Second, Aizenman has extended the framework to a quadrilemma by adding financial stability as a fourth policy goal. The global financial crisis showed that capital mobility and fixed exchange rates can import financial instability, requiring macroprudential tools that effectively act as a new constraint on the system. This extension recognises that sound banking systems are a distinct policy objective that cannot be subsumed within the traditional three-way trade-off.

Third, corner solutions are rare in practice. Most countries adopt intermediate regimes: managed floats, partial capital controls, or soft pegs. Klein and Shambaugh (2015) showed that partial capital controls still bind in proportion, meaning the trilemma operates on a continuum rather than as a strict binary, but the key constraint remains. Even soft controls create enough friction to allow some monetary divergence, though not full independence.

Fourth, a sterilised intervention can temporarily relax the constraint. A central bank can buy foreign currency to prevent appreciation while selling domestic bonds to mop up the resulting liquidity, maintaining monetary control while defending the peg. However, sterilisation is costly because the central bank earns low returns on foreign reserves while paying higher interest on domestic bonds. This quasi-fiscal loss limits how long sterilisation can persist before reserve accumulation becomes unsustainable.

Empirical Evidence for the Trilemma

The empirical validity of the Mundell trilemma is well established across different historical periods and institutional arrangements. Obstfeld, Shambaugh, and Taylor (2005) provided comprehensive historical tests across the gold standard, Bretton Woods, and post-1973 floating era. Their analysis confirms that the trilemma is binding: interest rate correlations are highest under fixed exchange rates with open capital markets, confirming the loss of monetary autonomy.

Specific historical episodes provide stark demonstrations. The 1992 ERM crisis forced the United Kingdom off the European Exchange Rate Mechanism on Black Wednesday. The Bank of England attempted to maintain the pound’s parity against the Deutsche Mark while keeping capital markets open. When the Bundesbank raised interest rates to manage German reunification inflation, the UK was forced to follow suit despite being in recession. The resulting domestic pain was unsustainable, and speculators, most notably George Soros, bet against the pound. The Bank of England lost billions in reserves in a single day before abandoning the peg. The UK chose floating rates and monetary independence thereafter.

The 1997 Asian financial crisis devastated Thailand, Indonesia, and South Korea. These economies had maintained de facto dollar pegs while liberalising capital accounts. When export growth slowed and current account deficits widened, speculators attacked the pegs. Without sufficient reserves and with capital fleeing, the central banks could not defend the fixed rates. The resulting currency collapses caused widespread banking and corporate insolvencies because much of the private sector had borrowed in foreign currencies. The Asian crisis was a classic trilemma failure: countries attempted to maintain fixed rates and capital mobility while needing independent monetary easing, an impossible combination.

The 2015 Swiss franc unpeg showed the trilemma’s force even for advanced economies with deep financial markets. The Swiss National Bank (SNB) established a 1.20 floor against the euro in 2011 to combat deflationary pressures and safe-haven capital inflows. Defending this floor required the SNB to buy euros and sell francs, expanding its balance sheet to over 80 percent of Swiss GDP. When the European Central Bank signalled massive quantitative easing in January 2015, the SNB faced an untenable prospect of unlimited balance sheet expansion. Abandoning the peg caused the franc to appreciate 30 percent within minutes, illustrating the immense cost of maintaining the impossible trinity.

China’s policy mix represents a deliberate trilemma compromise. By maintaining partial capital controls and a managed exchange rate, the People’s Bank of China retains significant monetary autonomy. Beijing has slowly liberalised the capital account but retains tools to enforce the trilemma compromise when needed, intervening to manage the exchange rate while using administrative measures to control cross-border flows.

Klein and Shambaugh (2015) further refined the empirical understanding by examining partial capital controls. They found that even limited restrictions on cross-border flows provide some monetary policy autonomy, though less than complete closure. Countries with moderate capital controls can set interest rates partially independently, but their scope diverges proportionally to the degree of openness. Their findings confirm the trilemma operates on a gradient; partial controls yield partial autonomy, but the binding constraint remains intact.

The 2022–2024 Federal Reserve tightening cycle provided a real-time demonstration of the trilemma’s force for emerging markets. As the Fed raised rates aggressively to combat inflation, emerging markets with high financial openness faced a stark choice: raise domestic rates to prevent capital outflows, or cut rates to support domestic growth and accept currency depreciation. Brazil’s Banco Central do Brasil raised its Selic rate to 13.75 percent despite domestic recessionary pressures, explicitly to prevent capital flight and stabilise the real. Indonesia’s Bank Indonesia also raised rates, even though the domestic economy was still recovering from the pandemic, because allowing the rupiah to depreciate would have inflated the cost of food and energy imports. Both cases showed that floating regimes do not guarantee full monetary autonomy when global financial conditions tighten, supporting Rey’s dilemma argument that the global financial cycle constrains even floating regimes.

Sources: Aizenman, Chinn and Ito (2008, 2013); updated trilemma index database.

| Country / Region | Fixed Rate? | Capital Mobile? | Mon. Indep.? | What Is Sacrificed | Period |

|---|---|---|---|---|---|

| United States | No (Float) | Yes (Open) | Yes | Fixed exchange rate | 1973–present |

| Eurozone members | Yes (Euro) | Yes (Open) | No (ECB) | National monetary autonomy | 1999–present |

| China | Yes (Managed) | No (Restricted) | Yes | Capital mobility | 1994–present |

| Hong Kong | Yes (Board) | Yes (Open) | No (US rate) | Monetary independence | 1983–present |

| Switzerland (1.20 floor) | Yes (Floor) | Yes (Open) | No (ECB tied) | Monetary autonomy | 2011–2015 |

| United Kingdom | No (Float) | Yes (Open) | Yes | Fixed exchange rate | 1992–present |

| Argentina (Board) | Yes (1:1 USD) | Yes (Open) | No (US rate) | Monetary autonomy | 1991–2002 |

|

|||||

How the Trilemma Matters

The Mundell trilemma is more than an academic theorem; it is the organising framework for understanding the international monetary system. Its logic explains the rise and fall of exchange rate regimes, the architecture of the Eurozone, and the policy dilemmas facing emerging markets today.

The collapse of the Bretton Woods system between 1971 and 1973 was a direct consequence of the trilemma. Under Bretton Woods, countries maintained fixed exchange rates to the US dollar, which was convertible to gold. Capital mobility was restricted, preserving some monetary autonomy. As European and Japanese economies recovered and capital controls eroded, the system became untenable. The United States faced a choice between maintaining the gold peg and pursuing domestic monetary expansion to finance the Vietnam War and Great Society programmes. President Nixon closed the gold window in August 1971, choosing monetary autonomy and capital mobility over the fixed exchange rate. The international monetary system transitioned to floating rates, exactly as the trilemma predicted.

The Eurozone’s construction represents the most deliberate application of the trilemma in history. By adopting the euro, member states explicitly chose a fixed exchange rate and free capital mobility, permanently surrendering national monetary autonomy to the European Central Bank. For core countries like Germany and France, this trade-off was manageable. For peripheral countries like Greece, Portugal, and Spain, the loss of monetary independence proved catastrophic during the 2010–2015 sovereign debt crisis. These countries could not devalue their currencies to regain competitiveness, nor could they cut interest rates to stimulate demand. The Eurozone crisis was the inevitable cost of the fixed-rate, open-capital corner of the trilemma.

Currency board regimes like Hong Kong and Bulgaria explicitly embrace this same corner. They maintain fixed exchange rates and open capital accounts, accepting that their monetary policy is determined by the anchor currency’s central bank. Hong Kong’s interest rates follow the Federal Reserve’s decisions, regardless of local economic conditions. This arrangement provides credibility and stability but removes the ability to respond to domestic shocks.

China’s hybrid model occupies the opposite corner of the triangle. By restricting capital mobility, China maintains a managed exchange rate and independent monetary policy. The People’s Bank of China sets interest rates based on domestic conditions and intervenes heavily in foreign exchange markets to manage the yuan’s value. Beijing has slowly liberalised the capital account but retains tools to enforce the trilemma compromise when needed. The Chinese experience shows that the capital-controls corner of the trilemma is viable but requires extensive administrative capacity and comes at the cost of financial efficiency.

Modern emerging-market crises are routinely analysed through the trilemma lens. IMF surveillance and Article IV consultations frame country positions explicitly using this framework. Pakistan’s 2022–2023 economic crisis is a textbook case of trilemma violation. The State Bank of Pakistan attempted to maintain a managed exchange rate while foreign reserves dwindled to below $4 billion, barely covering one month of imports. Capital controls were partially in place, but extensive trade financing and informal channels kept effective capital mobility high. When reserves ran out, the central bank was forced into a chaotic depreciation, and the government had to impose strict capital controls and seek an IMF bailout. The crisis showed that maintaining a peg with limited reserves and incomplete capital controls is an unstable trilemma compromise that eventually collapses under market pressure.

Argentina’s repeated crises follow a similar pattern. The 1991–2002 currency board explicitly chose the fixed-rate, open-capital corner, sacrificing monetary autonomy entirely. When the Brazilian devaluation and low commodity prices made the peg overvalued, Argentina could not devalue or cut interest rates. The resulting depression, with unemployment exceeding 20 percent, forced the abandonment of the peg in 2002. Subsequent governments attempted intermediate regimes but repeatedly ran out of reserves defending managed rates while capital fled. Argentina’s experience confirms that the trilemma’s constraint cannot be negotiated away through partial measures.

Looking forward, central bank digital currencies (CBDCs) could reshape the capital mobility axis of the trilemma. Programmable digital currencies could allow governments to impose granular, real-time capital controls, altering the degree of financial openness with unprecedented precision. Aizenman has speculated that this technological shift could make the capital-controls corner of the trilemma easier to maintain. Currently, capital controls are blunt administrative instruments that are difficult to enforce and easy to evade through offshore financial centres. CBDCs could change this by embedding regulatory conditions directly into the currency. Smart contracts could automatically block or tax cross-border transfers above certain thresholds, dynamically lowering the KAOPEN index during periods of financial stress without requiring formal institutional changes. This would allow central banks to fluctuate between corners of the trilemma as conditions warrant, automating the capital control process and making the “impossible trinity” more of a policy dial than a hard structural switch.

Post-Brexit Britain illustrates the open trilemma choice. The UK has full monetary independence, free capital mobility, and a floating exchange rate. The cost is borne entirely through sterling volatility. The pound depreciated sharply after the 2016 referendum and again during the 2022 mini-budget crisis. This volatility is the price of maintaining the other two goals.

MASEconomics Explains

4 economic concepts behind the Mundell trilemma

Conclusion

Mundell trilemma theory establishes a binding logical and empirical constraint on open-economy policymaking, proving that no country can simultaneously maintain a fixed exchange rate, free capital mobility, and an independent monetary policy. Nations from Greece to China to Switzerland have shown the trilemma’s force through crisis and deliberate policy design. Modern critiques, including Rey’s global financial cycle dilemma and Aizenman’s quadrilemma extension, refine the framework by emphasising the power of global financial conditions and the distinct goal of financial stability, but they do not overturn the key trade-off. The trilemma remains the essential lens through which IMF surveillance, central bank decision-making, and international macroeconomic analysis are conducted.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.