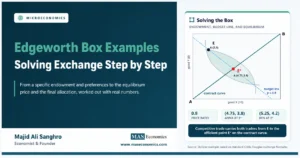

In a two-person, two-good exchange economy, every point inside an Edgeworth box is feasible, but only a narrow set of points leaves no unrealized gains from trade. That set is the contract curve: the locus of Pareto-efficient allocations where the two agents’ indifference curves are tangent, so their marginal rates of substitution are equal.

The idea sits at the center of exchange theory because it turns a geometric diagram into a welfare result. The Edgeworth Box shows all feasible allocations. The contract curve separates allocations where mutually beneficial exchange remains possible from allocations where no further Pareto improvement exists.

Where Feasible Trade Becomes Efficient

Start with an exchange economy containing two agents, A and B, and two goods, \(x\) and \(y\). Total quantities are fixed at \(\bar{x}\) and \(\bar{y}\). Agent A’s consumption bundle is \((x_A,y_A)\), while agent B receives the residual bundle:

The Edgeworth box plots A’s consumption from the lower-left origin and B’s consumption from the upper-right origin. Every point inside the box exhausts the available quantities of both goods, so feasibility is built into the diagram. What changes from point to point is not total resources, but their distribution between the two agents.

Each agent has an indifference map. A’s indifference curves slope downward from A’s origin. B’s indifference curves also slope downward from B’s perspective, but because B’s origin is reversed in the box, they appear mirrored against A’s map. Where the two curves cross, there is normally room for exchange. Where they are tangent, the local willingness to trade is the same for both agents.

In standard intermediate microeconomics, this tangency condition is written as equality of marginal rates of substitution. Hal Varian’s exchange chapter presents the Edgeworth box as the natural diagram for feasible allocations, Pareto improvements, and exchange equilibrium in a two-person economy Varian, Intermediate Microeconomics. The same logic appears in open teaching materials from Oregon State University’s intermediate microeconomics text and in the EconGraphs treatment of Pareto efficiency and the contract curve.

The Tangency Condition Does the Work

At any interior Pareto-efficient allocation, the slope of A’s indifference curve must equal the slope of B’s indifference curve. If the slopes differ, the agents value the marginal trade-off between \(x\) and \(y\) differently. That difference creates a trading interval: one agent is willing to give up a good at a rate the other agent is willing to accept.

Let \(U_A(x_A,y_A)\) and \(U_B(x_B,y_B)\) represent the utility functions. The marginal rate of substitution for each agent is:

The interior contract-curve condition is therefore:

This equation is not a bargaining rule. It does not say which efficient point will be chosen. It says only that any interior allocation that fails the equality condition cannot be Pareto efficient. If \(MRS_A>MRS_B\), agent A values good \(x\) more highly relative to good \(y\) than B does. A mutually beneficial exchange can move \(x\) toward A and \(y\) toward B. If \(MRS_A<MRS_B\), the direction reverses.

The equality condition connects the contract curve to welfare economics and Pareto efficiency. A Pareto improvement means at least one agent becomes better off without making the other worse off. At a contract-curve point, such a movement is no longer available inside the feasible set.

From Endowment to Trading Lens

The initial endowment matters because it determines which efficient allocations are reachable through voluntary trade. Suppose the economy begins at point \(E\). Through \(E\), draw one indifference curve for A and one for B. The lens-shaped region between the two curves contains allocations that both weakly prefer to \(E\), with at least one agent strictly better off.

Movement inside that lens is a Pareto improvement relative to the endowment. Movement outside it hurts at least one agent compared with the starting point. The contract curve may run across the entire Edgeworth box, but only the segment inside the voluntary-trade lens is relevant when initial ownership must be respected.

This distinction matters for general equilibrium analysis. A planner could select any Pareto-efficient point on the full curve if redistribution were unrestricted. Voluntary exchange from a given endowment can normally reach only the part that both agents accept. Princeton lecture notes by Avinash Dixit make the same distinction between the full efficient locus and the segment relevant after the initial endowment is imposed Dixit, General Equilibrium and Pareto Efficiency.

Deriving the Curve Algebraically

The contract curve can be derived by solving the tangency equation together with feasibility. A common classroom case uses Cobb-Douglas utility functions:

For A, the marginal rate of substitution is:

For B, because B consumes the residual quantities:

Setting the two expressions equal gives the contract-curve equation:

This equation describes all interior allocations where the two indifference curves are tangent. If \(\alpha=\beta\), both agents have the same relative preference weights. In a rectangular box with identical Cobb-Douglas weights, the contract curve becomes the diagonal connecting the two origins. If \(\alpha\neq\beta\), the curve bends toward the agent who values one good more strongly.

The algebra shows why the contract curve is not merely a drawn line. It is the solution set of a welfare problem: maximize one agent’s utility subject to feasibility and a promised utility level for the other agent. UCLA notes on Pareto efficiency present this interior condition as equality of marginal rates of substitution at efficient allocations UCLA, Pareto Efficiency and Edgeworth Box.

Why Crossing Curves Signal Waste

When two indifference curves cross inside the Edgeworth box, they reveal different marginal valuations. At that crossing, the agents do not agree about the local rate at which \(x\) should trade for \(y\). That disagreement is not a conflict by itself. It is a source of gains from exchange.

Suppose A is willing to give up 2 units of \(y\) for 1 unit of \(x\), while B is willing to accept 1 unit of \(y\) for giving up 1 unit of \(x\). Any exchange rate between 1 and 2 units of \(y\) per unit of \(x\) can make both agents better off. The allocation is therefore not efficient.

At tangency, this interval disappears. The two agents place the same marginal value on the last unit traded. A small movement along any feasible direction helps one agent only by hurting the other. This is the geometric meaning of Pareto efficiency.

The same logic underlies indifference-curve analysis in individual choice and marginal analysis through differentiation. The contract curve extends those tools from one consumer-facing price to two consumers trading with each other.

When the Simple Formula Breaks

The equality \(MRS_A=MRS_B\) is the clean interior condition, but it relies on well-behaved preferences and interior allocations. If preferences are convex, continuous, and locally nonsatiated, tangency is the standard characterization. The site’s article on monotonicity, convexity, and differentiability gives the preference assumptions behind this result.

Corner solutions require more care. If one agent consumes none of a good, the marginal rate of substitution may not be defined in the usual way. With perfect substitutes, efficient allocations can occur along borders rather than smooth tangencies. With nonconvex preferences, the efficient set can be disconnected or kinked. EconGraphs notes this point directly: when preferences are not well behaved, Pareto-efficient allocations may not be characterized by smooth tangency. EconGraphs, Pareto Efficiency and Contract Curve.

The contract curve also does not choose a distribution. One point may give most resources to A. Another may give most resources to B. Both can be Pareto efficient. Efficiency says that no mutually beneficial rearrangement remains. It does not say that the allocation is fair, politically acceptable, or produced by equal bargaining power.

Markets Select a Point

A competitive equilibrium can be represented inside the Edgeworth box by a budget line passing through the initial endowment. Prices determine the line’s slope. Each agent chooses the best affordable bundle on that line. When both agents choose the same feasible allocation, markets clear.

Under standard assumptions, such a Walrasian equilibrium lies on the contract curve. The reason is direct: if markets clear and both agents maximize utility at the same price ratio, each agent’s marginal rate of substitution equals the same price ratio. Hence, the two marginal rates of substitution are equal to each other.

This result links the contract curve to the first welfare theorem: competitive equilibrium allocations are Pareto efficient under the usual assumptions. It also explains why the contract curve is more than a geometry exercise. It is the bridge between individual optimization, relative prices, and welfare evaluation. The same optimization structure appears in the MASEconomics discussion of constrained optimization and Lagrange methods.

What the Curve Does Not Say

The contract curve identifies efficiency, not justice. It cannot rank two efficient points unless a social welfare function or distributional criterion is added. An allocation near A’s origin may leave A with very little. It can still be Pareto efficient if improving A requires reducing B’s utility.

This is why the contract curve should be read alongside welfare economics rather than as a full social evaluation. Pareto efficiency is a weak criterion. It rules out obvious waste but remains silent about unequal endowments, bargaining power, and interpersonal comparisons of utility.

It also abstracts from production, externalities, uncertainty, and institutions. In a richer economy, goods are produced, property rights are enforced, contracts are incomplete, and information may be asymmetric. The two-person exchange box isolates one important mechanism: once resources are fixed and preferences are known, efficiency requires equal marginal trade-offs.

MASEconomics Explains

3 economic concepts behind the contract curve

These concepts are explored in depth across our educational articles library.

Explore the MASEconomics BlogConclusion

Contract curve analysis shows that Pareto-efficient exchange allocations are found where two agents’ indifference curves are tangent inside the Edgeworth box. The formal condition \(MRS_A=MRS_B\) identifies the points where no further mutually beneficial trade remains. The curve, therefore, gives a compact bridge from feasible allocation to marginal valuation to welfare efficiency. It does not determine fairness or bargaining outcomes, but it does identify the boundary beyond which exchange cannot create another Pareto improvement.

Frequently Asked Questions

What is the contract curve in economics?

The contract curve is the set of Pareto-efficient allocations in an Edgeworth box. At interior points on the curve, the two agents’ indifference curves are tangent and their marginal rates of substitution are equal.

How is the contract curve derived?

The contract curve is derived by setting the two agents’ marginal rates of substitution equal and imposing feasibility. With two goods, feasibility means one agent’s allocation determines the other agent’s residual allocation.

Why is the contract curve Pareto efficient?

It is Pareto efficient because no feasible movement from a point on the curve can make one agent better off without making the other worse off. Away from the curve, different marginal rates of substitution normally leave room for mutually beneficial exchange.

Is every point on the contract curve fair?

No. Pareto efficiency does not imply fairness. A point can be efficient even if one agent receives much more than the other, because improving the worse-off agent may require reducing the better-off agent’s utility.

How is the contract curve related to the Edgeworth box?

The Edgeworth box shows all feasible allocations of two goods between two agents. The contract curve is the subset of those feasible allocations where the agents’ indifference curves are tangent or where no Pareto improvement remains.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics