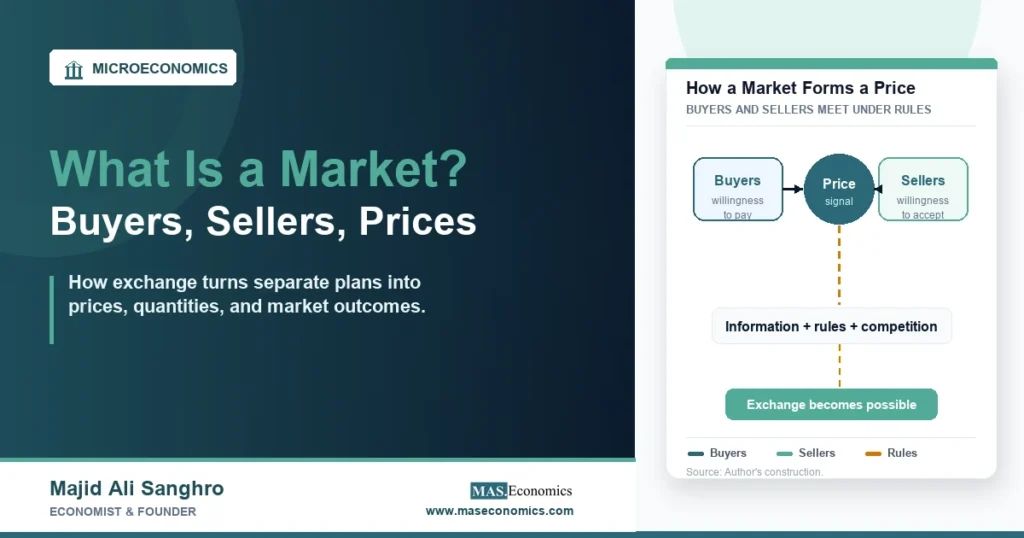

A loaf of bread, a used car, a nursing shift, a Treasury bond, and a smartphone app can all be traded in markets, even though only one of them may involve a physical stall or shop counter. what is a market is therefore not a question about a place alone. In economics, a market is an arrangement through which buyers and sellers interact, exchange information, and make trades under a set of rules.

The simplest market has three elements: buyers who want a good or service, sellers who can supply it, and some way to agree on terms. Those terms usually include price, quantity, quality, timing, delivery, and payment. A market can be local or global, physical or digital, formal or informal, highly regulated or lightly organized. What matters is the interaction that makes exchange possible.

Markets Coordinate Separate Plans

Buyers enter a market with willingness to pay. Sellers enter with willingness to accept. The buyer’s side reflects preferences, income, substitutes, urgency, expectations, and the value of alternative uses of money. The seller’s side reflects production costs, inventory, technology, competition, and the value of alternative uses of the same resources. A market brings these plans into contact.

This coordination role is why markets matter so much in economics. No single buyer needs to know every farmer’s cost of production, every shipping delay, every wage bill, and every weather shock before buying tomatoes. No single seller needs to know every household’s weekly menu. Prices compress much of that dispersed information into a signal. A higher price tells buyers to economize and sellers to supply more, while a lower price does the opposite.

The Federal Reserve education resource on self-interest and competition in a market economy frames markets around incentives, choice, and competition. That is the core economic point. Markets work by letting many separate decision-makers respond to incentives, rather than requiring one authority to assign every resource directly.

The MASEconomics article on supply and demand is the natural next layer. Demand describes how much buyers want at different prices. Supply describes how much sellers are willing to offer at different prices. A market price emerges where these two sides are brought into balance, at least for that moment and under those conditions.

Price Is the Market’s Signal

A price is more than a number on a tag. It is a signal, a rationing device, and an incentive at the same time. It signals relative scarcity. It rations goods among buyers because not everyone will buy at every price. It gives sellers an incentive to expand, shrink, enter, leave, or improve production.

Consider a simple local market for apples. If a frost reduces the crop, fewer apples are available at each price. Sellers will not be willing to sell the same quantity as before unless the price rises. The higher price does two things at once: it encourages sellers with available apples to bring more to market, and it encourages buyers to reduce waste, switch to substitutes, or buy less. No one needs to issue a central instruction. The price carries the pressure created by scarcity.

The same logic appears in financial markets. The SEC’s Investor.gov page on how stock markets work describes an organized setting where investors, brokers, exchanges, public companies, and order types interact under rules. The traded object is different from apples, but the market function is familiar: buyers and sellers submit orders, information is processed, and trades occur when terms match.

Prices also connect to opportunity cost. A buyer who spends $40 on one good gives up the next best use of that $40. A seller who supplies one customer gives up alternative uses of the same inventory, labor, time, and capital. Market prices help both sides compare alternatives.

Markets Need Rules

A market is never just spontaneous trade. It also needs rules. Those rules may be explicit laws, exchange rules, platform terms, religious norms, local customs, professional standards, licensing requirements, or informal reputation systems. They define what can be sold, who can participate, how quality is verified, how disputes are handled, and what counts as fraud.

This is easiest to see in markets for financial assets, medicine, food, housing, labor, and electricity. In each case, a simple buyer-seller story is not enough. Securities markets need disclosure rules, trading rules, settlement systems, and enforcement. Food markets need safety rules. Labor markets need contract and employment law. Housing markets need property rights, zoning, lending rules, and title systems.

The Federal Trade Commission’s guide to antitrust laws states that antitrust policy aims to protect the process of competition for consumers, including incentives for firms to operate efficiently, keep prices down, and keep quality up. That matters because market exchange does not automatically guarantee competition. Sellers can collude, merge, exclude rivals, mislead buyers, or exploit information gaps.

The 2023 Merger Guidelines from the US Department of Justice and Federal Trade Commission show how regulators assess whether mergers may reduce competition. This is not an argument against markets. It is an argument that markets have structure, and structure shapes outcomes. A market with many active sellers behaves differently from a market dominated by one firm.

| Building block | Economic role | Failure if weak |

|---|---|---|

| Buyers | Create demand through willingness and ability to pay | Too little demand, thin trading, weak price discovery |

| Sellers | Create supply through production, inventory, or ownership | Shortages, monopoly power, unreliable availability |

| Information | Lets both sides judge price, quality, risk, and alternatives | Fraud, lemons problems, poor matching |

| Rules | Define legal exchange, property rights, settlement, and enforcement | Disputes, nonpayment, unsafe goods, weak trust |

| Competition | Pressures sellers and buyers to offer better terms | Market power, high markups, low quality, exclusion |

|

|

||

The table highlights a point often missed in beginner definitions. A market is not only a crowd. A crowded bazaar can work badly if goods are fake, payments fail, contracts are unenforceable, or buyers cannot compare quality. A digital platform can work well with no physical crowd if search, reputation, payment, delivery, and dispute systems are reliable.

Many Markets Are Not Places

Some markets are physical places: a wholesale fish market, a street market, a livestock auction, or a farmers market. Others are networks: the foreign exchange market, the labor market, the market for used cars, the market for electricity, or the market for bank loans. The word market describes the exchange system, not necessarily a location.

This is why economists are careful about market boundaries. A market has to be defined by the good or service, the relevant buyers and sellers, the geographic area, the time period, and the available substitutes. The market for coffee in one neighborhood at 8 a.m. is not identical to the world coffee market, even though the two are connected. A price in one market can transmit pressure to another only when buyers, sellers, goods, or information can move between them.

Labor markets show why this matters. Workers are not goods, but their time and services are exchanged under contracts. Wages emerge from demand for labor, supply of labor, bargaining power, skill, institutions, regulation, and local conditions. The MASEconomics article on jobs reports and labor markets explains why employment data must be read through definitions, participation, wages, and hours rather than a single headline.

Financial markets also differ from ordinary goods markets. Stocks and bonds are claims on future cash flows, so information, expectations, liquidity, and regulation matter heavily. The MASEconomics article on the efficient market hypothesis explains one formal view of how asset prices may incorporate information. That does not make financial markets perfect. It shows how quickly information can matter when many traders compete over future value.

Digital markets add another layer. A platform may match drivers and riders, hosts and travelers, sellers and buyers, advertisers and users, or workers and tasks. In such markets, the platform often sets rules, ranks search results, processes payment, collects data, and sometimes competes with sellers on its own platform. The market is no longer only a meeting point. It is designed infrastructure.

Competition Shapes Market Outcomes

Market outcomes depend on competition. In a competitive market, many buyers and sellers make it difficult for one participant to control the price. If one seller charges too much for an identical product, buyers can switch. If one buyer offers too little, sellers can look elsewhere. Competition narrows the gap between price and cost, although it does not eliminate profit, risk, or differences in quality.

In less competitive markets, price formation changes. A monopoly may restrict quantity to raise price. An oligopoly may involve strategic interaction among a few firms. A platform may control access to buyers. A labor market may have one dominant employer in a local area. The MASEconomics article on market structures explains these differences in more detail.

Competition also affects incentives beyond price. Firms may compete through quality, delivery speed, product variety, warranties, reputation, privacy protection, return policies, or after-sale service. Buyers may compete through willingness to pay, timing, search effort, creditworthiness, or location. A market is therefore not only a price machine. It is a sorting system that allocates goods, services, risks, and attention.

The link with price determination is direct. The same demand curve can produce different prices depending on whether sellers are competitive, monopolistic, oligopolistic, or regulated. A market definition must therefore include the number of participants, entry conditions, product differentiation, information, and rules.

Information Can Break Exchange

Markets rely on information. Buyers need to know what they are buying. Sellers need to know whether buyers can pay. Both sides need some confidence that contracts will be honored. When information is missing or uneven, exchange can shrink or become distorted.

The classic example is the used-car market in George Akerlof’s model of lemons. If sellers know car quality and buyers cannot distinguish good cars from bad cars, buyers may offer only an average price. Owners of good cars may then exit the market, leaving more low-quality cars behind. The MASEconomics article on the Akerlof model explains how asymmetric information can reduce trade even when gains from trade exist.

Information problems appear in insurance, credit, healthcare, used goods, professional services, online platforms, and financial products. Markets respond with warranties, licensing, audits, reviews, collateral, disclosure rules, brand reputation, certification, and regulation. These devices are not outside the market. They are often what make the market possible.

The MASEconomics article on missing markets shows the extreme case: some valuable things are not traded at all because property rights, information, enforcement, or payment mechanisms are absent. Clean air, biodiversity, unpaid care, and some forms of risk are difficult to price through ordinary exchange. A market can allocate only what its institutions allow people to trade.

Markets Can Fail

A market works well when prices reflect relevant costs and benefits, competition disciplines participants, information is usable, and property rights are clear. When those conditions fail, market outcomes can be inefficient or unfair. The existence of a price does not prove that the price reflects full social value.

Externalities are a common failure. If a factory sells output at a price that excludes pollution damage, the market price is too low from society’s point of view. Public goods create another problem because nonpayers may still benefit, making private supply too low. Market power can keep price above competitive levels. Information asymmetry can cause bad products, bad loans, or bad contracts to crowd out better ones.

The MASEconomics article on market failure and externalities covers the logic directly. The point for a beginner article is simpler: markets are powerful coordination devices, not magic devices. Their performance depends on the conditions under which buyers and sellers interact.

Policy can improve markets when it strengthens competition, clarifies property rights, improves information, corrects externalities, or supplies public goods. Policy can also damage markets when it blocks entry, freezes prices without addressing scarcity, creates perverse incentives, or protects favored firms. The question is not markets or policy in the abstract. The question is which rule system makes exchange work better for the problem at hand.

MASEconomics Explains

4 economic concepts behind markets

These concepts are explored in depth across our educational articles library.

Explore the MASEconomics BlogConclusion

What is a market is best answered by looking at interaction, not location. A market is a rule-based arrangement where buyers and sellers meet directly or indirectly, compare terms, exchange information, and make trades.

Markets coordinate separate plans through prices, but their results depend on competition, information, property rights, enforcement, and institutional design. A good market makes exchange easier and prices more informative. A weak market can produce monopoly power, fraud, missing trade, external costs, or unstable outcomes. The economic task is to understand which market conditions are present before judging what the price means.

Frequently Asked Questions

What is a market in economics?

A market is an arrangement where buyers and sellers interact to trade goods, services, labor, assets, or rights. It does not have to be a physical place. It can be a platform, exchange, auction, network, or set of recurring transactions.

How do prices emerge in a market?

Prices emerge when buyer willingness to pay meets seller willingness to accept under market rules. Demand, supply, information, competition, costs, and expectations all affect the final price.

Does a market have to be physical?

No. A market can be physical, digital, or institutional. A street market, stock exchange, labor market, online platform, and foreign exchange market are all markets because they connect buyers and sellers.

What makes a market competitive?

A market is more competitive when many buyers and sellers can participate, information is usable, entry barriers are low, and no single participant can control price or access. Competition can occur through price, quality, service, location, reputation, or product variety.

Why do markets fail?

Markets can fail when prices do not reflect full costs and benefits, when firms have market power, when information is uneven, or when goods are difficult to exclude people from using. Externalities, public goods, monopolies, and asymmetric information are common causes.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics