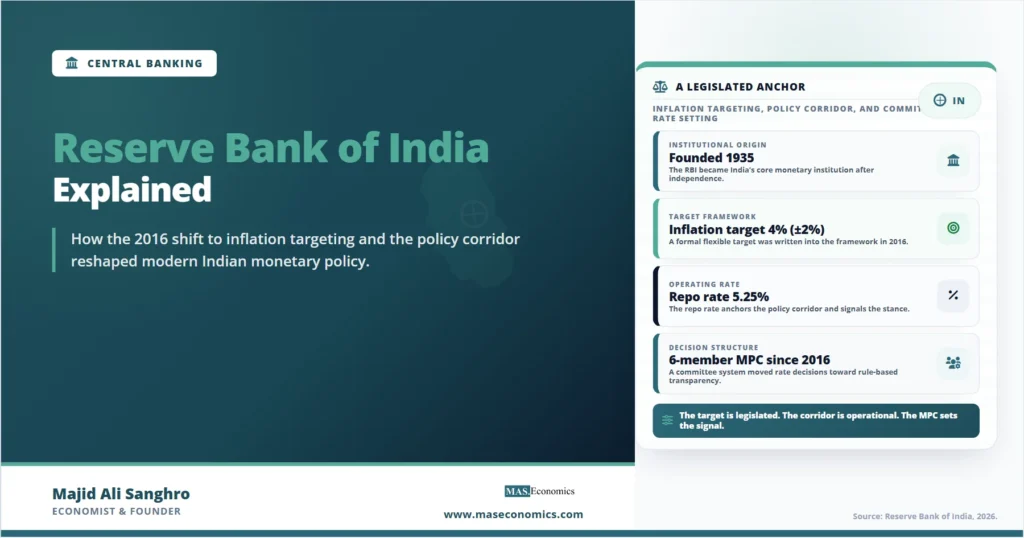

In 2016, the way India runs its monetary policy changed fundamentally. For eight decades, the Reserve Bank of India had pursued a shifting mix of goals: growth, the exchange rate, credit for priority sectors, and price stability, with the governor balancing them largely at his own discretion. Then Parliament amended the law to give the bank a single, legislated anchor: keep consumer price inflation at 4%, within a band of 2 to 6%, and decide rates through a formal committee rather than by the governor alone. Nearly a decade later, in early 2026, that framework was renewed for another five years, and the bank’s six-member committee was setting the repo rate at 5.25% with inflation comfortably near target. India had become, in the modern sense, an inflation-targeting central bank.

The Reserve Bank of India is the central bank of the world’s most populous country and one of its fastest-growing major economies. Established in 1935, it issues the rupee, sets the policy rate, regulates the banking system, manages the exchange rate and the nation’s foreign reserves, and acts as banker to the government. What makes it distinctive is the breadth of role it has historically played. Where many central banks confine themselves to monetary policy, the Reserve Bank of India has long been a developmental institution as well, charged with building banking access, financing priority sectors, and supporting the growth of a developing economy. The 2016 reform narrowed its formal monetary mandate to inflation, but the wider developmental inheritance still shapes the institution.

Central Bank Born Before Independence

The Reserve Bank of India predates the Republic it serves. Its origins lie in the Royal Commission on Indian Currency and Finance of 1926, known as the Hilton Young Commission, which recommended creating a central bank to separate control of currency and credit from the colonial government and to extend banking across the country. The recommendation became the Reserve Bank of India Act of 1934, and the bank commenced operations on April 1, 1935, with its central office initially in Calcutta before moving permanently to Mumbai in 1937.

The bank began life as a privately owned institution, with shares held largely by the Indian business community under government oversight. That changed soon after independence. Under the Reserve Bank (Transfer to Public Ownership) Act, the institution was nationalized on January 1, 1949, transferring full ownership to the Government of India, where it has remained since. The bank thus carries a dual character that still defines it: a government-owned institution that nonetheless exercises substantial operational autonomy over monetary policy, an arrangement that has occasionally produced tension between the bank and the government of the day.

The preamble to the 1934 Act, still in force, charged the bank with regulating the issue of banknotes and keeping reserves with a view to securing monetary stability and operating the currency and credit system to the country’s advantage. That last phrase, to the country’s advantage, is broad by design, and it is the legal root of the bank’s expansive developmental role. For much of its history, the Reserve Bank acted as a nation-builder as much as a monetary authority, directing credit toward agriculture and industry, building rural banking, and more recently helping construct the digital payments and financial-inclusion infrastructure that distinguishes India’s development model. The 2016 reform sharpened its monetary objective without erasing this wider inheritance.

2016 Shift to Inflation Targeting

The defining modern development in the institution is the adoption of flexible inflation targeting in 2016. Before then, the Reserve Bank pursued multiple objectives without a single, explicit, legislated priority among them, and the governor held considerable discretion over how to weigh growth against inflation. India had experienced episodes of high and volatile inflation, and a broad consensus emerged that a clear nominal anchor would improve credibility and outcomes, the logic set out in our explainer on inflation targeting.

The reform amended the Reserve Bank of India Act to put the framework on a statutory footing. Under Section 45ZA, the government, in consultation with the bank, sets a numerical inflation target every five years. That target was fixed at 4% consumer price inflation, with a tolerance band of two percentage points on either side, effectively a 2 to 6% range. The target was renewed unchanged for the period from April 2026 to March 2031, confirming the framework’s durability through a full decade of operation.

Two features of the Indian design are worth noting. The first is that the target is set by the government rather than by the bank alone, which gives it democratic legitimacy while leaving the bank independent in how it pursues the goal. The second is a formal accountability mechanism with real teeth: under Section 45ZN, if inflation stays outside the 2 to 6% band for three consecutive quarters, the bank is legally required to submit a report to the central government explaining why it failed, what it proposes to do, and how long it expects to take to return inflation to target. This is a more explicit failure clause than most inflation-targeting regimes contain, and it makes the bank’s accountability concrete rather than rhetorical.

Monetary Policy Committee Decisions

Alongside the inflation target, the 2016 reform created a statutory Monetary Policy Committee to set the policy rate, replacing a system in which the decision rested ultimately with the governor advised by an internal committee. This was a deliberate move toward shared, transparent decision-making, and it brought the bank closer to the practice of peer central banks.

The committee has six members. Three are from the Reserve Bank: the Governor, who chairs it, a Deputy Governor in charge of monetary policy, and a bank official. The other three are external members appointed by the central government, typically economists, brought in to provide independent judgment. Decisions are taken by majority vote, and in the event of a tie the Governor holds a casting vote, which preserves the bank’s ultimate authority while genuinely opening the decision to outside views. As of 2026, the Governor is Sanjay Malhotra. The committee meets bi-monthly, six times a year, and publishes both its decision and, after a delay, the minutes recording how each member voted and why, a level of transparency the old system did not provide.

Policy Corridor and Toolkit

The Reserve Bank’s primary instrument is the repo rate, the rate at which it lends short-term funds to commercial banks against government securities. But the repo rate does not operate alone. It sits at the centre of a policy corridor, bounded above and below by two other rates that together keep market interest rates in a controlled range.

The floor of the corridor is the Standing Deposit Facility rate, at which banks can park surplus funds with the Reserve Bank and earn interest. The ceiling is the Marginal Standing Facility rate, alongside the Bank Rate, at which banks can borrow emergency funds. The repo rate sits between them. By setting these three rates, the bank confines the overnight market rate to a narrow band around its policy rate. As of early 2026, the repo rate stood at 5.25%, with the deposit-facility floor at 5.00% and the marginal-facility ceiling at 5.50%, a corridor of half a percentage point. The diagram below shows how the corridor works.

Beyond the corridor, the bank uses two reserve requirements that are more prominent in India than in most advanced economies. The cash reserve ratio is the share of deposits banks must hold as cash with the Reserve Bank, recently at 3%, and changing it directly adds or drains liquidity from the banking system. The statutory liquidity ratio is the share of deposits banks must hold in safe, liquid assets such as government securities, recently at 18%. These quantity tools sit alongside the price tools, giving the bank levers over both the cost and the availability of credit. The full table of instruments is below.

| Tool | What It Does | Recent Level |

|---|---|---|

| Repo rate | The benchmark policy rate; the MPC’s main instrument | 5.25% |

| Standing Deposit Facility (SDF) | Corridor floor; rate banks earn on surplus parked at the RBI | 5.00% |

| Marginal Standing Facility / Bank Rate | Corridor ceiling; emergency borrowing rate | 5.50% |

| Cash Reserve Ratio (CRR) | Cash banks must hold at the RBI; a direct liquidity lever | 3.00% |

| Statutory Liquidity Ratio (SLR) | Liquid assets banks must hold against deposits | 18.00% |

| Open market operations | Buying or selling government securities to manage liquidity | As needed |

| Exchange-rate and reserve management | Managing the rupee’s float and the foreign reserves | Ongoing |

|

Source: Reserve Bank of India monetary policy documentation, early 2026.

|

||

One feature makes the transmission of policy unusually direct in India. New floating-rate loans to retail and small-business borrowers must be linked to an external benchmark, typically the repo rate itself. When the Monetary Policy Committee changes the repo rate, the cost of these loans moves almost mechanically with it, so a rate decision reaches household and small-business borrowing quickly, the broader process described in our explainer on the monetary transmission mechanism. The bank also manages the rupee under a managed float, intervening to smooth volatility rather than to defend a fixed level, the role of the exchange rate explored in our piece on exchange rates in global trade.

The recent rate cycle illustrates the framework in action. To combat the post-pandemic inflation surge, the bank raised the repo rate to 6.5% and held it there through a long pause, then, as inflation fell back toward target, began easing in 2025, cutting in steps to 5.25% by the end of that year and holding into 2026.

Pressures Ahead

Three challenges will shape the Reserve Bank’s work through the rest of the decade.

The first is managing inflation in an economy where food prices carry enormous weight. Food makes up a large share of India’s consumer price index, far more than in advanced economies, and food prices are driven heavily by the monsoon, by supply shocks, and by global commodity movements that monetary policy cannot influence. A poor harvest can push headline inflation outside the tolerance band for reasons that a rate rise does little to address, while still imposing a cost on growth. Keeping inflation expectations anchored through volatile food-price swings, without overreacting to shocks the bank cannot control, is the central operational difficulty of Indian monetary policy.

The second is the balance between its inflation mandate and its developmental inheritance. The 2016 reform gave the bank a clear, narrow monetary objective, but the institution retains its wider role in financial inclusion, banking regulation, and the development of the financial system, and it sits within a government that prioritizes rapid growth. Reconciling the discipline of an inflation target with the pull toward supporting growth and credit, and managing the periodic tension between the bank’s autonomy and the government’s priorities, is a recurring feature of its position as a state-owned but operationally independent central bank, the broader principle examined in our explainer on central bank independence.

The third is financial deepening and stability in a fast-growing system. India’s banking and financial sector is expanding rapidly, alongside a boom in digital payments and credit, which brings both opportunity and risk. The bank must supervise a large, diverse financial system, including non-bank lenders whose growth has at times raised stability concerns, while extending formal finance to a population much of which has only recently entered the banking system. Maintaining financial stability as credit deepens, without choking the access that supports growth, is a balance the bank must strike continually as the economy it serves continues its rapid expansion.

Explains

Four ideas behind the Reserve Bank of India

Connect these ideas to the wider library of central banking and inflation articles.

Explore the MASEconomics BlogConclusion

The Reserve Bank of India is a central bank that has spent the past decade narrowing a historically broad mandate into a clear, legislated commitment to price stability. Established in 1935 and nationalized in 1949, it long served as both a monetary authority and a developmental institution, balancing growth, credit, and the currency at the governor’s discretion. The 2016 move to flexible inflation targeting, with a statutory 4% target, a six-member committee, and a formal failure clause, gave it the architecture of a modern inflation-targeting central bank, an architecture renewed for another five years in 2026 and tested successfully through a full rate cycle.

The framework now faces the distinctive pressures of steering monetary policy for 1.45 billion people: an inflation basket dominated by volatile food prices, a standing tension between the inflation mandate and the developmental and growth priorities the bank and the government still carry, and the task of supervising a rapidly deepening financial system without choking the access that supports growth. The repo rate, the policy corridor, and the reserve requirements give the bank a full and direct toolkit, and the external-benchmark link makes its decisions reach borrowers faster than in most economies. Whether the inflation-targeting regime continues to deliver will be judged in the harder moments ahead, when price stability and the pull of growth diverge, but the framework has given India something it lacked for most of its history: a clear and credible monetary anchor.

Frequently Asked Questions

What is the Reserve Bank of India?

The Reserve Bank of India is India’s central bank, established in 1935 and headquartered in Mumbai. It issues the rupee, sets the policy interest rate, regulates banks, manages the exchange rate and foreign reserves, and acts as banker to the government. It has been fully owned by the Government of India since its nationalization in 1949.

What is the RBI’s inflation target?

Under the flexible inflation-targeting framework adopted in 2016, the RBI aims to keep consumer price inflation at 4%, within a tolerance band of 2 to 6%. The target is set in law by the government in consultation with the bank every five years, and it was renewed unchanged for the period from April 2026 to March 2031.

Who sets interest rates in India?

Interest rates are set by the six-member Monetary Policy Committee, created by the 2016 reform. Three members are from the Reserve Bank, including the Governor as chair, and three are external economists appointed by the government. Decisions are made by majority vote, with the Governor holding a casting vote, and the committee meets six times a year.

What is the repo rate?

The repo rate is the rate at which the Reserve Bank lends short-term funds to commercial banks, and it is the bank’s main policy tool. It sits inside a corridor between the Standing Deposit Facility rate, which forms the floor, and the Marginal Standing Facility rate, which forms the ceiling. As of early 2026, the repo rate was 5.25%.

When was the Reserve Bank of India established?

The Reserve Bank of India commenced operations on April 1, 1935, under the Reserve Bank of India Act of 1934, following the recommendation of the Hilton Young Commission. It began as a privately owned institution and was nationalized on January 1, 1949, becoming fully owned by the Government of India.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics