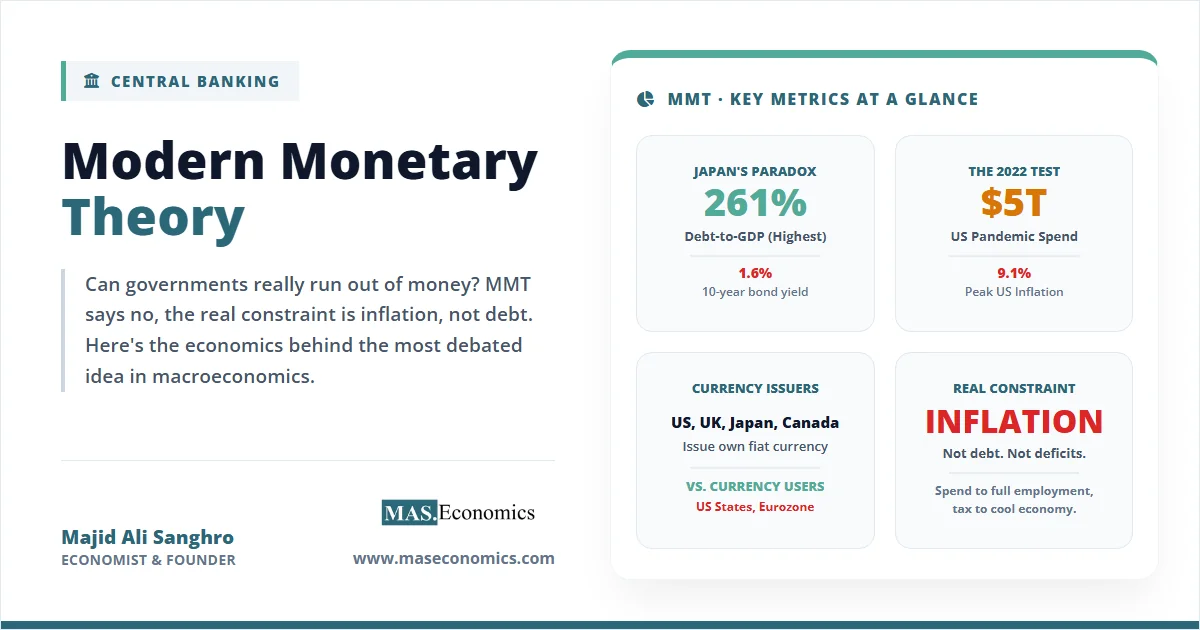

In March 2020, the United States government authorised $2.2 trillion in emergency pandemic spending. Over the following 18 months, that figure grew to more than $5 trillion, pushing federal debt from 79% of GDP to nearly 100%. Under conventional economic logic, this should have produced either a sovereign debt crisis or a fiscal emergency that forced sharp cuts in public services. Neither happened. Treasury yields remained historically low, the US continued to borrow at nominal rates under 2%, and the government’s ability to spend was not constrained by any market-imposed ceiling on debt. Critics called it reckless. Supporters called it overdue. A small but influential school of economists called it vindication: Modern Monetary Theory, or MMT, had predicted exactly this outcome.

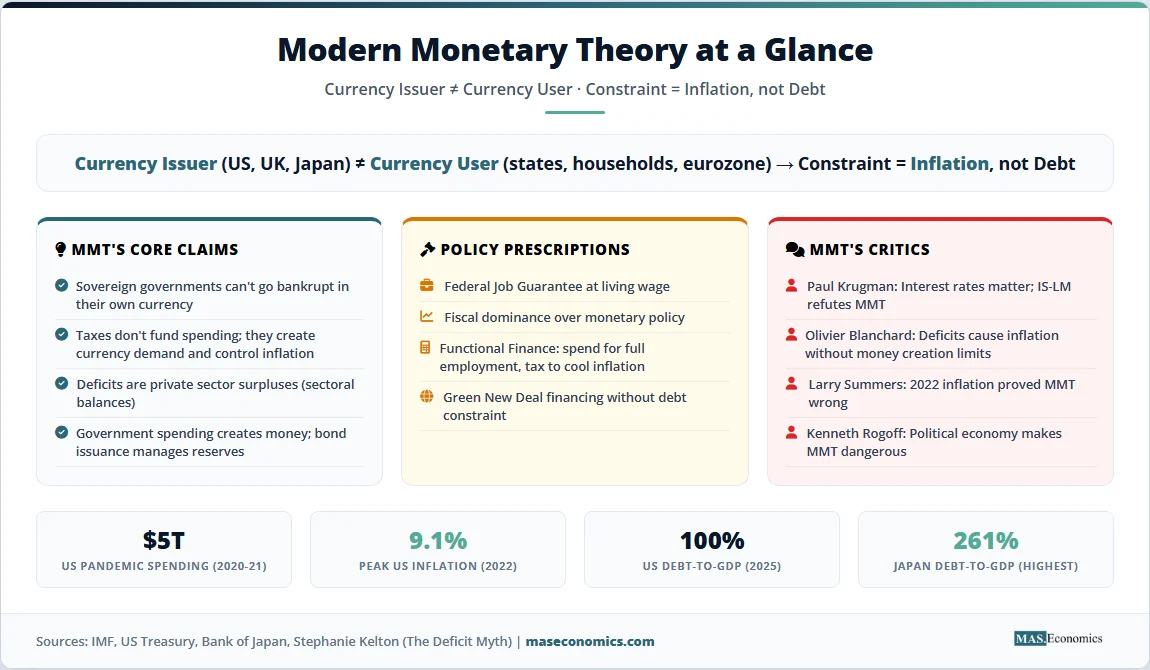

Modern Monetary Theory explained in a single sentence: a government that issues its own fiat currency cannot go bankrupt in that currency, so the real constraint on public spending is not the deficit or debt level but inflation. This deceptively simple claim, advanced most prominently by Stephanie Kelton of Stony Brook University in her New York Times bestseller The Deficit Myth (2020), has sparked the most consequential macroeconomic debate of the 2020s. It pits heterodox economists against mainstream Nobel laureates like Paul Krugman and Olivier Blanchard, divides progressives from fiscal conservatives, and directly challenges the institutional foundation of central banking itself. When the 2022 global inflation surge drove consumer prices up 9.1% in the United States and 11.1% in the United Kingdom, MMT’s critics declared the theory falsified. Its supporters argued the opposite: that inflation was the binding constraint all along, and MMT was the only framework that had identified it correctly.

Currency Issuers Cannot Go Bankrupt

The foundational insight of MMT rests on a distinction that most economic discourse ignores: the difference between a currency issuer and a currency user. Households, businesses, and US states are currency users. They must acquire dollars before they can spend them. They can run out of money. They can go bankrupt. The US federal government, by contrast, is a currency issuer. It creates the dollars the rest of the economy uses. It cannot, in any operational sense, run out of dollars.

This insight is not controversial among central bankers. As former Fed Chair Ben Bernanke explained on 60 Minutes in 2009, when asked whether the Fed was spending tax money to rescue banks during the financial crisis: “It’s not tax money. The banks have accounts with the Fed, and we simply use the computer to mark up the size of the account.” The same mechanism applies to all government spending. When Congress authorises payments, the Federal Reserve credits the accounts of recipients. New money is created in the process. There is no warehouse of pre-existing dollars that must be collected through taxes before they can be spent.

MMT draws a radical conclusion from this operational reality: the sequence in which we typically describe government finance, tax first, then spend, or borrow first, then spend, is backwards. Spending comes first. Taxation and bond issuance are not funding operations. They are monetary management operations that drain reserves from the banking system to prevent inflation and to maintain demand for the currency.

Stephanie Kelton’s formulation is stark: “The entire national debt could be paid off tomorrow, and none of us would have to chip in a dime.” The Federal Reserve could simply credit the accounts of Treasury bondholders and mark the debt satisfied. The constraint is not financial. It is what MMT places at the centre of its analysis: real resources and inflation.

The Inflation Constraint

MMT does not argue that governments can spend infinitely without consequence. The theory places inflation as the binding constraint on fiscal policy. Once an economy’s real resources (labour, capital, raw materials, productive capacity) are fully utilised, additional government spending bids against existing private demand for those same resources, driving up prices.

This is a point MMT economists have argued they emphasise more, not less, than mainstream economists. In Kelton’s words: “No school of macroeconomic thought treats inflation more seriously than MMT. We place it at the centre of the analytic framework. Inflation is the binding constraint.”

The practical implication is that the deficit size should be determined by the output gap between actual and potential GDP. When the economy is operating below capacity, as during the 2009 to 2019 period or in the immediate aftermath of the pandemic, deficits are not only safe but desirable. They employ idle resources and generate real economic output. When the economy approaches full capacity, deficits must contract, either through reduced spending, higher taxes, or some combination of both.

This framework inverts the standard policy hierarchy. In orthodox macroeconomics, monetary policy is the primary tool for managing inflation: central banks raise rates when prices rise too fast and cut rates when demand is insufficient. MMT dismisses this approach. Kelton describes monetary policy as “a sideshow” and argues that interest rate adjustments have small, lagged, and often contradictory effects on inflation. In MMT’s framework, the primary anti-inflation tool is fiscal policy: raising taxes to withdraw spending power from the private sector when the economy overheats.

Taxes

MMT’s treatment of taxation is one of its most counterintuitive elements. In the standard view, taxes fund government spending. In MMT, the causation runs the other way: government spending creates the money that is later collected as taxes.

But if taxes do not fund spending, why tax at all? MMT identifies four distinct functions of taxation:

1. Creating demand for the currency. When the government requires taxes to be paid in its currency, it creates a baseline demand for that currency across the entire population. Everyone needs dollars to settle their tax obligations. This is why sovereign currencies have value: not because they are backed by gold, but because they are required to extinguish tax liabilities.

2. Controlling inflation. Taxes withdraw spending power from the private sector. When the economy approaches full capacity, raising taxes reduces aggregate demand and releases real resources for government use without generating price pressure.

3. Redistributing wealth. Progressive taxation reduces inequality by transferring resources from those with high spending capacity to those with lower spending capacity, with different consumption patterns.

4. Discouraging certain behaviours. Pigouvian taxes on pollution, tobacco, or financial speculation correct market failures and shift incentives toward socially desirable outcomes.

None of these functions requires that tax revenue “pay for” spending. The purpose of taxation is to shape the economy, not to finance the government.

| Concept | Orthodox View | MMT View |

|---|---|---|

| Government funding | Taxes and borrowing fund spending | Spending creates money; taxes drain it |

| Deficit constraint | Debt-to-GDP ratios limit borrowing | Inflation is the only real constraint |

| Primary stabilisation tool | Monetary policy (interest rates) | Fiscal policy (spending and taxation) |

| Full employment | Market forces + monetary policy | Federal Job Guarantee |

| Purpose of taxes | Revenue for government | Create currency demand; manage inflation |

| Purpose of bonds | Finance deficits | Monetary policy tool for reserve management |

| National debt | A burden on future generations | Private sector savings in the currency |

|

||

The Job Guarantee

MMT’s most concrete policy prescription is the Federal Job Guarantee (JG), a programme in which the federal government would offer a living-wage job to anyone willing and able to work, at a fixed wage set by the government. Proponents argue this would serve three purposes simultaneously: eliminate involuntary unemployment, create a price anchor for the economy, and function as an automatic stabiliser.

The automatic stabiliser logic is central. In a recession, private employers lay off workers. Under the Job Guarantee, these workers move into the JG programme, maintaining their incomes and preventing the collapse in aggregate demand that deepens recessions. When the private economy recovers, employers poach workers back from the JG programme by offering higher wages. The JG workforce shrinks automatically. This mechanism, MMT economists argue, would do for unemployment what existing automatic stabilisers (unemployment insurance, food stamps) do incompletely.

Pavlina Tcherneva, a leading MMT economist, has calculated that a Job Guarantee at $15 per hour could be implemented for approximately 1 to 2% of GDP, significantly less than the cost of recessions in foregone output. Critics, however, question the administrative feasibility. Could the federal government actually provide meaningful, productive work for 10 to 15 million workers during a severe recession? What kind of jobs? Would the programme simply be make-work, crowding out private employment without generating real value?

The Academic Debate

MMT’s rise has been met with sustained resistance from mainstream economists, including several Nobel laureates. The criticisms fall into three broad categories.

1. The Interest Rate Critique (Krugman)

Paul Krugman has argued that MMT ignores the role of interest rates in reconciling different deficit levels with full employment. In his formulation, the IS-LM framework implies that for any level of fiscal policy, a corresponding interest rate exists that achieves full employment. Monetary policy can substitute for fiscal policy across a wide range.

MMT’s response, articulated by Kelton in her direct exchange with Krugman, is that interest rates are far less effective than Krugman assumes. Multiple Fed and BoE studies find that interest rates have a small effect on private investment decisions, which are driven primarily by profit expectations. Further, MMT argues that cutting rates can actually be contractionary in some contexts because it reduces government interest payments (which flow primarily to wealthy bondholders) and reduces interest income for retirees and savers.

2. The Inflation Critique (Blanchard, Summers)

Olivier Blanchard, former IMF chief economist, has acknowledged MMT’s technical accuracy about the mechanics of money creation but rejected its policy implications. In Blanchard’s view: “The deficit, unless very small, cannot be fully financed through non-interest-bearing money creation, without leading to high or hyperinflation.”

Larry Summers has been more pointed. In 2021, he warned that the American Rescue Plan’s $1.9 trillion in additional spending, combined with existing pandemic support, would drive inflation to levels “we have not seen in a generation.” When US inflation hit 9.1% in 2022, Summers’ prediction was widely seen as vindicated. MMT critics argued that this proved the deficit does matter, and that the theory’s framework had led to dangerous over-stimulation.

MMT economists dispute this interpretation. Bill Mitchell and other MMT scholars have argued that the 2022 inflation was primarily supply-side (energy shocks from the Ukraine war, supply chain disruptions from COVID, corporate pricing power) rather than demand-driven. In their view, the inflation was consistent with MMT’s framework: it emerged precisely when real resource constraints became binding, not when the deficit crossed some arbitrary debt threshold.

3. The Institutional Critique (Cochrane, Rogoff)

John Cochrane of the Hoover Institution has argued that MMT’s theoretical foundations are incoherent and its policy prescriptions dangerous. In his review of The Deficit Myth, he wrote that “her implications don’t lead to her desired conclusions” and that MMT lacks formal models with explicit equilibrium conditions that would allow it to be tested against alternatives.

Kenneth Rogoff, co-author of This Time is Different, has argued that MMT underestimates the political economy of fiscal policy. Even if sovereign governments can technically print money to pay debts, doing so would destroy the independence of central banks, undermine the credibility of inflation expectations, and trigger currency crises as investors lose confidence in the currency’s long-term value. The historical record of hyperinflation in Weimar Germany, Zimbabwe, and Venezuela illustrates where MMT’s logic can lead when institutional constraints break down.

The Japan Case Study: MMT’s Best Evidence

Japan presents what MMT proponents consider the strongest real-world evidence for their framework. Japan has run large fiscal deficits for three decades, accumulated a debt-to-GDP ratio of approximately 261% (the highest in the developed world), and financed large portions of that debt through Bank of Japan purchases. Under conventional economic logic, Japan should have experienced a debt crisis, currency collapse, or hyperinflation long ago. None of these has occurred.

Instead, Japan’s persistent problem has been the opposite: inflation has remained stubbornly below the BoJ’s 2% target for most of the past 30 years, often flirting with outright deflation. Japanese government bond yields have remained among the lowest in the world. The yen has fluctuated but not collapsed.

MMT economists cite Japan as evidence that the debt-to-GDP threshold models (such as Reinhart and Rogoff’s famous “90% threshold” that sparked controversy when errors in their dataset were revealed) have no empirical basis. A currency-issuing government with strong institutions can sustain debt levels far higher than orthodox economics predicts.

Critics offer alternative explanations. Japan’s high savings rate means domestic investors voluntarily hold government bonds. Japan’s declining population and demographic structure have suppressed aggregate demand, creating an unusually large output gap. Japan’s external trade position (historically a current account surplus) supports the yen. None of these conditions translates automatically to other economies. The US, UK, and eurozone face demographic, trade, and savings patterns very different from Japan’s.

The 2022 Inflation Test

The most important empirical test of MMT to date came with the post-pandemic inflation surge. Between March 2020 and December 2021, the US Treasury borrowed, and the Federal Reserve effectively monetised more than $5 trillion in pandemic-related spending. In 2022, US inflation reached 9.1%, the UK reached 11.1%, and the eurozone inflation reached 10.6%.

Critics seized on this as a falsification of MMT. If deficit spending did not matter, why had prices surged? The argument became particularly sharp because several prominent MMT advocates had endorsed aggressive pandemic-era fiscal support and dismissed inflation warnings.

MMT economists responded with three arguments. First, the inflation was substantially supply-driven, caused by energy shocks, supply chain disruptions, and the war in Ukraine, all of which would have raised prices regardless of fiscal policy. Second, inflation behaved exactly as MMT predicted: it emerged only when real resource constraints became binding (labour shortages, supply chain bottlenecks, capacity utilisation at historic highs). Third, the solution prescribed by orthodox policy (aggressive rate hikes by the Fed from 0.25% to 5.50% in 18 months) imposed high costs, including a banking crisis in early 2023 and elevated unemployment risk, which MMT argued could have been addressed more effectively through fiscal tightening.

The post-pandemic inflation debate remains unresolved. What is clear is that the simple version of MMT (“deficits don’t matter”) is untenable. The more sophisticated version (“deficits matter to the extent they generate inflation at full employment”) is harder to reject but also harder to distinguish operationally from mainstream Keynesian economics.

Monetary Sovereignty

MMT is explicit that its framework applies only to countries with full monetary sovereignty. Kelton, Wray, and other MMT scholars recognise a spectrum:

Full monetary sovereignty: The United States, United Kingdom, Japan, Canada, Australia, and a handful of others. These countries issue their own floating currencies, do not peg to another currency, and do not borrow significantly in foreign currencies. MMT’s framework applies most fully here.

Limited monetary sovereignty: Eurozone member states. Individual countries like France, Italy, or Spain do not control the euro. They are effectively currency users of a currency issued by the European Central Bank. Their fiscal constraints resemble those of US states more than those of sovereign currency issuers. This is why the eurozone sovereign debt crisis of 2010 to 2012 was possible: Greece, Ireland, Portugal, and Spain faced genuine solvency risks because they could not print euros.

Constrained monetary sovereignty: Emerging economies with significant foreign currency debt or fixed exchange rates. Argentina, Turkey, and Venezuela fall in this category. For these countries, MMT’s framework does not apply because they owe debts denominated in currencies they cannot create. Their policy space is fundamentally different.

This nuance is frequently lost in public discussions of MMT. Critics sometimes cite Zimbabwe or Weimar Germany as evidence that MMT fails. MMT proponents respond that both cases involved economies with severe supply-side collapses, foreign-denominated debts, or both, precisely the conditions under which the theory does not apply.

MMT and Central Bank Independence

MMT poses a direct challenge to the principle of central bank independence, which has dominated macroeconomic governance for four decades. In the orthodox framework, independent central banks are essential because democratically elected politicians face irresistible short-term incentives to overstimulate the economy before elections.

MMT inverts this logic. Kelton and Mitchell argue that democratically accountable fiscal policy should be the primary stabilisation tool, with the central bank playing a subordinate role in managing the payment system and reserve levels. In MMT’s framework, the distinction between fiscal and monetary policy largely collapses. Spending, taxation, and money creation are all aspects of a unified “functional finance” approach oriented toward full employment and price stability.

This position has made MMT particularly controversial among central bankers. The ECB, the Bank of England, and the Federal Reserve have all publicly rejected MMT’s policy prescriptions. Former ECB chief economist Otmar Issing called MMT “a dangerous idea.” The concern is not merely theoretical. If governments come to believe that central banks must accommodate fiscal policy, the credibility that anchors inflation expectations dissolves. The result, critics argue, is not the utopia MMT envisions but the Turkish experience: policy distortion, currency collapse, and eventual forced U-turns at extreme cost.

Source: IMF World Economic Outlook (October 2025), Japan Ministry of Finance, Eurostat, US Treasury, Bank of England | MASEconomics.com

The chart illustrates MMT’s central empirical puzzle: Japan, with the world’s highest debt-to-GDP ratio at 261%, pays the lowest 10-year bond yield at just 1.6%. The United States, with debt at 100% of GDP, pays 4.1%. Germany, with a debt of only 64% of GDP, pays 2.5%. The relationship between debt levels and borrowing costs is far weaker than conventional economics predicts, particularly for countries with full monetary sovereignty. This is the evidence MMT uses to argue that the market does not impose a strict debt ceiling on sovereign currency issuers.

Where Orthodox Economics Has Moved Toward MMT

Despite the intensity of the debate, significant elements of MMT have quietly become mainstream. The proposition that sovereign governments issuing their own currencies face different constraints than households is now widely accepted. Even Paul Krugman, one of MMT’s sharpest critics, has acknowledged that the US faces no “bond vigilantes” who will force a debt crisis at a specific debt threshold.

The extensive use of quantitative easing by major central banks since 2008 has operationally demonstrated MMT’s claim that central banks can absorb arbitrary quantities of government debt without triggering immediate inflation. The Bank of England holds government bonds equal to roughly 30% of GDP. The Bank of Japan holds more than 50%. The ECB holds approximately 35% of eurozone government debt. In each case, governments effectively finance large portions of spending through central bank money creation without the hyperinflation MMT’s critics predict.

Mainstream economists have also shifted on the output gap question. Blanchard, Summers, and Jason Furman have argued that potential GDP should be measured more flexibly, and that the “Phillips curve” relationship between unemployment and inflation is flatter than previously believed. Both positions move closer to MMT’s framework, even if these economists reject the MMT label.

The 2020 to 2021 pandemic response involved unprecedented fiscal-monetary coordination that violated traditional separation principles. The Treasury issued bonds that the Fed then purchased, effectively monetising deficit spending on a scale MMT had long advocated. Whether this represented de facto MMT or simply emergency policy is contested, but the operational reality aligned with MMT’s description of how sovereign finance actually works.

MMT’s Political Economy Problem

The strongest argument against MMT is not theoretical but institutional. Even if MMT’s operational description of money creation is accurate, the framework removes the institutional guardrails that have, historically, prevented governments from over-relying on inflation finance.

The Federal Reserve’s independence, the ECB’s treaty protections, and the Bank of England’s operational autonomy all serve as commitment devices. They make it credible that central banks will resist political pressure to accommodate excessive deficits. This credibility is what anchors inflation expectations at 2%. If MMT’s framework replaces central bank independence with democratically accountable fiscal dominance, this credibility dissolves.

The historical record is not encouraging. Governments with unconstrained ability to finance deficits through money creation have, repeatedly, abused that power: Germany in 1923, Zimbabwe in the 2000s, Venezuela in the 2010s, Argentina through much of its modern history. MMT proponents argue these are cases of constrained monetary sovereignty (foreign debt, supply collapse) rather than MMT in action. Critics respond that the political temptation to finance popular spending with money creation is universal, and the institutional constraints MMT would remove exist precisely because this temptation must be resisted.

MASEconomics Explains

Four concepts behind Modern Monetary Theory

Monetary Sovereignty

The ability of a government to issue its own fiat currency, allow it to float freely, and avoid borrowing in foreign currencies. Countries with full monetary sovereignty (US, UK, Japan, Canada, Australia) can theoretically never be forced into default on currency-denominated debt. Eurozone members and emerging economies with dollar debt lack this flexibility.

Functional Finance

Abba Lerner’s 1943 principle that fiscal policy should be judged by its effects on employment and inflation rather than by arbitrary financial metrics like deficit-to-GDP ratios. MMT builds on this foundation, arguing that governments should spend what is needed to achieve full employment and raise taxes when inflation threatens, regardless of the resulting deficit.

Sectoral Balances

The accounting identity that (Government Deficit) = (Private Sector Surplus) + (Current Account Deficit). Wynne Godley’s framework, which MMT incorporates, shows that a government surplus must come at the cost of private sector deficits or trade imbalances. This is why deficit reduction in a weak economy typically produces recession.

Job Guarantee

MMT’s signature policy: a federal programme offering a living-wage job to anyone willing and able to work. Designed to eliminate involuntary unemployment, serve as an automatic stabiliser during recessions, and anchor wages at a socially acceptable floor. The JG buffer stock would expand in downturns and contract when private employers poach workers.

Conclusion

Modern Monetary Theory, explained as a complete framework, represents the most significant heterodox challenge to mainstream macroeconomics in four decades. Its core insight, that currency-issuing governments face inflation rather than solvency as the binding constraint on spending, is operationally accurate and increasingly accepted even by its critics. Its policy prescriptions, particularly the Federal Job Guarantee and the subordination of monetary policy to fiscal policy, remain deeply contested and have not been adopted by any major economy.

The 2020 to 2022 experience provided the closest thing to a real-world test MMT has received. The expansion of fiscal and monetary policy during the pandemic operated closer to MMT’s framework than any period in modern history. Inflation surged to 9.1% in the US and over 11% in the UK, and the subsequent correction required aggressive rate hikes that MMT’s framework did not cleanly predict. Whether this represents falsification of MMT or confirmation that inflation is indeed the binding constraint remains an active scholarly debate.

What is beyond dispute is that MMT has permanently changed the terms of debate about fiscal policy, central banking, and sovereign debt. The Japanese case, with 261% debt-to-GDP and 1.6% bond yields, cannot be explained by orthodox models that predict debt crises at much lower thresholds. The coexistence of massive central bank balance sheets and stable inflation expectations for most of the 2010s undermined the simple monetarist view that money creation mechanically produces inflation. The sectoral balances framework has been quietly absorbed into mainstream analysis without the MMT label.

Whether MMT ultimately prevails as the dominant framework, fails as a failed experiment, or persists as a useful corrective to orthodox dogma depends on how the next decade of fiscal and monetary policy unfolds. What seems certain is that the question “can governments really run out of money?” now has a more complex answer than either the traditional affirmative or MMT’s categorical negative. The answer depends on monetary sovereignty, real resource constraints, institutional credibility, and political economy, precisely the variables MMT insists we examine rather than assume away.

Did you find this article helpful? Share it with someone who loves economics. And remember, at MASEconomics, we make complex ideas simple.