Central bank independence is the legal and operational separation between a country’s monetary policy authority and its elected government. It is the institutional arrangement under which interest rate decisions are taken by appointed officials with statutory protection, not by ministers or legislators responding to electoral pressure. The arrangement is recent. As late as 1989, only New Zealand had a formal inflation target combined with full operational independence for its central bank. By 2000, every G7 central bank operated under broadly similar arrangements. Today, the Garriga (2025) dataset codes 192 countries on a 0 to 1 independence index, with the global average rising from roughly 0.40 in 1980 to 0.65 by 2023.

The arrangement is also contested. The 2025 to 2026 transition at the Federal Reserve, the long-running political conflict over the Bank of Turkey, and Argentina’s history of forced governor resignations all show that independence is granted by legislatures and can be removed by them. The empirical evidence that independent central banks deliver lower inflation without higher unemployment is the central reason the framework has held across most advanced economies. The rest of this article explains where independence comes from, how it is measured, what the evidence shows, and where the framework is being tested.

Two types of independence. Goal independence is the authority to set the policy objective itself (the inflation target, for example). Instrument independence is the authority to choose the tools to achieve that objective. Most modern central banks have instrument independence but not goal independence: the government or legislature sets the target, and the central bank decides how to reach it.

Defining Central Bank Independence

Central bank independence is a multi-dimensional concept. The widely used Cukierman, Webb, and Neyapti (CWN) framework, developed in 1992, codes four legal dimensions: the appointment and dismissal rules for the chief executive, the institution’s stated policy objectives, the procedure for resolving policy conflicts between the central bank and the government, and the legal limits on central bank lending to the government. Each dimension is scored from 0 (no independence) to 1 (maximum independence), and the four are aggregated into a composite index.

The framework distinguishes between two operational types. Goal independence is the authority to set the policy objective itself, such as the inflation target or the trade-off between price stability and employment. Instrument independence is the authority to choose the tools used to achieve a given objective. The Federal Reserve Act of 1913 grants the Fed both forms: the dual mandate is internally defined by the FOMC, and the rate-setting tools are chosen by the Committee. The Bank of England has instrument independence only: the 2 percent inflation target is set by HM Treasury annually under the Bank of England Act 1998. The European Central Bank has both, with the primary objective of price stability defined in the Treaty on the Functioning of the European Union and the operational target chosen by the Governing Council.

This distinction matters because it locates democratic accountability where it sits comfortably (with elected officials setting the goals) and technical authority where it works best (with appointed experts choosing the instruments). The arrangement is documented in greater detail in our article on central banking and monetary policy.

The Theoretical Foundation: Time Inconsistency

The economic case for central bank independence rests on the time inconsistency literature of Kydland and Prescott (1977) and Barro and Gordon (1983). The argument runs in three steps. A government that controls monetary policy faces a temptation to generate surprise inflation, either to reduce the real value of public debt or to boost employment before an election. Rational agents anticipate this temptation, raising inflation expectations and producing higher inflation without the temporary output boost. The result is worse on both counts: higher inflation and no employment gain.

The way out is to delegate monetary policy to an institution that cannot benefit from surprise inflation. An appointed central banker, given a clear price-stability mandate and removed from the electoral cycle, is structurally less tempted than an elected official. Rational agents observe the delegation, lower their inflation expectations, and the equilibrium shifts to lower inflation without higher unemployment. The 1985 work of Kenneth Rogoff formalised this as the “conservative central banker” model, in which the chosen monetary authority is institutionally biased toward inflation aversion relative to the median voter.

The empirical predictions of this literature are testable. Countries with more independent central banks should have lower inflation on average, but no worse employment or output performance. The cross-country evidence on this prediction is among the most robust findings in modern macroeconomics and is documented in the next section.

How Independence Is Measured

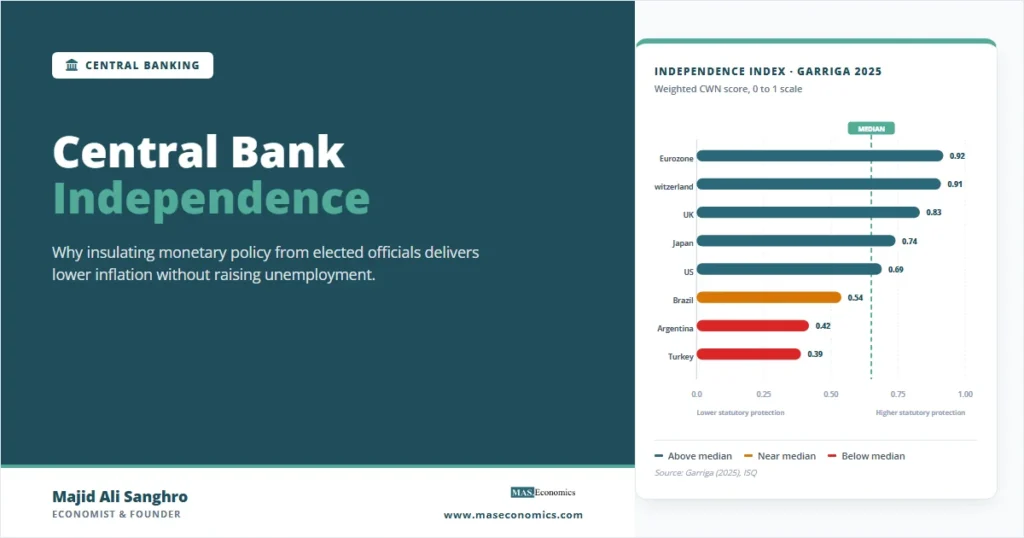

The Garriga (2025) dataset, the most current systematic measure of de jure independence, codes 192 countries from 1970 to 2023. Each country receives a weighted score on the 0-to-1 scale based on the four CWN dimensions. The 2025 extension covers a longer period and a broader country sample than the original 2016 release, with the weighted index giving extra weight to legal limits on central bank lending to the government.

Three patterns emerge from the data. First, there has been a substantial global increase in independence since 1989. The average weighted index across all countries rose from around 0.40 in 1980 to 0.65 by 2023. Second, the pattern of reform has not been monotonic. Garriga (2025) identifies more than 100 reforms reducing CBI alongside the larger number of reforms increasing it. Third, regional patterns matter: Western Europe and North America have higher average independence than Latin America or Africa, but within-region variance is also large.

The de jure measure captures what the law says. A separate literature on de facto independence captures what happens in practice, often using indicators like governor turnover rates, the frequency of resignations under political pressure, or the gap between the policy rate and a Taylor-rule benchmark. The two measures correlate but are not identical. Turkey, for example, has had moderately strong de jure protections but very weak de facto independence since 2018, with the central bank governor replaced four times in five years.

| Country | Central bank | Independence index (0-1) | Year of major reform | Notable feature |

|---|---|---|---|---|

| Eurozone | European Central Bank | 0.92 | 1998 (Maastricht) | Treaty-level protection, no instructions allowed |

| Switzerland | Swiss National Bank | 0.91 | 2004 (revised law) | Constitutional independence |

| Sweden | Sveriges Riksbank | 0.89 | 1999 | Independence reaffirmed 2023 |

| Chile | Banco Central de Chile | 0.84 | 1989 | Constitutional autonomy |

| United Kingdom | Bank of England | 0.83 | 1998 | Operational only; goal set by Treasury |

| Canada | Bank of Canada | 0.78 | 1991 | Inflation target jointly set with government |

| Japan | Bank of Japan | 0.74 | 1997 | Independence Act of 1997 |

| United States | Federal Reserve | 0.69 | 1951 (Accord) | Both goal and instrument independence |

| India | Reserve Bank of India | 0.55 | 2016 (MPC Act) | Formal target adopted 2016 |

| Brazil | Banco Central do Brasil | 0.54 | 2021 (autonomy law) | Recent statutory upgrade |

| Argentina | Banco Central de la República Argentina | 0.42 | 2012 (charter change) | Reforms have eroded independence |

| Turkey | Türkiye Cumhuriyet Merkez Bankası | 0.39 | 2001 (formal autonomy) | De facto independence weak post-2018 |

|

||||

The table illustrates the wide spread. The Eurozone, Switzerland, and Sweden sit at the top with weighted indices above 0.85. The Federal Reserve sits below them despite being widely regarded as a strongly independent institution, because the CWN coding gives weight to the procedure for resolving policy conflicts (where the Federal Reserve Act leaves some ambiguity) and to legal limits on lending to the government (where the Fed has more flexibility than the ECB). The lower-scoring countries (Argentina, Turkey) have legal frameworks that, on paper, grant moderate independence but in practice have been overridden repeatedly.

Visualising the Cross-Country Distribution

The bar chart below shows the same data sorted from most to least independent, with a vertical reference line at the cross-country median (approximately 0.65 on the weighted index for the 192 countries in the Garriga 2025 sample). Countries to the right of the median have above-average statutory independence; countries to the left fall below.

The chart makes the empirical pattern visible. The cluster at the top (ECB, SNB, Riksbank, BCCh, BoE) represents the post-1989 model of explicit inflation targets combined with strong statutory protection. The middle cluster (BoC, BoJ, Fed) represents older institutional arrangements with strong de facto independence but moderately weaker formal protection. The lower cluster (RBI, BCB) represents emerging-market institutions that have upgraded their frameworks more recently. Argentina and Turkey sit below the median despite having formal autonomy provisions, because the index has not been updated to reflect the de facto erosion that the literature documents.

The Empirical Case: Independence and Inflation

The strongest piece of evidence for central bank independence is the cross-country correlation with inflation. Alesina and Summers (1993) showed that in a sample of OECD countries, the simple correlation between central bank independence and average inflation was strongly negative: countries with more independent central banks had lower inflation on average. The result held when controlling for the standard determinants of inflation (openness, exchange rate regime, fiscal stance) and across multiple coding schemes for independence.

Subsequent work extended this finding. Cukierman, Webb, and Neyapti (1992) showed that the relationship held in developing countries when independence was measured by de facto turnover rather than de jure protection. Bodea and Hicks (2015) showed that the inflation-independence relationship is conditional on the strength of democratic institutions: independence works to lower inflation only when courts and legislatures can credibly enforce the central bank’s mandate. Garriga and Rodriguez (2020) extended this to a 70-country emerging market sample and confirmed the inflation-reducing effect.

Crucially, the same studies find no evidence that independence raises unemployment. The Phillips Curve relationship implies a short-run trade-off between inflation and unemployment, but cross-country data shows that independent central banks deliver lower inflation without paying for it in higher long-run unemployment. This finding, robust across decades of empirical work, is the central reason most advanced economies converted to independent inflation-targeting frameworks between 1989 and 1998.

The Independence Movement: 1989 to 1998

The institutional conversion happened in a remarkably short window. New Zealand was first, with the Reserve Bank Act 1989 introducing the world’s first explicit inflation target combined with statutory governor independence. The Act formalised goal independence at the political level (the Minister of Finance and the Governor jointly agree the target) and full instrument independence for the Reserve Bank.

Canada followed in 1991, with a joint Bank of Canada and Department of Finance inflation target of 2 percent within a 1-to-3 percent control band. The United Kingdom adopted an inflation target in 1992 after exiting the European Exchange Rate Mechanism, and granted operational independence to the Bank of England in May 1997. Sweden followed in 1993, and the Reserve Bank of Australia in the same year. The Bank of Japan Act of 1997 formalised the BoJ’s independence, though the de facto degree of independence has varied across governorships.

The European Central Bank, created in 1998 under the Maastricht Treaty, was designed from the outset as the most independent central bank in the world. Article 130 of the Treaty on the Functioning of the European Union explicitly prohibits ECB officials from accepting instructions from any government, and the legal protection is at the Treaty level rather than at the ordinary statute level. Changing the ECB’s mandate requires unanimous agreement among all member states, a far higher bar than amending domestic legislation.

The Federal Reserve is an older institution that converged on the same model through a different path. The 1951 Treasury-Fed Accord ended the wartime arrangement under which the Fed had pegged Treasury yields, restoring operational independence. The 1977 Federal Reserve Reform Act established the dual mandate. The 2012 statement of long-run goals adopted the 2 percent inflation target formally. The 2020 framework review introduced average inflation targeting. Each step institutionalised the practice that had developed under Paul Volcker (1979-1987) and Alan Greenspan (1987-2006).

The Democratic Critique

The strongest critique of central bank independence is the democratic-deficit argument. Central bank decisions on interest rates have first-order effects on employment, asset prices, mortgage costs, and the distribution of wealth. Yet those decisions are taken by unelected officials, often with limited public scrutiny of individual votes, and the officials cannot be removed except for cause. Whether this is compatible with democratic governance is a contested question.

Three responses have developed in the literature. The first is the delegation argument: legislatures delegate technical authority all the time, to courts, to military officers, to medical boards, and the central bank is just another example. Delegation does not eliminate democratic control; it locates it at the level of the statute. The legislature can amend the central bank’s mandate, change its governance, or remove its independence entirely. This requires a higher political cost, which is the institutional design intent.

The second is the accountability argument: independence does not mean opacity. Modern central banks publish meeting minutes, hold press conferences, testify before legislatures, and produce monetary policy reports several times a year. The European Central Bank President appears before the European Parliament’s Economic and Monetary Affairs Committee quarterly. The Federal Reserve Chair testifies to Congress semi-annually under the Humphrey-Hawkins requirements. The Bank of England Governor appears before the Treasury Committee approximately monthly. The associated transparency framework is documented in our article on monetary policy accountability and transparency.

The third is the empirical argument: democracies with independent central banks have delivered lower inflation without compromising employment or growth. If independence had clear democratic costs and no economic benefits, the framework would not have spread as it did. The combination of formal accountability mechanisms and the empirical record is what most political economists treat as the live answer to the democratic-deficit critique.

Where Independence Has Been Tested

The framework has been tested repeatedly. Three cases illustrate the range of outcomes.

Argentina. The Banco Central de la República Argentina has formal independence under its charter, but political interference has been chronic. In 2010, the central bank governor, Martín Redrado, refused a presidential request to use foreign reserves to service sovereign debt; he was removed by emergency decree the same week. The reserves were subsequently used, and Argentina entered a period of high inflation that exceeded 50 percent annually by 2015 and reached above 200 percent in 2024. The case illustrates how de jure independence can be overridden when de facto enforcement mechanisms are weak.

Turkey. The Türkiye Cumhuriyet Merkez Bankası has been a textbook case of de facto independence collapse. Between 2019 and 2023, four central bank governors were replaced by presidential decree after refusing to cut interest rates against staff recommendations. Inflation rose from 11 percent in 2019 to over 80 percent in 2022 before partial stabilisation. The lira fell from roughly 5 per US dollar in 2018 to over 30 per dollar by 2024. The case shows the empirical cost of political interference in an emerging-market context with weak institutional checks.

The United States in 2025-2026. The Federal Reserve faced unprecedented political pressure during the second Trump administration, including public demands for rate cuts, calls for the resignation of Chair Jerome Powell, and the eventual nomination of Kevin Warsh as a successor. The Federal Reserve Act protects governors from removal except “for cause”, and the Powell-led FOMC continued to set policy based on staff forecasts rather than presidential preference. The episode is analysed in our article on threats to central bank independence: lessons from the 2025-2026 Fed transition. The institutional outcome demonstrated that legal protection can hold under sustained political pressure, but the conflict surfaced the fragility of the underlying political consensus.

Independence in the Post-2008 World

The global financial crisis stress-tested the boundary between independent monetary policy and elected fiscal policy. Quantitative easing programmes expanded central bank balance sheets to levels that made the central bank the largest single holder of government debt in several major economies. The Bank of Japan owns more than half of all outstanding Japanese government bonds. The Federal Reserve’s Treasury holdings peaked at roughly 25 percent of marketable Treasury debt in 2022. The European Central Bank’s holdings under APP and PEPP reached EUR 4.9 trillion at peak.

The size of these holdings raises the question of where monetary policy ends and debt management begins. The literature on fiscal dominance, dating to Sargent and Wallace (1981), shows that when fiscal authorities issue debt at levels that cannot be sustained at non-monetary rates, the central bank eventually loses operational independence. The political pressure on the Fed during the 2022 to 2023 tightening cycle, and the parallel pressure on the ECB to limit the impact of rising yields on peripheral sovereigns, were both partial manifestations of this concern.

The wider boundary debate continues over central bank engagement with climate policy. The Network for Greening the Financial System now includes 138 central banks and supervisors. The ECB has tilted its corporate bond purchases toward issuers with lower carbon footprints. The Bank of England has run climate stress tests. The Federal Reserve has been more cautious, framing climate involvement as financial-stability work rather than monetary policy. Whether climate policy belongs inside the independence framework is now an active institutional question.

MASEconomics Explains

Four economic concepts behind central bank independence

These concepts are explored in depth across our educational articles library.

Explore the MASEconomics BlogConclusion

Central bank independence is the institutional arrangement that gives monetary policy authority to appointed officials with statutory protection rather than to elected ministers. The theoretical case rests on time inconsistency: a delegated, conservative monetary authority can deliver lower inflation than a government tempted by surprise inflation. The empirical case rests on cross-country evidence that more independent central banks have lower average inflation without higher unemployment. The institutional case rests on the conversion of nearly every major economy to inflation targeting combined with independent governance between 1989 and 1998. The framework is contested in three places: the democratic-deficit critique that unelected officials should not make consequential macroeconomic decisions, the operational pressure from large central bank balance sheets that blur the line with fiscal policy, and the recent political pressure on the Federal Reserve, the Bank of Turkey, and other institutions where the de facto enforcement of de jure protections has been tested. The Garriga (2025) dataset shows that the global average independence index has risen from 0.40 in 1980 to 0.65 in 2023, with the institutional model still spreading despite the high-profile reversals.

Frequently Asked Questions

What is central bank independence?

Central bank independence is the legal and operational separation between monetary policy decisions and elected government control. An independent central bank sets interest rates and conducts monetary operations without instruction from the executive branch, with statutory protection for its officials. The arrangement is intended to insulate monetary policy from electoral pressure and short-term political incentives.

Why is central bank independence considered important?

Independence is considered important because cross-country evidence shows that more independent central banks deliver lower average inflation without higher unemployment. The theoretical foundation is the time-inconsistency literature of Kydland and Prescott, which shows that governments controlling monetary policy face a temptation to generate surprise inflation that rational agents anticipate, producing higher inflation without the temporary output boost.

What is the difference between goal independence and instrument independence?

Goal independence is the authority to set the policy objective itself, such as the inflation target. Instrument independence is the authority to choose the tools used to achieve that objective. Most modern central banks have instrument independence but limited goal independence: the government or legislature sets the target and the central bank decides how to reach it. The Bank of England has only instrument independence; the Federal Reserve has both.

Can a central bank be too independent?

The democratic-deficit critique argues that unelected central bank officials should not make decisions with such large economic and distributional effects. The response from the economic literature is that legislatures delegate technical authority routinely, that modern central banks operate under extensive accountability and transparency requirements, and that the empirical record shows independence has lowered inflation without raising unemployment. The trade-off is real but the framework has held across most advanced economies.

Which countries have the most independent central banks?

The European Central Bank, the Swiss National Bank, and the Swedish Riksbank score highest on the Garriga (2025) weighted independence index, with values above 0.85. The Bank of England, the Bank of Canada, and the Bank of Japan score in the 0.7 to 0.85 range. The Federal Reserve scores around 0.69. Emerging market central banks generally score lower, with significant variation. The cross-country median is approximately 0.65 across the 192 countries in the Garriga sample.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics