In April 2026, as the Strait of Hormuz crisis sent oil prices surging past $100 per barrel and governments scrambled to release emergency reserves, a question that had been debated in seminar rooms for years suddenly became urgent: what if a country did not need oil for its cars at all? China, where more than half of all new cars sold are now electric, experienced the oil shock differently from nations still dependent on internal combustion. Norway, where 93% of new car sales were battery electric in 2024, barely noticed at the pump. Meanwhile, the United States, where EVs account for roughly 10% of new sales, and the federal tax credit was eliminated in late 2025, faced the full force of rising fuel costs.

Electric vehicles are no longer a niche technology or a climate policy experiment. In 2025, global EV sales exceeded 20 million units, capturing more than one in every four new cars sold worldwide, according to the IEA’s Global EV Outlook 2025. The global EV market generated nearly $1 trillion in revenue. Battery costs have fallen 90% in a decade. Chinese manufacturers are producing electric cars that are already cheaper than their petrol equivalents. By 2030, EVs are projected to displace more than 5 million barrels of oil per day, fundamentally reshaping global energy markets.

But the EV revolution is also creating new dependencies, new market failures, and new geopolitical vulnerabilities. The economics of electric vehicles are far more complex than the simple narrative of “green cars replacing dirty ones.”

How Electric Vehicles Went from Curiosity to Global Force

The modern electric vehicle revolution began not with an environmental movement, but with a Silicon Valley bet. When Tesla delivered its first Roadster in 2008, the idea that battery-powered cars could compete with petrol vehicles seemed absurd. Batteries were expensive ($1,000 per kilowatt-hour), range was limited, and charging infrastructure was virtually nonexistent. Established automakers dismissed EVs as toys for wealthy early adopters.

Fifteen years later, the economics have inverted. Lithium-ion battery pack prices have fallen from over $1,000/kWh in 2010 to approximately $115/kWh by 2024, according to BloombergNEF. In China, battery packs now cost as little as $94/kWh, and industry forecasts project costs approaching $80/kWh by 2027. This collapse in battery costs, the single largest component of an EV’s price, has transformed the economics of vehicle ownership. In China, two-thirds of electric cars are now cheaper than their petrol equivalents. In Europe, Transport & Environment projects price parity across all vehicle segments by 2030.

The growth trajectory has been staggering. Global EV sales grew 25% in 2024 to 17.8 million units. In 2025, sales exceeded 20 million, with the EV share of the global car market surpassing 25%. China alone accounted for roughly 65% of global EV sales, with companies like BYD overtaking Tesla as the world’s largest EV manufacturer by units sold. In Europe, tighter emissions regulations pushed the battery electric share to 24% in Q4 2025. Emerging markets in Southeast Asia and Latin America are now among the fastest-growing EV markets, with Vietnam reaching nearly 40% EV sales penetration.

The Rise of Electric Vehicles: Key Milestones (2008-2026)

| Year | Event | Economic Significance |

|---|---|---|

| 2008 | Tesla Roadster delivered; first modern highway-capable EV | Proved EVs could compete on performance; battery cost >$1,000/kWh |

| 2012 | Tesla Model S launched; Nissan Leaf reaches mass market | First viable luxury EV; Leaf becomes world’s best-selling EV |

| 2015 | Paris Climate Agreement signed; 196 nations commit to emissions targets | Created policy framework driving EV mandates and subsidies worldwide |

| 2017 | China launches New Energy Vehicle (NEV) mandate | World’s largest car market commits to electrification; subsidies exceed $60 billion |

| 2020 | Battery costs fall below $140/kWh; EU Green Deal announced | Price inflection point; EU commits to 2035 ICE sales ban |

| 2022 | US Inflation Reduction Act: $7,500 EV tax credit with sourcing rules | Largest US clean energy investment; reshapes North American supply chains |

| 2024 | Global EV sales reach 17.8 million; China exceeds 50% EV share | EVs displace 1.3 million barrels of oil per day globally |

| 2025 | US federal EV tax credit eliminated (October); global sales exceed 20 million | US EV growth stalls; Europe and emerging markets accelerate |

| 2026 | Hormuz crisis drives oil past $100; EV demand surges in oil-importing nations | Energy security becomes primary driver of EV adoption beyond climate policy |

|

||

Why EVs Are Disrupting the Global Energy Order

The EV revolution can be explained through four interconnected economic concepts that together illuminate why this transition is accelerating, why it is uneven, and why it is creating both opportunities and new risks.

Negative Externalities and the Case for Government Intervention

The fundamental economic justification for EV subsidies is the concept of negative externalities. When a driver fills their tank with petrol, they pay for the fuel but not for the climate damage, air pollution, or health costs that combustion imposes on society. The IMF estimates that global fossil fuel subsidies, both explicit and implicit, reached $7 trillion in 2022 when accounting for these unpaid environmental and health costs. Because the market price of petrol does not reflect its true social cost, too many petrol cars are produced and driven, representing a classic case of market failure.

Government subsidies for EVs are, in economic theory, a correction for this market failure. By making EVs cheaper relative to petrol cars, subsidies shift consumer behaviour toward the socially optimal level of EV adoption. The US offered a $7,500 federal tax credit (eliminated in late 2025), China provided purchase subsidies exceeding $60 billion cumulatively, and European nations have offered a patchwork of incentives from direct grants to tax exemptions. The question economists debate is not whether subsidies are justified in principle, but whether the specific design of each subsidy is efficient, and whether the cost to taxpayers is proportionate to the environmental benefit achieved.

Comparative Advantage and the New Geography of Manufacturing

The EV revolution is reshaping the global geography of automobile manufacturing, and the theory of comparative advantage helps explain why. China has achieved dominance through a combination of massive industrial policy, a head start in battery manufacturing, and access to the critical mineral supply chain. Chinese companies control roughly 80% of global battery cell production capacity. CATL and BYD together hold over 55% of the global EV battery market. China processes over 60% of the world’s lithium, 73% of cobalt, and over 90% of graphite, according to the US Energy Information Administration.

This concentration has created a new form of comparative advantage: China can produce EV batteries and complete vehicles at costs that Western manufacturers cannot match. BYD’s Seagull, a fully electric city car, sells for under $10,000 in China. No European or American manufacturer can produce a comparable vehicle at that price. The result is a flood of competitively priced Chinese EVs entering global markets: in 2025, Chinese-made EVs accounted for 26% of sales in the UK, 36% in Spain, and nearly 80% in Australia.

This has triggered a protectionist backlash. The European Union imposed tariffs of up to 38% on Chinese-made EVs in 2024. The United States maintains a 100% tariff on Chinese EVs. Canada followed with 100% tariffs of its own. The global tariff war has extended directly into the EV sector, with governments torn between the consumer benefits of cheap Chinese EVs and the strategic imperative to maintain domestic manufacturing capability.

Creative Destruction

Joseph Schumpeter’s concept of creative destruction, the process by which innovation destroys existing industries while creating new ones, is playing out in real time in the EV transition. The internal combustion engine (ICE) industry supports a vast ecosystem: engine manufacturing, transmission production, exhaust systems, oil changes, spark plugs, fuel injection, and the entire petrol station network. An electric vehicle needs none of these. A typical ICE powertrain contains over 2,000 moving parts; an electric motor contains roughly 20.

The implications for employment are enormous. The European Automobile Manufacturers’ Association estimates that the transition could put 600,000 jobs at risk across the EU automotive supply chain by 2040. Germany, home to the world’s largest automotive component suppliers, faces particular exposure: companies like Bosch, Continental, and ZF Friedrichshafen derive substantial revenue from ICE-specific components that EVs simply do not need.

Simultaneously, the EV transition is creating entirely new industries: battery manufacturing (projected to exceed $200 billion annually by 2030), charging infrastructure ($100+ billion in investment planned), battery recycling, and critical mineral mining and processing. The economic question is whether the new jobs created by the EV ecosystem will match, in number, skill level, and geographic distribution, the old jobs destroyed. History suggests that creative destruction creates more value overall, but the benefits are rarely distributed evenly.

Energy Security

The 2026 Strait of Hormuz crisis has made the energy security argument for EVs impossible to ignore. Twenty percent of the world’s oil passes through the Strait, and the disruption sent Brent crude surging above $100. Countries with high EV penetration experienced the shock differently from those still reliant on petrol.

Norway, where EVs account for the vast majority of new sales and road transport oil consumption fell 12% between 2021 and 2024, is significantly less vulnerable to oil price spikes than it was a decade ago. China’s expanding EV fleet displaced oil demand equivalent to roughly 800,000 barrels per day in 2024, providing a meaningful buffer against supply disruptions. Across all vehicle types globally, EVs displaced over 1.3 million barrels of oil per day in 2024, a figure that grew 30% year-over-year, and is projected to reach 5 million barrels per day by 2030, according to the IEA.

This oil displacement has profound implications for the economics of oil price shocks. As the global EV fleet grows, each successive oil crisis will have a diminishing impact on transport costs for electrified economies. Countries that accelerate EV adoption are, in effect, buying insurance against future oil shocks. The inflationary effects of energy price shocks are attenuated in proportion to the electrification of the transport fleet.

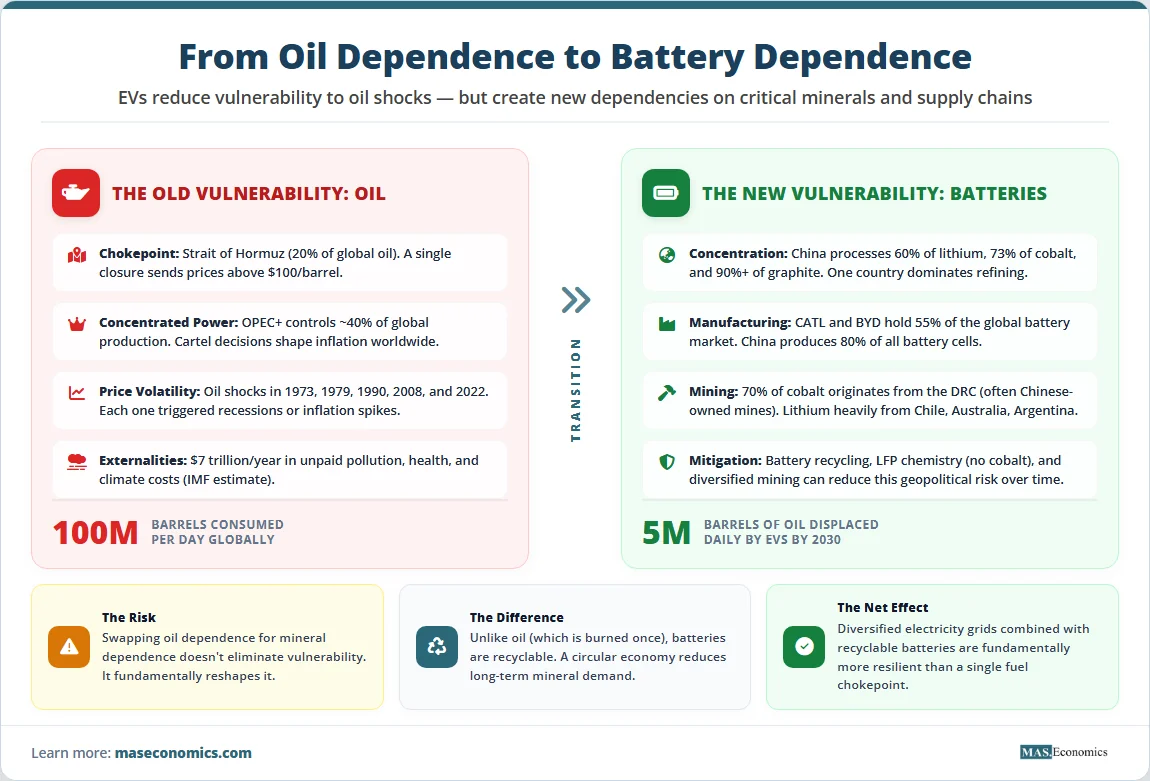

However, there is a critical caveat: replacing oil dependence with battery mineral dependence does not eliminate strategic vulnerability. It reshapes it. China’s dominance of the battery supply chain, from mining to refining to manufacturing, creates a new single point of failure. The geopolitics of lithium and cobalt may prove just as contentious as the geopolitics of oil. Economists increasingly recognise that true energy security requires diversification of both fuel sources and supply chains.

The Numbers Behind the EV Revolution

The speed of the EV transition becomes clear when you examine the sales trajectory. The chart below shows global EV sales and market share from 2018 to 2025, with the 2026 projection.

Global Electric Vehicle Sales and Market Share (2018-2026 Projected)

Source: IEA Global EV Outlook 2025, Benchmark Mineral Intelligence, and EV Volumes. 2026 figure is a projected estimate.

The collapse in battery costs is the single most important economic driver of the EV transition. The chart below shows the dramatic decline in lithium-ion battery pack prices from 2013 to 2025.

Lithium-Ion Battery Pack Price ($/kWh, Global Average, 2013-2025)

Source: BloombergNEF. Prices are volume-weighted averages for lithium-ion battery packs globally.

The following table quantifies the energy security dividend of EV adoption by showing how oil displacement is growing across regions.

Oil Displacement by Electric Vehicles (Million Barrels Per Day)

| Region | 2022 | 2024 | 2030 (Projected) | Key Driver |

|---|---|---|---|---|

| China | 0.4 | 0.8 | 2.5 | 50%+ EV sales share; 150M EVs projected by 2030 |

| Europe | 0.2 | 0.3 | 1.2 | EU CO2 standards; 2035 ICE ban commitment |

| United States | 0.1 | 0.15 | 0.6 | Tax credit removed 2025; state mandates continue |

| Rest of World | 0.05 | 0.1 | 0.7 | Emerging market growth (Vietnam, Brazil, Thailand) |

| Global Total | 0.75 | 1.3 | 5.0+ | Equivalent to entire transport oil demand of Japan |

|

||||

The Uneven Impact of the EV Transition

The Winners

China is the undisputed winner of the EV era so far. Chinese companies dominate every layer of the value chain, from lithium processing to battery manufacturing to finished vehicle production. BYD alone sold over 4 million EVs in 2025. China’s strategic investment in the battery supply chain, which began in earnest after the 2008 financial crisis, has given it a structural advantage that rivals will take decades to replicate. For Chinese consumers, the result is abundant, affordable electric vehicles that are shielding them from the worst effects of oil price volatility.

Oil-importing developing nations that embrace EVs stand to gain enormously. Countries like Vietnam, Thailand, Indonesia, and Brazil spend billions annually on oil imports. Every barrel of oil displaced by an EV-powered kilometre improves the current account balance, reduces inflation exposure, and strengthens the balance of payments. Vietnam’s EV sales share has surged to nearly 40%, driven partly by domestic manufacturer VinFast, illustrating how electrification can simultaneously reduce oil dependence and build domestic industrial capacity.

Consumers globally benefit from falling vehicle operating costs. Electricity is cheaper than petrol per mile driven in virtually every country. EVs have fewer moving parts and require less maintenance. As purchase prices continue to fall toward parity with ICE vehicles, the total cost of ownership advantage will become overwhelming.

The Losers

Oil-exporting nations face an existential long-term challenge. If EVs displace 5 million barrels per day by 2030 and potentially 20 million by 2040, the structural decline in transport fuel demand will permanently reduce the revenue that countries like Saudi Arabia, Russia, Iraq, and Nigeria depend upon. This is not a short-term cyclical risk. It is a structural shift that will reshape the geopolitics of energy over the coming decades.

Workers in the ICE supply chain face significant displacement risk, particularly in Germany, Japan, and the American Midwest. The skills required to manufacture electric powertrains are fundamentally different from those needed for combustion engines. Reskilling programmes exist, but the pace of transition may outstrip the capacity to retrain workers, creating concentrated pockets of economic hardship in regions historically dependent on ICE manufacturing.

The United States risks falling behind in the global EV race. The elimination of federal tax credits, the rollback of fuel economy standards, and 100% tariffs on Chinese EVs have slowed domestic adoption. US EV sales grew just 1% in 2025 after the policy shifts, while the global market grew 20%. American consumers face higher vehicle prices and less model choice than their European or Asian counterparts, while US automakers lose ground in export markets to Chinese competitors.

What the EV Transition Teaches About Economic Change

The electric vehicle revolution offers four lessons that extend far beyond the automotive industry.

First, technology-driven cost reduction is the most powerful economic force in the energy transition. Subsidies accelerated EV adoption, but the underlying driver is the relentless decline in battery costs, a learning curve effect that mirrors the trajectory of solar panels, semiconductors, and telecommunications. When a technology improves by 15-20% per year in cost-performance, policy merely determines the speed of adoption, not whether adoption occurs.

Second, supply chain concentration creates new vulnerabilities even as old ones are resolved. The transition from oil dependence to battery mineral dependence does not eliminate geopolitical risk. It relocates it. True energy security requires not just electrification, but diversification of the mineral supply chain, investment in battery recycling, and development of alternative chemistries that reduce reliance on any single material or country.

Third, trade policy shapes technology adoption as powerfully as technology itself. China’s dominance was built through decades of deliberate industrial policy. The US and European tariff responses are attempting to protect domestic industries but risk slowing adoption and raising costs for consumers. The tension between free trade efficiency and strategic industrial autonomy is at the heart of every EV policy debate.

Fourth, energy transitions are always uneven. Some countries, industries, and workers will benefit enormously. Others will bear disproportionate costs. The economic case for EVs is overwhelming at the macro level, but the distributional consequences require deliberate policy attention, especially for communities and nations whose livelihoods depend on the oil economy that EVs are displacing.

MASEconomics Explains

Conclusion

The electric vehicle revolution is not just an automotive story. It is an energy story, a trade story, a geopolitical story, and an economic transformation story all at once. In a world where oil shocks can still send prices surging past $100 a barrel, the strategic case for electrification has never been stronger. Countries that electrify their transport fleets are buying insurance against the next crisis, whether it comes from the Strait of Hormuz, an OPEC production cut, or a geopolitical conflict that disrupts supply.

But the transition also carries risks. Replacing oil dependence with battery mineral dependence does not eliminate vulnerability. It reshapes it. The economics of EVs are overwhelming: costs are falling, adoption is accelerating, and the technology is improving every year. The question is not whether the internal combustion engine will be replaced. It is how fast, how evenly, and at what cost to the workers, communities, and nations that built the oil-powered economy of the 20th century.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.