On January 26, 2026, the Monetary Policy Committee of the State Bank of Pakistan held its policy rate at 10.5%, the level it had reached after cutting from a record 22% over the preceding eighteen months. The decision was unremarkable in itself, a hold to consolidate disinflation, but the body that made it would have been unrecognizable a few years earlier. Until recently, the central bank set monetary policy in close coordination with the Ministry of Finance, financed government deficits on demand, and operated as something close to an extension of fiscal policy. Today it sets rates through a statutory committee, is legally barred from lending to the government, and names price stability as its overriding objective. The transformation is the most consequential institutional reform in the bank’s modern history.

The State Bank of Pakistan is the central bank of a country of roughly 240 million people. Inaugurated in 1948 by Muhammad Ali Jinnah as a symbol of the new state’s financial sovereignty, it issues the rupee, sets the policy rate, regulates the banking system, manages the country’s foreign reserves, and acts as the lender of last resort. What makes it analytically interesting is not the standard list of central bank functions but the gap between its new legal mandate and the economic reality it operates in. An economy with chronic fiscal deficits, heavy debt, and recurring balance-of-payments crises is precisely the environment in which central bank independence is hardest to sustain, and the SBP’s recent grant of autonomy is being tested against exactly those pressures.

Central Bank Born With the State

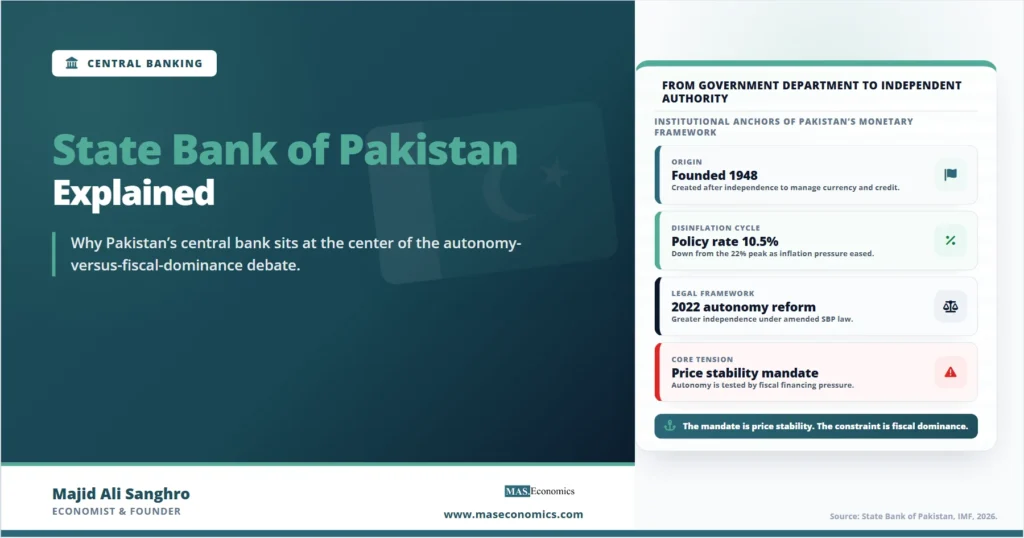

The State Bank of Pakistan was among the first institutions the new country built. When Pakistan came into being in 1947, the Reserve Bank of India continued to act as its currency and banking authority under a transitional arrangement. That arrangement was cut short, and in 1948 the assets of the colonial central bank were divided between the two successor states. Muhammad Ali Jinnah, traveling from Ziarat to Karachi despite failing health, inaugurated the State Bank of Pakistan on July 1, 1948, in a ceremony he framed explicitly as an assertion of monetary sovereignty. Zahid Husain became the first governor. The symbolism mattered: a central bank and a national currency were treated as essential attributes of independent statehood, not merely as technical machinery.

The institution’s legal foundation was set by the State Bank of Pakistan Act of 1956, which has governed it ever since and which the modern reforms have amended rather than replaced. The bank is wholly state-owned, headquartered in Karachi, the country’s financial capital, and its governor serves as chief executive. For most of its history it carried out the full range of central banking functions while remaining, in practice, subordinate to the federal government. Until the early 1990s, it was administratively treated as an arm of the Ministry of Finance: its board and governor could be appointed and removed at will, it could not publish its own analysis without clearance, and monetary policy was widely understood as an extension of fiscal policy rather than an independent discipline.

That subordination is the backdrop against which the recent reforms must be read. The history of the State Bank of Pakistan is, to a large degree, the history of a slow and contested effort to convert a government department into an independent monetary authority.

The 2022 Autonomy Reform

The decisive break came with the State Bank of Pakistan Amendment Act, passed by Parliament and effective in early 2022. Adopted as a prior action under an IMF program, the amendment rewrote the bank’s mandate, governance, and relationship with the government along the lines of modern central banking practice. It is the single most important development in understanding the institution today.

The reform did several distinct things. It established a clear hierarchy of objectives, naming domestic price stability as the primary goal, with financial stability as a secondary objective and support for the government’s economic policies, including growth, as a tertiary one only insofar as it does not conflict with the first two. This ordering moved the bank toward a framework of flexible inflation targeting, in which controlling inflation is the overriding mission. It is a meaningful departure from the older model in which the bank balanced growth, the exchange rate, and the financing needs of the government with no clear priority among them.

The amendment also prohibited monetary financing of the government. The practice of the central bank lending directly to the treasury, in effect printing money to cover fiscal deficits, is one of the classic drivers of high inflation, and the law now bars it. It strengthened the security of tenure for the governor, deputy governors, and members of the policy committee, protecting them from arbitrary dismissal so they can take unpopular decisions without fear of removal. It freed the bank’s administration from Ministry of Finance supervision. And, to balance this new independence with democratic accountability, it strengthened the bank’s reporting obligations to Parliament, where the governor must account for the conduct of monetary policy and the achievement of the bank’s objectives.

The reform was not without controversy. Critics argued that it concentrated extensive powers and legal protections in the governor and the bank, and that an autonomous central bank inside a fiscally fragile state risked creating an unaccountable authority. Supporters countered that insulating monetary policy from short-term political pressure was exactly what Pakistan’s history of inflation and fiscal dominance demanded. That debate is a specific instance of the broader question explored in our explainer on central bank independence: independence is valuable precisely because it lets a central bank resist the temptation to finance deficits and inflate, but it must be paired with genuine accountability to remain legitimate.

Monetary Policy Committee Decisions

Monetary policy is set by the Monetary Policy Committee, a statutory body that held its first meeting in early 2016 and was strengthened by the 2022 reform. The committee is the locus of the bank’s new independence, and its design reflects an attempt to bring outside judgment into decisions that were once taken internally and in coordination with the government.

The committee is chaired by the governor, who as of 2026 is Jameel Ahmad. Its membership combines three groups: senior ex officio officials of the State Bank, non-executive members of the bank’s Board of Directors, and external economists appointed by the federal government to bring independent expertise and perspective. This mix is deliberate. The external members are meant to prevent groupthink and to subject the bank’s internal view to outside challenge, while the institutional members ensure operational continuity. The committee meets on a regular schedule, typically several times a year, sets the policy rate, and publishes a monetary policy statement explaining the decision along with the governor’s press conference.

Around the committee sit two other bodies created or clarified by the reform. The Board of Directors oversees the bank’s general administration and finances but does not set monetary policy. An Executive Committee, comprising the governor and deputy governors, handles the bank’s core operational and management decisions that fall outside the remit of either the policy committee or the board. This separation of monetary policy, governance, and administration into distinct bodies is itself a modernization, replacing a structure in which authority was less clearly divided.

The communication practice has improved markedly. The bank now publishes detailed monetary policy statements, holds press conferences, and reports to Parliament, a degree of transparency that supports the credibility its inflation-targeting framework requires. The logic of how that framework anchors expectations is the subject of our explainer on inflation targeting, and the broader role of a credible nominal anchor is covered in our piece on monetary anchors.

The Policy Toolkit

The State Bank’s instruments are those of a conventional inflation-targeting central bank, adapted to a developing financial system. The table below sets out the main tools.

| Tool | What It Does | Typical Use |

|---|---|---|

| Policy (target) rate | The benchmark rate that anchors short-term borrowing costs across the economy | Set by the Monetary Policy Committee to steer inflation toward target |

| Interest rate corridor | A ceiling and floor around the policy rate that keep market rates in range | Used continuously to implement the rate decision |

| Open market operations | Injecting or draining liquidity through repo and reverse repo operations | Day-to-day management of money-market liquidity |

| Cash reserve and liquidity requirements | The reserves and liquid assets banks must hold against deposits | Adjusted to influence the supply of credit and bank liquidity |

| Foreign exchange operations | Buying or selling foreign currency and managing reserves | Rebuilding reserves and smoothing disorderly exchange-rate moves |

| Regulation and supervision | Licensing, capital rules, and oversight of banks and financial institutions | Continuous prudential supervision of the financial system |

| Lender of last resort | Emergency liquidity to solvent banks during stress | Financial-stability backstop in a crisis |

|

Source: State Bank of Pakistan Act and SBP monetary policy documentation, 2022–2026.

|

||

The policy rate is the headline instrument, and its recent path tells the story of the post-crisis stabilization. Facing inflation that climbed above 23%, the committee raised the rate to a record 22% to break the inflationary spiral and stabilize the rupee. As inflation fell sharply through 2024 and 2025, reaching a multi-year low, the committee cut the rate by roughly 1,150 basis points to 10.5%, easing the cost of borrowing while keeping policy restrictive enough to hold inflation inside its 5 to 7% target range. The exchange-rate operations have run alongside this: with a market-determined rupee as an IMF program condition, the bank has used foreign exchange purchases to rebuild reserves, which climbed toward the $16 to $18 billion range, rather than to defend a fixed rate. The way these rate changes work through the wider economy is set out in our explainer on the monetary transmission mechanism.

Autonomy Against the Pull of Fiscal Dominance

The central question facing the State Bank of Pakistan is whether its new legal independence can survive the economic environment it operates in. That environment is defined by fiscal dominance, the condition in which a government’s fiscal position is so strained that monetary policy ends up being shaped by the need to finance the deficit and manage the public debt rather than by the pursuit of price stability.

Pakistan’s public finances are the textbook setting for this problem. The state runs persistent deficits, carries a heavy stock of domestic and external debt, collects too little tax, and spends a large share of its budget on interest. In such conditions, even a legally independent central bank faces intense indirect pressure. High interest rates, the natural tool against inflation, also raise the government’s borrowing costs and worsen the deficit, creating a standing tension between the bank’s mandate and the treasury’s solvency. The prohibition on monetary financing closes the most direct channel of fiscal dominance, but it does not eliminate the underlying pull. The dynamics of how government debt can constrain a central bank are exactly those we examine in the context of the wider economy in our profile of the economies we cover and in Pakistan’s own case in our coverage of structural financial reform.

The bank’s autonomy is therefore conditional in practice even where it is unconditional in law. Its independence holds most easily when it aligns with the government’s interest, as during a disinflation that everyone wants, and is tested hardest when the two diverge, as when fighting inflation requires rates high enough to strain the budget. The reform gave the institution the legal architecture of an independent central bank. Whether that architecture proves durable depends less on the statute than on whether Pakistan can repair its public finances, broaden its tax base, and reduce its debt burden enough that monetary and fiscal policy stop pulling against each other. This is the same fragility that defines the country’s recurring boom-bust cycle, traced in our profile of the broader Pakistani economy.

There is also the question of the exchange rate and the financial account. The bank manages a market-determined rupee, but it must do so while rebuilding reserves from low levels and while remittances and external borrowing, rather than exports, finance the import bill. A central bank in this position has less room to run a purely domestic monetary policy than one in an economy with deep reserves and strong export earnings, because every move has implications for the currency and the external accounts. The bank’s use of exchange-rate and reserve management tools reflects this constraint.

What the Next Decade Will Test

Three issues will determine whether the State Bank’s modern framework holds.

The first is the durability of the autonomy reform itself. Legal independence granted under an IMF program can be eroded after the program ends, through amendment, through informal pressure, or through appointments. The credibility the bank has begun to build rests on the expectation that the framework is permanent. Whether successive governments respect it when fighting inflation becomes politically costly is the central test, and it is the same test of central bank independence that plays out, in different forms, in every economy.

The second is the inflation-targeting framework under supply shocks. Pakistan’s inflation is driven heavily by factors outside the bank’s control: global energy and food prices, the exchange rate, and administered increases in fuel and electricity tariffs. A framework built to manage demand-driven inflation is harder to operate when the shocks are on the supply side, because raising rates does little to reverse an oil-price spike while still imposing a cost on growth. The bank’s ability to keep expectations anchored through such shocks, rather than merely reacting to them, will define the success of the new regime.

The third is financial deepening and inclusion. A large share of Pakistan’s economy operates informally and outside the banking system, which weakens the transmission of monetary policy and limits the reach of the financial sector. The bank’s longer-term agenda includes expanding financial inclusion, modernizing the payment system, and developing digital finance, the area covered in our piece on Pakistan’s digital currency ambitions. A deeper, more formal financial system would make monetary policy more effective and the economy more resilient, and building it is as important to the bank’s long-run mandate as any single rate decision.

Explains

Four ideas behind the State Bank of Pakistan

Connect these ideas to the wider library of central banking and inflation articles.

Explore the MASEconomics BlogConclusion

The State Bank of Pakistan is an institution in the middle of a transformation. Inaugurated in 1948 as a symbol of the new state’s sovereignty, it spent most of its history as an instrument of fiscal policy, financing deficits and setting rates in coordination with the Ministry of Finance. The 2022 amendment rewrote that relationship, naming price stability as the bank’s primary objective, prohibiting monetary financing, protecting the tenure of its decision-makers, and vesting monetary policy in an independent committee accountable to Parliament. The disinflation since, from above 23% to single digits, and the cut in the policy rate from 22% to 10.5%, is the first major test the new framework has passed.

Whether the transformation endures is a different question from whether it has begun. The bank’s legal independence operates inside an economy of chronic deficits, heavy debt, and recurring external crises, the conditions under which fiscal dominance is hardest to resist. Its autonomy will be tested not in calm periods but when fighting inflation collides with the government’s need for cheap borrowing, and its inflation-targeting framework will be tested by the supply shocks that drive much of Pakistan’s inflation. The institution now has the architecture of a modern central bank. Whether that architecture holds depends, in the end, less on the State Bank itself than on whether Pakistan repairs the public finances that have constrained it for most of its history.

Frequently Asked Questions

What is the State Bank of Pakistan?

The State Bank of Pakistan is the central bank of Pakistan, headquartered in Karachi and inaugurated in 1948. It issues the Pakistani rupee, sets the policy interest rate, regulates and supervises banks, manages the country’s foreign exchange reserves, and acts as a lender of last resort. Since a 2022 reform it operates with legal autonomy and names price stability as its primary objective.

Is the State Bank of Pakistan independent?

The State Bank of Pakistan Amendment Act, effective in 2022, granted the bank legal autonomy, made price stability its primary objective, prohibited it from financing government deficits, and protected the tenure of its decision-makers, while making it accountable to Parliament. In practice, its independence is tested by the country’s strained public finances, a condition known as fiscal dominance.

Who sets interest rates in Pakistan?

Interest rates are set by the Monetary Policy Committee of the State Bank of Pakistan, which first met in 2016 and was strengthened by the 2022 reform. The committee is chaired by the governor and includes senior bank officials, non-executive board members, and external economists appointed by the government. It meets several times a year and publishes a statement with each decision.

When was the State Bank of Pakistan established?

The State Bank of Pakistan was inaugurated on July 1, 1948, by Muhammad Ali Jinnah, who framed it as a symbol of the new state’s financial sovereignty. It took over the central banking role previously held by the Reserve Bank of India, and its first governor was Zahid Husain. Its current legal basis is the State Bank of Pakistan Act of 1956, as amended.

What is the State Bank of Pakistan’s inflation target?

The bank operates a flexible inflation-targeting framework with price stability as its primary objective. In the current cycle it has aimed to keep inflation within a 5 to 7% range over the medium term, using the policy rate as its main tool. Inflation had fallen from above 23% to single digits by 2025, allowing the bank to cut its policy rate substantially.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics