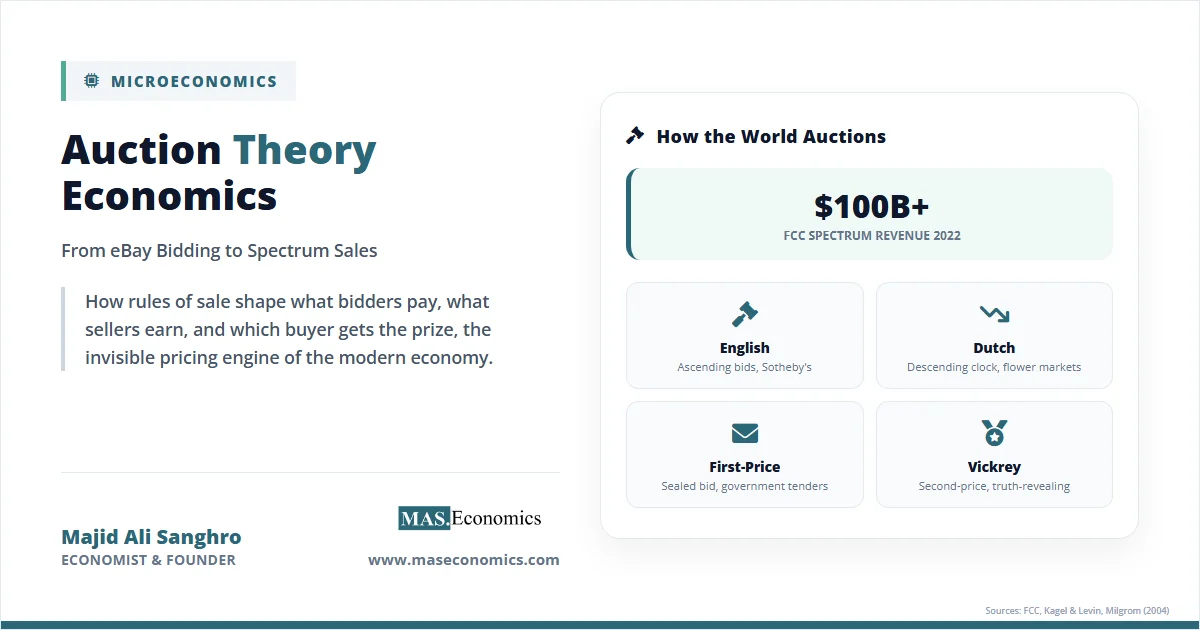

In 2022, the US Federal Communications Commission’s spectrum auctions raised over $100 billion in cumulative revenue across multiple bands, with the C-band auction alone clearing $81 billion. That same year, a single bidder paid $450.3 million for Leonardo da Vinci’s Salvator Mundi at Christie’s, the highest price ever recorded at auction. Every second of the day, Google’s ad system runs millions of automated auctions to decide which advertiser appears on a search results page.

Auction theory economics is the branch of microeconomics that studies how rules of sale shape what bidders pay, what sellers earn, and which buyer ends up with the prize. Auctions are the invisible pricing engine of the modern economy. They allocate radio spectrum, internet ad slots, US Treasury bonds, electricity, fine art, fish at the dawn market in Tokyo, and footballers at the transfer window. The 2020 Nobel Prize in Economic Sciences went to Paul Milgrom and Robert Wilson for improvements to auction theory and inventions of new auction formats, recognising the field as one of the most successful applications of economic theory to real markets.

The strange thing about auctions is that the seller does not know what bidders are willing to pay. Auction theory is the science of designing rules that extract this private information through bids while still producing efficient outcomes.

Core Concepts of Auction Theory

Most markets assume the seller posts a price and buyers decide whether to pay it. Auctions invert that logic. The seller does not know each buyer’s valuation and uses the bidding process itself to discover prices. The whole field studies one question: which set of rules produces the best outcome for the seller, the buyers, or society, given that valuations are private information.

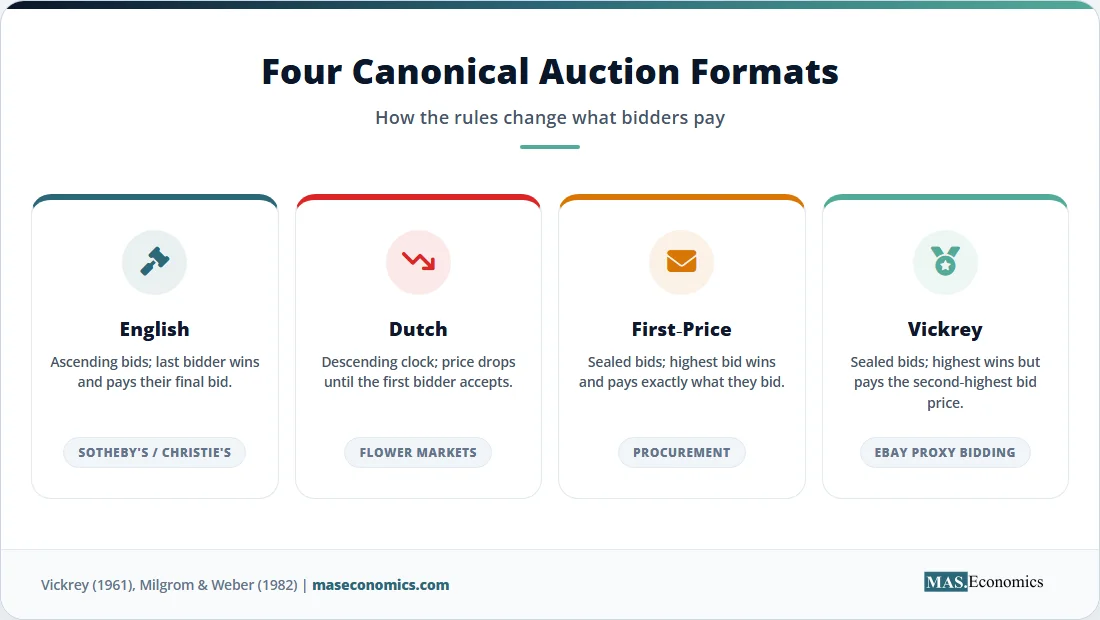

Four canonical formats anchor the theory. The English auction is the open ascending format used at Sotheby’s and Christie’s: the price rises until only one bidder remains. The Dutch auction works in reverse, with the auctioneer announcing a high price that falls until a bidder accepts. It is named after the Aalsmeer flower auction in the Netherlands, where billions of cut flowers move through descending-clock auctions every year. The first-price sealed-bid auction asks each bidder to submit one bid in a sealed envelope; the highest bidder wins and pays their bid. The second-price sealed-bid auction, named after Columbia economist William Vickrey, who analysed it in 1961, also gives the object to the highest bidder, but the winner pays the second-highest bid.

Three valuation models classify auction settings. In the private values model, each bidder knows their own valuation and that valuation does not depend on what others think. A collector who values a painting purely for personal enjoyment is the textbook case. In the common value model, the object has the same true value to everyone, but no one knows it exactly. An offshore oil tract is worth the same to every drilling company, but each firm has only a noisy estimate of how much oil sits below. The interdependent values model sits in between: each bidder’s valuation depends partly on private taste and partly on information held by rivals.

Common value settings produce the winner’s curse. Suppose ten oil companies bid on a tract worth an unknown amount $V$. Each company’s geologist generates an unbiased estimate of $V$, but estimates vary. The company with the highest estimate wins the auction. Conditional on winning, the winner’s estimate is systematically too high. Naive bidders who do not adjust for this will overpay and earn negative profits. Empirical studies of OCS oil lease auctions in the Gulf of Mexico documented exactly this pattern in the 1970s, with winning bids often exceeding eventual revenues from the wells.

The Mathematics of Auctions

The core results of auction theory rest on a small set of clean models. Consider \(n\) risk-neutral bidders competing for a single object. Each bidder \(i\) has a private valuation \(v_i\) drawn independently from a common distribution \(F\) on \([\underline{v}, \overline{v}]\). Bidder \(i\) submits a bid \(b_i\) to maximise expected payoff.

In a Vickrey (second-price sealed-bid) auction, the dominant strategy is to bid your true valuation, \(b_i = v_i\), regardless of what others do. The proof is direct. Suppose bidder \(i\) has valuation \(v_i\) and considers bidding \(b_i\). Let \(m = \max_{j \neq i} b_j\) be the highest competing bid.

If bidder \(i\) wins, the price paid is \(m\), which does not depend on \(b_i\). Truthful bidding cannot do worse than any alternative. Suppose \(b_i < v_i\). Then the bidder loses cases where \(b_i < m < v_i\), surrendering positive payoff \(v_i – m\). Suppose \(b_i > v_i\). Then the bidder wins cases where \(v_i < m < b_i\), paying \(m > v_i\) and earning negative payoff. Bidding \(b_i = v_i\) weakly dominates every other strategy. Each bidder reveals their true value, the highest-valuation bidder wins, and the auction is efficient.

The first-price sealed-bid auction has no dominant strategy because the price paid equals the bid. With \(n\) symmetric bidders drawing values from \(F\), the symmetric Bayesian Nash equilibrium bid function is:

Bidders shade their bids below their valuations. The shading shrinks as \(n\) grows: more competition forces bids closer to true values. With \(F\) uniform on \([0,1]\) and \(n\) bidders, the equilibrium simplifies to \(b(v) = \frac{n-1}{n} v\). With two bidders, each bids half their value; with ten, each bids 90 percent.

The revenue equivalence theorem, due to Vickrey (1961) and generalised by Roger Myerson (1981), is the field’s central result. Under independent private values, risk-neutral bidders, and symmetric value distributions, every auction format that allocates the object to the highest-valuation bidder and gives the lowest type zero expected payoff produces the same expected revenue for the seller. The English, Dutch, first-price, and second-price formats all generate identical expected revenue in this benchmark world.

The intuition runs through expected payments. In a second-price auction, the winner expects to pay the expected second-highest value, \(E[v_{(2)} \mid v_i = v_{(1)}]\). In a first-price auction, each bidder shades their bid to exactly this same expected amount. The mechanism differs, but the expected revenue is the same.

Table 1 lays out the four canonical formats and their key properties.

| Format | Information Structure | Equilibrium Strategy | Price Paid by Winner | Efficient Allocation? |

|---|---|---|---|---|

| English (open ascending) | Bidders observe drop-out points | Stay until price reaches valuation | Just above second-highest value | Yes (private values) |

| Dutch (open descending) | Bidders see only the falling clock | Stop the clock at strategic price below value | Stopping price set by winner | Yes (in equilibrium) |

| First-price sealed-bid | No information about rivals’ bids | Bid below valuation: \(b(v) = v – \frac{\int_{\underline{v}}^{v} F(x)^{n-1} dx}{F(v)^{n-1}}\) | Own bid | Yes (symmetric case) |

| Second-price sealed-bid (Vickrey) | No information about rivals’ bids | Bid true valuation: \(b_i = v_i\) (dominant) | Second-highest bid | Yes |

| ||||

Table 1. Auction Formats: Equilibrium Strategies and Properties Under Independent Private Values

Notation: \(v_i\) is bidder \(i\)’s private valuation; \(b_i\) is the bid; \(F\) is the common distribution of valuations; \(n\) is the number of bidders; \(v_{(k)}\) is the \(k\)-th highest order statistic of valuations. The Dutch and first-price formats are strategically equivalent in this setting because the only information a Dutch bidder can use is the clock price, which functions like a sealed bid.

What the Theory Takes for Granted

Revenue equivalence rests on four assumptions, and each one breaks in real markets. The first is independent private values. When valuations are correlated or have a common-value component, the linkage principle of Milgrom and Weber (1982) shows that open formats like the English auction reveal information through observed drop-outs and produce higher revenue than sealed-bid formats. Open auctions let bidders update their estimates as rivals exit, reducing the winner’s curse and encouraging more aggressive bidding.

The second assumption is risk neutrality. With risk-averse bidders, the first-price auction generates higher revenue than the second-price auction. Risk aversion makes losing painful, so bidders shade less in first-price auctions. The seller benefits from the same anxiety that hurts the bidders.

The third assumption is symmetry. When bidders draw values from different distributions, allocation efficiency breaks down. Asymmetric first-price auctions can give the object to a lower-valuation bidder if a stronger bidder shades more aggressively. Spectrum auctions involve incumbents and entrants with different cost structures, and asymmetry is the rule rather than the exception.

The fourth assumption is the absence of collusion and entry barriers. Bidder rings agree to suppress competing bids and split surplus afterwards, a practice documented in stamp auctions, antiques, and some industrial procurement settings. The 2000s saw multiple cases of bid-rigging convictions in the US Treasury and municipal bond markets. Entry costs also distort outcomes: if entering an auction requires costly information acquisition, fewer bidders show up, and revenue falls below the symmetric benchmark.

Practical auctions face additional pathologies. Shill bidding, where the seller or an accomplice places fake bids to push the price up, plagued early eBay and forced the platform to ban it. Sniping, the practice of bidding seconds before close to deny rivals time to respond, breaks the theoretical equivalence between proxy bidding and second-price formats. The winner’s curse itself is not a theoretical assumption violation but a behavioural failure: bidders in common-value settings who do not adjust for adverse selection systematically lose money.

What the Lab and Field Reveal

Experimental economics has tested auction theory for forty years, and the evidence is mixed. The Vickrey auction’s truthful-bidding prediction holds only loosely in the lab. John Kagel and Dan Levin’s experiments, summarised in their book on common value auctions, found that subjects in second-price auctions often deviate from the dominant strategy, sometimes bidding above their valuations. The dominant strategy result is mathematically clean but cognitively demanding for inexperienced bidders.

First-price auctions show persistent overbidding in the lab. Hundreds of experimental sessions document bids systematically above the risk-neutral Nash equilibrium prediction. Risk aversion explains part of the gap, but not all. Spite, joy of winning, and probability misperception have all been proposed as additional drivers. The implication is uncomfortable for theory: real first-price auctions generate more revenue than the benchmark model predicts.

Field studies have produced sharper insights. Susan Athey and Jonathan Levin’s work on US Forest Service timber auctions found that the choice between sealed-bid and open ascending formats meaningfully shifts revenue and entry, with effects that depend on the timber’s species composition and bidder characteristics. Studies of eBay show that experienced bidders snipe to avoid revealing information, and the platform’s proxy bidding system produces outcomes close to a second-price auction in theory but with empirical deviations driven by bidder behaviour.

Reserve prices on eBay show a “less is more” pattern documented by Tanjim Hossain and John Morgan. Auctions with lower reserves attract more bidders, more attention, and ultimately higher final prices than auctions with higher reserves on identical items. The conventional wisdom that high reserves protect sellers is contradicted by data on real consumer auctions.

The Federal Communications Commission’s spectrum auctions are the largest natural experiment in auction design. Since 1994, the FCC has run dozens of auctions, often with tens of billions of dollars at stake. The simultaneous multiple round (SMR) auction, designed by Milgrom, Wilson, and Preston McAfee, allows bidders to express preferences over packages of licences across geographic regions. The FCC’s 2017 incentive auction simultaneously bought spectrum from television broadcasters in a reverse auction and sold it to mobile carriers in a forward auction, transferring 84 MHz of spectrum and clearing $19.8 billion in net revenue.

The chart below compares average bid-to-value ratios across the four canonical formats in a representative laboratory experiment with induced private values. The pattern is consistent across replications: first-price and Dutch auctions produce overbidding relative to the Nash equilibrium, English auctions track the dominant strategy closely, and Vickrey auctions show modest overbidding from cognitive error.

Source: Stylised representation based on Kagel and Levin (2002, 2011) and Cox, Roberson, and Smith (1982) experimental data on independent private value auctions with five bidders.

How Auction Theory Shapes the Modern Economy

Auction theory is the most successful applied branch of mechanism design. The 2020 Nobel Prize citation for Milgrom and Wilson noted that their work translated abstract game-theoretic ideas into auction formats that have raised hundreds of billions of dollars for governments and improved efficiency in resource allocation worldwide. The connection to Nash equilibrium and strategic behaviour is direct: every auction format defines a game, and equilibrium analysis predicts how rational bidders will play it.

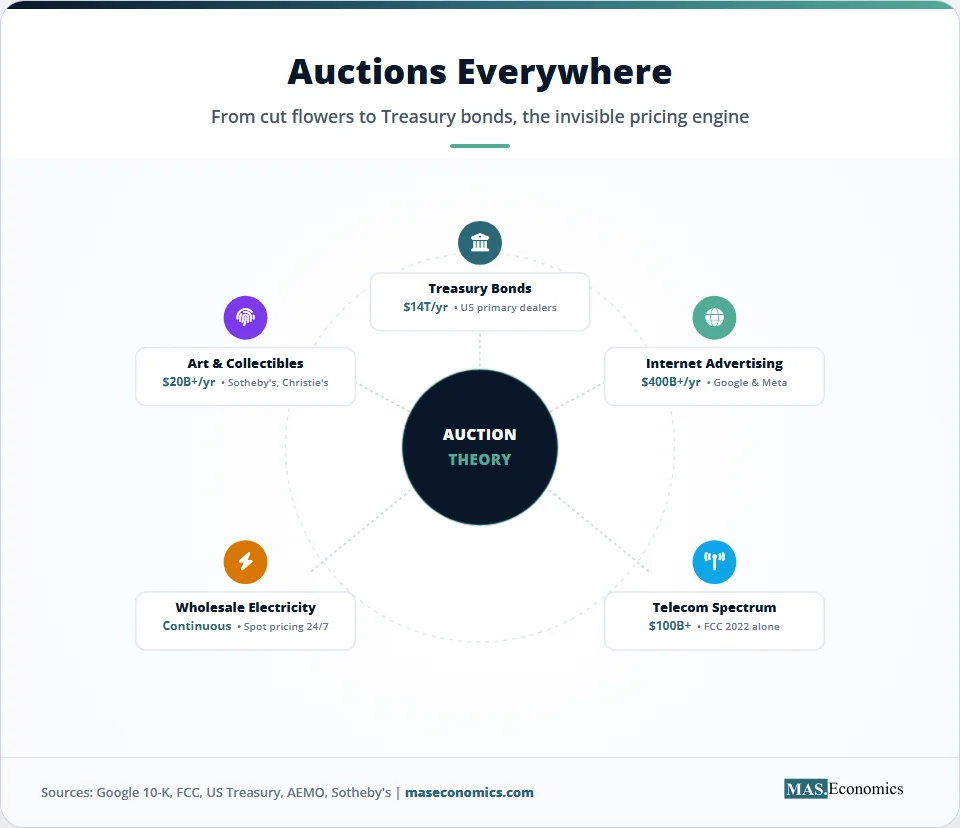

Internet advertising is the largest commercial application by volume. Google’s AdWords, launched in 2002, originally used a generalised second-price (GSP) auction designed by Hal Varian. Advertisers bid for keywords; the highest bidder gets the top slot but pays the second-highest bid plus a small increment, and so on down the page. The GSP auction is not strategy-proof in the way Vickrey’s is, but it produces stable equilibria and is easy for advertisers to understand. Google has since moved most ad surfaces to first-price auctions, partly to give advertisers cleaner attribution. Meta and Amazon run similar systems. Together, they intermediate well over $400 billion in annual ad spending through real-time auctions that complete in milliseconds.

The economics of these digital platforms rest on auction design. Search advertising auctions decide which company appears first when a consumer searches for “running shoes” or “car insurance”. Display ad exchanges auction billions of impressions daily. Programmatic advertising is auction theory at an industrial scale, and small changes in auction rules shift hundreds of millions of dollars between buyers and sellers.

Spectrum allocation is the highest-stakes public application. Before auctions, the FCC awarded radio licences through “comparative hearings” or lotteries, both of which produced corruption complaints and inefficient allocation. The 1993 budget law authorised spectrum auctions, and the SMR design has been adopted in over 80 countries. The UK’s 3G auction in 2000 raised £22.5 billion, briefly making it the largest auction in history. The German 3G auction the same year raised €50.8 billion. These numbers far exceeded ex-ante estimates and showed that well-designed auctions can extract revenue that would otherwise have gone to incumbents through softer allocation methods.

The 2017 FCC incentive auction is the most ambitious auction design ever implemented. It paid TV broadcasters to give up spectrum (reverse auction) and sold the freed spectrum to mobile carriers (forward auction), with the two sides linked by complex constraints to ensure repacking remained feasible. The auction took 13 months and required millions of lines of optimisation code. Milgrom led the design team, and the auction is the textbook case for the 2020 Nobel citation.

Government bond markets run on auctions. The US Treasury auctions roughly $14 trillion in debt every year through uniform-price (single-price) auctions, where all winning bidders pay the lowest accepted bid. Japan, Germany, and the UK use similar formats. The choice between uniform-price and discriminatory (pay-as-bid) auctions for government debt has been studied extensively, with theoretical predictions favouring uniform-price formats and empirical evidence broadly consistent.

Wholesale electricity markets in the US, UK, Australia, and Nordic countries clear through hourly or sub-hourly auctions. Generators submit supply bids, retailers and large consumers submit demand bids, and a market operator finds the price that clears each grid zone. Australia’s National Electricity Market and the UK’s Balancing Mechanism both run on multi-unit auction formats descended from the academic auction literature.

The art world’s English auctions remain economically meaningful. Sotheby’s and Christie’s together transact over $20 billion per year. The format, virtually unchanged for two centuries, is theoretically well-suited to private-value goods like paintings, where the winner’s curse is muted. Football transfer markets run informal auctions: when Paris Saint-Germain bid €222 million for Neymar in 2017, they outbid all rival clubs in a process closer to a sealed-bid first-price auction than to anything formal. The economics of sports intersect auction theory whenever broadcast rights, stadium naming rights, or player contracts go through competitive bidding.

From cut flowers in Aalsmeer to Treasury bonds in New York to clicks on a search engine, auctions price goods that conventional posted-price markets cannot handle. The theory tells designers when to choose open over sealed, when reserve prices help, and when collusion will undermine revenue. Forty years of theory and empirical work have made auction design one of economics’ most concrete contributions to public policy and private commerce.

MASEconomics Explains

4 economic concepts behind auction theory

Conclusion

Auction theory economics is the body of work that explains how bidding rules turn private valuations into prices. The four canonical formats (English, Dutch, first-price sealed-bid, and second-price sealed-bid) generate identical expected revenue under the strict assumptions of the revenue equivalence theorem, but real auctions deviate from this benchmark when bidders are risk-averse, asymmetric, collusive, or facing common-value uncertainty. Vickrey’s dominant-strategy result for second-price auctions, the linkage principle for open formats, and Myerson’s optimal auction design are the field’s three theoretical pillars.

Empirical and experimental work has shown both the power and the limits of the theory. Lab subjects systematically overbid in first-price auctions. eBay reserves work in the opposite direction than theory predicts. The 2017 FCC incentive auction transferred 84 MHz of spectrum through a design built directly on the academic literature and cleared nearly $20 billion in net revenue. Google, Meta, and Amazon spend hundreds of billions of dollars in advertising through automated auctions that run in milliseconds. The 2020 Nobel Prize to Milgrom and Wilson recognised that auction theory has moved from the blackboard to the centre of how the modern economy allocates spectrum, advertising, electricity, and government debt.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.