The IMF Spring Meetings 2026, held April 13 – 18 at the Fund’s headquarters in Washington, D.C., convened the world’s finance ministers, central bank governors, and heads of international institutions at a moment of acute global economic stress. The Strait of Hormuz remained largely blocked. OPEC production had collapsed 27% in a single month. Peace talks in Islamabad had ended without a deal. And the tariff war continued to reshape global trade flows.

We have reviewed the official IMFC statements from 12 major delegations and institutions: Saudi Arabia, the United States, China, Japan, France, Canada, Turkiye, the European Central Bank, the European Commission, the OECD, OPEC, and the United Nations, plus the G-24 communique. These documents, submitted to the 53rd Meeting of the International Monetary and Financial Committee, reveal five warnings that define the global economic outlook for the remainder of 2026.

The following analysis distils what these officials said, what they meant, and what it means for the global economy.

Warning 1: Saudi Arabia Invokes the 1970s

The most striking statement came from Saudi Central Bank Governor Ayman Al-Sayari, who drew an explicit comparison between the current crisis and the stagflation of the 1970s. The war in the Middle East, he said, carries “potential for the global economy to experience conditions similar to those of the stagflation episode in the 1970s.” The resulting negative supply shock, he warned, “is likely to have implications that surpass those experienced during the post-pandemic energy shock.”

This is not a casual comparison. The 1970s stagflation combined rising oil prices, slowing growth, and persistent inflation in a combination that defied conventional monetary policy. Central banks could not cut rates to stimulate growth without fuelling inflation further, and could not raise rates to fight inflation without deepening the recession. The result was a decade of economic misery across the industrialised world.

Al-Sayari’s warning was grounded in a specific observation: the spillovers from the current crisis extend “beyond crude oil and LNG to refined products, fertilisers, and other critical inputs, with implications for transport costs, food security, industrial production, and price stability.” In other words, this is not merely an oil shock. It is a supply chain shock that is propagating through the entire global production system.

Saudi Arabia also used its statement to highlight its own strategic foresight. The Kingdom’s East-West Pipeline, built in the 1980s after fears that the Iran-Iraq “tanker war” would close the Strait, “has proven to be a lifeline, not just for Saudi exports, but also for global energy supply.” This pipeline, which can carry up to 7 million barrels per day to the Red Sea port of Yanbu, is now the primary mechanism through which Saudi oil reaches global markets. As our analysis of the Strait of Hormuz crisis documented, Saudi Arabia’s production fell 23% in March, the least among Gulf producers precisely because of this bypass infrastructure.

Warning 2: Growth Is Falling, Inflation Is Rising

The OECD’s statement to the IMFC provided the most detailed quantitative assessment of the damage. Secretary-General Mathias Cormann reported that global GDP growth is now projected at 2.9% in 2026, down 0.3 percentage points from the pre-war forecast. G20 headline inflation has been revised sharply upward to 4.0%, a 1.2 percentage-point increase from December 2025’s projection.

The OECD’s adverse scenario is more alarming still: if oil and gas prices remain 26% and 17% above baseline, respectively, and global financial conditions tighten further, global GDP would fall by an additional 0.5% and consumer prices would rise by a further 0.9%.

Table 1: IMF Spring Meetings 2026 – Key Economic Forecasts from Official Statements

| Economy | 2025 Growth | 2026 Forecast | 2027 Forecast | Source |

|---|---|---|---|---|

| Global | 3.3% | 2.9% | 3.0% | OECD |

| United States | 2.1% | 2.0% | 1.7% | OECD |

| Euro Area | 1.4% | 0.8 – 0.9% | 1.2 – 1.3% | OECD / ECB |

| China | 5.0% | 4.4 – 4.5% | 4.3 – 4.5% | OECD / OPEC / China |

| Japan | 1.2% | 0.9% | 0.9% | OECD |

| United Kingdom | 1.3% | 0.7% | 1.3% | OECD |

| India (fiscal year) | 7.6% | 6.1% | 6.4% | OECD |

| G20 Inflation | 3.4% | 4.0% | 2.7% | OECD |

|

||||

Sources: OECD Interim Economic Outlook (March 26, 2026), ECB staff projections (March 2026), OPEC IMFC statement (April 2026), People’s Bank of China IMFC statement (April 2026).

The ECB’s statement, delivered by President Christine Lagarde, revealed the complexity of the policy challenge for Europe. Euro area headline inflation rose to 2.6% in March, up from 1.9% in February, driven by energy prices. The Governing Council kept interest rates unchanged in March, caught between rising inflation (which argues for higher rates) and weakening growth (which argues for lower rates). Under the ECB’s “severe scenario,” in which energy disruption continues through late 2026, euro area growth would be “significantly reduced” this year and next. This is the stagflation trap that Saudi Arabia warned about: a central bank unable to move in either direction without making one problem worse.

Warning 3: China’s Economy Is Growing. Everyone Else’s Is Slowing.

People’s Bank of China Governor Pan Gongsheng delivered a statement that read like a parallel universe compared to the Western delegations. China’s GDP grew 5.0% in 2025, “fully achieving the major targets.” Q1 2026 growth came in at 5.0% year-on-year, up from 4.5% in Q4 2025. Retail sales rose 2.4%. Fixed asset investment returned to positive territory. Manufacturing and services PMIs both returned to expansionary territory above 50. Corporate profits surged 15.2% in the first two months of the year.

Pan’s statement carried three strategic messages. First, China is presenting itself as a global stabiliser: “China’s overall economic performance has remained stable with progress, demonstrating strong resilience. This has also provided stable support for the world economy and expanded opportunities for cooperation.” Second, China positioned itself against protectionism: “All countries should practice true multilateralism, firmly safeguard free trade, and build an open world economy.” Third, China called for IMF reform to increase the representation of emerging and developing countries, urging “quota share realignment as early as possible.”

The contrast with the US statement could not be sharper. While US Treasury Secretary Bessent called for the IMF to “drop extraneous items” and return to basics, China called for the Fund to “take a clear stand against protectionism and defend multilateralism.” These competing visions of the IMF’s purpose, articulated at the same meeting by the world’s two largest economies, define the institutional battle that will shape global economic governance for years to come.

China’s fiscal policy for 2026 is aggressively expansionary: the deficit target is set at approximately 4% of GDP, national general public expenditure will reach RMB 30 trillion for the first time, and the government will issue RMB 1.3 trillion in ultra-long special government bonds. Monetary policy remains “appropriately accommodative,” with the PBOC injecting approximately RMB 2 trillion in medium- and long-term funds through open market operations since January. This coordinated fiscal-monetary expansion stands in contrast to the constrained policy space available to most Western economies, where elevated debt levels and above-target inflation limit the scope for stimulus.

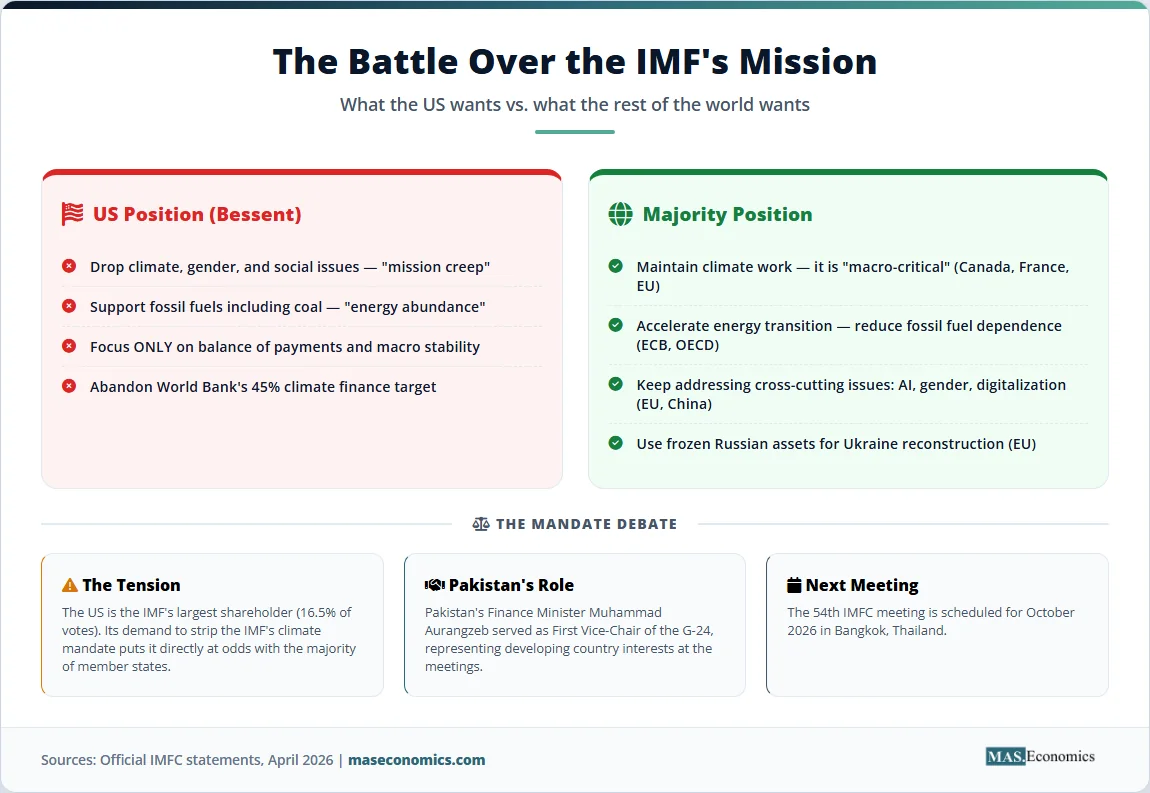

Warning 4: The US and the Rest of the World Disagree on What the IMF Should Do

The most politically charged statement came from US Treasury Secretary Scott Bessent. His message was blunt: “In recent years, the IMF has suffered from mission creep. Its work has too often extended into areas such as international development, climate change, gender, and social issues, which are disconnected from the institution’s core mandate. To restore its relevance and impact, the Fund must drop these extraneous items.”

Bessent went further, calling on the World Bank to “abandon its distortionary 45% climate finance target” and to “support an all-of-the-above approach to energy technologies, including fossil fuels such as gas, oil, and coal, rather than restrict borrower choice.” He described the climate target as breeding “inefficiency” and “distorting economic decision making.”

This position was directly contradicted by nearly every other major delegation. Canada’s Finance Minister Champagne stated that his constituency “remains supportive of the IMF’s efforts to adequately fund, sustain, and mainstream work on macro-critical issues, such as climate and gender.” France’s Minister Lescure “encourages the IMF to maintain a high level of ambition” on climate and “further develop its existing toolkit.” The ECB’s Lagarde called for “reducing the share of the EU’s energy that is imported and accelerating the energy transition.” The European Commission’s Dombrovskis described the US-demanded abandonment of the climate target as something to be resisted.

The OECD took a measured but clear position: “Policies that lower reliance on imported fossil fuels help reduce exposure to supply shocks,” a direct rebuttal of the US position that fossil fuels should be promoted rather than reduced.

This is not an abstract policy debate. The United States holds 16.5% of IMF voting power, giving it an effective veto on major decisions. If Washington insists on stripping climate from the Fund’s mandate, it can block funding, delay reforms, and reshape institutional priorities. The fact that virtually every other major member state opposes this position creates a governance crisis that will play out over the coming months.

Warning 5: The Poorest Countries Are Running Out of Options

UN Secretary-General Antonio Guterres’s statement carried the most urgent language of any submission. “The consequences are already visible in the daily lives of people struggling with rising food and energy costs from the Philippines to Sri Lanka to Mozambique,” he quoted himself as saying on April 2. “It is high time to stop the war that is inflicting immense human suffering and already triggering devastating economic consequences.”

The UN’s core message was that developing countries face a fundamentally different crisis from advanced economies. They cannot deploy the fiscal cushioning measures that wealthier nations use to protect households from rising energy and food costs. Many are already in or at high risk of debt distress. Their currencies are weakening, pushing up the local-currency cost of external debt service and imports. And aid budgets are shrinking precisely when they are needed most.

The G-24 communique, chaired by Nigeria’s Finance Minister Olawale Edun with Pakistan’s Finance Minister Muhammad Aurangzeb as First Vice-Chair, reinforced this message. It noted that “traditional approaches such as contracting domestic demand or allowing currency depreciation may prove insufficient for absorbing the shocks.” It called for regular issuance of Special Drawing Rights (SDRs) to support all emerging market and developing economies, and urged the IMF to explore gold sales to bolster its lending capacity.

Japan’s statement, delivered by Finance Minister Katayama, announced a concrete response: the “POWERR Asia” initiative, providing approximately $10 billion in financial support for Asian economies to procure oil and essential materials, strengthen supply chains, and enhance energy supply capacity. This initiative reflects the specific vulnerability of Asia, where economies depend heavily on oil and LNG imports from the Middle East through the Strait of Hormuz.

Turkiye’s Finance Minister Simşek raised an issue largely absent from other statements: the macroeconomic impact of refugees and forced displacement. “Protracted refugee movements, often triggered by conflict, can impose persistent fiscal, social, and macroeconomic pressures on host and transition countries,” he noted. Turkiye hosts millions of refugees from Syria and faces potential new displacement from the Iran war, creating fiscal pressures that compound the energy shock.

OPEC’s Own Numbers Tell the Story

OPEC Secretary General Haitham Al Ghais’s statement provided the most detailed oil market data presented at the meetings. World oil demand in 2026 is forecast to increase by 1.4 million barrels per day to average 106.5 million bpd. Non-OECD Asia, led by China and India, will drive the growth. Global exploration and production capital expenditure is expected to fall 3% to $390 billion, well below the $604 billion peak in 2014.

The chart below shows the OECD’s growth forecast revisions for 2026, illustrating how the Iran war has reshaped the economic outlook presented at the IMF Spring Meetings 2026.

Source: OECD Interim Economic Outlook (March 26, 2026). Comparison of December 2025 forecasts vs. March 2026 forecasts, showing the impact of the Middle East conflict on growth projections.

OPEC’s statement notably avoided mentioning the Iran war directly, referring instead to “current geopolitical dynamics” that “require close monitoring.” It did not address the 27% production collapse in March or the infrastructure damage to member states. The statement instead emphasised that the organisation “remains committed to supporting oil market stability for the benefit of both consuming and producing nations.” The gap between OPEC’s diplomatic language and the reality documented in its own monthly report, which MASEconomics analysed in our OPEC article, is itself revealing.

The Institutional Reform: Diriyah Guiding Principles

Beyond the immediate crisis, the IMF Spring Meetings 2026 produced a significant institutional milestone: the agreement on the Diriyah Guiding Principles for IMF Quota and Governance Reforms. Named after the historic Saudi Arabian site where the principles were developed, the framework represents the first governance reform consensus in nearly two decades.

The principles address a long-standing imbalance: the IMF’s voting structure does not reflect the current global economy. China’s voting share remains far below its share of global GDP. Emerging markets collectively are underrepresented despite generating the majority of global growth. The Diriyah Principles provide a roadmap for the 17th General Review of Quotas, which will determine how voting power is redistributed.

Every major delegation welcomed the Diriyah Principles in their statements. Saudi Arabia called them “a historic milestone.” China urged “quota share realignment as early as possible to reflect the relative weights of its members in the global economy.” Japan, in a particularly detailed argument, proposed that voluntary financial contributions (VFCs) to IMF trust funds should be considered in quota adjustments, a position that would benefit donor countries like Japan. France supported “a limited quota realignment in favour of the most underrepresented countries” while insisting that “higher quota shares should be accompanied by greater responsibility.”

The US statement, notably, conditioned its support on the principle that “IMF shareholding should reflect members’ relative position in the world economy, and any future quota realignment must be underpinned by a new quota formula.” This sets the stage for a complex negotiation in which the US will seek to maintain its veto power while acknowledging the need for greater representation of emerging economies. The next chapter of this debate will unfold at the 54th IMFC meeting, scheduled for October 2026 in Bangkok, Thailand.

One Point of Agreement: Energy Security Is Now Macro-Critical

If there was a single point of consensus across all 12 statements, it was the recognition that energy security has become inseparable from macroeconomic stability. Saudi Arabia stated it directly: “Energy security should be treated as integral to macroeconomic and financial stability.” The OECD noted that “Persian Gulf states account for 34% of the world’s urea exports” and “over one-third of the global supply of helium,” demonstrating that the disruption extends far beyond oil. Japan announced $10 billion for Asian energy security. The ECB called for “reducing the EU’s dependence on fossil fuels.”

The specifics of how to achieve energy security, however, revealed deep divisions. The US called for more fossil fuel production, including coal. The EU and OECD called for accelerating the energy transition away from fossil fuels. Saudi Arabia emphasised the “continued role of fossil fuels in sustaining global growth.” China highlighted its own energy diversification while expanding domestic consumption.

Table 2: How Major Delegations Framed Energy Security at the IMF Spring Meetings 2026

| Delegation | Energy Security Position | Fossil Fuel Stance |

|---|---|---|

| United States | “Energy abundance sparks economic abundance” | Support all technologies “including gas, oil, and coal” |

| Saudi Arabia | “Energy security derives from managing risks proactively” | “Avoid conclusions that understate the continued role of fossil fuels” |

| ECB | “Reduce the share of the EU’s energy that is imported” | “Accelerate the energy transition” |

| OECD | “Expand domestic energy production from renewables” | “Lower reliance on imported fossil fuels” |

| Japan | $10B POWERR Asia for emergency procurement and supply chains | Pragmatic: strengthen supply capacity across all sources |

| China | “Actively expand domestic demand” | Not explicitly addressed; focused on trade openness |

|

|

||

Sources: Official IMFC statements, April 16 – 17, 2026.

What Was Not Said

The most revealing aspects of the IMF Spring Meetings 2026 were in the silences. No major delegation mentioned the Islamabad Talks by name, despite the fact that the Pakistan-brokered ceasefire was the single most consequential diplomatic development since the war began. Pakistan’s Finance Minister Muhammad Aurangzeb served as First Vice-Chair of the G-24, giving the country a formal leadership role at the meetings, but the institutional statements avoided acknowledging the specific mediation effort that delivered the ceasefire markets rallied on.

No delegation provided a clear estimate of the total economic cost of the war. Saudi Arabia spoke of “spillovers” and “scars.” The OECD quantified the growth and inflation impact. The UN spoke of “devastating economic consequences.” But no official figure for the cumulative GDP loss, the total infrastructure damage, or the full humanitarian cost was presented. The closest came from the OECD’s adverse scenario, which estimated that a sustained disruption could reduce global GDP by 0.5% and raise consumer prices by 0.9%, translating to roughly $500 billion in lost output annually.

No delegation addressed the economic sanctions architecture in the context of the Iran war, despite the fact that Trump’s 50% tariff threat on countries supplying weapons to Iran was announced the same week the ceasefire took effect. The G-24 communique was the only document to address sanctions directly, noting that “unilateral trade actions, including tariffs, sanctions, secondary sanctions, and other protectionist policies, especially those inconsistent with WTO rules, have extraterritorial impacts that hinder global trade.”

What Comes Next

Table 3: Scenarios for the Global Economy Based on the IMF Spring Meetings 2026 Outlook

| Scenario | Trigger | Growth Impact | Inflation Impact |

|---|---|---|---|

| Peace dividend (Bull) | Islamabad Talks succeed; Hormuz fully reopens; oil returns below $80; ceasefire holds | Global growth recovers to 3.2 – 3.4%; Gulf reconstruction begins | Inflation falls back toward 3%; central banks resume rate cuts |

| Fragile ceasefire (Base) | Ceasefire holds but Hormuz partially restricted; no comprehensive deal; tariff uncertainty persists | OECD baseline: 2.9% global growth; euro area at 0.8 – 0.9% | G20 inflation at 4.0%; central banks hold rates; “security premium” in oil |

| Conflict resumes (Bear) | Ceasefire collapses; Hormuz fully closed; Israeli operations in Lebanon escalate; oil spikes above $130 | Global growth falls to 2.4% (OECD adverse scenario); stagflation risk materialises | G20 inflation rises toward 5%+; second-round effects entrench; 1970s parallel realised |

|

|

|||

Sources: MASEconomics scenario analysis based on OECD, ECB, and IMF projections presented at the 2026 Spring Meetings.

MASEconomics Explains

Four economic concepts behind the IMF Spring Meetings 2026

Stagflation

Stagflation is the simultaneous occurrence of stagnant economic growth, rising unemployment, and persistent inflation. It is particularly dangerous because the standard policy tools for fighting inflation (raising interest rates) worsen the growth problem, and the tools for stimulating growth (cutting rates, fiscal expansion) worsen inflation. Saudi Arabia’s comparison of the current crisis to the 1970s invokes the most severe stagflation episode in modern economic history.

Supply Shock

A supply shock is a sudden disruption to the availability of a critical input. The Strait of Hormuz closure created a negative supply shock by removing approximately 20% of global oil supply from the market. Unlike demand-driven inflation, supply-driven inflation cannot be easily addressed by monetary policy because raising interest rates reduces demand without restoring supply. Multiple IMFC statements emphasised this distinction.

Special Drawing Rights (SDRs)

SDRs are an international reserve asset created by the IMF. They can be exchanged among governments for freely usable currencies. The G-24 called for regular SDR issuance to support developing countries, a proposal that would effectively create new international liquidity. Developed countries have pledged to channel $113.8 billion in SDRs to vulnerable nations through the IMF’s trust funds, with approximately $97.3 billion delivered so far.

Quota and Governance Reform

IMF quotas determine each member country’s financial contribution, voting power, and access to IMF financing. The current quota formula underrepresents emerging markets relative to their share of global GDP. The Diriyah Guiding Principles, agreed at the 2026 Spring Meetings, provide a framework for realigning quotas under the 17th General Review, the most significant governance reform effort in nearly two decades.

Explore our full library of economic explainers, from international economic organisations to fiscal and monetary policy coordination.

Explore the MASEconomics Blog →Conclusion

The IMF Spring Meetings 2026 will be remembered as the moment when the world’s top economic officials confronted, in formal institutional language, the possibility that the global economy is entering a new era of structural instability. Saudi Arabia’s invocation of 1970s stagflation was not rhetorical: it was a warning rooted in the specific observation that the current supply shock is propagating through energy, fertilisers, food, and industrial inputs simultaneously. The OECD’s growth downgrades and inflation upgrades quantified the damage. China’s counter-narrative of resilient growth highlighted the divergence between the world’s two largest economies. And the US-versus-everyone fracture over the IMF’s mandate revealed an institutional crisis that will shape global economic governance well beyond 2026.

The next IMFC meeting is scheduled for October 2026 in Bangkok, Thailand. Between now and then, the outcome of the Islamabad peace process, the central bank rate decisions of the Fed, ECB, and Bank of England, and the trajectory of oil prices will determine whether the world gathers in Bangkok to celebrate recovery or to manage a deepening crisis.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.