On June 12, 2026, Finance Minister Muhammad Aurangzeb stood before a National Assembly session that began two hours late and was interrupted by opposition protests and presented a federal budget with a total outlay of Rs18,771 billion. The headline numbers of the Pakistan budget 2026-27 are a 4 percent growth target, average inflation projected at 8.2 percent, a federal deficit held to 3.6 percent of GDP, and a record Federal Board of Revenue collection target of Rs15,264 billion. Beneath those headlines sits a more revealing arithmetic, and that arithmetic is the real subject of this analysis.

A budget is not a wish list. It is a constraint made visible. Every rupee the government plans to spend has to be raised, borrowed, or transferred, and the structure of those flows tells you far more about the state of the economy than any single growth target. The most important fact in this document is not the size of the budget but how little of it the federal government actually controls once interest payments and the constitutionally mandated provincial share are accounted for. That is where this analysis begins.

Centre’s Net Revenue Constraint

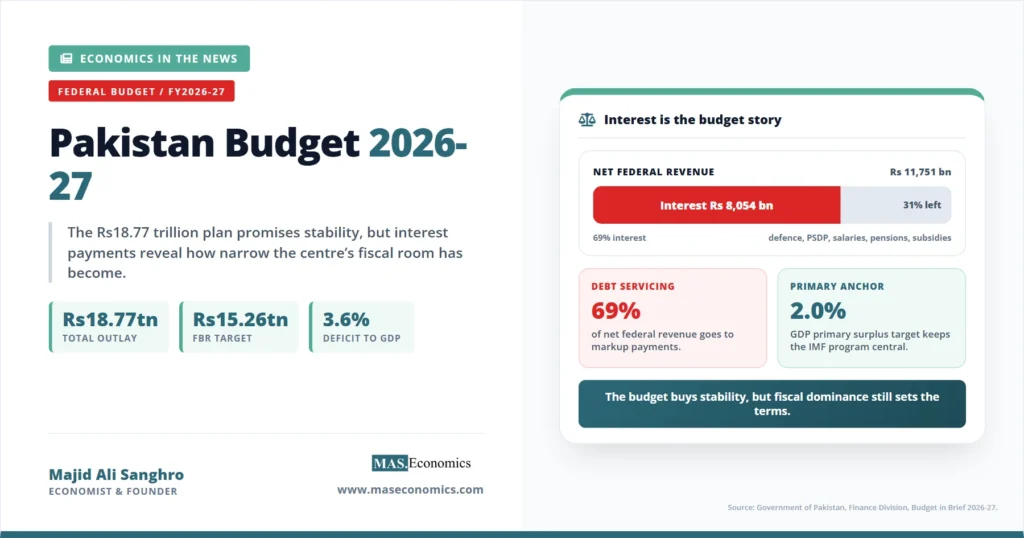

Start with gross revenue. The budget projects gross revenue receipts of Rs20,600 billion, of which FBR taxes account for Rs15,264 billion and non-tax revenue for the remainder. From that gross figure, a large slice is removed before the federal government can spend a rupee on its own priorities. Under the National Finance Commission award, provinces receive their constitutional share of the divisible pool, budgeted at Rs8,848 billion for the coming year. After this transfer, net revenue for the federal government falls to Rs11,751 billion.

That single transfer, set out in the seventh NFC framework that assigns provinces fifty-seven and a half percent of the divisible pool, reshapes the entire fiscal picture. The federal government is responsible for defence, debt servicing, and the bulk of national development, yet it keeps barely more than half of the taxes it collects. The waterfall below shows the descent from gross collection to the deficit that remains after spending.

With net revenue of Rs11,751 billion and total expenditure of Rs18,771 billion, the federal government runs a deficit of Rs7,020 billion, which it must finance entirely through borrowing. This gap, equal to roughly 3.6 percent of the projected nominal GDP of Rs143,604 billion, is the number every other choice in the budget bends around.

Interest Payments Dominate Spending

The single largest line in the entire budget is not defence, development, or salaries. It is the cost of servicing debt the government has already accumulated. Markup payments for the coming year are budgeted at Rs8,054 billion, with the overwhelming majority owed on domestic debt rather than foreign loans. To see what that means, set it against the Rs11,751 billion the federal government actually keeps.

Interest consumes about sixty-nine percent of net federal revenue. Once that obligation is met, only around Rs3,697 billion of genuinely federal money remains to cover defence, the federal development program, the running of civil government, pensions, subsidies, and grants. Since those commitments together far exceed Rs3,697 billion, the shortfall is bridged by borrowing, which adds to next year’s debt stock, which raises the following year’s interest bill. This is the mechanics of fiscal dominance, where debt servicing crowds out everything a government might otherwise choose to do. It is the same trap explored in our analysis of debt sustainability, and it is the defining feature of Pakistan’s public finances.

There is one piece of modestly good news buried in the interest line. Budgeted markup of Rs8,054 billion is slightly below the Rs8,206 billion budgeted a year earlier, reflecting the sharp fall in the State Bank’s policy rate as inflation came down from its crisis peak. Lower rates reduce the cost of rolling over domestic debt. That relief is real but fragile: it depends on inflation staying contained, and the budget itself projects inflation rising from about 7 percent in the outgoing year to 8.2 percent in the year ahead, partly because of the regional energy shock. The connection between the policy rate and the government’s borrowing cost is set out in our explainer on the State Bank of Pakistan.

Allocation Shifts in the Budget

Because the federal government has so little discretionary room, the choices it does make are revealing. Comparing this year’s budgeted allocations to last year’s budget shows where the priorities shifted.

Defence affairs and services rose to Rs3,000 billion, a 17.6 percent increase over the Rs2,550 billion budgeted a year earlier. The finance minister framed this explicitly in terms of regional security and what he described as Pakistan’s demonstrated defence capability. In a budget where almost every other discretionary line was squeezed, defence received the clearest real-terms increase, which signals where political priority sits.

Development spending moved the other way. The federal Public Sector Development Program, the part of the budget that builds roads, dams, power infrastructure, and human capital, was held roughly flat in nominal terms and cut once inflation is accounted for. The total national PSDP, including provincial and state-owned-enterprise components, was budgeted lower than the previous year. Development is the most politically expendable line because its benefits are slow and diffuse, while interest and defence are non-negotiable. The predictable result is that the investment a country needs for future growth is the first thing sacrificed to current obligations. Subsidies were also trimmed, from Rs1,186 billion to Rs1,091 billion, with the composition shifting toward targeted power-sector support and away from broad commodity subsidies.

Revenue Plan and FBR Targets

The FBR target of Rs15,264 billion is the most scrutinized number in any Pakistani budget, because it is the one the government most often misses. It represents an increase of roughly 8 percent over the Rs14,131 billion budgeted last year, but the more telling comparison is against the revised collection for the outgoing year, which the document records at Rs12,983 billion. Measured against what was actually collected, the new target requires growth closer to 17 to 18 percent.

| Measure | Amount (Rs bn) | What it tells you |

|---|---|---|

| FY2025-26 budget target | 14,131 | What was promised last year |

| FY2025-26 revised (actual projection) | 12,983 | What was actually collected, a shortfall of about Rs1,148 bn |

| FY2026-27 budget target | 15,264 | The new promise |

| Implied growth over actual | ~17.6% | The real climb the FBR must achieve, not the headline 8% |

|

Source: Budget in Brief 2026-27, Tables 3 and 4.

|

||

The government argues it can close most of this gap without broad new taxes. The plan rests on autonomous growth, meaning the natural rise in tax receipts as nominal GDP expands at the projected 4 percent real growth plus 8.2 percent inflation, supplemented by enforcement and digitization rather than higher rates. Production monitoring, retail formalization, and a fixed-tax scheme for smaller retailers are expected to bring untaxed activity into the net. This is the same documentation problem that our earlier piece on Pakistan’s tax system and digitalization examined, and the budget’s credibility rests on whether enforcement finally delivers what rate increases alone never could.

The risk is structural. Pakistan’s tax base is narrow and leans heavily on indirect taxes and on a small, fully documented salaried class whose income is withheld at source. When collection falls short, the government’s instinct has historically been to lean harder on the groups already in the net rather than to widen it. Whether this budget breaks that pattern is the central test of its revenue plan.

Salaried Relief Under IMF Constraints

The most direct change ordinary earners will feel is the cut in income tax for the salaried class. After several years of rising burden, the budget reduced rates across four income slabs and abolished the surcharge that high earners paid on top of their income tax. For income between Rs2.2 million and Rs3.2 million a year, the rate falls to 20 percent; for Rs3.2 million to Rs4.1 million, it drops from 30 to 25 percent; higher slabs were eased as well. A 7 percent increase in salaries and pensions for federal employees and a 10 percent rise in the minimum monthly wage to Rs40,700 accompany the rate cuts.

Note. The relief is real but not a net tax cut for the economy. Under the IMF Extended Fund Facility, the government must still hit its revenue target and maintain a primary surplus. Every rupee of salaried relief has to be recovered elsewhere, through enforcement, base-broadening, or other measures. The slab cuts reflect a judgment that the salaried class was overtaxed relative to its share of national income, not a loosening of the overall fiscal stance.

This is the honest way to read the relief. The salaried class is one of the few fully documented segments, and it had absorbed a disproportionate share of recent tax increases precisely because its income could not be hidden. Easing that burden is fair, but within an IMF program that fixes the revenue and primary-surplus targets, the relief is a reallocation, not a reduction. The pressure simply moves to whoever the enforcement effort can reach next.

Deficit, Primary Surplus, and IMF Anchor

The budget targets a federal deficit of Rs7,020 billion, about 3.6 percent of GDP, down from the 3.9 percent targeted a year earlier. More important than the headline deficit is the primary balance, which strips out interest payments to show whether the government’s own day-to-day operations are in surplus or deficit. The budget targets a primary surplus of about 2 percent of GDP.

The distinction matters because it isolates what the government can control. Interest is a legacy cost of past borrowing; the primary balance reflects current policy. A primary surplus means that, setting aside inherited debt service, the government is taking in more than it spends, which is the precondition for the debt-to-GDP ratio to stabilize and eventually fall. This is the IMF program’s core anchor. The Extended Fund Facility requires Pakistan to run a primary surplus while hitting its revenue target, and the entire budget is built backward from that constraint. The logic of why a primary surplus is the hinge of any debt-stabilization effort is laid out in our piece on sovereign debt sustainability.

The financing plan shows how the Rs7,020 billion gap is filled. The bulk comes from domestic borrowing through government securities, with a smaller contribution from net external financing and a token Rs161 billion pencilled in from privatization proceeds. The heavy reliance on domestic borrowing is itself a warning: it is what keeps the interest bill growing, and it ties the government’s fortunes tightly to the level of domestic interest rates and the appetite of local banks to keep lending to the state.

| Financing source | Amount (Rs bn) | Nature |

|---|---|---|

| Net domestic financing (govt securities and savings) | 6,046 | Borrowing from local banks and the public |

| Net external financing | 813 | Multilateral, bilateral, and commercial sources |

| Privatization proceeds | 161 | Asset sales, historically optimistic |

| Total financing | 7,020 | Equals the federal deficit |

|

Source: Budget in Brief 2026-27, Table 2.

|

||

Budget Structure Remains Unchanged

For all the relief measures and the defence increase, the structure of the budget is almost identical to last year’s and the year before. Interest still dominates. Provincial transfers still claim a constitutional first call on revenue. Development is still the residual that absorbs the squeeze. The revenue target still depends on enforcement gains that have repeatedly disappointed. Privatization proceeds are still budgeted at a level the government rarely achieves.

This continuity is the most important analytical point in the whole document. A budget that changes the headline numbers but leaves the structure untouched is a budget that manages the crisis rather than resolving it. The path out of fiscal dominance runs through two changes the budget gestures at but does not deliver: a genuinely broader tax base that brings agriculture, retail, and real estate into proportionate contribution, and a primary surplus large enough and sustained long enough to bend the debt trajectory down. Until those arrive, each year’s budget will look much like this one, with the interest bill setting the terms and everything else fitting into what remains. The broader pattern of stabilization without structural escape is the theme of our profile of the Pakistan economy.

There are reasons for cautious optimism. Inflation has fallen sharply from its crisis peak, which lowered the policy rate and gave the budget its small interest reprieve. Remittances are running near record levels and increasingly flow through formal banking channels, supporting the external account. The macroeconomic stability achieved under the current IMF program is real, and it is the foundation on which any future reform would have to be built. The fuel and energy prices that feed directly into household budgets and into the subsidy bill remain a live risk, a dynamic our earlier piece on the fuel price hike in Pakistan examined in detail.

Assessing the Budget as a Whole

The Pakistan budget 2026-27 is best understood not as a growth plan but as a stability plan operating inside very tight constraints. Its central reality is that interest payments consume roughly sixty-nine percent of net federal revenue, leaving the government with little genuine room to maneuver. Within that constraint, the budget made a clear choice to raise defence by 17.6 percent, deliver overdue relief to the salaried class, and hold the deficit to 3.6 percent of GDP while targeting a 2 percent primary surplus, all to keep the IMF program on track.

What it did not do is change the structure that produces the squeeze in the first place. The revenue plan still rests on enforcement gains that must materialize, the tax base remains narrow, and development spending was again the line that gave way. The budget buys another year of stability, which for an economy that has lurched through repeated crises is not a trivial achievement. But stability purchased by holding the structure in place is not the same as the structural reform that would eventually make the next budget easier to write. On the evidence of this document, that harder work still lies ahead.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics