In April 2024, two simultaneous price shocks tested everything economists know about how markets respond. Oil prices fell by nearly nine percent after OPEC unexpectedly raised production, while a US tariff increase pushed imported electronics prices up by 12 percent within weeks. Within a single quarter, gasoline consumption barely moved while imported electronics sales dropped by a third. Two markets, two price shocks of similar magnitude, two completely different outcomes. The concept that explains this is elasticity in economics, the family of measures that turn directional facts about markets into quantitative ones.

Elasticity answers the question that price theory alone cannot. Demand falls when prices rise. Supply rises when prices rise. These are directional facts, and they describe what markets do. Elasticity describes how much. The difference matters because policy decisions, business strategies, and forecasting models all rest on magnitudes, not directions. A fuel tax that consumers barely notice in the short run can transform consumption patterns over a decade. A price cut that boosts revenue in one market destroys it in another. Knowing which case applies requires knowing the elasticity, and that single number has unusual analytical weight in applied economics.

What Elasticity Measures, and Why It Is Unit-Free

Elasticity is a measure of responsiveness. It is calculated as the percentage change in one variable divided by the percentage change in another. Because both numerator and denominator are in percentages, the units cancel. An elasticity of 1.5 means the same thing whether the underlying market is wheat priced in dollars per bushel, smartphones priced in rupees per unit, or housing rents in pounds per month. This unit-free property is what makes elasticities comparable across goods, countries, and time periods, and it is the reason the concept has survived nearly two centuries of empirical work.

GENERAL FORM

The intuition is most easily seen with a single example. If a 10 percent price increase causes quantity demanded to fall by 20 percent, the elasticity is −2. Demand responded twice as strongly as the price stimulus. If the same price increase causes quantity to fall by only 2 percent, the elasticity is −0.2, and demand barely budged. The two numbers describe very different markets, even though the price shock was identical. That is the analytical payoff: a single number distinguishes a flexible market from a rigid one.

The concept was first formalized by Alfred Marshall in 1890, who recognized that the slope of a demand curve is not enough to characterize how a market behaves. The slope depends on units. Elasticity does not. By dividing percentage changes rather than absolute ones, Marshall produced a measure that economists could compare across the dissimilar markets that actual economies contain.

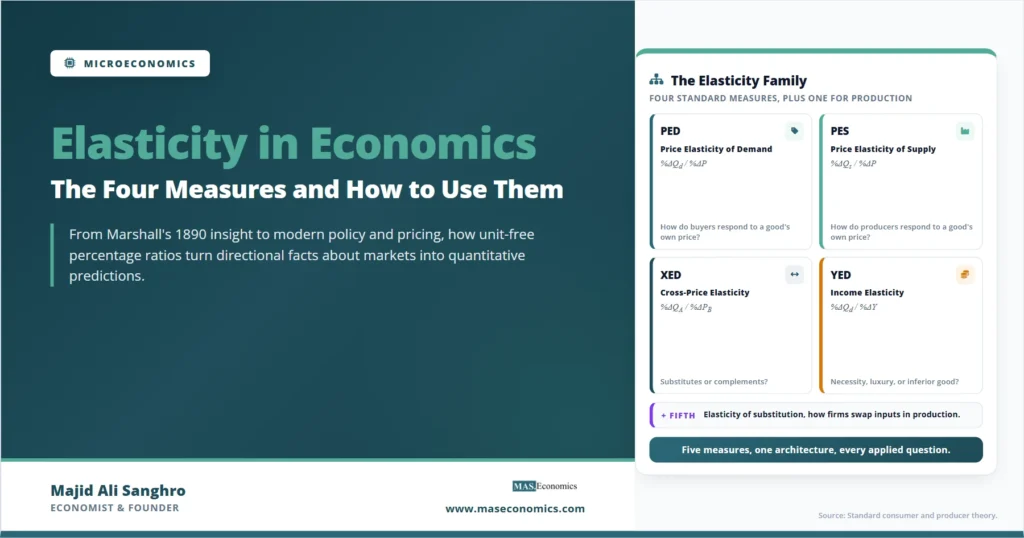

Four Elasticities, Four Different Questions

Modern economics uses four elasticity measures routinely. Each answers a different question, and each is useful in different applied contexts. The differences are clearer when the questions are stated directly.

| Measure | Question it answers | Formula | Typical sign | Read more |

|---|---|---|---|---|

| Price Elasticity of Demand (PED) | How does quantity demanded respond to a change in the good’s own price? | \( \dfrac{\%\Delta Q_d}{\%\Delta P} \) | Negative | See dedicated PED article |

| Price Elasticity of Supply (PES) | How does quantity supplied respond to a change in the good’s own price? | \( \dfrac{\%\Delta Q_s}{\%\Delta P} \) | Positive | See dedicated PES article |

| Cross-Price Elasticity of Demand (XED) | How does quantity demanded of one good respond to a change in the price of another? | \( \dfrac{\%\Delta Q_d^A}{\%\Delta P^B} \) | Positive for substitutes, negative for complements | See dedicated XED article |

| Income Elasticity of Demand (YED) | How does quantity demanded respond to a change in consumer income? | \( \dfrac{\%\Delta Q_d}{\%\Delta \text{Income}} \) | Positive for normal goods, negative for inferior goods | See dedicated YED article |

|

Source: MASEconomics editorial synthesis based on standard consumer and producer theory.

|

||||

The four measures share the same mathematical structure but serve different analytical purposes. PED and PES describe how a single market responds to changes in its own price, and together they determine how taxes are split between buyers and sellers, whether a price cut boosts or shrinks revenue, and how quickly supply can absorb a demand shock. XED describes the relationship between markets, identifying competitors and partners that may not be obvious from product categories alone. YED describes how consumer choices shift with prosperity, organizing decades of empirical work on consumer behavior and the changing composition of demand as economies develop.

Price Elasticity of Demand

Price elasticity of demand measures how strongly the quantity demanded of a good responds when its own price changes. The formula divides the percentage change in quantity demanded by the percentage change in price, and the result is typically negative because the two variables move in opposite directions. Economists usually interpret PED in absolute value when categorizing demand as elastic or inelastic.

The categorization is straightforward. Demand is elastic when the absolute value of PED is greater than one, meaning consumers respond more than proportionally to price changes. Demand is inelastic when the absolute value is below one, meaning quantity barely moves when price changes. The boundary at one matters because it marks the threshold where total revenue starts to move with price: above one, a price cut raises revenue; below one, a price cut lowers it.

The most useful insight in applied work is that PED depends heavily on what alternatives consumers have. A good with many close substitutes carries elastic demand because consumers can switch easily. A good with few substitutes carries inelastic demand because they cannot. This is why insulin, gasoline, and basic utilities carry low PED estimates, while luxury smartphones, designer clothing, and brand-specific consumer goods carry high ones. The time horizon also matters: short-run PED estimates for gasoline after the 1970s oil shocks were around −0.1, while long-run estimates reached −0.6 to −0.8 after consumers had time to switch to fuel-efficient vehicles.

For the full treatment with worked examples, determinants, and applications, the dedicated price elasticity of demand and supply article covers PED in depth alongside its supply-side counterpart.

Price Elasticity of Supply

Price elasticity of supply measures how strongly producers respond to price changes. The formula divides the percentage change in quantity supplied by the percentage change in price. PES is typically positive because higher prices encourage more production. The categorization mirrors PED: elastic supply when PES exceeds one, inelastic when it falls below.

The decisive factor is how quickly producers can adjust their output. A factory with spare capacity, flexible production lines, and abundant inputs can ramp up quickly when prices rise. A farmer constrained by the growing season cannot. A wheat market in the middle of a season is highly inelastic on the supply side; smartphone manufacturing is highly elastic. The wheat PES might be 0.25 in the short run, while the smartphone PES might be 2.5. The contrast reflects production technology, not consumer preferences, and it determines how much of a price spike is absorbed by extra output and how much remains as higher prices.

The time horizon matters even more for supply than for demand. Short-run supply is constrained by fixed factors such as capital stock and skilled labor. Long-run supply allows for capacity expansion, new entrants, and technology adoption. The difference between short-run and long-run supply elasticity is often a factor of three or more, which is why supply shocks have outsized price effects in the immediate term and smaller ones once markets adjust. The dedicated article on price elasticity of demand and supply treats both PED and PES in depth, including their joint role in tax incidence analysis.

Cross-Price Elasticity of Demand

Cross-price elasticity of demand measures how the quantity demanded of one good responds when the price of a different good changes. The formula divides the percentage change in quantity demanded of one good by the percentage change in the price of another. Unlike PED, the sign of XED is informative on its own: it tells you what kind of relationship the two goods have.

A positive XED indicates that the goods are substitutes. When the price of coffee rises, demand for tea rises because some coffee drinkers switch. The XED for tea with respect to coffee might be around plus 0.5, indicating a moderate substitute relationship. The same logic applies to Coca-Cola and Pepsi, generic and brand-name medications, and any pair of products that satisfy similar consumer needs.

A negative XED indicates that the goods are complements. When the price of smartphones rises, demand for phone cases falls because fewer new phones are being purchased. The XED for cases with respect to phones might be around -0.53. Game consoles and games, printers and ink, cars and gasoline all show the same pattern. The negative sign reflects joint consumption: the value of one good depends on access to the other.

A value near zero indicates that the two goods are unrelated. Most random pairs of products fall into this category. Toothpaste and mobile data plans, dishwashers and music streaming services, none of these pairs show measurable cross-price effects, which is why they operate in genuinely separate markets.

The practical use of XED runs across business strategy, antitrust, and tax policy. Firms use it to identify their real competitors, who are not always the firms operating in nominally similar markets. Regulators use it to define competitive markets for merger review, since two products with high positive XED belong to the same market. The dedicated article on cross-price elasticity of demand covers the magnitude thresholds, asymmetries between goods, and dynamic changes in cross-price relationships over time.

Income Elasticity of Demand

Income elasticity of demand measures how consumer spending responds to changes in income, not prices. The formula divides the percentage change in quantity demanded by the percentage change in income. Like XED, the sign of YED is informative: it classifies goods into broad categories that economists have studied for more than a century and a half.

Positive YED defines a normal good. Most goods fall into this category. The further refinement turns on magnitude. A YED between zero and one defines a necessity: demand rises with income, but less than proportionally. Basic food, electricity, and utilities all fit this pattern. A YED above one defines a luxury: demand rises faster than income, so the good takes a growing share of household spending as people get richer. International travel, fine dining, and luxury vehicles fall into this category.

Negative YED defines an inferior good. As income rises, households buy less of it because they substitute toward higher-quality alternatives. Public transportation, generic store-brand groceries, and instant noodles often show this pattern. The label is descriptive, not pejorative: an inferior good is not low quality. It is simply lower on the quality ladder that consumers climb as they grow richer.

The empirical anchor for YED is Engel’s Law, the 1857 observation that the share of household income spent on food declines as income rises. Engel’s regularity has been replicated in nearly every country and decade since, with food YED clustering between 0.3 and 0.5 in modern economies. The same logic extends beyond food: as economies develop, demand shifts predictably from basic necessities to discretionary services. Forecasting these shifts is one of the main uses of YED in applied work, and it underlies projections of how middle-class growth in developing economies will reshape global demand patterns over the coming decades.

The dedicated article on income elasticity of demand covers Engel’s Law, the four-category classification, and the practical applications in business cycle forecasting and tax design.

How the Four Elasticities Connect

The four elasticities are not independent. They interact, and the interactions carry analytical content that no single elasticity captures on its own.

The clearest example is tax incidence. When a government taxes a good, the question of who pays the tax (buyers or sellers) depends on the relative magnitudes of PED and PES. If demand is highly inelastic and supply is elastic, consumers absorb most of the tax because they cannot easily reduce consumption. If supply is inelastic and demand is elastic, producers absorb it because they cannot easily reduce output. This is why excise taxes on gasoline and tobacco fall heavily on consumers, while taxes on commercial real estate often fall on landlords. The joint behavior of PED and PES decides the split.

Another connection runs between YED and PED. The income elasticity of a good and its price elasticity are often related, but not in a fixed way. Necessities tend to be both income-inelastic and price-inelastic because consumers buy them regardless of price and only modestly more when richer. Luxuries tend to be both income-elastic and price-elastic because consumers can postpone or skip purchases. The pattern is empirical, not theoretical, and exceptions are common. Healthcare often shows low price elasticity at the point of consumption (because of insurance) and high income elasticity over long horizons (because of changing standards of care). Quoting one elasticity without checking the other is a frequent source of misleading analysis.

The XED and PED relationship is more subtle. A good with high positive XED to many alternatives also tends to have high own-price elasticity, because consumers facing a price increase have many options to switch toward. A good with low XED to other products tends to have lower own-price elasticity, because the alternatives are weaker. This is why monopoly pricing power and substitute availability are tightly linked in industrial organization theory: a firm whose product has few substitutes (low XED with everything else) can charge prices well above marginal cost without losing customers, while a firm in a market thick with substitutes cannot.

Note. The four elasticities together provide a complete picture of how a market responds to economic shocks. No single elasticity is sufficient on its own. Tax incidence requires PED and PES together. Pricing strategy requires PED and XED together. Long-run demand forecasting requires YED and PED. The interactions are where most applied insight lives.

A Fifth Elasticity: Substitution Between Inputs in Production

The four elasticities above describe consumer behavior and market response. A fifth elasticity, less prominent in introductory treatments but central to growth theory and applied production analysis, describes how firms substitute between inputs. The elasticity of substitution measures the percentage change in the capital-to-labor ratio per one-percent change in the ratio of marginal products, holding output constant.

The concept was formalized by John Hicks in 1932 and reworked by Joan Robinson and others into the form used today. It answers a different question than the demand and supply elasticities: not how consumers respond to price changes, but how firms reorganize production when input prices change. A wage increase pushes firms toward more capital-intensive techniques, and the elasticity of substitution measures how strongly they push.

The applied importance of this fifth elasticity is hard to overstate. It governs how factor shares respond to wage changes, how trade affects wage distribution through the Stolper-Samuelson channel, and whether capital deepening can sustain long-run growth or runs into diminishing returns. In modern quantitative models of growth, trade, and macroeconomics, a single parameter representing the elasticity of substitution often drives the headline results. The dedicated article on elasticity of substitution covers the geometry, the CES production function family, and the empirical estimation challenges that make this parameter one of the most contested in applied economics.

The Time Horizon Cuts Across Every Elasticity

One pattern unifies all five elasticities: they all grow with the time horizon. Short-run elasticities are smaller than long-run elasticities, often by a factor of three or more.

The mechanism is the same in each case. In the short run, consumers and producers face constraints that cannot be relaxed quickly. Consumers have established habits, durable goods already purchased, and limited information about alternatives. Producers have fixed capital, specialized equipment, and labor with current skills. These constraints make short-run responses small even when prices or incomes change sharply.

In the long run, the constraints relax. Consumers replace durables, develop new habits, and discover alternatives. Producers expand capacity, retrain workers, and adopt new technologies. The elasticities measured over five or ten years are therefore systematically larger than those measured over months or quarters. This difference is not a flaw in the measurement; it is a fact about how markets adjust, and it has direct implications for policy.

A fuel tax that produces a small short-run response is often dismissed as ineffective on the consumption side. The long-run response, however, may be three or four times larger as consumers transition to alternative transportation. A minimum wage increase that produces small short-run employment effects may eventually produce larger effects as firms adopt labor-saving technology. Conflating short-run and long-run elasticities is one of the most common sources of misleading policy analysis, and it is why careful empirical work always specifies which horizon a given estimate covers.

Where Elasticities Come From: A Note on Estimation

Elasticity estimates come from empirical data, not from theory alone. The standard estimating equation for any elasticity regresses the log of the response variable on the log of the driver variable, with the slope coefficient interpreted as the elasticity. The simplicity of the equation hides considerable practical difficulty.

Identification is the first challenge. Quantity and price are jointly determined in markets, which makes naïve regressions of quantity on price biased toward zero. Modern empirical work uses instrumental variables, natural experiments, and quasi-experimental variation to isolate the causal effect of price on quantity from the joint determination problem. The same logic applies to income elasticity (where income may correlate with unobserved preferences) and cross-price elasticity (where joint shocks affect multiple markets simultaneously).

Heterogeneity is the second challenge. Elasticities differ across households, regions, time periods, and product subcategories. A pooled estimate that averages across these dimensions can mask substantial variation underneath, and policy decisions made on average estimates may fail in subgroups where the elasticity is very different. The trend in applied work over the past two decades has been toward more granular estimates that exploit microdata to capture this heterogeneity.

The third challenge is functional form. The elasticity formula assumes a constant percentage relationship, but real demand curves often have varying elasticity along their length. A demand curve that is elastic at high prices may become inelastic at low prices. Empirical work increasingly uses flexible functional forms that allow elasticity to vary across the price range, rather than imposing a single constant value.

Why Elasticities Matter Beyond the Classroom

The elasticities are not abstract pedagogical devices. They sit at the center of nearly every applied economic question that involves a quantitative response.

Central banks use price elasticity estimates to forecast how monetary policy will affect aggregate demand. Tax authorities use income and price elasticities to predict revenue from changes in tax rates. Antitrust authorities use cross-price elasticity to define competitive markets. Business strategists use all four to set prices, plan capacity, and identify competitors. Trade economists use the elasticity of substitution to model how globalization affects wages. International organizations use income elasticity to project consumer demand patterns as developing economies grow.

In each application, the elasticity is the bridge between economic theory and quantitative prediction. Theory says demand falls when price rises. Elasticity says by how much, in this market, over this horizon, for this consumer group. The qualifiers matter, and they are what make elasticity a serious empirical concept rather than a textbook abstraction. The applied economist’s job is often to estimate the relevant elasticity carefully, defend the estimate against alternatives, and trace through what the magnitude implies for the question at hand.

Explains

Four ideas that anchor the elasticity family

Continue building your microeconomics foundation with related explainers.

Explore the MASEconomics BlogConclusion

The family of elasticity in economics measures takes the directional facts of supply and demand theory and turns them into quantitative predictions. Five members of the family, four for consumer and market behavior and one for production, cover most of the empirical territory that applied economics works in. Each answers a different question. PED measures how consumers respond to a good’s own price. PES measures how producers respond. XED measures how markets connect to one another. YED measures how consumption shifts with income. The elasticity of substitution measures how firms reorganize production when input prices change.

The numbers themselves are useful, but the deeper value is what they discipline. A policy proposal that does not specify the relevant elasticities is incomplete. A business strategy that assumes elasticities without estimating them is risky. A forecast that confuses short-run and long-run elasticities will misstate the trajectory of adjustment. Marshall’s 1890 insight, that the responsiveness of markets is best measured in unit-free percentage ratios, remains the foundation of how economists answer the most practical question in their toolkit: by how much. Each of the dedicated articles in this elasticity series builds out one branch of that answer in detail, and together they provide the full applied vocabulary for thinking quantitatively about how markets respond.

Frequently Asked Questions

What is elasticity in economics?

Elasticity in economics is a unit-free measure of how strongly one variable responds to a change in another, calculated as the ratio of percentage changes. The four most common forms are price elasticity of demand, price elasticity of supply, cross-price elasticity of demand, and income elasticity of demand. A fifth, the elasticity of substitution, describes how firms substitute between inputs in production.

What are the four types of elasticity in economics?

The four standard elasticities are: price elasticity of demand (how quantity demanded responds to the good’s own price), price elasticity of supply (how quantity supplied responds to the good’s own price), cross-price elasticity of demand (how demand for one good responds to the price of another), and income elasticity of demand (how demand responds to changes in consumer income). Each measures a different aspect of how markets respond to economic shocks.

Why is elasticity unit-free?

Because elasticity is calculated as a ratio of percentage changes, the units in the numerator and denominator cancel. An elasticity of 1.5 means the same thing whether the underlying market is in dollars, rupees, or pounds, and whether the quantity is measured in tons, units, or hours. This makes elasticities directly comparable across goods, countries, and time periods, which is why they have become the standard measure of responsiveness in applied economics.

What does it mean for demand to be elastic or inelastic?

Demand is elastic when the absolute value of the price elasticity exceeds one, meaning quantity demanded responds more than proportionally to price changes. Demand is inelastic when the absolute value is below one, meaning quantity barely moves when price changes. The threshold at one matters because it marks the point where total revenue stops moving with price.

Who developed the concept of elasticity?

The concept was first formalized by Alfred Marshall in his 1890 work Principles of Economics. Marshall recognized that the slope of a demand curve depends on units of measurement and is therefore not directly comparable across markets. By dividing percentage changes rather than absolute ones, he produced a measure that allows comparison across the dissimilar markets that real economies contain. The elasticity of substitution was added later by John Hicks in 1932 for production analysis.

Why does the time horizon matter for elasticity estimates?

Short-run elasticities are typically smaller than long-run elasticities, often by a factor of three or more, because consumers and producers face constraints that relax over time. Consumers have established habits and durable goods that limit short-run substitution; firms have fixed capital that limits short-run output adjustment. Over longer horizons, both consumers and producers can re-optimize fully, producing much larger elasticities. Conflating the two horizons is one of the most common sources of misleading economic analysis.

How are elasticities used in tax policy?

Tax incidence depends on the relative magnitudes of price elasticity of demand and price elasticity of supply. When demand is inelastic and supply is elastic, consumers absorb most of a tax because they cannot easily reduce consumption. When supply is inelastic and demand is elastic, producers absorb it. Excise taxes on gasoline, tobacco, and alcohol generate stable revenue precisely because demand for these goods is inelastic. Income elasticity guides progressive tax design, and cross-price elasticity warns of spillover effects into related markets.

What is the difference between elasticity and slope?

The slope of a demand or supply curve measures the absolute change in quantity per absolute change in price, and it depends on the units used to measure both. Elasticity measures the percentage change in quantity per percentage change in price, and it is unit-free. Two demand curves can have identical slopes but very different elasticities at different points along the curve, which is why elasticity is the more useful measure for applied economic analysis.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics