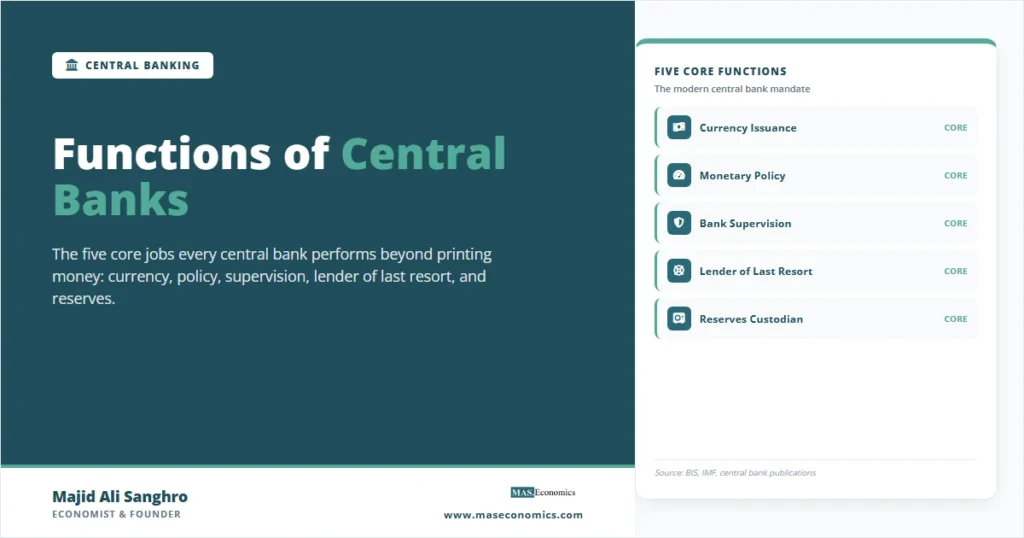

The functions of central banks extend far beyond issuing currency. The Federal Reserve, the European Central Bank, the Bank of England, and every other major central bank perform a defined set of jobs that together hold modern economies together. The Bank for International Settlements identifies five core mandates shared across virtually all major central banks: currency issuance, monetary policy, bank supervision, lender-of-last-resort intervention, and reserves management. A sixth role, payment system operation, sits underneath all of them and processes roughly five times the annual world GDP every year through real-time gross settlement systems.

None of these functions involves a literal printing press doing the heavy lifting. Physical currency is typically less than 10 percent of the money supply in advanced economies. The actual work of a central bank is regulatory, supervisory, and systemic. The rest of this article walks through each function with the institutional detail that distinguishes a working central bank from a textbook description of one.

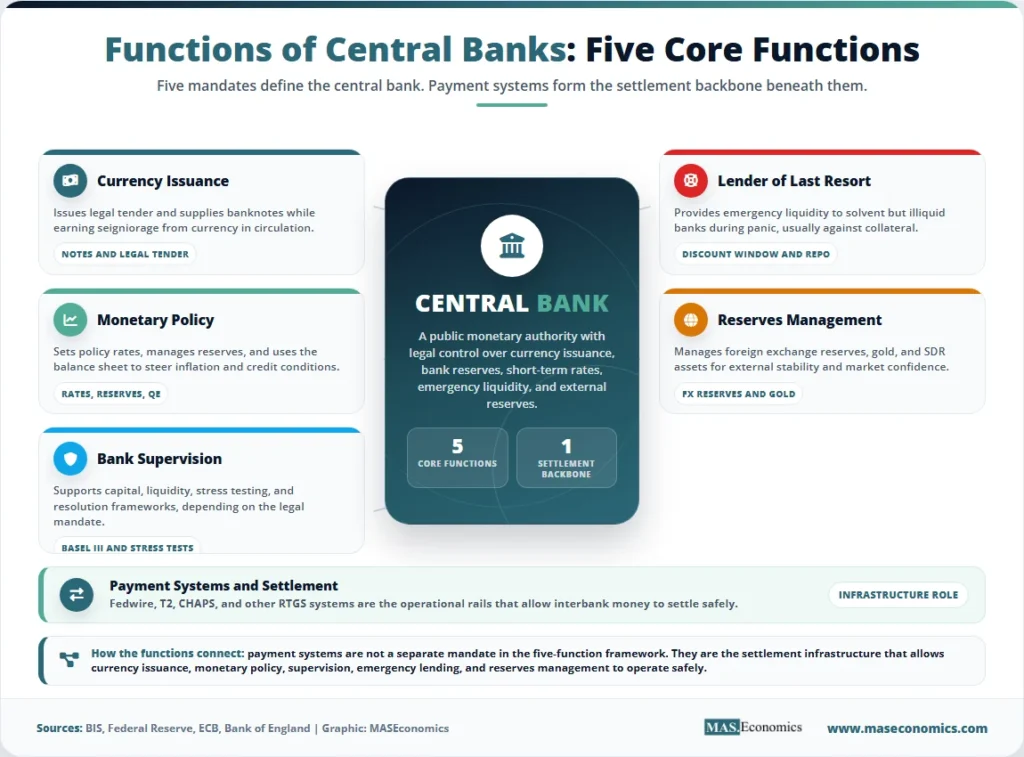

The five-function framework. Currency issuance (monopoly on legal tender). Monetary policy (setting the policy rate and managing the balance sheet). Bank supervision (capital, liquidity, stress tests). Lender of last resort (emergency liquidity to solvent banks against collateral). Reserves management (foreign exchange and gold holdings). A sixth function, payment system operation, runs through all the others.

What Defines a Central Bank

A central bank is a public institution with three legally protected privileges: monopoly issuance of the national currency, the right to hold the reserve accounts of commercial banks, and operational authority over short-term interest rates. Those three privileges separate a central bank from any other financial institution, including state-owned commercial banks.

The institution is not profit-driven. Most major central banks generate operating surpluses (from interest on government securities and seigniorage on currency in circulation), but those surpluses are remitted to the Treasury, not paid to shareholders. The Federal Reserve remitted USD 76.1 billion to the US Treasury in 2022 before reporting operating losses in 2023 and 2024 as interest expenses on reserves exceeded interest income on securities. The European Central Bank similarly distributes its profits to euro area national central banks, who then pass them to their finance ministries.

Three institutions appear repeatedly through this article as worked examples: the Federal Reserve (created in 1913, twelve regional Reserve Banks plus a Board of Governors), the European Central Bank (created in 1998 under the Maastricht Treaty), and the Bank of England (chartered in 1694, granted operational independence in 1997). Where the function being discussed differs meaningfully across these three, the article notes the contrast. For a deeper structural comparison, see our companion article on central banking and monetary policy.

Issuance of Currency and the Money Supply

Currency issuance is the most visible function, but the smallest in economic weight. The Federal Reserve issues Federal Reserve Notes, the ECB issues euro banknotes (with the European national central banks minting coins under quota), and the Bank of England issues pound sterling notes (with separate issuing rights held by three Scottish and four Northern Irish commercial banks under historical statutes).

Physical currency is roughly 8 to 12 percent of the broad money supply in advanced economies. The other 88 to 92 percent is bank deposits, created through commercial bank lending and held as electronic entries on bank balance sheets. The central bank does not directly create this larger portion of the money supply. It influences it through the policy rate, reserve requirements, and the supply of bank reserves. The detailed mechanics of how the broader money stock is generated are covered in our article on how central banks create money.

The seigniorage from currency issuance, the difference between the face value of notes and the cost of producing them, accrues to the central bank as interest-free funding. For the Federal Reserve, currency in circulation grew from USD 1.0 trillion in 2010 to USD 2.4 trillion in 2024, a substantial source of revenue that flows back to the Treasury after central bank operating expenses.

Setting Monetary Policy

The most consequential function of a central bank is setting the short-term interest rate. This is what determines the cost of credit across the economy and what gives the central bank leverage over inflation, employment, and the exchange rate. Every major central bank now operates with an explicit inflation target, typically 2 percent, and adjusts the policy rate to keep inflation near that target.

Three operational mechanisms make this work. The first is the administered rate: interest paid on reserves (the Fed’s IORB, the ECB’s deposit facility rate, the Bank of England’s Bank Rate). Since 2008, advanced-economy central banks have moved to “floor systems” in which this administered rate directly sets the market overnight rate. The second is open market operations, the purchases and sales of government securities that adjust the quantity of reserves. The third is standing facilities, the lending and deposit windows that bound the policy corridor. The full toolkit is documented in the monetary policy tools.

Monetary policy is set by a committee, not by an individual. The Federal Open Market Committee has 12 voting members. The ECB Governing Council has 26 members, with 21 voting on a rotating basis. The Bank of England Monetary Policy Committee has 9 members. Decisions are taken by majority vote, and the votes themselves are published shortly after each meeting, which is a meaningful constraint on individual board members because each vote becomes part of the public record. The Taylor Rule remains the most influential benchmark against which committee decisions are compared.

Banker to the Government

Central banks act as the government’s bank in three concrete ways. They hold the Treasury’s operating cash account and process incoming tax receipts and outgoing payments. They serve as the fiscal agent for issuing government debt, running the auctions through which Treasury bills, notes, and bonds are sold to primary dealers. And they manage the government’s foreign exchange operations when required.

The line between banker-to-government and monetary financing of the deficit is policed by statute. The European Central Bank is explicitly prohibited from purchasing government debt in the primary market under Article 123 of the Treaty on the Functioning of the European Union, though it can buy bonds in the secondary market under its asset purchase programmes. The Federal Reserve is similarly barred from directly funding the Treasury and operates only in the secondary market. The Bank of England’s Ways and Means facility, which allowed direct lending to the Treasury, was expanded temporarily during the COVID-19 crisis and then closed.

The line matters because the long-run literature, most notably Sargent and Wallace’s 1981 “unpleasant monetarist arithmetic”, shows that when fiscal authorities issue debt at rates the central bank cannot accommodate, monetary policy eventually loses its grip on inflation. The institutional design of secondary-market-only purchases is what keeps that boundary intact in normal times. The full debate is documented in our coverage of central banks in public debt management.

Custodian of Reserves and Foreign Exchange

Central banks hold and manage their country’s foreign exchange reserves. These reserves provide the buffer that the country can use to defend its exchange rate, settle international obligations, and maintain market confidence. The reserves are typically a mix of US dollars (still 58 percent of allocated global reserves as of late 2025, per IMF COFER data), euros (around 20 percent), Japanese yen, pound sterling, and gold.

The institutional arrangements vary. In the United States, the Treasury technically owns the foreign exchange reserves, but the Federal Reserve operates them on the Treasury’s behalf through the Exchange Stabilization Fund. In the euro area, each national central bank holds its own reserves, with the ECB holding a separate pool transferred from member states. In emerging market economies, foreign reserves are typically large relative to GDP because they serve a defensive function during currency stress. India’s reserves stood at USD 668 billion in early 2026, China’s at USD 3.2 trillion.

The use of reserves involves exchange-control operations in some jurisdictions and direct FX intervention in others. The Swiss National Bank’s accumulation of foreign reserves to defend the EUR/CHF floor from 2011 to 2015 is the canonical example of a developed-economy intervention episode. The 2022 to 2024 yen-defence operations by the Japanese Ministry of Finance, executed by the Bank of Japan, are the canonical recent emerging-market-style intervention by an advanced economy.

The Five Core Functions Compared

The five core functions vary in scope, frequency, and political sensitivity. The table below summarises each one, the operational instrument that delivers it, and one major central bank’s specific implementation.

| Function | Operational instrument | Federal Reserve example | European Central Bank example | Bank of England example |

|---|---|---|---|---|

| Currency issuance | Note issue, payment systems | Federal Reserve Notes, Fedwire | Euro banknotes, TARGET2 / T2 | Pound sterling notes, CHAPS |

| Monetary policy | Policy rate, balance sheet | Fed funds target, IORB, ON RRP | Deposit facility rate (DFR), APP, PEPP | Bank Rate, APF |

| Bank supervision | Capital, liquidity, stress tests | Fed supervision of holding companies (shared with OCC, FDIC) | Single Supervisory Mechanism for euro area significant institutions | Prudential Regulation Authority (PRA, part of BoE) |

| Lender of last resort | Discount window, repo facilities | Discount window primary credit, BTFP (2023) | Marginal Lending Facility, ELA | Discount Window Facility, Indexed Long-Term Repo |

| Reserves management | FX reserves, gold, SDR holdings | Treasury ESF (Fed operates) | National central banks plus ECB pool | BoE manages reserves for HM Treasury |

|

||||

The split between supervision and monetary policy is one of the most variable institutional design choices across countries. The Federal Reserve combines monetary policy with shared supervisory authority. The ECB conducts monetary policy at the eurosystem level but operates supervision through a separate legal pillar (the Single Supervisory Mechanism) covering only banks above defined size thresholds. The Bank of England separates the two functions internally, with the Monetary Policy Committee setting rates and the Prudential Regulation Authority handling supervision under the same institutional roof.

The Lender of Last Resort Role

The most consequential single intervention a central bank ever makes is acting as a lender of last resort. The principle, articulated by Walter Bagehot in his 1873 book Lombard Street, is that during a panic the central bank should lend freely, against good collateral, at a penalty rate, to solvent but illiquid banks. Each clause carries weight: lending freely prevents a panic from spreading, requiring good collateral prevents the bank from socialising losses, and the penalty rate keeps banks from using the facility as a substitute for prudent funding.

The function has been activated repeatedly in modern crises. During the 2007 to 2009 financial crisis, the Federal Reserve extended over USD 1 trillion in emergency liquidity at its peak, through the discount window, the Term Auction Facility, the Primary Dealer Credit Facility, and the swap lines extended to foreign central banks. During the March 2020 COVID stress, the Fed reopened the same facilities plus new ones for corporate and municipal credit. During the March 2023 Silicon Valley Bank failure, the Fed created the Bank Term Funding Programme, lending against par-value collateral at one-year terms to ease bank funding stress. Peak BTFP usage reached USD 168 billion in early 2024.

The function is politically contested because lending against collateral that is impaired (even if the bank is technically solvent) can transfer losses from private creditors to the central bank’s balance sheet, and ultimately to the Treasury. The 2008 rescue of Bear Stearns, where the Federal Reserve Bank of New York took a USD 30 billion non-recourse loan against a portfolio of mortgage-related assets, is the canonical case study. The portfolio was eventually wound down at a modest profit, but the precedent of the central bank taking credit risk for an investment bank remains controversial.

Supervising the Banking System

Bank supervision is the function that consumes the most staff time at most central banks but receives the least public attention. The Federal Reserve has roughly 23,000 employees, of whom over a third work on supervision and regulation. The ECB’s Single Supervisory Mechanism directly supervises 113 “significant” euro area banks holding around 82 percent of total euro area banking assets. The Bank of England’s Prudential Regulation Authority supervises roughly 1,500 firms.

The substance of supervision falls into four categories. First, capital requirements: under Basel III, banks must hold common equity tier 1 capital of at least 4.5 percent of risk-weighted assets, plus a 2.5 percent capital conservation buffer, plus countercyclical and systemic buffers. Second, liquidity requirements: the liquidity coverage ratio (LCR) requires banks to hold high-quality liquid assets sufficient to survive a 30-day stress scenario; the net stable funding ratio (NSFR) requires a minimum proportion of stable long-term funding. Third, stress testing: annual exercises (the Fed’s CCAR, the ECB’s EU-wide stress test) that simulate adverse macroeconomic scenarios and assess whether banks would remain adequately capitalised. Fourth, resolution planning: the “living wills” that document how a failing bank would be wound down without public funds.

The supervisory function is the central mechanism through which the lessons of 2008 were operationalised. Pre-2008, capital requirements were lower, liquidity rules were nonexistent at the international level, and stress tests were not systematic. The Basel III framework, agreed in 2010 and phased in through 2019, represents the largest single tightening of banking supervision in the post-Bretton Woods period. The accountability and transparency framework around supervision has tightened in parallel.

Payment Systems and Settlement

Underneath every other function sits the payment system. The Federal Reserve operates Fedwire (large-value gross settlement) and FedNow (the retail real-time payment system launched in 2023). The ECB and the eurosystem national central banks operate TARGET2 (transitioned to T2 in 2023), settling roughly EUR 2.5 trillion daily. The Bank of England operates CHAPS for large-value sterling payments, settling around GBP 360 billion daily.

These systems are not commercially neutral. They are run by the central bank because the alternative, private operation, would create systemic risk concentrated in the operator. A failure at a privately operated payment hub would propagate through the financial system in ways that the central bank cannot fully insure against. By operating the payment infrastructure itself, the central bank ensures that interbank settlement remains operational even during periods of acute stress, and that the rules governing settlement are set by a public authority rather than negotiated between counterparties.

The frontier in payment systems is the design of central bank digital currency. The 2024 BIS survey of central banks reported 134 jurisdictions exploring CBDCs, 44 running pilots, and three with launched retail systems (the Bahamas, Jamaica, and Nigeria). The People’s Bank of China’s e-CNY has the largest population reach with active retail pilots in over 25 cities. The ECB has approved a digital euro preparation phase; the Federal Reserve is researching wholesale applications without committing to a retail launch. This expanded role connects to the broader future-of-money discussion in central banks in the digital age.

Economic Data Collection and Research

Central banks are major statistical authorities. The Federal Reserve produces the H.15 release on interest rates, the H.6 release on monetary aggregates, the G.17 release on industrial production, the Z.1 release on financial accounts, and the quarterly Survey of Consumer Finances. The European Central Bank produces the Statistical Data Warehouse, the Euro Area Bank Lending Survey, and the consumer expectations survey. The Bank of England produces money and credit statistics, the Decision Maker Panel survey, and the financial stability indicators.

This data role is integral to the policy function. Modern monetary policy cannot be conducted without reliable, high-frequency data on credit conditions, bank balance sheets, inflation expectations, and labour markets. The central bank both consumes this data and produces large portions of it, which gives the policy committee an information advantage that private analysts cannot fully replicate. The associated monetary transmission mechanism research published by central bank economists is among the most cited applied macroeconomics works in the field.

Why These Functions Cannot Be Separated

One persistent question in institutional design is whether the five functions can be split across separate agencies. The 2010 Dodd-Frank Act in the United States debated separating bank supervision from monetary policy. The Wallace Commission in Australia separated supervision (to APRA) from monetary policy (RBA) in 1998. The UK separated supervision (to the FSA) from monetary policy (BoE) in 1997, then reunified them at the BoE in 2013 after the 2008 crisis exposed coordination failures.

The economic case for keeping the functions together rests on information complementarities. The supervisory function generates real-time information about bank balance sheets, lending conditions, and counterparty stress that is directly relevant to monetary policy decisions. The lender of last resort function requires supervisory information to distinguish solvent-but-illiquid banks (which should receive support) from insolvent banks (which should not). The 2008 to 2010 experience of regulators failing to share information with central banks, particularly in jurisdictions where the functions were separated, contributed to the consolidation movement that followed.

The opposing argument is that combining bank supervision with monetary policy can create conflicts of interest. A central bank that is also a supervisor may be reluctant to raise rates aggressively if doing so would impair the balance sheets of banks it regulates. Empirical evidence on whether this conflict is real or theoretical remains contested. The independence framework is what most jurisdictions rely on to manage the tension.

The Frontier Challenges

The functions of central banks are not static. Three challenges are reshaping the institutional perimeter in 2026.

The first is the climate question. The Network for Greening the Financial System, founded in 2017, now includes 138 central banks and supervisors. The ECB has tilted its corporate bond purchases toward issuers with lower carbon footprints. The Bank of England has run climate stress tests on the largest UK banks. The Federal Reserve has been more cautious, framing climate involvement as financial stability rather than monetary policy work. Whether climate risk belongs inside the supervisory function is now a live institutional question rather than a hypothetical one.

The second is the digital currency design choice. A retail CBDC would extend the central bank’s currency-issuance function from physical notes to electronic accounts held directly by the public, bypassing commercial bank deposits. The implications for commercial bank funding, payment system competition, and monetary policy transmission are substantial. The institutional choices being made now will shape the function for decades.

The third is the boundary with fiscal policy. Post-2008 and post-COVID balance sheet expansions have left central banks holding large stocks of government debt. The Bank of Japan owns over half the JGB market. The Federal Reserve’s holdings of Treasury securities and agency MBS peaked at USD 8.5 trillion in 2022. When the central bank is the largest single holder of government debt, the line between debt management and monetary policy blurs. The literature on fiscal dominance and recent episodes of quantitative tightening are testing where the boundary will eventually settle.

MASEconomics Explains

Four economic concepts behind central bank functions

These concepts are explored in depth across our educational articles library.

Explore the MASEconomics BlogConclusion

The functions of central banks form an integrated system that holds modern monetary economies together. Currency issuance gives the institution its visible authority. Monetary policy gives it economic leverage. Bank supervision gives it regulatory authority over commercial banks. The lender of last resort role gives it the ability to stabilise the financial system during stress. Reserves management gives it the buffer to defend the currency and meet international obligations. Payment system operation runs beneath all of these, ensuring that the day-to-day plumbing of the economy works. The five functions cannot be cleanly separated because the information flows between them are what make each one effective. The frontier debates over climate, digital currency, and the boundary with fiscal policy are now reshaping a framework that took shape across the late twentieth century.

Frequently Asked Questions

What are the main functions of a central bank?

The main functions of a central bank are issuing currency, conducting monetary policy, supervising the banking system, acting as lender of last resort, managing foreign exchange reserves, and operating the payment system. Together these six functions cover the institutional perimeter that defines a modern central bank.

Why is a central bank called the lender of last resort?

A central bank is called the lender of last resort because it lends to commercial banks when no private lender will. The principle, formalised by Walter Bagehot in 1873, is to lend freely against good collateral at a penalty rate to banks that are solvent but temporarily illiquid. This prevents a liquidity shortage at one institution from spreading into a system-wide panic.

How does a central bank differ from a commercial bank?

A central bank is a public institution with a monopoly on currency issuance, a mandate to manage monetary policy, and authority to supervise other banks. It does not take retail deposits, does not lend to the public, and is not profit-driven. A commercial bank takes deposits from the public, makes loans, and operates for profit under the supervision of the central bank.

Do central banks really print money?

Central banks do issue physical currency, but currency is only 8 to 12 percent of the broad money supply in advanced economies. Most money is created through commercial bank lending and exists as electronic deposits, not paper notes. When commentators say a central bank is “printing money” during quantitative easing, they usually mean it is creating bank reserves to purchase government bonds, not literally producing more banknotes.

Who supervises central banks themselves?

Central banks are accountable to the legislature that created them. In the United States, the Federal Reserve reports to Congress and the Chair testifies semi-annually. The European Central Bank reports to the European Parliament. The Bank of England reports to Parliament through the Treasury Committee. They are operationally independent in setting interest rates but subject to oversight on mandate compliance, financial accounts, and policy outcomes.

Thanks for reading! If you found this helpful, share it with friends and spread the knowledge. Happy learning with MASEconomics