In a 1985 experiment by Hal Arkes and Catherine Blumer, people who had paid full price for a season ticket attended more theater performances than people who had received the same ticket at a discount. The future benefit of attending a play was the same once the ticket was bought. The difference was psychological: the higher past payment made nonattendance feel like a waste. A sunk cost is money, time, effort, or reputation already spent and no longer recoverable.

The sunk cost fallacy occurs when that irrecoverable past cost is allowed to influence a current decision. The economic rule is narrower and stricter: compare the future benefits of each option with the future costs of each option. Past costs explain how the decision point was reached, but they do not determine what should happen next.

What a Sunk Cost Is

A sunk cost is a cost that has already been incurred and cannot be recovered by any current choice. A factory lease already paid for the month, a completed advertising campaign, a nonrefundable airline ticket, and years spent developing an abandoned product can all be sunk. The common feature is not size. The common feature is irreversibility.

Economists separate sunk costs from avoidable costs because decisions happen at the margin. A marginal decision asks what changes from this point forward. If a firm has already spent $10 million building a prototype, that historical expense is not the cost of finishing the project. The cost of finishing is the additional engineering, production, marketing, legal, and financing cost still required. If those future costs exceed the future revenue the product can reasonably generate, continuation destroys value even if abandonment feels painful.

This is where sunk cost logic connects directly to opportunity cost. The relevant cost of continuing is not only the cash still to be spent. It is also the best alternative use of the same money, labor, managerial attention, and time. A failed investment does not become rational because it has absorbed resources in the past. It becomes rational only if the future payoff from staying with it beats the future payoff from switching to the next best alternative.

Richard Thaler’s 1980 paper on consumer choice helped bring such departures from standard rational choice into economics. He showed that people often evaluate decisions through mental categories rather than through one unified budget constraint. That insight matters for sunk costs because a person may treat a past payment as something that must be “used up,” even when the money cannot be recovered and the current option is unattractive.

The Fallacy in One Decision Rule

The sunk cost fallacy can be stated as a simple mistake: “Because resources have already been spent, more resources should be spent.” The conclusion does not follow from the premise. Past spending proves that an investment happened. It does not prove that more investment is justified.

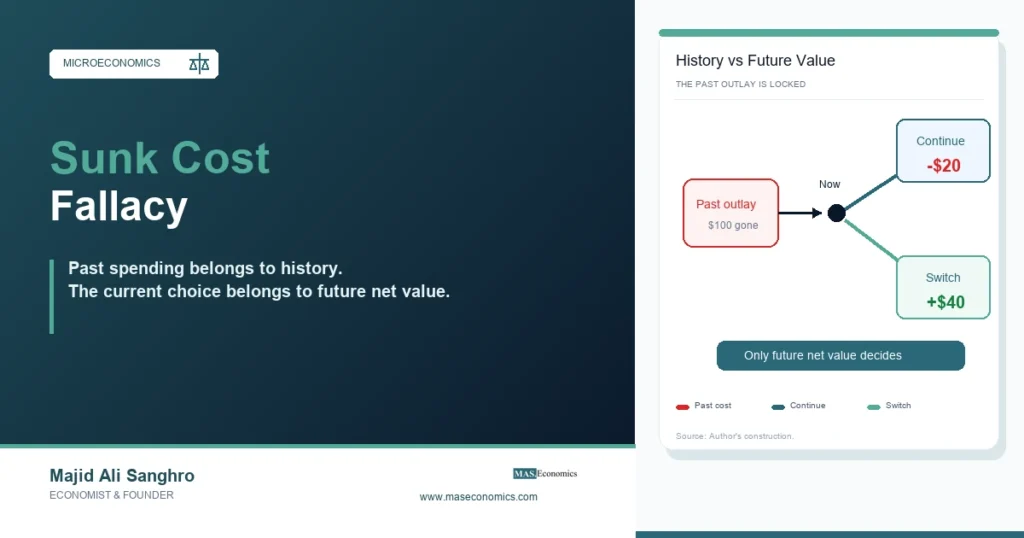

The correct rule is forward-looking. A decision-maker should continue only if the expected future benefit of continuing exceeds the expected future cost of continuing. If stopping produces a better future net outcome, stopping is the efficient choice. That remains true even when stopping forces recognition that the earlier investment failed.

The key term is future. The equation contains no term for money already spent because the decision cannot change it. A $500 nonrefundable conference fee should not decide whether a person attends if illness, travel disruption, or better work opportunities make attendance costly today. A $500 million public project already spent should not decide whether another $500 million should be spent if the remaining benefits no longer justify the remaining costs.

This logic sits close to marginal analysis. Marginal analysis does not ask whether the total project once looked attractive. It asks whether the next unit of action is worth its next unit of cost. The sunk cost fallacy replaces that margin with a backward-looking desire to make past spending feel meaningful.

Why the Mistake Persists

The sunk cost fallacy persists because human decision-making is not only arithmetic. Abandoning a project can feel like admitting error. Continuing can feel like protecting the earlier choice from judgment. Barry Staw’s 1976 study of escalating commitment showed how responsibility for an earlier decision can lead people to commit more resources to a failing course of action. The economic loss and the psychological loss become tangled.

Hal Arkes and Catherine Blumer’s classic sunk cost experiments made the mechanism especially clear. Participants behaved as if the original payment created an obligation to consume, continue, or attend. That response treats the past payment as if it can be recovered through use. Economically, it cannot. A bad movie does not become better because the ticket was expensive. A failing project does not become profitable because the first phase was costly.

Prospect theory deepens the explanation. In Prospect Theory: An Analysis of Decision under Risk, Daniel Kahneman and Amos Tversky argued that people evaluate outcomes relative to a reference point and often feel losses more sharply than gains. The prospect theory lens helps explain why a recognized loss can feel different from the same loss left embedded in an unfinished project. Continuing delays the recognition of failure, even when it raises the final cost.

The Nobel Prize committee’s 2017 press release for Richard Thaler emphasized limited rationality, mental accounting, and loss aversion as key parts of modern behavioral economics. Those concepts belong together here. Mental accounting gives the past cost its own psychological ledger. Loss aversion makes closing that ledger painful. Limited rationality makes the decision frame narrow enough that “getting value from what was paid” can crowd out the better question: what is the best use of resources now?

How Firms Misread Past Spending

Firms face sunk costs in research and development, advertising, hiring, capacity expansion, software implementation, and real estate. Some of those costs are part of normal business risk. The fallacy begins when managers defend continuation mainly because the firm has already spent too much to stop.

A product team may keep funding a weak product because the prototype is nearly finished. A retailer may hold obsolete inventory because selling at a discount would make the original buying decision look bad. A company may keep using a poor software system because the installation cost was high. These choices confuse accounting history with economic value. The original cost may matter for financial reporting, tax treatment, or managerial accountability. It does not decide whether the next dollar should be spent.

The same distinction appears in production costs. Fixed costs are not always sunk, and sunk costs are not always fixed. A factory lease may be fixed for the current month but avoidable next year. A specialized machine with no resale value may be sunk once purchased. A salaried team may be fixed in the short run but redeployable across projects. The decision depends on what can still be changed.

| Decision item | Status today | Relevant for current choice? | Reason | Decision question |

|---|---|---|---|---|

| Past development spending | Already paid | No | Cannot be recovered by continuing or stopping | What future payoff remains? |

| Additional production cost | Still avoidable | Yes | Depends on whether the project continues | Does expected revenue exceed it? |

| Managerial attention | Redeployable | Yes | Using it here prevents use elsewhere | What is the opportunity cost? |

| Reputation from canceling | Future consequence | Yes | May affect trust, contracts, or financing | How large is the future effect? |

| Embarrassment about failure | Psychological cost | Only if it affects future outcomes | Private discomfort is not project value | Would continuation create net value? |

|

|

||||

The table does not say that firms should cancel projects quickly. It says the argument for continuation must be forward-looking. Some projects look bad halfway through but still have strong expected value because most of the cost is sunk and the remaining completion cost is small. Others look respectable because total spending has been large, but the remaining work has poor expected value. The sunk cost rule cuts in both directions. It rejects both wasteful continuation and premature abandonment based on shame, fear, or fatigue.

Households Face the Same Trap

Households encounter sunk costs in memberships, subscriptions, travel plans, repair bills, education choices, and financial decisions. The pattern is familiar: a person keeps attending a class that no longer fits because tuition has been paid, keeps eating after feeling full because the meal was expensive, keeps repairing an aging car because earlier repairs were costly, or holds a losing investment because selling would make the loss visible.

The economic issue is not whether the past decision was foolish. Many sunk costs were reasonable when they were made. A gym membership may have been sensible in January. A repair may have been sensible before new information arrived. A business trip may have been worthwhile before the meeting was canceled. The fallacy appears when new information changes the future payoff but the old payment keeps controlling the choice.

This is why the idea overlaps with behavioral economics. The fully rational benchmark treats the past payment as gone. Real decision-makers often treat it as a claim on future behavior. That claim can be strengthened by social pressure: abandoning a plan may require explaining the change to family, colleagues, voters, investors, or employees. The cost that matters then is not the original payment itself, but any real future consequence of changing course.

There is also a link to satisficing and optimizing. Optimizing compares the available options carefully, but it can be costly to compute every possible future path. Satisficing uses simpler rules. “Finish what was started” is often a useful rule for discipline, learning, and credibility. It becomes dangerous when applied mechanically to options whose expected future value has turned negative.

When Sunk Costs Still Matter Indirectly

The phrase “ignore sunk costs” is sometimes misunderstood. It does not mean past decisions contain no information. Past spending may reveal commitment, technical difficulty, hidden quality problems, managerial competence, or political constraints. A failed first phase can teach something about future costs. A completed pilot can reduce uncertainty about demand. The information generated by past spending can matter, even though the spending itself is gone.

The distinction is between cost as history and information as evidence. Suppose a firm has spent $2 million testing a product and learned that customers dislike the core feature. The $2 million is sunk. The evidence from the test is not sunk; it is current information about future demand. Ignoring sunk costs does not require ignoring evidence. It requires using evidence to estimate future payoffs instead of using past spending to justify more spending.

This matters for public projects. Governments often face pressure to continue infrastructure, defense, technology, or energy projects because cancellation would expose earlier waste. Yet cancellation itself may create real future costs: contract penalties, loss of supplier capacity, legal disputes, regional employment effects, or damage to policy credibility. Those costs should be counted because they are future consequences. The past budget already spent should not be counted again.

The World Bank’s 2015 World Development Report placed decision-making, mental models, and social influences at the center of policy design. The OECD’s 2017 report on behavioral insights and public policy also documented how governments use behavioral science to improve policy. Sunk cost problems fit that broader policy lesson: better decisions often require changing the frame in which choices are evaluated.

Decision Frames That Reduce Bias

A useful sunk cost test removes the past investment from the question. Instead of asking whether a project should continue after $10 million has been spent, ask whether the same project would be started today if the remaining cost and expected future benefits were the only facts. If the answer is no, continuation needs a separate forward-looking reason.

A second test separates accountability from allocation. Accountability asks why the earlier choice was made, whether evidence was ignored, and what governance process should change. Allocation asks where resources should go now. Combining the two can make current decisions worse because the desire to avoid blame distorts the use of resources. A project can be canceled and still be audited. A past mistake can be investigated without funding a larger future mistake.

A third test uses pre-commitment. Before launching a project, decision-makers can specify exit criteria: demand thresholds, cost overrun limits, technical milestones, or external review points. These criteria do not remove judgment, but they make it harder to keep moving the goalposts after losses accumulate. The decision becomes less about saving face and more about whether the project still satisfies the conditions that justified it.

A fourth test assigns review authority to people who were not responsible for the original decision. Staw’s escalation-of-commitment logic suggests why this helps. The person who approved the first investment may have a personal stake in proving it was wise. An independent review group can still be biased, but it is less likely to treat cancellation as a personal defeat.

None of these tools makes decision-making mechanical. They simply restore the economic frame. The current choice is about future net value, not emotional recovery of the past.

MASEconomics Explains

4 economic concepts behind sunk cost decisions

These concepts are explored in depth across our educational articles library.

Explore the MASEconomics BlogConclusion

Sunk cost reasoning is one of the clearest tests of economic discipline: a past cost may explain regret, but it cannot by itself justify current spending. The relevant decision compares future benefits, future costs, and the opportunity cost of the resources still under control.

The sunk cost fallacy survives because people dislike admitting loss, managers dislike visible failure, and organizations often mix accountability with allocation. Good decision processes separate those questions. Past choices can be reviewed, audited, and learned from, while current resources are directed toward the option with the strongest expected future value.

Frequently Asked Questions

What is a sunk cost in economics?

A sunk cost is a cost that has already been incurred and cannot be recovered. Because no current choice can change it, it should not decide whether a person, firm, or government continues with an action.

What is the sunk cost fallacy?

The sunk cost fallacy is the mistake of continuing an activity because resources have already been spent on it. The rational decision is based on future benefits and future costs, not on costs that are already gone.

What is a simple sunk cost example?

A nonrefundable movie ticket is a simple sunk cost. If the movie turns out to be unpleasant, the ticket price cannot be recovered by staying, so the relevant choice is whether the remaining time would be better spent elsewhere.

Why should sunk costs be ignored?

Sunk costs should be ignored in the current allocation decision because they cannot be changed. They may matter for learning and accountability, but the current choice should depend on avoidable future costs, expected future benefits, and opportunity cost.

How is sunk cost different from opportunity cost?

A sunk cost is a past cost that cannot be recovered. Opportunity cost is forward-looking: it is the value of the best alternative use of resources still available. Sunk costs are excluded from the current choice, while opportunity costs are included.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics