Monetary policy tools are the operational instruments through which central banks influence interest rates, credit conditions, and the money supply. The modern toolkit has six instruments: administered rates (interest on reserves), open market operations, standing facilities, reserve requirements, large-scale asset purchases, and forward guidance. Each instrument plays a defined role inside a policy corridor that bounds the overnight rate between a deposit floor and a lending ceiling. The toolkit looks similar across the Federal Reserve, the European Central Bank, the Bank of England, and the Bank of Japan, but the operational details differ in ways that matter for how policy actually transmits to the economy.

The toolkit was overhauled after 2008. Before the financial crisis, most major central banks ran “scarce reserve” systems in which open market operations directly determined the overnight rate. After 2008, the Federal Reserve and the European Central Bank moved to “ample reserve” systems in which an administered interest rate on reserves became the primary control instrument. That structural shift, and the addition of asset purchases and forward guidance as standing parts of the toolkit, define how monetary policy operates today.

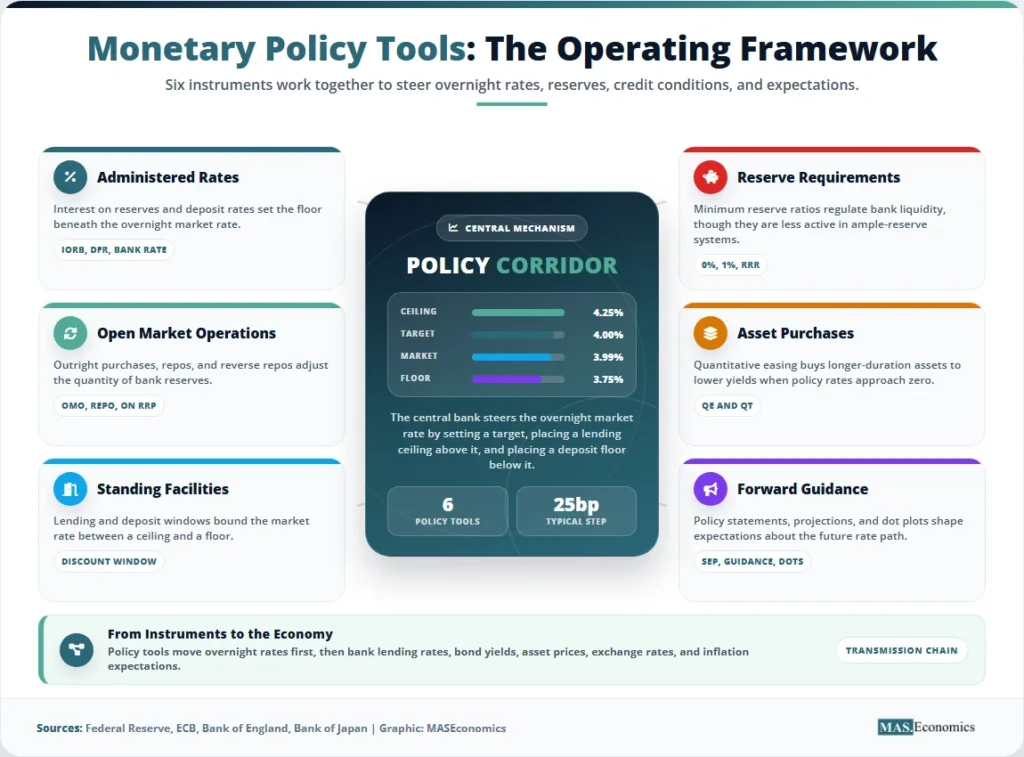

The modern toolkit at a glance. Administered rates set the policy stance. Open market operations adjust the quantity of reserves. Standing facilities bound the policy corridor. Reserve requirements set minimum bank holdings. Asset purchases compress term premia at the zero lower bound. Forward guidance shapes expectations of the future rate path. The six instruments work together inside one operating framework.

The Policy Rate as the Anchor

Every monetary policy decision starts with the policy rate. This is the short-term interest rate the central bank chooses to target. In the United States, it is the federal funds rate, currently targeted at a range of 3.50 to 3.75 percent. In the euro area, it is the ECB deposit facility rate, at 2.00 percent. In the United Kingdom, it is the Bank Rate, at 3.75 percent. In Japan, it is the uncollateralised overnight call rate, at 0.75 percent. Each rate is the price at which commercial banks lend reserves to each other overnight, and every other interest rate in the economy is built off it.

The policy rate is set by a committee. The Federal Open Market Committee meets eight times a year. The ECB Governing Council meets eight times a year. The Bank of England Monetary Policy Committee meets eight times a year. Each meeting produces a published decision, plus, after a short delay, the minutes that record the discussion and the vote count. Markets price the next several meetings continuously through interest rate futures and overnight index swaps, which gives the central bank a real-time read on what the public expects.

The reason the policy rate matters is the term structure of interest rates. A change in the overnight rate moves expectations of the rate over the next month, the next quarter, and the next year, and these expectations are embedded in the prices of bonds, mortgages, and corporate loans. The transmission from policy rate to economic outcomes is documented in our article on the monetary transmission mechanism. The benchmark for whether the chosen rate is appropriate is the Taylor Rule, which prescribes a rate based on inflation and output gaps.

Open Market Operations and Reserve Quantities

Open market operations are the purchases and sales of government securities the central bank uses to adjust the supply of bank reserves. In a scarce-reserve system, daily open market operations are how the policy rate is kept on target. In an ample-reserve system, open market operations play a different role: they adjust the size of the balance sheet over time without being the primary tool for setting the overnight rate.

Three operational forms are used. Outright purchases (or sales) acquire bonds permanently onto the central bank’s balance sheet, expanding (or contracting) reserves accordingly. Repurchase agreements are short-term lending operations: the central bank buys securities, and the counterparty agrees to repurchase them at a slightly higher price after a fixed term. Reverse repurchase agreements are the mirror image, with the central bank lending securities and absorbing reserves. The Federal Reserve’s Overnight Reverse Repurchase Agreement Facility (ON RRP) had outstanding balances above USD 2 trillion at its peak in late 2022 and remains active as a floor for the federal funds rate.

The shift from scarce to ample reserves was operational, not theoretical. Before October 2008, the Federal Reserve held approximately USD 850 billion of Treasury securities, and bank reserves were around USD 10 billion. By 2014, reserves had grown to USD 2.8 trillion through three rounds of quantitative easing. The Federal Reserve formally adopted ample reserves as its operating regime in January 2019. The contrast between the two regimes is documented in greater detail in our coverage of quantitative tightening.

Standing Facilities and the Corridor

Standing facilities are the standing offers from the central bank to lend or accept deposits at fixed rates, available daily, against eligible collateral. Together, they form the policy corridor that bounds the overnight rate.

The lending facility sets the ceiling. The Federal Reserve’s primary credit rate (the modern discount window) is currently 3.75 percent, 25 basis points above the upper bound of the federal funds target. The ECB’s marginal lending facility is currently 2.40 percent, 40 basis points above the deposit facility rate. The Bank of England’s Operational Standing Lending Facility is 25 basis points above Bank Rate. A bank that cannot fund itself overnight in the interbank market has the option to borrow from the central bank at these rates, against acceptable collateral, with no preset cap on the amount.

The deposit facility sets the floor. The ECB’s deposit facility rate (currently 2.00 percent) is the policy rate itself. The Federal Reserve’s interest on reserve balances (IORB) of 3.65 percent and the Overnight Reverse Repo rate of 3.55 percent serve as the floor under the federal funds rate. A bank with surplus reserves will not lend below these rates because it can earn them risk-free at the central bank. The corridor structure means the market overnight rate has very little room to wander outside the range the central bank has set.

Reserve Requirements as a Direct Lever

Reserve requirements are a regulated minimum fraction of deposits that commercial banks must hold as reserves at the central bank. The Federal Reserve cut its reserve requirement ratio to zero in March 2020 and has not raised it since. The ECB requires euro area banks to hold reserves equal to 1 percent of certain liabilities. The Bank of England does not maintain a formal reserve requirement, relying instead on regulatory liquidity ratios. The Bank of Japan requires a small fraction (0.05 percent to 1.20 percent, depending on liability size) that has been unchanged since 2008.

Reserve requirements have become a minor instrument in advanced economies because the move to ample reserves made them redundant: banks already hold reserves far in excess of any plausible regulatory minimum. The People’s Bank of China is the major exception. The PBoC actively uses its required reserve ratio (RRR), currently around 6.5 percent for large banks, as a primary policy tool. Cuts to the RRR are announced in step with broader monetary easing and free up significant lending capacity for Chinese commercial banks. This use of the reserve requirement as an active instrument is one of several institutional differences that distinguish the PBoC from the Federal Reserve and the ECB.

The Six Core Tools Compared

The toolkit looks broadly similar across the four largest reserve-currency central banks. The table below summarises each instrument, current settings as of May 2026, and the operational differences across the Federal Reserve, the European Central Bank, the Bank of England, and the Bank of Japan.

| Tool | Federal Reserve | European Central Bank | Bank of England | Bank of Japan |

|---|---|---|---|---|

| Policy rate | Fed funds target 3.50–3.75% | Deposit facility rate 2.00% | Bank Rate 3.75% | O/N call rate 0.75% |

| Administered rates | IORB 3.65%, ON RRP 3.55% | DFR is the policy rate | Bank Rate paid on reserves | Tiered IOER (negative tier removed Mar 2024) |

| Standing facility ceiling | Primary credit 3.75% (discount window) | Marginal lending 2.40% | OSLF Bank Rate + 25 bp | Complementary lending facility |

| Open market operations | Outright + ON RRP daily | Weekly MROs + LTROs | Indexed Long-Term Repo, weekly | Outright JGB purchases (reduced) |

| Reserve requirements | 0% (since March 2020) | 1% of certain liabilities | No formal requirement | 0.05% – 1.20% |

| Asset purchases (QE) | SOMA portfolio in QT since 2022 | APP and PEPP in wind-down | APF in active gilt sales | JGB purchases reduced Mar 2024 |

| Forward guidance | SEP dot plot, qualitative statement | Data-dependent, meeting-by-meeting | Conditional on inflation outturn | State-contingent on inflation trend |

|

||||

The table makes three operational differences visible. First, the operating regime differs: the Federal Reserve and the ECB run floor systems with administered rates, while the Bank of England runs a similar floor but with a simpler single-rate design. Second, the role of reserve requirements differs sharply: zero at the Fed, low at the ECB and BoJ, and active at the PBoC (not shown). Third, every major central bank now carries asset purchase programmes as part of the standing toolkit even when not currently buying, because the infrastructure to restart purchases must remain in place between cycles.

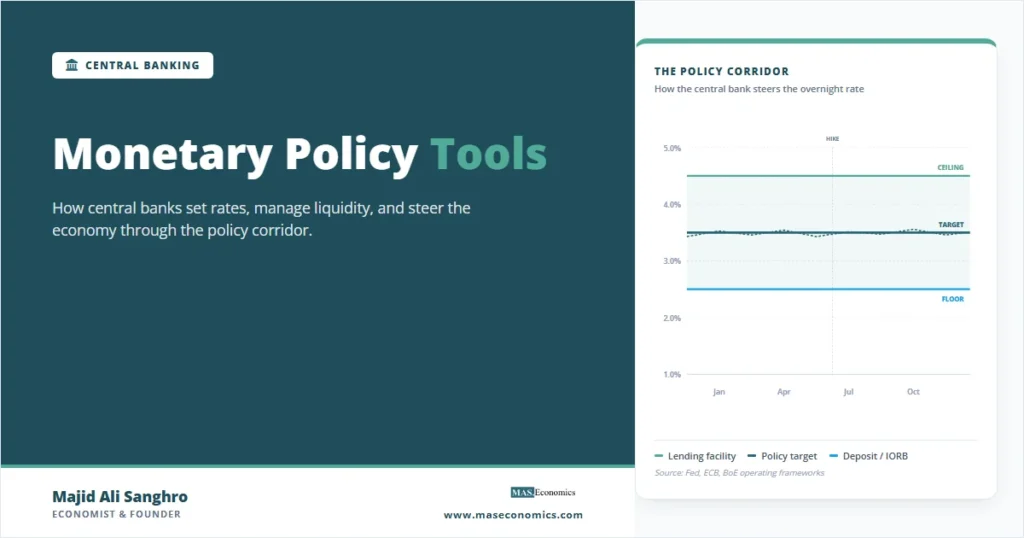

How the Policy Corridor Works

The mechanics of the policy corridor become visible when the three rates are plotted together. The ceiling (lending facility), the policy target, and the floor (deposit facility or IORB) together define the range within which the market overnight rate can move. In a well-functioning floor system, the market rate tracks the policy target almost exactly, with very small daily deviations.

The chart shows what a 25 basis point rate hike looks like inside the corridor. In April, all three administered rates stepped up together. The ceiling moves from 4.00 to 4.25 percent. The target moves from 3.75 to 4.00 percent. The floor moves from 3.50 to 3.75 percent. The market overnight rate, shown as the dashed line, tracks the target almost exactly with daily fluctuations of one or two basis points. This is the signature of a working floor system. In a scarce-reserve system, the dashed line would be much more volatile, and the central bank would have to conduct daily open market operations to keep it on target.

Forward Guidance and Communication

Forward guidance is the deliberate use of communication to shape market expectations about the future path of the policy rate. It has become a standing part of the toolkit because long-term interest rates depend on expectations of future short rates, and those expectations can be shifted directly through statements rather than indirectly through actions.

Three forms are used. Qualitative forward guidance is the open-ended language used in policy statements (“the Committee will continue to monitor incoming data”). Date-based guidance commits the central bank to a specific time horizon (the Bank of Canada’s 2020 commitment to hold rates at the effective lower bound “until economic slack is absorbed”). State-contingent guidance ties the rate path to specific economic outcomes (the Federal Reserve’s 2020 commitment to hold rates near zero “until inflation has averaged 2 percent for some time”). Each form has different credibility properties and different exit costs.

The 2013 Taper Tantrum and the 2021 to 2022 inflation overshoot are the two cases that defined modern thinking about forward guidance. In 2013, Federal Reserve Chair Ben Bernanke’s signal that asset purchases would slow caused long-term Treasury yields to rise by 100 basis points within months, far more than the Fed had intended. The episode showed that markets weight forward guidance heavily, and that small changes in language can have large effects. The 2021 to 2022 episode showed the opposite risk: forward guidance that prevented the Fed from tightening fast enough as inflation accelerated.

The Federal Reserve’s Summary of Economic Projections, released four times a year, is the most structured form of forward guidance currently in use. The “dot plot” shows where each of the 19 FOMC participants thinks the federal funds rate should be at the end of each of the next three years and in the longer run. The dot plot is not a commitment, but it provides markets with the distribution of views inside the committee and shifts the expected rate path more reliably than narrative communication alone.

Unconventional Tools at the Zero Lower Bound

The toolkit changes shape when the policy rate is at or near zero. Conventional rate cuts run out of room. Asset purchases, sometimes called quantitative easing, become the primary instrument for further easing. The mechanism is different: instead of changing the overnight rate, the central bank purchases long-duration assets to compress term premia and lower long-term yields directly.

The Federal Reserve’s three rounds of quantitative easing (QE1 in 2008 to 2010, QE2 in 2010 to 2011, QE3 in 2012 to 2014) expanded its balance sheet from USD 880 billion to USD 4.5 trillion. A fourth round in 2020 and 2021 took it to USD 8.97 trillion at peak. The Bank of Japan’s holdings reached approximately 50 percent of the JGB market by 2024. The ECB’s Asset Purchase Programme and Pandemic Emergency Purchase Programme together added EUR 4.9 trillion to its balance sheet. The Bank of England’s Asset Purchase Facility reached GBP 875 billion at peak.

The empirical literature on QE finds meaningful but uncertain effects on long-term yields. Estimates of the impact of a USD 100 billion purchase on the 10-year Treasury yield range from roughly 2 to 10 basis points, depending on the period and the methodology. The effects on inflation and output are smaller and slower than conventional rate cuts. The episode-by-episode discussion of these effects is documented in our article on quantitative easing.

The reverse process, quantitative tightening, runs the balance sheet down by allowing maturing securities to roll off or by outright sales. The Federal Reserve has reduced its balance sheet by approximately USD 2.1 trillion since 2022. The Bank of England has been the most aggressive, actively selling gilts as well as letting them mature. The ECB has stopped reinvestments and is letting its portfolios run off passively. The Bank of Japan started reducing JGB purchases in March 2024 but has not yet committed to active sales.

Lender of Last Resort Operations

The discount window and equivalent facilities exist for exceptional circumstances. They are not part of normal monetary policy operations, but they are part of the toolkit because their availability changes how the financial system behaves. The principle, articulated by Walter Bagehot in 1873, is to lend freely against good collateral at a penalty rate to solvent but illiquid banks. Every modern emergency lending programme traces its design back to this rule.

Three episodes show the function in action. In 2008, the Federal Reserve created the Term Auction Facility, the Primary Dealer Credit Facility, and the Term Asset-Backed Securities Loan Facility, lending over USD 1 trillion at peak through these and the discount window combined. In March 2020, the Fed reopened these facilities plus new programmes for corporate credit, municipal credit, and main street lending under CARES Act authority. In March 2023, the Bank Term Funding Programme was created in response to the Silicon Valley Bank failure, lending against par-value collateral at one-year terms; outstanding BTFP balances peaked at USD 168 billion in early 2024. The full episode-by-episode account is in our article on central banks as lenders of last resort.

How the Tools Transmit to the Economy

A change in any of the policy instruments works through five transmission channels: the interest rate channel (policy rate moves bank lending rates and bond yields), the credit channel (bank willingness to lend and borrower balance sheets respond to rate changes), the asset price channel (equity and house prices respond to discount rates, generating wealth effects), the exchange rate channel (higher domestic rates appreciate the currency), and the expectations channel (credible guidance moves long rates before any action is taken).

The lags are well documented. The full effect of a rate change on output peaks at around 12 to 18 months, and the effect on inflation at around 18 to 24 months. These monetary policy lags are why central banks must act on inflation forecasts rather than current data. The 2022 to 2023 tightening cycle illustrates this: the Fed raised its target by 525 basis points over 16 months, and the full effect on US inflation was visible only by late 2024.

The Limits of the Toolkit

Three constraints shape what the toolkit can and cannot do. The first is the zero lower bound. Once the policy rate approaches zero, further conventional cuts are limited because households and firms can hold cash at zero return. The ECB, the Swiss National Bank, and the Bank of Japan all experimented with negative interest rates between 2014 and 2024, but the evidence suggests that the practical floor lies modestly below zero rather than at zero exactly.

The second is the trade-off between inflation and output. Rate cuts stimulate output but raise inflation. Rate increases cool inflation but reduce output. The Taylor principle, that policy rates should move more than one-for-one with inflation, ensures the trade-off is resolved in favour of price stability over the medium term. But in the short term every rate decision involves choosing where on the trade-off frontier to operate.

The third is the relationship with fiscal policy. Large fiscal deficits can constrain monetary policy by raising the risk that disinflation requires unacceptably high real rates. This concern, formalised in the literature on “fiscal dominance”, has gained renewed attention as advanced-economy government debt has risen to levels last seen after World War II. The political pressure on central banks during the 2025 to 2026 Fed transition, documented in our article on threats to central bank independence, shows that this constraint is now an operational rather than theoretical concern.

MASEconomics Explains

Four economic concepts behind the policy toolkit

These concepts are explored in depth across our educational articles library.

Explore the MASEconomics BlogConclusion

Monetary policy tools form an integrated operating framework rather than a list of independent instruments. The policy rate is the anchor. Administered rates and standing facilities create the corridor that keeps the market overnight rate close to the target. Open market operations adjust the size of the balance sheet and the quantity of reserves. Reserve requirements set a regulatory minimum that is largely inactive in advanced economies. Asset purchases and forward guidance extend the toolkit when the policy rate is constrained by the zero lower bound. Lender of last resort operations sit alongside the standard toolkit for exceptional circumstances. The Federal Reserve, the European Central Bank, the Bank of England, and the Bank of Japan all run versions of the same framework, with operational differences that matter for how policy actually transmits to credit, asset prices, and the real economy.

Frequently Asked Questions

What are the main tools of monetary policy?

The six core tools are administered rates (such as interest on reserves), open market operations, standing facilities (lending and deposit windows), reserve requirements, large-scale asset purchases (quantitative easing), and forward guidance. Modern central banks use these instruments together within a single operating framework rather than as independent levers.

How do open market operations work?

Open market operations are purchases and sales of government securities by the central bank, either outright or under repurchase agreements. They adjust the quantity of bank reserves and, in scarce-reserve regimes, steer the overnight interest rate. In ample-reserve regimes, they are used to manage the size of the balance sheet over time rather than to control the daily policy rate.

What is the difference between expansionary and contractionary monetary policy?

Expansionary policy lowers interest rates, expands the central bank balance sheet, or both, to raise aggregate demand. Contractionary policy raises rates or shrinks the balance sheet to cool the economy and bring inflation down. The Taylor principle prescribes that policy rates should move more than one-for-one with inflation, ensuring that real rates rise when inflation rises.

Why have reserve requirements become less important?

Reserve requirements have lost prominence in advanced economies because the move to ample-reserve operating regimes made them redundant. Commercial banks now hold reserves far in excess of any regulatory minimum, so changing the minimum has little practical effect. The People’s Bank of China remains the major exception, actively using its required reserve ratio as a primary policy instrument.

What is forward guidance and why do central banks use it?

Forward guidance is the use of communication about the future path of the policy rate to shape market expectations. Because long-term interest rates depend on expectations of future short rates, the central bank can move long yields directly through statements rather than indirectly through actions. The Federal Reserve, the ECB, the Bank of England, and the Bank of Japan all use forward guidance as a standing part of the toolkit.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics